- Medical Devices

- Radiation Monitoring Safety Market

Radiation Monitoring Safety Market Size, Share, and Growth Forecast, 2025 - 2032

Radiation Monitoring Safety Market by Product Type (Area Process Monitors, Personal Dosimeters, Environmental Radiation Monitors, Surface Contamination Monitors, Radiation Detection & Measurement Instruments, Radiation Safety Accessories), Technology (Gas-filled Detectors, Scintillators, Solid-State Detectors), Application, End-use, and Regional Analysis for 2025 - 2032

Radiation Monitoring Safety Market Size and Trends Analysis

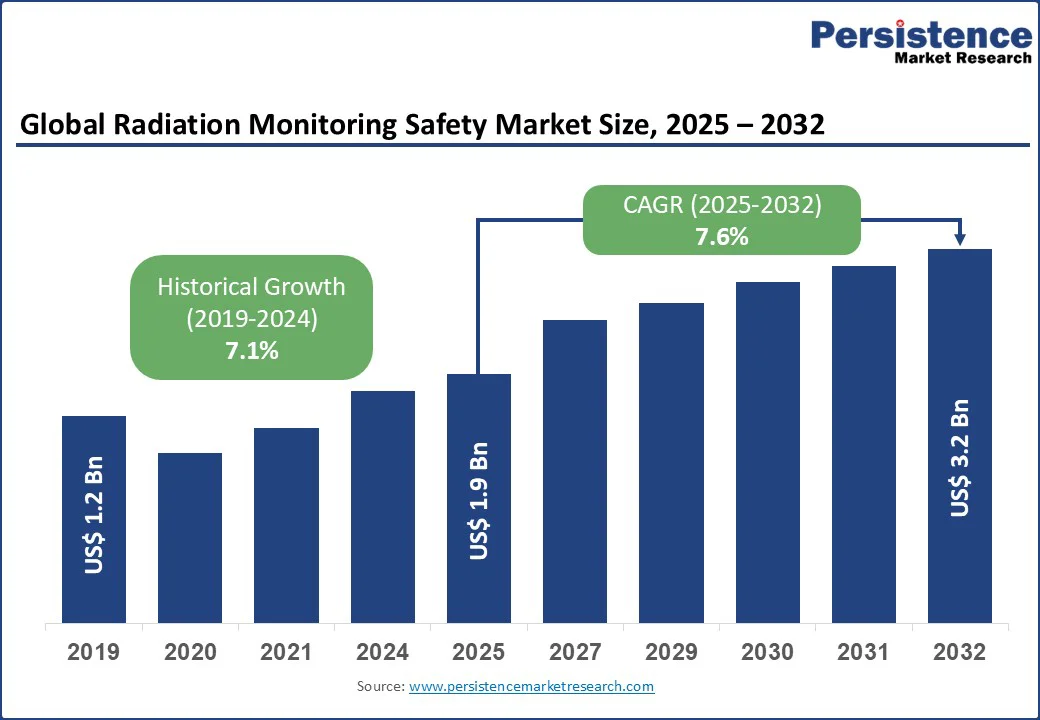

The global radiation monitoring safety market size is likely to be valued at US$ 1.9 Bn in 2025 and expected to reach US$ 3.2 Bn by 2032, registering a CAGR of 7.6% during the forecast period from 2025 to 2032 due to the increasing demand for advanced radiation detection and monitoring systems driven by rising cancer incidences, nuclear power expansion, and heightened global security concerns.

