- Communication Infrastructure & Services

- Printed Signage Market

Printed Signage Market Size, Share, and Growth Forecast, 2025 - 2032

Printed Signage Market By Product Type (Billboards & Outdoor, Backlit, Others), Print Technology (Large-format Inkjet, Screen/Offset, Others), End-user, and Regional Analysis for 2025 - 2032

Printed Signage Market Size and Trends Analysis

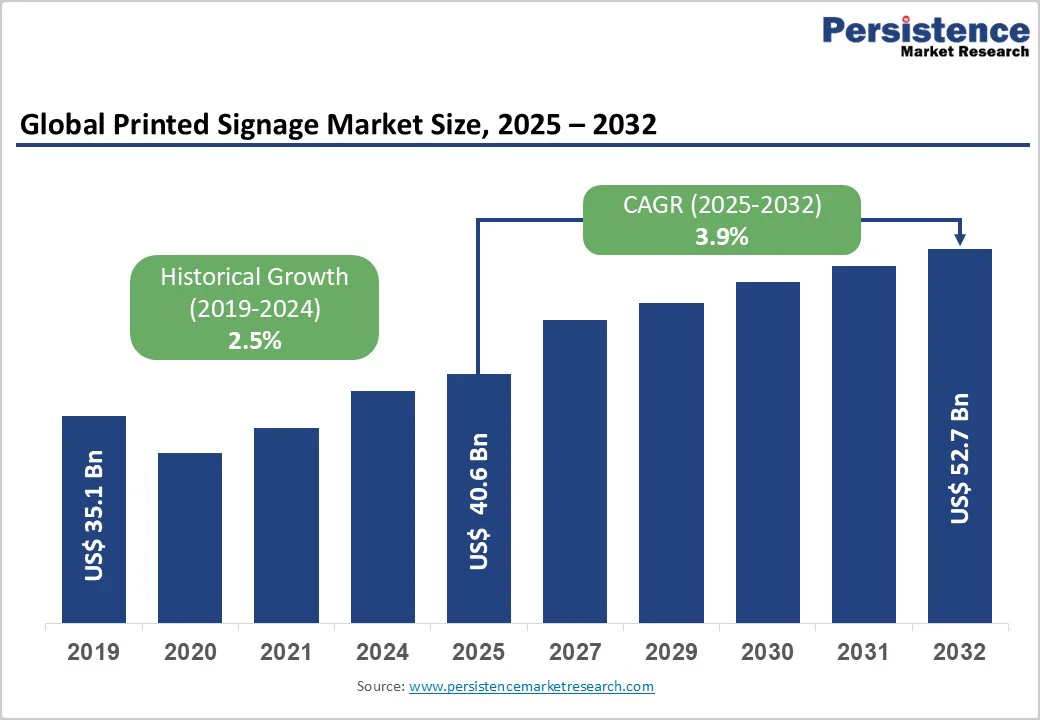

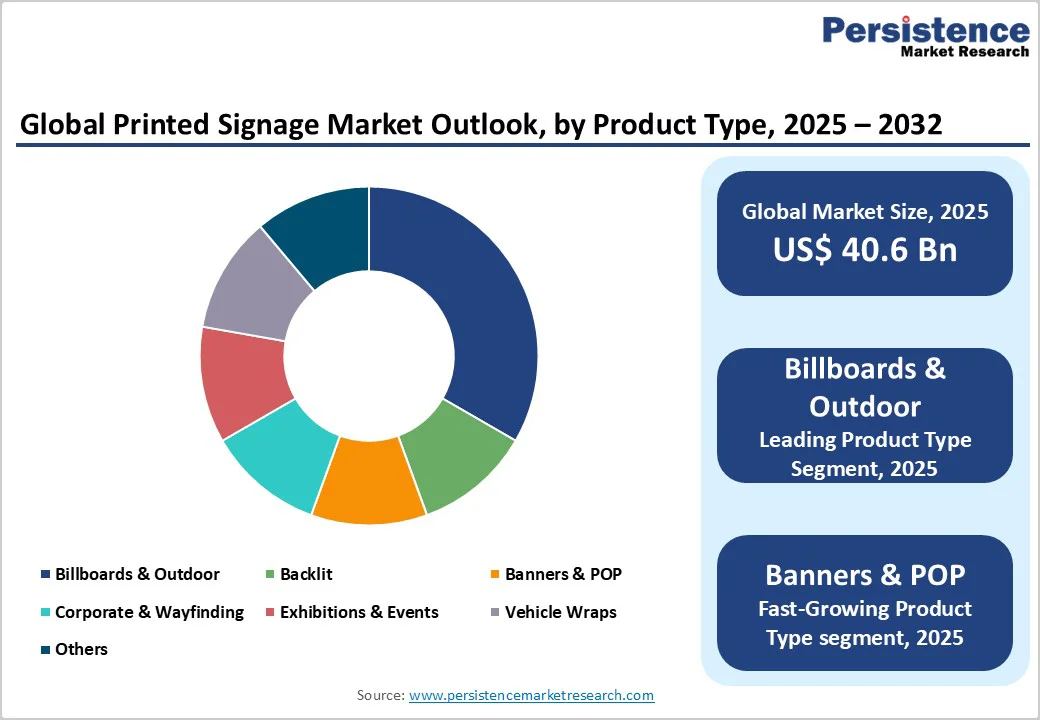

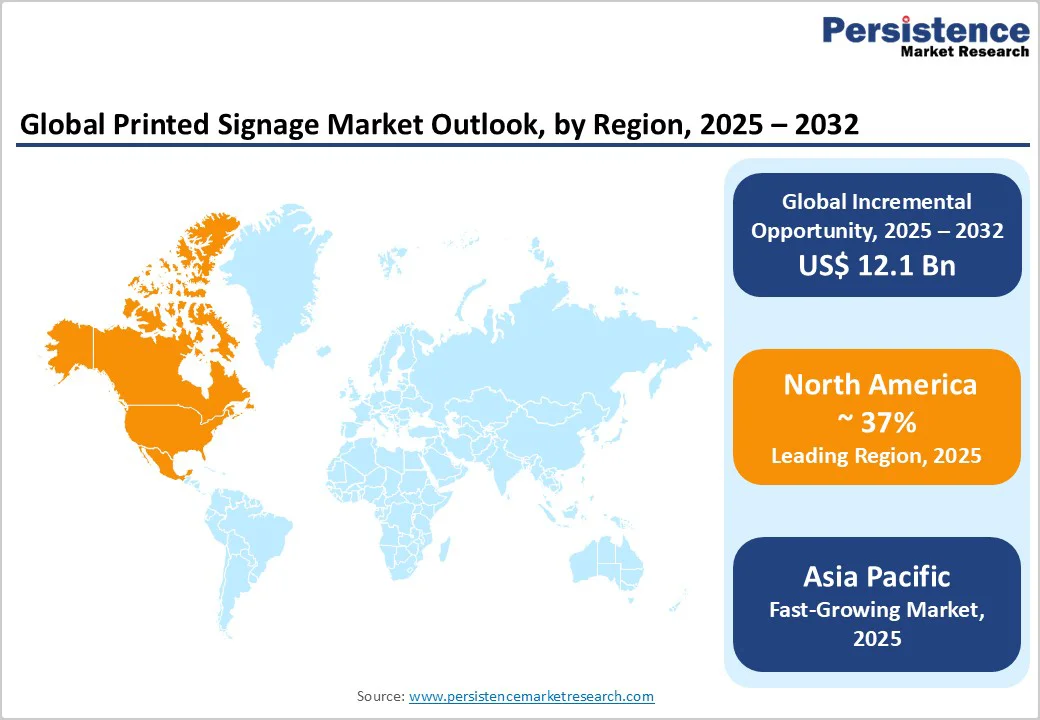

The global printed signage market size is likely to be valued at US$40.6 Billion in 2025 and is expected to reach US$52.7 Billion by 2032, growing at a CAGR of 3.9% during the forecast period from 2025 to 2032, driven by steady baseline demand from retail, outdoor advertising, and corporate wayfinding, supported by ongoing cost declines in digital/inkjet printing and growth in recyclable substrates, underpins stable mid-single-digit expansion.

The printed signage market is a mature but steady-growth sector driven by retail refresh cycles, outdoor advertising, and rising demand for short-run POP and event graphics. It’s shaped by the balance between durable long-life displays and fast, personalized print runs, while sustainability and print-to-store fulfillment models are reshaping supplier economics.

