- Non-food Packaging

- Returnable Transport Packaging Market

Returnable Transport Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Returnable Transport Packaging Market by Product Type (Intermediate Bulk Containers (IBCs), Pallets, Crates & Totes, Drums & Barrels, Others), Material Type (Plastic, Metal, Wood, Miscellaneous), Application (Food & Beverages, Pharmaceuticals & Healthcare, Automotive & Industrial, Others) and Regional Analysis for 2025 - 2032

Returnable Transport Packaging Market Size and Trends Analysis

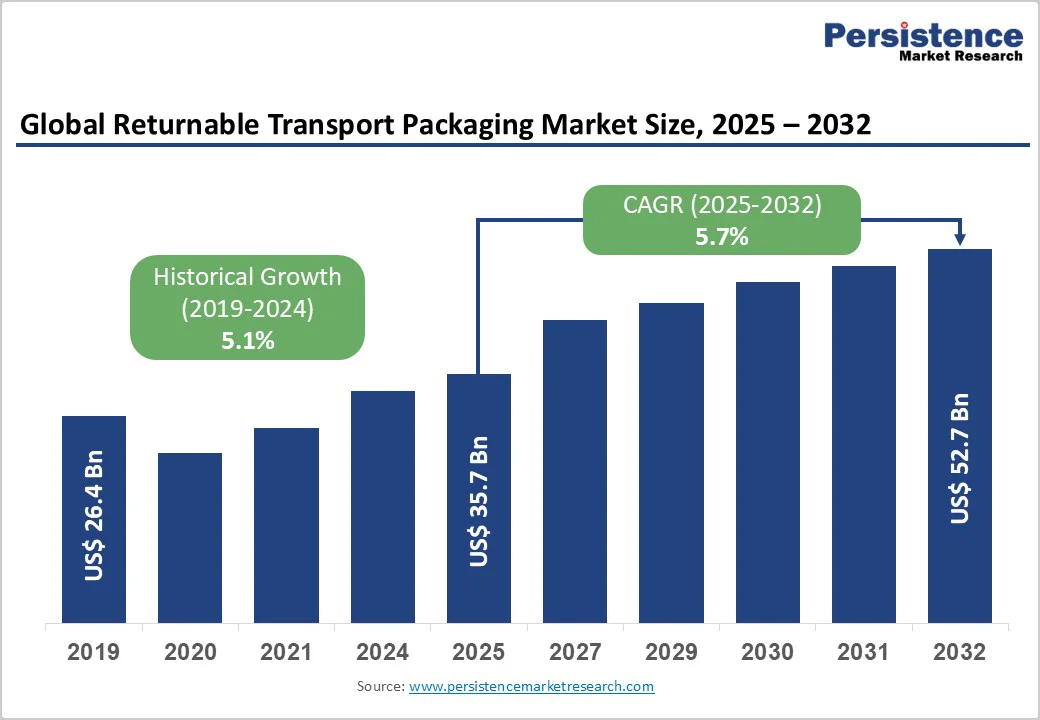

The global returnable transport packaging market size is valued at US$35.7 billion in 2025 and is projected to reach US$52.7 billion, growing at a CAGR of 5.7% between 2025 and 2032.

This market expansion reflects fundamental shifts toward circular economy principles, stringent regulatory frameworks mandating reusable solutions, and the rise in total cost of ownership advantages associated with durable, multi-trip packaging systems.

Key Industry Highlights:

- Leading Product Segment: Intermediate Bulk Containers (IBCs) dominate the market with a 38.3% share in 2025, driven by chemical, pharmaceutical, and food industry demand.

- Fastest-Growing Product: Crates & Totes show rapid adoption due to e-commerce and fresh produce logistics, projected to grow at 5.1% CAGR through 2035.

- Leading Material: Plastic remains the dominant material with 47.4% market share in 2025, owing to cost efficiency, hygiene, and design flexibility.

