- Pharmaceuticals

- Radiation Pneumonitis Treatment Market

Radiation Pneumonitis Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Radiation Pneumonitis Treatment Market by Treatment Type (Corticosteroids, Bronchodilators, Cough suppressants, Others), by Route of Administration (Oral, Intravenous (IV), Others), by End User (Hospitals, Clinics, Specialty cancer centers, Home care), and Regional Analysis from 2026 to 2033

Radiation Pneumonitis Treatment Market Size and Trend Analysis

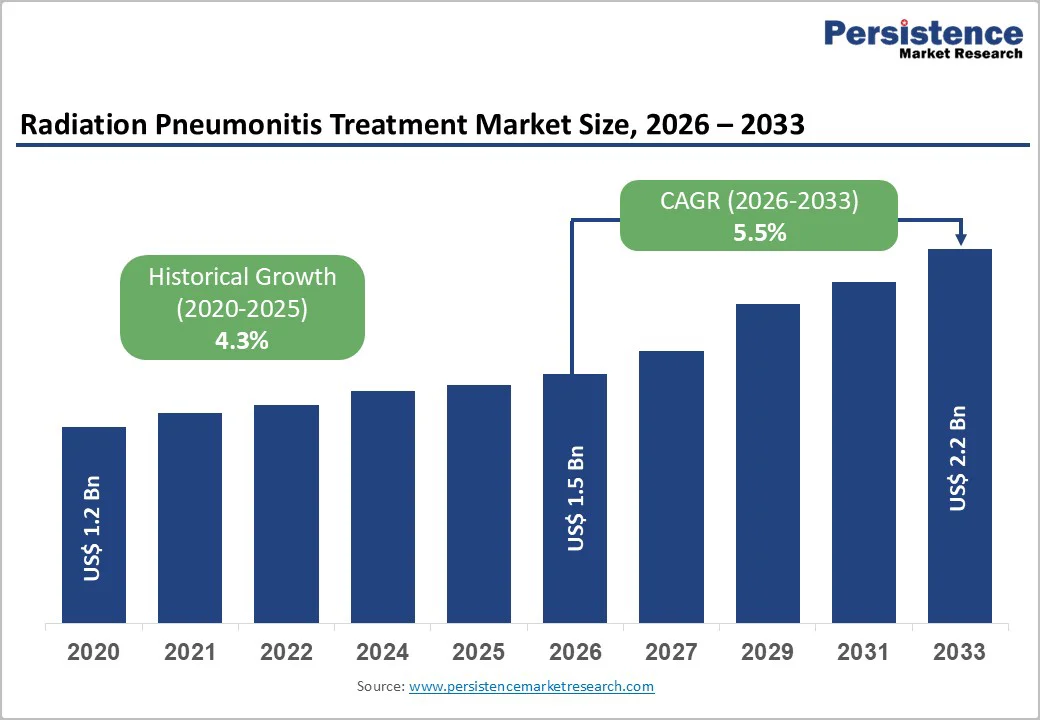

The global Radiation Pneumonitis Treatment Market is estimated to grow from US$ 1.5 billion in 2026 to US$ 2.2 billion by 2033. The market is projected to record a CAGR of 5.5% during the forecast period from 2026 to 2033.

The Radiation Pneumonitis Treatment Market is a focused segment within the broader supportive oncology and respiratory therapeutics industry, driven by rising thoracic radiotherapy utilization and the increasing burden of lung and mediastinal cancers worldwide. Radiation induced pneumonitis is a key doselimiting toxicity of chest irradiation, especially when combined with chemotherapy or immune checkpoint inhibitors, and frequently requires pharmacologic management using corticosteroids, bronchodilators, and cough suppressants. The market spans inpatient, outpatient, and home care settings, with treatment decisions influenced by symptom severity, imaging findings, and lung function. Clinical guidelines and evidence from leading cancer centers support the use of systemic oral prednisone up to 60 mg/day followed by gradual taper, as well as high dose inhaled steroids such as budesonide 800 micrograms twice daily for selected patients, ensuring continued demand for these drug classes. Expansion of radiotherapy capacity in emerging regions, together with improved cancer survivorship, is expected to fuel steady growth over the next decade.

