- Rail

- Rail Bellows Market

Rail Bellows Market Size, Share, and Growth Forecast, 2026 - 2033

Rail Bellows Market by Product Type (Folding, Corrugated, Double-Corrugated, Aerodynamic Wind Fairing System), Material (Rubber, Steel, Aluminum, Composites), Sales Channel (Retro Fit, Line Fit), and Regional Analysis for 2026-2033

Rail Bellows Market Share and Trends Analysis

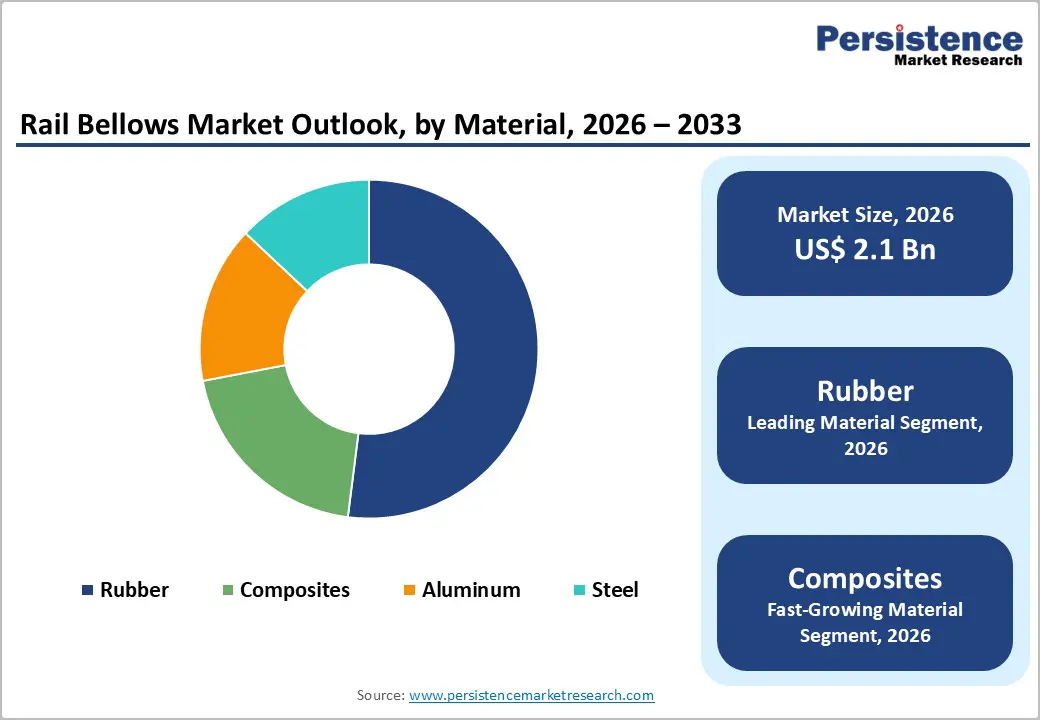

The global rail bellows market size is likely to be valued at US$ 2.1 billion in 2026, and is projected to reach US$ 3.0 billion by 2033, growing at a CAGR of 5% during the forecast period 2026−2033. The expansion of this market is stimulated by escalating investments in high-speed rail networks, particularly across Asia Pacific and Europe, alongside stringent regulatory mandates requiring advanced gangway systems for inter-carriage connectivity. Rising urbanization and government initiatives promoting sustainable mass transit solutions are compelling rail operators to upgrade existing rolling stock with technologically advanced bellows systems that ensure enhanced operational efficiency and passenger experience.