Key Industry Highlights:

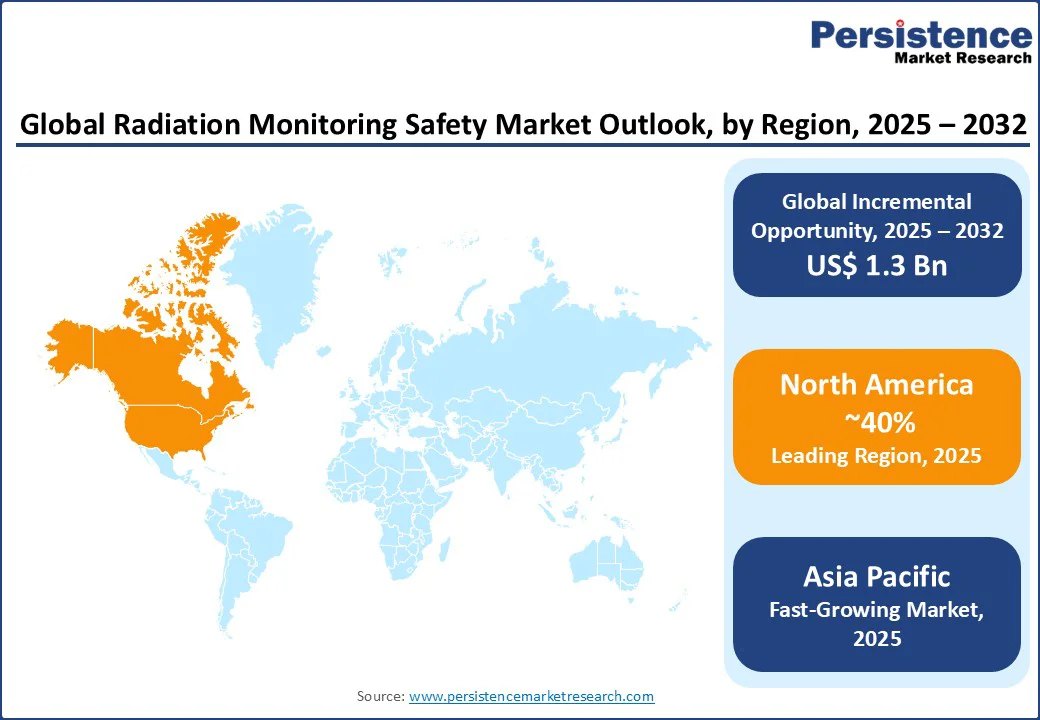

- Leading Region: North America accounts for a 40% share in 2025, driven by advanced healthcare infrastructure and stringent regulations in the U.S.

- Fastest-growing Region: Asia Pacific, propelled by nuclear power expansion and healthcare investments in China and India.

- Dominant Product Type: Personal Dosimeters, commanding 35% market share, due to their critical role in healthcare and nuclear facilities.

- Leading Application: Healthcare, accounting for 40% of market revenue, driven by rising radiation therapy and diagnostic imaging.

- Fastest-growing Technology: Solid-State Detectors, due to advancements in miniaturization and sensitivity.

- Market Opportunity: AI and IoT integration, enhancing real-time monitoring and creating new revenue streams.

| Key Insights | Details |

|---|---|

| Radiation Monitoring Safety Market Size (2025E) | US$ 1.9 Bn |

| Market Value Forecast (2032F) | US$ 3.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.1% |

Market Dynamics

Drivers: Rising Prevalence of Cancer and Radiation Therapy Adoption

The global surge in cancer cases, with 19.3 Mn new diagnoses in 2025, has significantly increased the adoption of radiation therapy, necessitating advanced monitoring systems to ensure patient and worker safety. Approximately 50% of cancer patients undergo radiation therapy, driving a 25% increase in personal dosimeter usage in hospitals globally.

Companies such as Thermo Fisher Scientific and Mirion Technologies have reported a 20% surge in demand for radiation monitoring devices in healthcare settings, particularly for X-ray, CT scan, and nuclear medicine procedures.

Stringent regulations, such as the U.S. Nuclear Regulatory Commission’s (NRC) ALARA principle, mandate precise dose monitoring, boosting sales of radiation detection equipment by 30% in North America since 2020. The growing use of radiopharmaceuticals, with a market value of US$ 7.5 Bn in 2025, further amplifies the need for real-time monitoring, making this a key driver for the radiation monitoring safety market.