Key Industry Highlights

- Corticosteroids remain the cornerstone of radiation pneumonitis management, with clinical practice commonly using prednisone up to 60 mg/day for 2–4 weeks followed by 3–12 weeks of taper, delivering predictable anti-inflammatory control in symptomatic patients.

- Evidence supports the role of high dose inhaled corticosteroids, with studies showing that budesonide 800 micrograms twice daily can improve symptoms in grade 2 radiation induced lung injury, allowing some patients to avoid or minimize systemic steroid exposure.

- The market covers multiple therapy classes—including systemic steroids, inhaled steroids, bronchodilators, and cough suppressants—to control cough, dyspnea, and inflammation in patients receiving thoracic radiotherapy.

- Rising lung cancer incidence and improving survival, as documented by the American Lung Association and American Cancer Society, increase the number of patients living long enough to experience and require treatment for radiation induced lung injury.

- Growing use of combined chemoradiotherapy and immuno radiotherapy elevates pneumonitis risk, embedding standardized corticosteroid based management protocols into modern thoracic oncology pathways and supporting sustained treatment demand.

| Global Market Attributes | Key Insights |

|---|---|

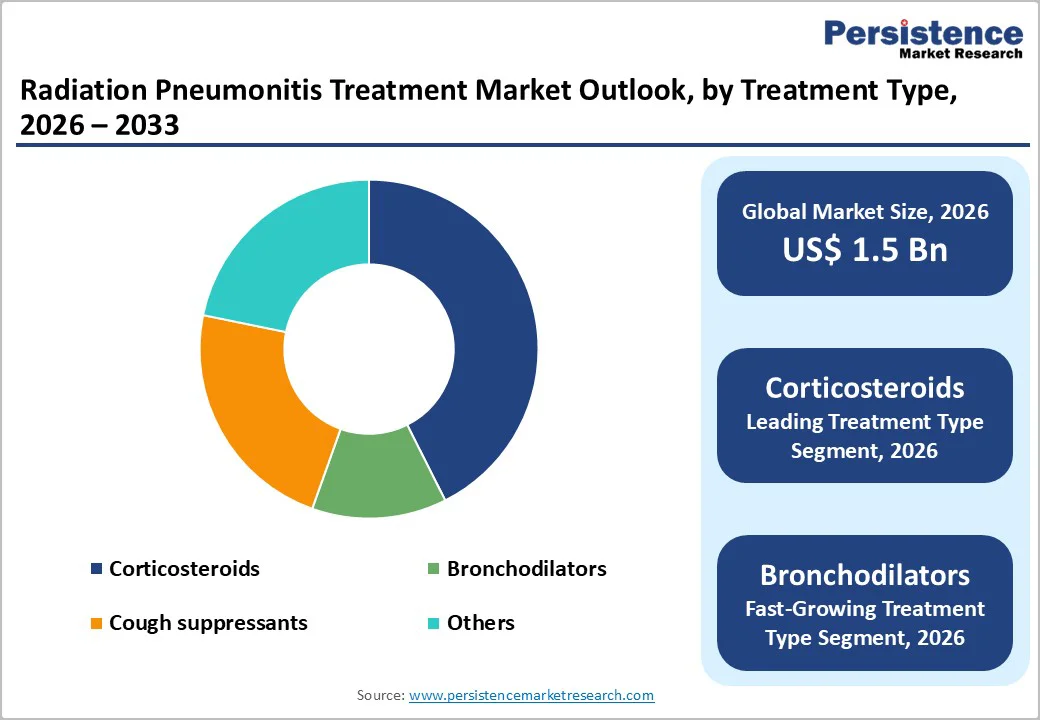

| Radiation Pneumonitis Treatment Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 2.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver – Rising Thoracic Cancer Burden and Radiotherapy Volumes