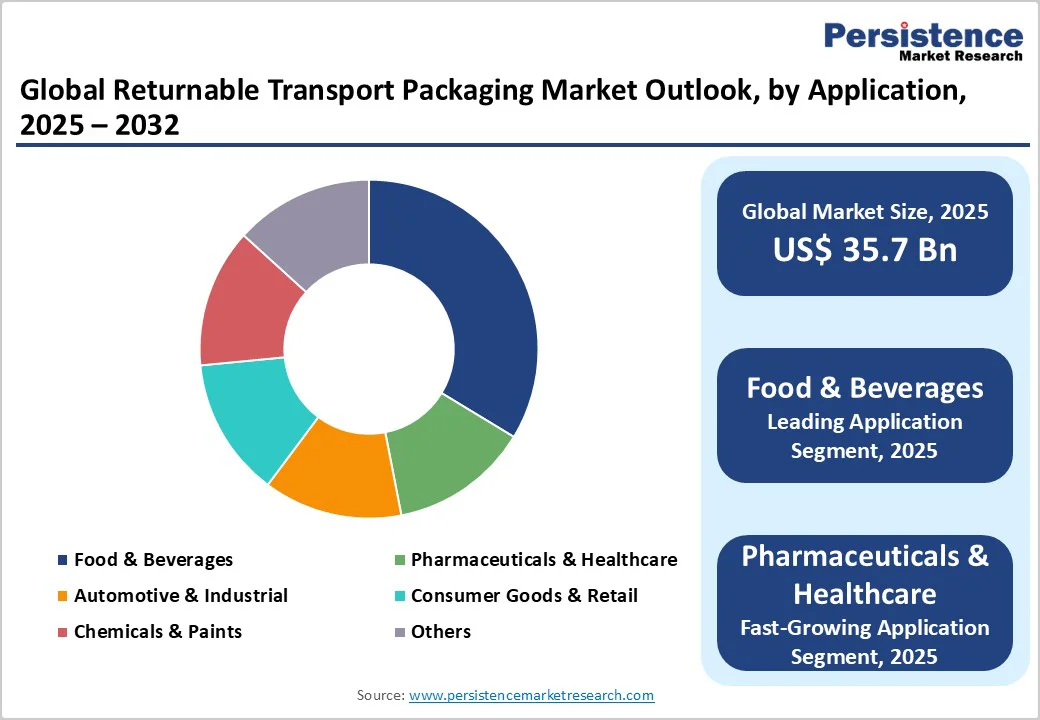

- Leading Application: Food & Beverages holds the largest application share at 38.4% in 2025, supported by cold chain expansion and regulatory compliance.

- Fastest-Growing Application: Pharmaceuticals & Healthcare are the fastest-growing segments, driven by biologics, cold chain logistics, and smart packaging adoption.

| Key Insights | Details |

|---|---|

| Returnable Transport Packaging Market Size (2025E) | US$ 35.7 Bn |

| Market Value Forecast (2032F) | US$ 52.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.1% |

Market Dynamics

Driver - Regulatory Mandates for Circular Economy Compliance

The European Union's Packaging and Packaging Waste Regulation (PPWR) represents one of the most consequential regulatory shifts influencing the Returnable Transport Packaging Market globally.

Effective from January 1, 2030, the PPWR mandates that all packaging must be either reusable or recyclable, with subsequent targets requiring 10% reusability for transport and sales packaging by 2030, growing to 70% by 2040. These regulatory thresholds compel manufacturers across continents to transition from single-use to returnable systems, fundamentally reshaping supply chain infrastructure.

The requirement that packaging void space in transport systems not exceed 50% by 2030 directly incentivises compact returnable designs, positioning the Returnable Transport Packaging Market as the compliance mechanism for enterprises operating across EU jurisdictions.

Beyond Europe, similar mandates in North America, including state-level initiatives and corporate sustainability commitments, amplify market demand. These regulatory drivers are projected to sustain the market's 5.7% CAGR through 2032, with acceleration in regions subject to stringent waste reduction penalties.

The mandatory minimum recycled content requirements, 50% for glass, 70% for paper, 25% for metal by 2030, create additional compliance incentives for returnable container adoption within the Returnable Transport Packaging Market, as enterprises seek circular infrastructure solutions demonstrating verifiable compliance documentation.

Total Cost of Ownership Advantage and Supply Chain Economics

Despite higher initial capital expenditure, returnable containers deliver compelling long-term financial advantages that distinguish them within the returnable transport packaging market. Comparative lifecycle assessments demonstrate that reusable transport packaging reduces carbon emissions by 28-30% relative to disposable alternatives, while simultaneously diminishing per-trip logistics costs after 4-6 usage cycles.

In North America's food and beverage sector, which accounts for approximately 38.4% of application-level demand, the adoption of returnable crates and pallets has generated measurable operational cost reductions across cold chain and ambient temperature logistics networks. The returnable transport packaging market benefits from this economic bifurcation: enterprises reduce waste-disposal expenditures, lower material procurement cycles, and decrease transportation emissions per unit of goods moved.

Financial modelling conducted by logistics providers confirms that returnable plastic crates deliver 15-22% total cost reductions over five-year deployment horizons compared to corrugated cardboard alternatives. This economic stratification has prompted cross-sector adoption acceleration, particularly among large-scale consumer goods, pharmaceutical, and quick-service restaurant enterprises. Companies, including Brambles (CHEP operations) and Nefab, have documented sustained ROI realization within 18-30-month deployment cycles, reinforcing market trajectory toward the projected 2032 valuation.