Key Industry Highlights

- Leading Region: North America, holding an estimated 37% share of the market, supported by strong retail networks and consistent billboard and POP display replacement cycles.

- Fastest-growing Region: Asia Pacific, driven by rapid urbanization, growing modern retail, political campaign volumes, and infrastructure-led advertising.

- Investment Plans: Notable regional investments include automation upgrades, cloud-based ordering systems, eco-friendly substrate expansion, and the establishment of new textile-printing and hybrid-printer manufacturing hubs, representing an estimated 6-7% annual capital expenditure growth across suppliers.

- Dominant Product Type: Billboards & outdoor lead the market with an estimated 33% share, owing to high material intensity, extensive installation requirements, and long-duration campaigns.

- Leading Print Technology: Large-format inkjet dominates with nearly 56% share, supported by wide substrate compatibility, fast turnaround, and ongoing hardware upgrades.

| Key Insights | Details |

|---|---|

| Printed Signage Market Size (2025E) | US$40.6 Bn |

| Market Value Forecast (2032F) | US$52.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Retail and POP Re-Investment

Retailers continue investing in in-store branding, seasonal promotions, and experiential activations, each dependent on printed POP, banners, and backlit displays. Physical stores rely on printed signage to guide navigation, influence conversion rates, and maintain visual identity. Store refresh cycles, new formats, and promotional calendars create recurring demand.

Retail and advertising remain the highest-consumption end-use areas and underpin the stability of demand. Consistent replenishment of graphics, combined with rapid campaign turnover, supports short-run digital print volumes that often deliver higher margins and faster throughput for suppliers.

Cost Decreases and Accessibility of Large-Format Digital Printing

Advances in inkjet printheads, UV-curable inks, and automated finishing systems have sharply reduced per-unit production costs. This makes personalized, localized, and rapid-turnaround signage more accessible to small and mid-sized customers.

Lower capital requirements for equipment allow print shops to expand capacity without long lead times, accelerating the shift from traditional screen printing to short-run digital formats. Market activity in large-format printers shows multi-billion-dollar annual demand with stable mid-single-digit growth expectations, indicating consistent investment in expanding signage production hardware.

Sustainability and Recyclable Substrates

Regulatory pressure and brand sustainability mandates are accelerating the adoption of recyclable, PVC-free, and reusable materials. Retailers and public sector buyers increasingly incorporate end-of-life criteria into procurement. New product lines, including biodegradable banner materials and water-based or latex ink systems, are gaining traction in national tenders.

Suppliers offering certified recyclable substrates and closed-loop programs tend to secure longer-term contracts with large buyers, increasing account stickiness and average deal value. This shift is reshaping R&D, procurement criteria, and pricing tiers across the signage ecosystem.

Barrier Analysis - Digital Signage Substitution and Budget Shift

Digital displays continue to capture advertising budgets in high-traffic environments where dynamic content, remote updates, and analytics provide measurable ROI. While upfront capital costs for LED/LCD installations are high, recurring revenue models and programmatic capabilities attract brand spending.

Growth in digital signage typically outpaces printed signage, which limits printed-share expansion in sectors such as transport hubs and quick-service restaurants. Printed signage remains critical for cost-sensitive applications, but budget share migration remains a structural constraint.

Raw Material & Logistics Cost Volatility

Fluctuations in substrate and ink prices, especially PVC films, PET media, and specialty papers, combined with periodic logistics bottlenecks, create cost pressure for converters. Many buyers, especially small businesses and public agencies, resist price increases, limiting cost pass-through.

Sudden surges in resin or shipping costs can compress converter margins by several percentage points. These pressures slow investment in new, higher-margin print solutions during uncertain cycles and reduce appetite for short-run premium formats.

Opportunity Analysis - Integration with Omni-channel Retail and Print-To-Store Fulfilment

Growing alignment between digital retail workflows and printed in-store signage enables recurring programmatic print orders rather than episodic purchases. Retailers are integrating signage into automated campaign workflows, linking online promotions with in-store materials.

If even a modest share of retail marketing budgets migrates to subscription-style print contracts, the global upside could reach several hundred million USD in recurring revenue. Print networks that offer API-enabled portals, templated SKUs, and regionalized fulfilment stand to benefit significantly.