Rising incidence of lung and other thoracic cancers, combined with expanding radiotherapy utilization, is a primary driver of the Radiation Pneumonitis Treatment Market. Lung cancer remains one of the most common and deadly cancers globally, with the American Cancer Society estimating over 234,000 new lung cancer cases in the United States in 2024, many of whom receive thoracic radiotherapy as part of curative or palliative care. Beyond lung cancer, esophageal malignancies, breast cancer with internal mammary node irradiation, and mediastinal lymphomas also require radiation fields that inevitably expose lung tissue, increasing the risk of radiation induced pneumonitis. As radiotherapy techniques such as IMRT and stereotactic body radiation therapy allow higher doses to be delivered more safely, more patients become eligible for aggressive treatment, which expands the at risk population. Simultaneously, improved screening and earlier detection, highlighted by initiatives from the American Lung Association, increase the number of patients undergoing thoracic radiation, thereby directly driving demand for pharmacologic management of radiation induced lung injury.

Driver – Growth of Combined Chemoradiotherapy and Immuno Radiotherapy

The increasing integration of systemic therapies with radiotherapy is another strong growth catalyst for the Radiation Pneumonitis Treatment Market. Modern treatment paradigms frequently combine thoracic radiotherapy with platinum based chemotherapy, targeted agents, and immune checkpoint inhibitors, improving survival but increasing the risk and severity of pulmonary toxicities such as pneumonitis. Clinical data indicate that combining radiotherapy with immunotherapy, including PD 1/PD L1 inhibitors, can raise pneumonitis incidence into the double digit range in certain cohorts, particularly in lung cancer, compared with substantially lower rates when either modality is used alone. These patients often require prompt initiation of systemic corticosteroids, careful tapering, and adjunctive bronchodilators to manage dyspnea and cough, embedding these therapies into standard toxicity management algorithms. As immuno oncology combinations expand into earlier stage disease and adjuvant settings, the absolute number of patients at risk for radiation and immune related pneumonitis is projected to rise, reinforcing long term demand for established treatment regimens.

Restraints – Safety Concerns with Prolonged Systemic Corticosteroid Use

Intellectual property challenges are less prominent in this pharmacology driven space, but clinical safety concerns related to prolonged systemic corticosteroid treatment significantly restrain market growth. Standard management protocols recommend oral prednisone up to 60 mg/day for 2–4 weeks, followed by a taper lasting 3–12 weeks, especially in patients with moderate to severe radiation pneumonitis. Many of these patients are older, have multiple comorbidities, or are receiving concurrent chemotherapy or immunotherapy, making them highly vulnerable to steroid related adverse effects such as infections, hyperglycemia, osteoporosis, muscle wasting, and mood disturbances. These risks can lead clinicians to under treat or shorten steroid courses, particularly in milder cases, thereby constraining the full pharmaceutical potential of the market even when clinical need exists. In some instances, steroid toxicity may prompt early discontinuation or dose reduction of anti cancer therapies, further complicating treatment decisions and reinforcing a cautious approach to high dose, long duration steroid use.

Restraints – Underdiagnosis, Misclassification, and Practice Variability

Another important restraint for the Radiation Pneumonitis Treatment Market is the underdiagnosis and misclassification of pneumonitis across different care settings. Clinical symptoms such as dry cough, low grade fever, and exertional dyspnea are non specific and can be easily mistaken for infections, chronic obstructive pulmonary disease exacerbations, immune related pneumonitis, or disease progression, particularly in community settings with limited subspecialty support. Access to high resolution CT imaging, diffusion capacity testing, and multidisciplinary tumor boards varies significantly across regions and facilities, especially in low and middle income countries. As a result, many mild or moderate cases of radiation induced lung injury may be empirically treated with antibiotics or supportive care without formal pneumonitis diagnosis, reducing identifiable market volume. Inconsistent use of standardized toxicity grading systems and follow up schedules further contributes to under recognition and variability in treatment thresholds, constraining uniform adoption of pharmacologic protocols and limiting market realization despite a growing base of at risk patients.