Key Industry Highlights

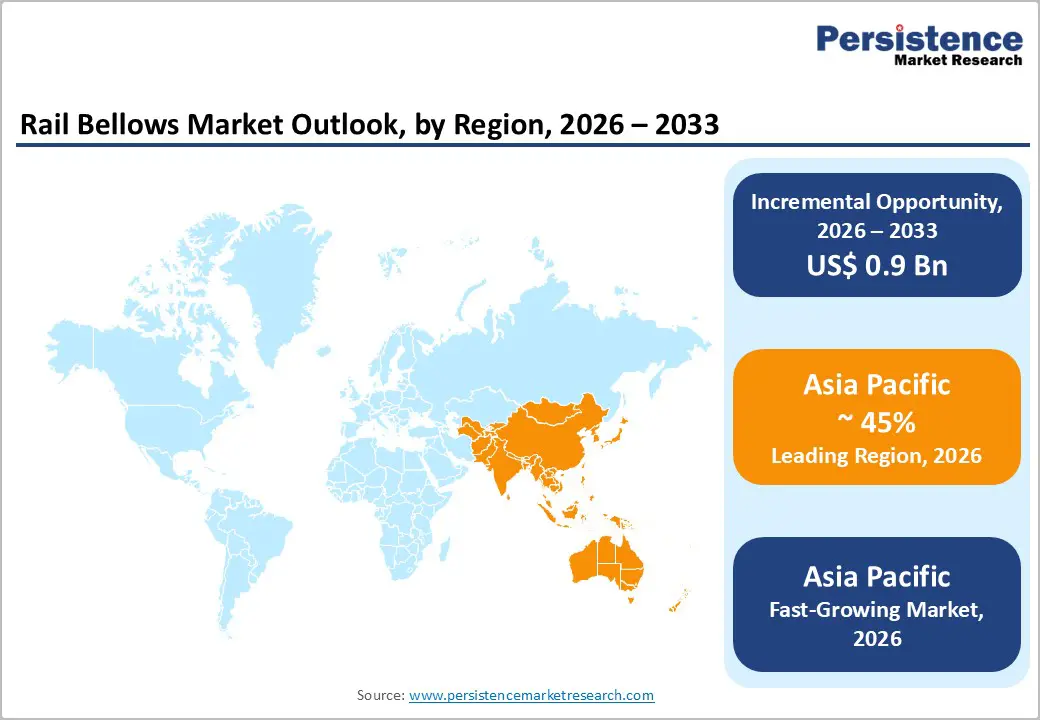

- Regional Leadership: Asia Pacific is forecast to be the leading and the fastest-growing market through 2033, accounting for approximately 45% of market share, owing to the extensive rail networks of China and India.

- Product Type Dominance: Corrugated bellows are slated to dominate with about 45% in 2026, as they are widely preferred across rail applications ranging from metropolitan transit systems to intercity express services.

- Fastest-growing Product Type: Aerodynamic wind fairing systems are likely to be the fastest-growing segment over the 2026-2033 forecast period, driven by the increasing deployment of energy-efficient equipment across railway operations worldwide.

- Market Drivers: Governments are prioritizing railway upgrades as a strategic lever for economic resilience, decarbonization, and improved urban mobility, aiding market growth.

- Market Opportunities: Developing economies across Southeast Asia, Africa, and Latin America are advancing ambitious rail infrastructure programs that are reshaping long-term demand for rail bellows and gangway systems.

| Key Insights | Details |

|---|---|

| Rail Bellows Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerating Global Rail Infrastructure Investments

Governments worldwide are prioritizing railway upgrades as a strategic lever for economic resilience, decarbonization, and improved urban mobility. Public authorities increasingly view rail as the backbone of national logistics and commuter transport, which is driving sustained investment in modern rolling stock, safer passenger interfaces, and more reliable inter-carriage systems. This policy focus strengthens the business case for components that enhance operational safety, reduce lifecycle maintenance, and support higher service availability. In this context, rail bellows are emerging as critical elements within gangways and articulation systems, because they protect passengers from external conditions and shield mechanical interfaces from environmental stress.

For suppliers of rail bellows, large-scale infrastructure and rolling stock programs in Europe and Asia Pacific create long-term visibility into future demand. Strategic initiatives in corridor-based connectivity, cross-border rail integration, and urban transit expansion increasingly specify high-performance gangway solutions that can support higher speeds and more stringent safety standards. High-speed and premium passenger services depend on advanced bellows that maintain airtight connections between cars, enhance passenger comfort, and minimize noise and vibration. This environment rewards manufacturers that align with operator priorities on durability, platform-specific customization, and compliance with evolving rail regulations, which positions rail bellows as a leveraged growth niche within the broader rail value chain.