Adjacent Product Bundling

Bundling installation, digital enhancements (QR/NFC integrations), recycling take-back services, and graphic design with printed signage boosts contract value and differentiates suppliers. Such bundled services can lift per-project revenue by 15-40%, depending on complexity.

Providers offering certified installation, campaign analytics, and sustainable end-of-life options secure multi-year contracts with national retailers and enterprises. This approach raises switching costs and supports premium positioning.

Category-wise Analysis

Product Type Insights

Billboards and outdoor signage continue to hold the largest share of 33% market value due to their large physical footprint, multi-year durability requirements, and high material consumption. Highway gantries, building wraps, airport façades, and transit shelters rely on reinforced vinyl, mesh fabrics, and rigid boards, which command higher production costs.

Long-duration campaigns, such as political advertising cycles, city branding projects, and large infrastructure announcements, expand the value of this segment. Brands running year-round visibility campaigns, for example, quick-service restaurants or telecom operators, frequently book long-term outdoor placements, reinforcing the segment’s dominance.

POP displays and banners are experiencing the fastest growth as retailers and service brands implement frequent layout refreshes, thematic promotions, and hyperlocal campaigns. Seasonal retail events such as Diwali sales in India, holiday promotions in North America, or back-to-school periods in Europe accelerate short-run demand.

Digital inkjet systems enable rapid production of small batches, making it easier for supermarkets, pharmacies, and mall kiosks to update in-store graphics weekly or monthly. Event organizers and franchise chains increasingly request quick-turnaround banner sets for launches or promotional roadshows, pushing this category’s expansion.

Print Technology Insights

Large-format inkjet printing maintains its leadership, holding a market share of 56% due to high-resolution output, versatile media handling, and shorter delivery cycles. Signage producers use it for diverse applications, including hoardings, wall graphics, transit panels, and storefront displays. Continuous upgrades in printhead technology and workflow automation support higher speeds and lower waste.

For example, print shops serving retail chains often rely on multi-roll inkjet systems to execute overnight refreshes for nationwide price-change campaigns. The technology’s compatibility with foam boards, PVC, self-adhesive vinyl, and textile substrates makes it the preferred backbone of modern signage operations.

Sustainable materials such as PVC-free films, polypropylene-based posters, fiber-based boards, and reusable aluminum composite panels are expanding at a rapid pace. Retailers increasingly specify recyclable signage kits for campaigns, especially in sectors such as fashion, cosmetics, and consumer electronics, where environmental impact is closely monitored.

Some quick-service restaurant chains have shifted to compostable or low-VOC graphics for indoor menu boards and promotional panels. Specialty substrates such as fabric tension systems for exhibitions or backlit eco-films for airports are gaining traction as brands adopt greener procurement standards and aim to reduce campaign waste volumes.

Regional Insights

North America Printed Signage Market Trends - Retail Refurbishment and Political Print Surges

North America remains the largest regional market with a market share of 37%, supported by high advertising intensity, extensive retail footprints, and a mature ecosystem of print providers and installers. The U.S. maintains consistent replacement cycles for POP displays, window graphics, and billboard skins, especially in sectors such as quick-service restaurants, consumer electronics, and automotive retail.

Mexico and Canada contribute rising demand through expanding metropolitan transit networks and increased adoption of digital-to-print hybrid campaigns. Election cycles generate significant surges in short-term yard signs, fleet wraps, and large-format political banners, reinforcing recurring print volumes.

Growth is powered by retail refurbishment, immersive store environments, and expanding infrastructure advertising across airports, rail systems, and urban furniture. The supplier landscape is diverse, with independent sign shops, national franchise printing chains, and major substrate producers participating across the value chain.

Investments are focused on automation upgrades, cloud-based ordering systems, and local fulfilment hubs. Several U.S. providers recently introduced high-speed roll-to-roll printers with reduced ink consumption and integrated color calibration, contributing to accelerated hardware replacement activity across the region.

Europe Printed Signage Market Trends - Sustainability - Driven Signage and PVC-Free Adoption

Europe operates as a regulation-led and sustainability-focused market with strong demand centered in Germany, the U.K., France, and Spain. Retailers, transport operators, and brand agencies increasingly prioritize PVC-free films, recyclable rigid boards, and certified low-VOC printing processes.