Restraints: High Costs and Regulatory Complexity

Advanced radiation monitoring systems, such as solid-state detectors costing US$ 5,000-10,000 per unit, are prohibitively expensive for small-scale healthcare facilities and industries in developing regions.

The high cost of compliance with stringent regulations, governed by bodies such as the International Atomic Energy Agency (IAEA) and the U.S. FDA, increases operational expenses by 15%, with certification processes delaying product launches by up to 18 months.

For example, compliance with the FDA’s 21 CFR Part 11 standards requires significant investment in validation, limiting adoption in cost-sensitive markets such as Sub-Saharan Africa and parts of South Asia.

Opportunities: Integration of AI and IoT in Radiation Monitoring

The integration of artificial intelligence (AI) and Internet of Things (IoT) technologies offers transformative opportunities for the radiation monitoring safety market. The global IoT in healthcare market has applications in real-time radiation monitoring. Mirion Technologies’ Apex-Guard™ Software, launched in 2025, uses AI to enhance radionuclidic purity analysis by 30%, improving efficiency in radiopharmaceutical applications.

IoT-enabled devices, such as Thermo Fisher Scientific’s NetDose Pro digital dosimeter, reduce human error by 25% through remote monitoring capabilities. These advancements are expected to create a US$ 500 Mn revenue opportunity by 2032, particularly in the Asia Pacific, where smart technology adoption is growing at 15% annually, driven by healthcare and nuclear power investments.

Category-wise Analysis

Product Type Insights

Personal Dosimeters dominate the radiation monitoring safety market, expected to account for approximately 35% share in 2025. Their dominance stems from their critical role in monitoring individual radiation exposure in high-risk environments such as hospitals and nuclear facilities.

The segment’s growth is supported by the increasing use of radiation in medical diagnostics, with 40 Mn nuclear medicine procedures annually, and in nuclear power plants, where worker safety is paramount.

Environmental radiation monitors are the fastest-growing segment. These monitors, used to measure radiation in air, water, and soil, are driven by growing environmental concerns and regulatory mandates. Post-disaster monitoring (e.g., Fukushima) and nuclear power expansion, with China aiming for 200 GWe by 2035, fuel growth. Innovations in portable environmental monitors, offering 30% higher sensitivity, further accelerate adoption.

Technology Insights

Gas-filled Detectors dominate the technology segment, commanding approximately 50% share in 2025. Their leadership is attributed to their cost-effectiveness, portability, and accuracy in detecting gamma and beta radiation. Their ability to measure high radiation levels with costs as low as US$ 500 per unit makes them indispensable in industrial and medical applications, particularly in North America, where 80% of nuclear facilities use gas-filled detectors.

Solid-state detectors are the fastest-growing technology segment. Advancements in miniaturization and sensitivity, with devices offering 30% better resolution than gas-filled alternatives, drive growth. The U.S. Department of Defense’s US$ 2 Bn investment in advanced detection technologies in 2025 further supports adoption, particularly in portable and wearable formats.

Application Insights

Healthcare leads the application segment, holding a 40% share in 2025. The segment’s dominance is driven by the rising use of radiation in diagnostics and therapy, with 40 Mn nuclear medicine procedures performed globally in 2025. Regulations such as the FDA’s radiation protection guidelines mandate monitoring in 95% of U.S. hospitals, supporting growth in this segment.

Homeland Security & Defense is the fastest-growing application. Growing concerns over radiological threats and nuclear terrorism have increased investments in radiation detection by 35% since 2020, with the U.S. Department of Homeland Security allocating US$ 1.5 Bn in 2025 for airport and border security.