Restraint - Capital Investment and Reverse Logistics Complexity

Despite compelling long-term economics, the Returnable Transport Packaging Market confronts significant adoption barriers related to upfront capital requirements and operational complexity. Implementation of returnable systems necessitates investment in container tracking infrastructure, cleaning and maintenance facilities, and reverse logistics networks capital expenditures estimated at 40-60% higher than disposable alternatives during initial deployment phases.

Contamination risks during return cycles and the requirement for standardised container dimension limits compatibility across supply chain partnerships, constraining market expansion in sectors characterised by distributed manufacturing or complex multi-party logistics arrangements.

These infrastructure barriers have historically protracted adoption timelines, particularly in emerging markets where depot networks remain underdeveloped and regulatory enforcement is inconsistent, thereby capping near-term market growth rates despite favourable long-term economics.

Opportunity - Circular Economy Integration and Recycled Content Mandates

The convergence of circular economy policy frameworks and mandatory recycled content requirements generates substantial opportunities within the returnable transport packaging market, particularly for innovators developing advanced material technologies.

The EU's mandated minimum recycled content standards establishing 50% recycled content requirements for glass, 70% for paper/cardboard, and 25% for metal packaging by 2030 create demand for returnable container designs optimised for high recycled material content while maintaining mechanical performance specifications. Enterprises developing returnable systems incorporating advanced composite materials, recycled plastic alloys, and hybrid configurations stand to capture premium pricing within regulated markets.

Specialised Application Development for Pharmaceuticals and Advanced Manufacturing

The pharmaceutical and healthcare sectors represent the fastest-growing application segment for returnable transport packaging, creating targeted opportunities for specialised container development. Pharma-grade returnable containers with validated cleaning protocols, enhanced chemical resistance, and integrated temperature monitoring are capturing share within this high-margin segment. IFCO Systems' 2023 partnership with a German startup to pilot reusable temperature-controlled boxes for pharmaceutical shipments with IoT-based condition tracking exemplifies this trend.

The European pharmaceutical market expenditure of €175 billion annually on medications through statutory health insurance systems creates substantial logistics volume supporting returnable container pools. Automotive supply chain localisation and complex component manufacturing also drive demand for custom-engineered returnable racks and handling systems designed for specific part geometries and protective requirements.

Companies developing specialized returnable solutions targeting pharmaceutical distribution, advanced manufacturing, and automotive sectors can command premium pricing and establish durable competitive advantages within the Returnable Transport Packaging Market.

Category-wise Analysis

Product Type Insights

Intermediate bulk containers maintain dominant market positioning within the Returnable Transport Packaging Market, representing 38.3% of total market value in 2025. IBCs serve as standardised, multi-purpose bulk storage and transport solutions for chemicals, pharmaceuticals, food ingredients, and industrial liquids, with plastic IBCs accounting for 52.3% of this subsegment in 2025.

The chemical processing industry-where IBCs represent 38.4% of application demand-relies on these containers for their exceptional chemical compatibility, standardised pallet footprints enabling robotic handling, and cost-effective capacity characteristics.

Crates and totes represent the fastest-growing product category within the Returnable Transport Packaging Market, driven by accelerating e-commerce adoption and warehouse automation requirements. These standardised, stackable containers are optimised for retail warehouses, poultry production, fresh produce distribution, and last-mile delivery fulfilment-sectors experiencing unprecedented growth.

Material Type Insights

Plastic materials dominate with a 47.4% share in 2025, reflecting polypropylene and polyethylene's superior cost-effectiveness, lightweight characteristics, and established manufacturing infrastructure. Returnable plastic containers withstand repeated usage cycles without significant degradation, with durable formulations tested for over 150 reuse cycles in demanding applications.

The material's lightweight properties reduce transportation costs during both forward and return logistics, directly improving the total cost of ownership calculations that drive returnable system adoption decisions. Plastic's compatibility with automated sorting systems and RFID tag integration makes it the preferred material for e-commerce and warehouse automation applications.

Metal returnable containers represent the fastest-growing material category within the Returnable Transport Packaging Market, capturing share in specialised applications requiring superior durability, chemical resistance, and structural integrity. In North America, 21 new steel returnable containers were introduced for chemical logistics in 2024, featuring reinforced corners and corrosion resistance that reduce average damage rates to below 2% annually.