Outdoor and indoor advertising volumes remain steady due to dense metropolitan transit systems, retail chains, and cultural events requiring consistent signage renewal. Backlit displays, textile frames, and window graphics are widely adopted across shopping centers and rail networks.

Regional distributors, substrate innovators, and installation specialists form a competitive and interconnected supply landscape. Investment themes include recyclable banner programs, the adoption of water-based ink, take-back schemes for spent graphics, and efficient cross-border logistics hubs.

Recent regional developments include the launch of fiber-based poster substrates for high-street retailers, the expansion of European fabric-printing hubs for exhibition graphics, and the rollout of certified recycling pilots for PVC-free signage materials in key Western European markets.

Asia Pacific Printed Signage Market Trends - Rapid Retail Expansion and High-Volume Production

Asia Pacific represents a dynamic and rapidly expanding market characterized by diverse economic and regulatory environments. China continues to dominate high-volume production and consumption of outdoor signage, driven by extensive transit advertising networks, commercial construction, and city branding initiatives.

Japan leads in precision equipment, advanced print head systems, and advancements in ink chemistry. India contributes strong growth through expanding modern retail, high-frequency promotional cycles, and significant political campaign-led print volumes. ASEAN countries such as Indonesia, Vietnam, and the Philippines show rising adoption of branded retail graphics and transit station advertising as urbanization accelerates.

Regional growth is linked to retail rollouts, infrastructure megaprojects, rising mall development, and the expansion of local manufacturing clusters for printers and substrates. Regulatory frameworks vary, from Japan’s established recycling mandates to emerging sustainability guidelines across Southeast Asia.

Recent developments include new textile-printing facilities launched in India for exhibition and event graphics, expanded distribution networks for eco-friendly substrates in Australia, and the introduction of high-speed hybrid flatbed printers in China targeting both retail and industrial signage requirements.

Competitive Landscape

The global printed signage market is moderately fragmented at the service provider level, dominated by local sign shops and regional converters. In contrast, materials and equipment segments exhibit higher concentration, with major global companies supplying films, rigid substrates, adhesives, and printing hardware.

Substrate distribution and specialty materials lean toward consolidation, while production and installation remain decentralized. National print franchises and integrated service providers are gaining share by offering consistent quality, bundled services, and rapid fulfilment across multiple locations.

Key themes include vertical integration, sustainability-driven product differentiation, and digital workflow enablement. Providers prioritize quick turnaround, certified eco-materials, and bundled installation or analytics services. Automation, online portals, and supply-chain optimization are central to gaining enterprise accounts.

Key Industry Developments

- In June 2025, HP introduced its Latex 730 and 830 large-format printers in India, along with a dedicated demo centre in Mumbai, aiming to boost local signage production with high-quality, low-VOC output.

- In March 2025, Avery Dennison and Maizey Plastics jointly launched a new Ultimate Wrapping Film™, a thick, calendered vinyl with improved conformability, enhanced UV and temperature resistance, and a removable adhesive designed to last up to two years.

- In May 2025, the Media Expo in New Delhi showcased a surge in innovation from India’s MSME-led signage sector, including sustainable substrates (recyclable boards, non-PVC films), UV flatbed printers, and modular exhibition graphics.

Companies Covered in Printed Signage Market

- HP

- Canon

- Epson

- Roland DG

- Mimaki Engineering

- Agfa-Gevaert

- Durst Group

- Ricoh

- Xerox

- 3M

- Avery Dennison

- ORAFOL

- Fujifilm

- Mutoh

- Mactac

- Spandex

- Drytac

- Novus Imaging

- Inktec

- Hexis

Frequently Asked Questions

The global printed signage market is estimated to be US$40.6 Billion in 2025.

By 2032, the printed signage market is projected to reach US$52.7 Billion.

Key trends include growing use of sustainable materials, rapid expansion of POP and event-driven short-run printing, greater automation and cloud-based ordering, wider deployment of large-format inkjet systems, and rising demand from retail refreshes, transit ads, and experiential marketing.

Billboards & outdoor remain the leading segment due to high material usage, large-scale installations, and long-term campaign volumes.

The market is projected to grow at a 3.9% CAGR between 2025 and 2032, supported by steady retail spending, infrastructure-led advertising, and increasing adoption of sustainable substrates.

Major players include HP, Canon, Epson, Roland DG, and Durst Group.