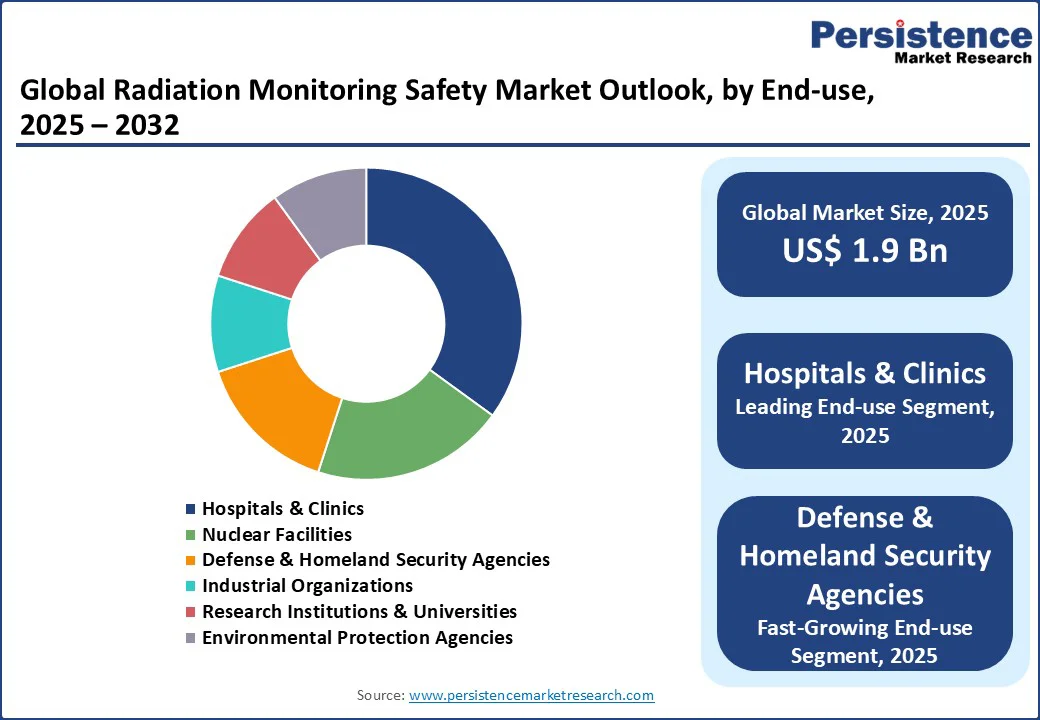

End-use Insights

Hospitals & Clinics dominate the end-use segment, holding a 35% share in 2025. The segment’s leadership is driven by the widespread use of radiation in diagnostics and cancer treatment. The segment benefits from the rising prevalence of cancer, with 50% of patients requiring radiation therapy, driving demand for personal dosimeters and area monitors.

Defense & Homeland Security Agencies is the fastest-growing end-use segment, fueled by global investments in border security, nuclear threat detection, and emergency preparedness. Governments are increasingly deploying radiation detection systems at airports, seaports, and public spaces to counter radiological threats, driving rapid growth.

Regional Insights

North America Radiation Monitoring Safety Market Trends

North America dominates the radiation monitoring safety market, likely to account for a 40% share in 2025, driven by advanced healthcare infrastructure, stringent regulatory frameworks, and significant defense investments. The U.S., accounting for 75% of the region’s market, invested US$ 1.5 Bn in radiation safety for healthcare and defense in 2025, with the NRC mandating monitoring in 90% of radiation-prone facilities.

Companies such as Thermo Fisher Scientific and Fortive (Fluke Biomedical) hold a 30% combined market share, supplying personal dosimeters and area monitors to hospitals and nuclear facilities. Canada’s nuclear power sector, with 19 operational reactors, drives a 10% increase in environmental monitor sales, supported by regulations such as the Canadian Nuclear Safety Commission’s safety standards.

The region is fueled by consumer awareness of radiation risks and government funding for security and healthcare infrastructure.

Europe Radiation Monitoring Safety Market Trends

Europe holds a 30% market share in 2025, led by Germany, France, and the U.K. Germany’s Federal Office for Radiation Protection enforces stringent regulations, driving a 20% increase in personal dosimeter adoption, with Ludlum Measurements and RaySafe leading supply.