Opportunity – Precision Risk Stratification and Structured Lung Protection Pathways

One of the most promising opportunities in the Radiation Pneumonitis Treatment Market is the development and adoption of precision risk stratification tools integrated within structured lung protection pathways. Recent research has emphasized that parameters such as mean lung dose, low dose lung volume (for example, V20), baseline lung function, age, performance status, and pre existing interstitial lung disease can be combined into predictive models to estimate pneumonitis risk after thoracic radiotherapy. When integrated into treatment planning systems, these models allow clinicians to categorize patients into low, intermediate, and high risk groups and to proactively tailor prophylactic or early intervention strategies. High risk individuals may benefit from closer surveillance, earlier initiation of inhaled corticosteroids such as budesonide 800 micrograms twice daily, and structured pulmonary rehabilitation to maintain lung function. Pharmaceutical and device companies that align products with such pathway based care—through optimized dosing, combination inhalers, or digital applications for remote symptom tracking—can unlock additional value and differentiate their offerings in this evolving market.

Category-wise Insights

Treatment Type Analysis – Corticosteroids Lead the Market

By treatment type, corticosteroids currently hold the largest share in the Radiation Pneumonitis Treatment Market, accounting for an estimated 43% of global revenue in 2025. Clinical guidelines consistently recommend corticosteroids as first line therapy for symptomatic radiation pneumonitis, with typical regimens including oral prednisone up to 60 mg/day for 2–4 weeks, followed by a taper of 3–12 weeks, depending on response and severity. Inhaled corticosteroids have also demonstrated efficacy; for example, high dose budesonide 800 micrograms twice daily improved symptoms in patients with grade 2 radiation induced lung injury in clinical studies, offering an alternative or adjunct to systemic therapy. This strong evidence base, combined with broad availability and clinician familiarity, solidifies corticosteroids as the dominant treatment class in both inpatient and outpatient settings, while bronchodilators, cough suppressants, and other agents typically act as supportive therapies to alleviate respiratory symptoms rather than replace steroids.

Route of Administration Analysis – Oral Segment Dominates

By route of administration, the oral segment leads the Radiation Pneumonitis Treatment Market and is expected to maintain the highest share, likely around 55–60% in 2025. Most patients with mild to moderate radiation pneumonitis are managed on an outpatient basis using oral corticosteroids, most commonly prednisone, which allows for flexible dosing and tapering schedules tailored to individual response. Oral dosage forms are also prevalent for adjunctive therapies such as cough suppressants and some bronchodilators, making oral delivery the most common and convenient route across care settings. Intravenous (IV) administration is generally reserved for severe or rapidly progressive pneumonitis, often requiring hospitalization, where IV steroids and supportive measures such as oxygen therapy or intensive monitoring are implemented. While IV use is clinically critical in acute high grade cases, its overall volume is lower than oral regimens. As healthcare systems emphasize ambulatory cancer care, oral and inhaled therapies will continue to dominate the treatment landscape.

End User Analysis – Hospitals as Primary Care Hubs

By end user, hospitals represent the leading segment in the Radiation Pneumonitis Treatment Market, accounting for more than 50% of total demand in 2025. Thoracic radiotherapy is most often delivered in hospital based radiation oncology departments, where patients undergo regular imaging and clinical evaluations that facilitate early detection of radiation induced lung injury. Moderate to severe pneumonitis cases, characterized by hypoxia, extensive radiographic infiltrates, or functional decline, are frequently managed in hospitals with systemic corticosteroids, IV therapies, and respiratory support. Hospitals also function as hubs for clinical research on radiotherapy and systemic therapy combinations, where pneumonitis is closely monitored and treated according to protocolized algorithms. While clinics, specialty cancer centers, and home care settings are increasingly involved in follow up, steroid tapering, and long term rehabilitation, hospitals remain central due to their diagnostic capacity, multidisciplinary expertise, and capability to manage acute complications, cementing their leadership in end user share.