Supply Chain Complexity and Raw Material Volatility

Rail bellows production relies on highly specialized raw materials such as synthetic rubber compounds, engineered industrial fabrics, and metallic reinforcement components engineered for demanding railway environments. Meeting strict safety, durability, and performance standards limits the number of qualified suppliers and often concentrates sourcing in specific regions. This concentration increases reliance on a narrow vendor base and reduces flexibility when procurement teams need to adjust specifications, renegotiate contracts, or approve alternative sources. As a result, rail manufacturers and operators should treat material sourcing as a strategic function rather than a transactional activity, aligning procurement decisions with long-term asset management priorities and risk-control objectives.

Supply continuity for custom-engineered bellows also depends on extended production cycles and close coordination among design, testing, and manufacturing teams. Long lead times for tailored assemblies make it difficult for rail operators to synchronize maintenance windows, fleet upgrades, and new rolling stock introductions with actual delivery schedules. Pandemic-era disruptions revealed how quickly these interdependencies can undermine project timelines, reliability targets, and budget assumptions, particularly when contingency inventories are limited. Going forward, industry stakeholders can strengthen operational resilience by diversifying their base of qualified suppliers, building collaborative partnerships with material producers, and integrating supply chain risk assessments into capital planning and lifecycle costing practices.

Emerging Market Rail Network Expansion

Developing economies across Southeast Asia, Africa, and Latin America are advancing ambitious rail infrastructure programs that are reshaping long-term demand for rail bellows and gangway systems. Flagship projects such as Indonesia’s Jakarta–Bandung high-speed corridor, Thailand’s Eastern Economic Corridor rail initiatives, and Kenya’s Standard Gauge Railway extensions show how large-scale networks create multi-decade procurement pipelines for critical components. For suppliers, these programs shift future growth toward markets where new corridors, urban transit systems, and cross-border routes are being planned or built rather than only upgraded. To respond effectively, rail bellows manufacturers should align commercial strategies with national transport policies, multilateral funding priorities, and local industrialization objectives.

India’s rapid expansion of metro rail systems in major urban centers further illustrates the structural opportunity in emerging markets for gangway and bellows solutions tailored to high-frequency, high-density operations. These projects favor partners that demonstrate reliable technical performance and also support localization through technology transfer, in-country assembly, and workforce capability building. Manufacturers that invest early in regional production facilities, aftermarket service networks, and collaborative engineering relationships with local rolling stock builders are better positioned to secure long-term framework agreements. From a strategic perspective, success in these markets depends on combining cost-competitive offerings with lifecycle support and risk-sharing models that help public authorities and private operators manage reliability, safety, and total cost of ownership across the full asset life.

Category-wise Analysis

Product Type Insights

Corrugated bellows are slated to maintain a dominant position in the market, with an estimated 2026 share exceeding 45%. Corrugated bellows are widely preferred across rail applications ranging from metropolitan transit systems to intercity express services because they offer a strong balance of flexibility, durability, and cost-effectiveness. Their corrugated structure enhances compression and extension performance, which is essential for managing changes in the distance between carriages during operation, especially on curved tracks and where vertical movement occurs between vehicles. Corrugated bellows also have a long track record of reliable service at conventional operating speeds, making them a standard choice for regional rail networks and mature metro systems that focus on lifecycle efficiency and straightforward maintenance practices.

Aerodynamic wind fairing systems are likely to be the fastest-growing segment over the 2026-2033 forecast period, driven by increasing deployment of high-speed rail networks where aerodynamic efficiency directly impacts energy consumption and operational economics. These advanced systems integrate streamlined external fairings with internal bellows assemblies, reducing aerodynamic drag by 15-20% at velocities exceeding 250 km/h compared to conventional gangway designs. Market acceleration is particularly pronounced in China's expanding high-speed network and European cross-border express services, where operational speeds routinely exceed 300 km/h, creating compelling economic rationale for aerodynamic optimization investments.

Material Insights

Rubber rail bellows hold the highest revenue share, estimated to reach 52% in 2026. The leadership attributed to their optimal combination of weather resistance, flexibility, and proven performance across diverse climatic conditions. Rubber formulations utilizing ethylene propylene diene monomer (EPDM) and neoprene compounds offer excellent ozone and UV resistance, temperature tolerance ranging from -40°C to +70°C, and service life exceeding 18-20 years under normal operating conditions. These materials meet stringent fire safety regulations mandated by railway authorities worldwide, including EN 45545 European fire safety standards and NFPA 130 North American requirements.