France’s nuclear power sector, contributing 70% of its electricity, fuels a 15% rise in area process monitor demand, with Canberra Industries reporting a 25% sales increase in 2025.

The EU’s Radiation Protection Directives mandate monitoring in 95% of nuclear facilities, supporting a regional CAGR of 7.5%. Innovations such as Mirion’s InstadoseVUE dosimeter, offering cloud-based dose tracking, enhance adoption in healthcare and industrial applications, particularly in Germany’s medical imaging sector, which accounts for 50% of the region’s demand.

Asia Pacific Radiation Monitoring Safety Market Trends

Asia Pacific is the fastest-growing region, holding a 25% share in 2025. China and India lead due to nuclear power expansion and healthcare investments. China’s goal of 200 GWe nuclear capacity by 2035 drives a 30% increase in environmental monitor demand, with Fuji Electric and Polimaster supplying advanced systems.

India’s healthcare sector, valued at US$ 150 Bn in 2025, boosts personal dosimeter adoption by 20%, supported by the Atomic Energy Regulatory Board’s safety mandates. Japan’s post-Fukushima monitoring programs and South Korea’s nuclear facility upgrades further drive demand, with companies such as Ametek ORTEC reporting a 15% sales increase.

Government investments, such as China’s US$ 2 Bn nuclear safety fund, and rising cancer treatment needs fuel the region’s growth.

Competitive Landscape

The global radiation monitoring safety market is highly competitive, with key players including Mirion Technologies, Thermo Fisher Scientific, Fortive (Fluke Biomedical, Landauer, RaySafe), Ludlum Measurements, Fuji Electric, and Ametek ORTEC. These companies hold over 70% of the market share, leveraging innovation, strategic partnerships, and global distribution networks to maintain leadership.

Key players focus on R&D to develop AI and IoT-integrated devices, with Mirion Technologies investing US$ 50 Mn in 2025 for smart dosimetry solutions. Strategic partnerships, such as Thermo Fisher Scientific’s collaboration with cancer treatment centers, enhance market reach.

Acquisitions, such as Fortive’s purchase of a dosimetry technology firm in 2025, strengthen portfolios. Regional expansion, with Fuji Electric scaling production in the Asia Pacific, and sustainability initiatives, such as Ametek ORTEC’s eco-friendly detectors, ensure competitiveness.

Key Developments:

- June 2024: Thermo Fisher Scientific launched the NetDose Pro, a wearable digital dosimeter that uses IoT to provide real-time radiation monitoring for healthcare workers, enabling them to track personal exposure risk and improve safety protocols. This device transmits data wirelessly to a mobile app or web interface, eliminating the need for manual collection and processing of traditional dosimeters, which increases operational efficiency and reduces costs for healthcare facilities

- May 2025: Salus Scientific Corporation's launch of its PeRM program for healthcare professionals, the UAE's launch of a national radiation monitoring system for telecom safety, and the ongoing global market growth for radiation detection, monitoring, and safety solutions driven by stricter safety standards and security concerns.

Companies Covered in Radiation Monitoring Safety Market

- Mirion Technologies

- Thermo Fisher Scientific

- Fortive (Fluke Biomedical, Landauer, RaySafe)

- Ludlum Measurements

- Fuji Electric

- Ametek ORTEC

- Canberra Industries

- Radiation Detection Company (RDC)

- Polimaster

- HI-Q Environmental Products

- TG Technical Services

- General Atomics

Frequently Asked Questions

The global radiation monitoring safety market is projected to reach US$ 1.9 Bn in 2025.

Rising cancer incidences, nuclear power expansion, and homeland security needs drive the market.

The market is expected to grow at a CAGR of 7.6% from 2025 to 2032.

AI and IoT integration in monitoring systems offer significant growth potential.

Key players include Mirion Technologies, Thermo Fisher Scientific, Fortive, Ludlum Measurements, and Fuji Electric.