Application Insights

Food and beverage applications maintain clear market leadership within the returnable transport packaging market, representing 38.4% of total demand in 2025. This dominance reflects the sector's operational scale, regulatory strictness concerning product safety and contamination prevention, and distribution complexity spanning farm-to-consumer supply chains.

The U.S. food and beverage production sector contributed more than $534.3 billion to GDP in 2023 and employed approximately 3.5 million workers, with food processing representing 60% of employment and experiencing robust growth. Returnable plastic crates, pallets, and bulk bins provide hygienic, sterilizable, and temperature-resistant solutions essential for perishable items, including fruits, vegetables, dairy products, and beverages.

Pharmaceuticals and healthcare represent the fastest-growing application segment within the returnable transport packaging market, reflecting accelerating investment in pharmaceutical manufacturing, temperature-sensitive biologics distribution, and healthcare supply chain modernisation.

European pharmaceutical production reached €390 billion in 2023, with export activity of €680 billion positioning the EU as a global pharmaceutical leader. Cold chain logistics for medications, vaccines, and biopharmaceuticals demand specialised returnable containers with integrated temperature monitoring, validated cleaning protocols, and compliance documentation capabilities.

Regional Insights and Trends

East Asia Returnable Transport Packaging Market Trends

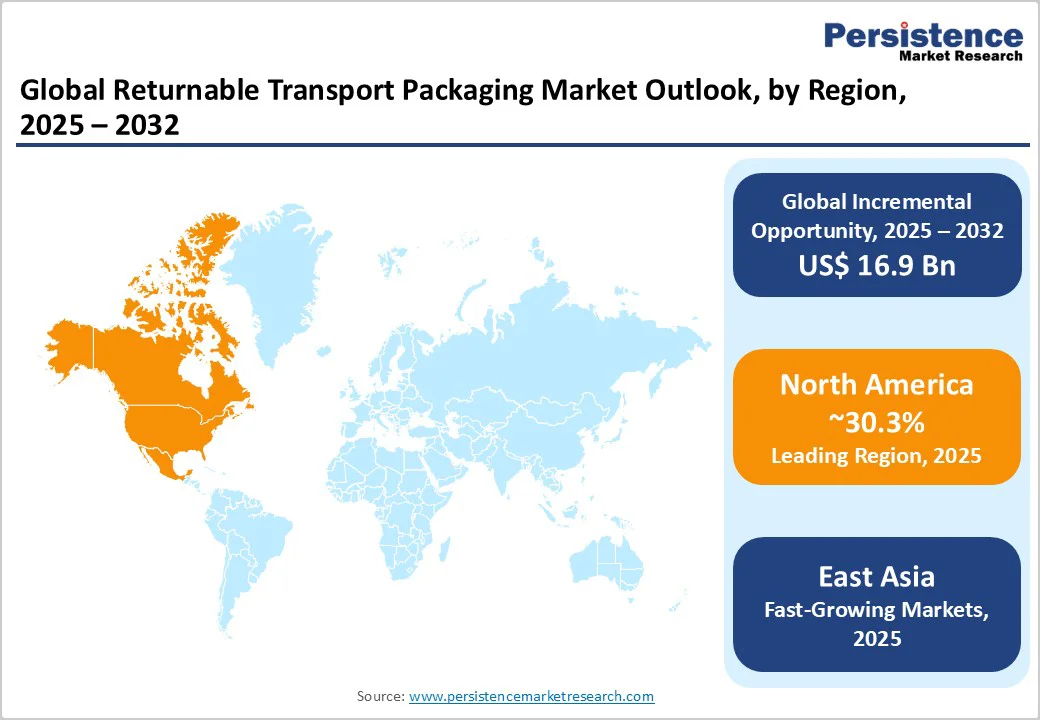

East Asia represents 22.4% of the global Returnable Transport Packaging Market value, with China, India, and ASEAN nations experiencing rapid growth driven by e-commerce expansion, manufacturing localisation, and government sustainability initiatives. The region is transitioning from import-dependent packaging models to domestic returnable container production and pooling operations.

China's returnable packaging infrastructure is modernising rapidly, with major e-commerce platforms including Alibaba and JD.com implementing closed-loop packaging systems across their logistics networks. India's packaging sector is valued at over US$ 86 billion in 2024 and growing at 22-25% annually, with returnable containers capturing an increasing market share as food processing, pharmaceuticals, and e-commerce logistics expand.

Government policies, including the National Mission on Sustainable Packaging, are creating regulatory tailwinds for returnable adoption. The East Asian market is forecast to achieve growth rates exceeding the global average, with manufacturing localisation and rising operational costs making returnable systems increasingly economically attractive compared to single-use alternatives.