Regional Insights

North America Radiation Pneumonitis Treatment Market Trends and Insights

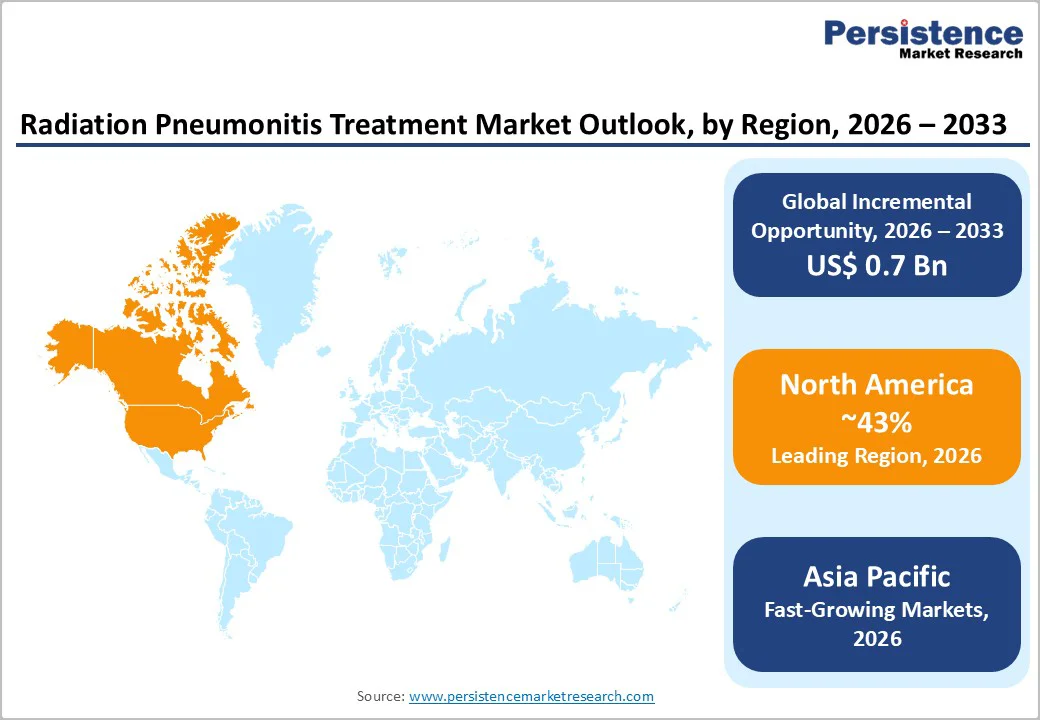

North America is the leading regional market for Radiation Pneumonitis Treatment, benefiting from high lung cancer incidence, extensive radiotherapy capacity, and advanced oncology systems. The Centers for Disease Control and Prevention (CDC) and American Cancer Society report that lung cancer remains a top cause of cancer death in the United States, with more than 218,000 new cases and substantial mortality annually, many treated with thoracic radiation. The American Lung Association’s 2024 “State of Lung Cancer” highlights a 26% improvement in lung cancer survival and a 15% reduction in incidence over five years, which translates into a growing population of survivors who may develop late onset or subacute radiation induced pneumonitis requiring pharmacologic therapy.

The region’s robust innovation ecosystem anchored by leading academic medical centers, cooperative oncology groups, and biopharmaceutical companies—supports high adoption of evidence based management strategies for treatment related lung toxicities. Regulatory oversight from the U.S. Food and Drug Administration (FDA) and Health Canada ensures availability of quality assured systemic and inhaled corticosteroids and bronchodilators, while numerous clinical trials exploring chemoradiotherapy and immuno radiotherapy combinations maintain a strong focus on pneumonitis as a safety endpoint. High healthcare expenditure, comprehensive insurance coverage, and broad access to advanced imaging and pulmonary function testing further facilitate early diagnosis and treatment, reinforcing North America’s market leadership and its estimated 43% global share in 2025.