Composite rail bellows is estimated to be the fastest-growing segment during the 2026-2033 forecast period, reinforced by compelling weight reduction advantages, corrosion immunity, and enhanced design flexibility enabling complex geometries optimized for aerodynamic performance. Advanced composite materials incorporating carbon fiber-reinforced polymers and glass fiber-reinforced thermoplastics achieve 35-40% weight savings compared to conventional rubber or steel alternatives while maintaining equivalent structural strength and durability specifications. The environmental advantages, including recyclability and reduced carbon footprint in manufacturing, align with circular economy principles increasingly influencing procurement specifications, positioning composites for accelerated market share gains, particularly in next-generation high-speed and maglev train applications.

Sales Channel Insights

Line fit segment currently leads with an approximate 74% of the rail bellows market revenue share in 2026. Line fit procurement typically involves long-term supply agreements that extend over several years, collaborative engineering partnerships that support customization for specific vehicle platforms, and integrated quality assurance processes that ensure compliance with railway technical standards and safety certifications. This structured approach creates a tightly aligned relationship between manufacturers and original equipment manufacturers (OEMs), which helps reduce technical risk and supports consistent product performance across fleets. This procurement channel provides manufacturers with stable production volumes, more predictable revenue streams, and frequent opportunities for value engineering that can optimize total system costs for both parties.

Retro-fit is expected to be the fastest-growing segment during the 2026-2033 forecast period, driven by aging global rolling stock fleets requiring systematic component replacement and increasing emphasis on fleet lifecycle extension strategies versus new vehicle procurement. This channel serves transit authorities, railway operators, independent maintenance service providers, and specialized refurbishment contractors that need replacement bellows for vehicles reaching the end of component life or experiencing in-service damage. As fleets age and utilization intensifies, these stakeholders depend on reliable access to compatible parts to sustain availability, safety, and regulatory compliance across existing rolling stock.

Regional Insights

Asia Pacific Rail Bellows Market Trends

Asia Pacific is likely to be both the leading and fastest-growing regional market for rail bellows in 2026, accounting for approximately 35% of market share. The growth is supported by a combination of large-scale high-speed rail programs, extensive urban transit networks, and ongoing fleet renewal initiatives across major economies. China continues to act as the primary demand anchor through its extensive high-speed and intercity rail operations, while Japan contributes a mature, technologically advanced network that places strong emphasis on reliability, safety, and innovation. India adds a significant growth dimension through the rapid expansion of metro rail systems and the increasing standardization of specifications for gangway and bellows solutions across new projects.

Industrial policy initiatives, such as national manufacturing promotion schemes and regional investment incentives, encourage local production, joint ventures, and technology transfer partnerships between global bellows specialists and domestic manufacturers. For rail bellows suppliers, an effective regional strategy involves balancing cost competitiveness with technology differentiation, building local engineering and service capabilities, and structuring long-term agreements that align with government infrastructure plans and clearly defined sustainability objectives.

Europe Rail Bellows Market Trends

Europe is predicted to capture a sizable portion of the rail bellows market share in 2026, supported by dense high-speed, regional, and metropolitan rail networks in countries such as Germany, the United Kingdom, France, and Spain. Germany’s integrated combination of intercity high-speed services, regional lines, and metro systems creates consistent demand across original equipment, mid-life refurbishment, and end-of-life replacement cycles. The United Kingdom and France deepen this demand through large, multi-stage modernization and expansion programs that require close coordination between rolling stock manufacturers and component suppliers. Spain’s extensive high-speed operations further strengthen the regional demand base, positioning Western Europe as a key reference market for performance, safety, and passenger comfort standards in gangway and bellows applications.

The European Union (EU) supports this ecosystem through regulatory harmonization and long-term policy commitments that position rail as a central pillar of sustainable transport. Technical Specifications for Interoperability (TSI) set common requirements across member states, which enables cross-border operations and allows suppliers to benefit from consistent rules for design, testing, and certification. Policy initiatives linked to the European Green Deal and trans-European transport network programmes provide greater visibility on future investment priorities and encourage the use of materials and designs that improve recyclability, reduce weight, and enhance energy efficiency.