Europe Returnable Transport Packaging Market Trends

Europe represents 23.8% of the global market, with the region serving as the regulatory vanguard for returnable adoption and circular economy implementation. European markets are experiencing mature growth with premium pricing reflecting strict regulatory compliance, environmental commitment, and advanced technology integration.

Europe's returnable packaging market is dominated by Brambles, IFCO Systems (recently acquired by Koch Industries), and Schoeller Allibert, which merged with IPL in 2025 to create a US$ 1.4 billion reusable packaging powerhouse.

The European regulatory environment is the world's most stringent, with the Single-Use Plastics Directive (SUPD) and incoming Packaging and Packaging Waste Regulation (PPWR) mandating returnable adoption across most supply chains.

North America Returnable Transport Packaging Market Trends

North America commands 30.3% of the global returnable transport packaging market, reflecting the region's mature supply chain infrastructure, established consumer goods distribution networks, and advanced regulatory environment driving returnable adoption.

The regulatory landscape is reshaping the market growth. Proposed federal regulations addressing packaging waste, combined with existing state-level bans on single-use containers and mandatory producer responsibility schemes, create compliance incentives for returnable adoption.

California's plastic waste reduction targets and similar initiatives across Western states are accelerating returnable infrastructure investments in a region representing approximately 35% of U.S. GDP.

Competitive Landscape

The global returnable transport packaging market is moderately consolidated yet displays some fragmentation due to the diversity of asset types, materials and regional players.

Major companies such as Greif, Inc., Brambles Limited (via CHEP), Mauser Packaging Solutions, Schoeller Allibert Services B.V., Schuetz GmbH & Co. KGaA and DS Smith Plc dominate the higher end of the value chain, leveraging pooling systems, reusable pallets, IBCs and global logistics networks.

These top players benefit from scale, integrated service offerings and circular economy positioning, making the structure more oligopolistic at the leading tier. At the same time, many mid-size and regional providers support the long tail of material types (wood, metal, plastic), local markets and niche applications, contributing to fragmentation in certain sub-segments.

The competitive dynamic is driven by sustainability mandates, reverse logistics optimisation, asset tracking sophistication and long-term reuse contracts rather than short-term commodity packaging sales.

Key Industry Developments

- On June 5, 2025, Mauser Packaging Solutions expanded its reconditioning and recycling operations in Spain with a new on-site facility at BASF’s Tarragona location. The facility reconditions Intermediate Bulk Containers (IBCs) and produces high-quality post-consumer resin, supporting the collection, reuse, and sustainable management of industrial plastic packaging. This investment enhances operational efficiency, reduces carbon emissions, and strengthens RTP adoption in the region through certified, reusable packaging solutions.

- Feb. 2, 2024, Mauser Packaging Solutions acquired Consolidated Container Company, a manufacturer, reconditioner, and distributor of industrial containers, along with recycling services. The acquisition strengthens Mauser’s RTP portfolio in North America by expanding its capacity for container reconditioning, reuse, and sustainable industrial packaging solutions. This strategic move enhances service offerings for customers while supporting circular economy practices in the RTP segment.

Companies Covered in Returnable Transport Packaging Market

- Borealis

- Grief, Inc.

- Brambles Limited

- Mauser Packaging Solutions

- Schoeller Allibert Services B.V.

- DS Smith Plc

- Time Technoplast Ltd.

- Berry Global, Inc.

- Cordstrap B.V.

- Schuetz GmbH & Co. KGaA.

- Supreme Industries Limited

- PalletOne, Inc

- Balmer Lawrie & Co. Ltd.

- Craemer Holding GmbH

- Cabka Group GmbH

- Bulk Lift International, Inc

Frequently Asked Questions

The global Returnable Transport Packaging Market is projected to be valued at US$49.8 Bn in 2025.

The Plastic segment is expected to hold approximately 47.4% market share by Material Type in 2025, driven by its cost-effectiveness, durability, and widespread adoption in packaging applications.

The Returnable Transport Packaging market is expected to witness a CAGR of 5.3% from 2025 to 2032.

The Returnable Transport Packaging market growth is driven by regulatory mandates enforcing sustainable packaging, expansion of cold chain and pharmaceutical logistics, and the acceleration of e-commerce requiring efficient, reusable packaging solutions.

Key market opportunities in the Returnable Transport Packaging market lie in smart packaging and real-time tracking technologies, circular economy-driven sustainable material innovations, and expansion into high-growth emerging markets with supportive infrastructure development.

The leading global players in the Returnable Transport Packaging market include Borealis, Greif Inc., Brambles Limited, Mauser Packaging Solutions and Schoeller Allibert Services B.V.