Asia Pacific Radiation Pneumonitis Treatment Market Trends and Insights

Asia Pacific is emerging as the fastest growing region in the Radiation Pneumonitis Treatment Market, driven by rapid cancer burden escalation, significant radiotherapy infrastructure expansion, and improving access to oncology services. Analyses of radiotherapy in the region indicate severe historical under provision, with some Southeast Asian countries having as few as 0.1 radiotherapy machines per million people compared with 11.7 per million in high income countries such as the United States. Recent initiatives, including national cancer control plans and investments supported by international partners, are dramatically increasing the number of linear accelerators and modern treatment platforms across China, India, Japan, South Korea, and ASEAN nations. This expansion means more patients with lung, esophageal, and breast cancers will be treated with thoracic radiation, increasing the absolute incidence of radiation pneumonitis and the requirement for effective pharmacologic therapy.

Clinical research has also highlighted potential differences in pneumonitis incidence and severity between Asian and non Asian populations after chemoradiotherapy, underscoring the need for tailored risk assessment and management strategies in Asia. As guidelines for radiation induced lung injury are disseminated and oncologists gain more experience in diagnosing and managing pneumonitis, utilization of oral prednisone, inhaled steroids, and bronchodilators is expected to rise substantially. Growing healthcare expenditure, expansion of public insurance schemes, and increasing patient awareness of cancer care and treatment related side effects further support market growth, positioning Asia Pacific as the fastest growing regional segment through 2033, from a relatively underpenetrated base.

Market Competitive Landscape

The Radiation Pneumonitis Treatment Market features a dynamic and moderately fragmented competitive landscape shaped by established respiratory and oncology portfolios and the widespread use of generic formulations. Market participants are primarily focused on optimizing systemic and inhaled corticosteroid use, enhancing bronchodilator and cough suppressant combinations, and integrating these therapies into standardized oncology care pathways. Competition is influenced by brand strength, hospital formularies, availability of long acting inhaled products, and alignment with evolving clinical guidelines. Strategic collaborations between pharmaceutical companies, academic centers, and radiotherapy technology providers are increasingly common, aiming to improve real world management of radiation induced lung injury. Investments in patient education, digital adherence tools, and real world evidence generation are also emerging as important differentiators in this supportive oncology market.

Key Industry Developments

- In May 2025, Health Canada granted a Notice of Compliance with conditions (NOC/c) for Tagrisso® (osimertinib) for the treatment of patients with locally advanced, unresectable (stage III) non-small cell lung cancer (NSCLC) whose tumours had EGFR exon 19 deletions or exon 21 (L858R) substitution mutations (either alone or in combination with other EGFR mutations) and whose disease had not progressed during or following platinum-based chemoradiation therapy. A validated test was required to identify EGFR mutation-positive status prior to treatment.

Frequently Asked Questions

The global market is projected to be valued at approximately US$ 1.5 Bn in 2026, driven by growing thoracic radiotherapy usage, higher cancer survivorship, and increased clinical recognition of radiation‑induced lung injury.

Rising thoracic cancer incidence, expanding radiotherapy capacity, and greater use of combined chemoradiotherapy and immunoradiotherapy regimens are key demand drivers, as they increase the number of patients developing symptomatic radiation pneumonitis that requires pharmacologic management.

The global market is poised to witness a CAGR of about 5.5% between 2026 and 2033, supported by expanding radiotherapy access in emerging regions and standardized toxicity management practices in advanced oncology centers.

North America currently leads the market, backed by high lung cancer burden, advanced radiotherapy infrastructure, strong clinical trial ecosystems, and robust adoption of guideline‑based corticosteroid and respiratory therapy regimens for radiation‑induced lung injury.

Key players include AstraZeneca, Novartis, Merck & Co, Gilead Sciences, Celgene, AbbVie, Sanofi, Roche Holding, Bristol-Myers Squibb, Amgen, Pfizer, Eli Lilly and Company, Johnson & Johnson, Bayer, Bluebird Bio, GlaxoSmithKline (GSK), Teva Pharmaceutical Industries, Cipla, and Sun Pharmaceutical Industries, along with regional generics manufacturers.