North America Rail Bellows Market Trends

The North America rail bellows market growth is shaped by large, established transit networks, ongoing modernization programs, and a robust regulatory environment that prioritizes safety, domestic manufacturing, and accessibility. The United States generates most of the regional demand through its extensive metropolitan transit systems and intercity passenger services, while Canada and Mexico contribute additional requirements through urban transit expansions and network upgrades. For suppliers, this context creates a stable foundation of original equipment opportunities, supported by increasing demand for refurbishment and mid-life overhaul solutions as aging fleets progress through replacement cycles.

Regulation and policy play a central role in shaping competitive dynamics in the North American rail bellows market. Safety requirements and domestic content rules in the United States favor manufacturers that maintain local production capacity, demonstrate strong compliance capabilities, and can operate effectively within public procurement processes. Major infrastructure and corridor upgrade programs are driving the adoption of higher-specification bellows solutions that enhance passenger comfort, accessibility, and operational reliability. Innovation ecosystems in North America also encourage the use of advanced materials and smart monitoring technologies, giving an advantage to suppliers that can prove both technical differentiation and clear lifecycle value.

Competitive Landscape

Leading firms such as Dellner Couplers AB, Hutchinson SA, ATG Autotechnik GmbH, Cavotec Group, and Schleifring GmbH have established a consolidated control over the global rail bellows market. These companies hold nearly half the market through focused investments in research & development efforts to drive product upgrades constantly. Advanced technologies have further boosted product performance and lifespan, with strategic partnerships enabling operational expansion across geographies for key players.

Firms are pursuing acquisitions and joint ventures to strengthen their market position. They are prioritizing durable materials to meet the rising demands of modern rail infrastructure. Global outreach is being amplified via collaborative deals, while innovators are integrating efficiency features for future networks. Brands are securing a competitive edge through ongoing enhancements, ensuring lasting dominance in this vital space.

Key Industry Developments

- In March 2025, EQT sold Dellner Couplers, a global leader in train connection systems such as couplers and gangways, to Wabtec Corporation for approximately EUR 890 million.

The deal strengthened Wabtec's transit portfolio with Dellner's safety-critical products and aftermarket services across Europe, North America, and Asia, promising synergies and profitable growth. - In March 2025, the Metropolitan Transportation Authority (MTA) introduced two R211 open-gangway subway trains on New York's G Line, making it the second line after the C to feature this design for smoother passenger movement. These modern cars offer wider doors, security cameras, accessible seating, brighter lights, and digital displays to boost reliability, boarding speed, and rider experience amid ongoing fleet upgrades.

- In February 2025, Hitachi Rail contracted HÜBNER Group to supply up to 280 gangway systems for new ETR 1000 high-speed trains entering service between 2025 and 2029. These trains, which already use HÜBNER gangways, benefit from corrugated bellows with aerodynamic fairings that align with the train’s exterior to cut air resistance, contributing to quieter operation and higher energy efficiency on Italian and wider European high-speed lines.

Companies Covered in Rail Bellows Market

- Dellner Couplers AB

- Hutchinson SA

- ATG Autotechnik GmbH

- Cavotec Group

- Schleifring GmbH

- Hubner Group

- CRRC Corporation Limited

- Narita Seisakusho Co., Ltd.

- Qingdao Huarui Rubber Co., Ltd.

- Pneumatik Berlin

- Scharfenberg GmbH

- Yutaka Manufacturing Co., Ltd.

- Escorts Railway Division

- Wabtec Corporation

- Knorr-Bremse AG

Frequently Asked Questions

The global rail bellows market is projected to reach US$ 2.1 billion in 2026.

The market is driven by accelerating investments in rail infrastructure, high-speed and urban transit expansion, and the need for safer, more reliable inter-carriage connections.

The market is poised to witness a CAGR of 5% from 2026 to 2033.

High-speed and metro projects, adoption of advanced materials and aerodynamic designs, and growing aftermarket demand for refurbishment and lifecycle extension are opening novel market opportunities.

Dellner Couplers AB, Hutchinson SA, ATG Autotechnik GmbH, Cavotec Group, and Schleifring GmbH. are some of the key players in the market.