- Specialty & Fine Chemicals

- Potassium Formate Market

Potassium Formate Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Potassium Formate Market by Form (Liquid, Solid), Application (Deicing Agent, Drilling & Completion Fluids, Fertilizer Additives), Industry (Oil & Gas, Construction, Agriculture, Industrial), and Regional Analysis 2025 - 2032

Potassium Formate Market Share and Trends Analysis

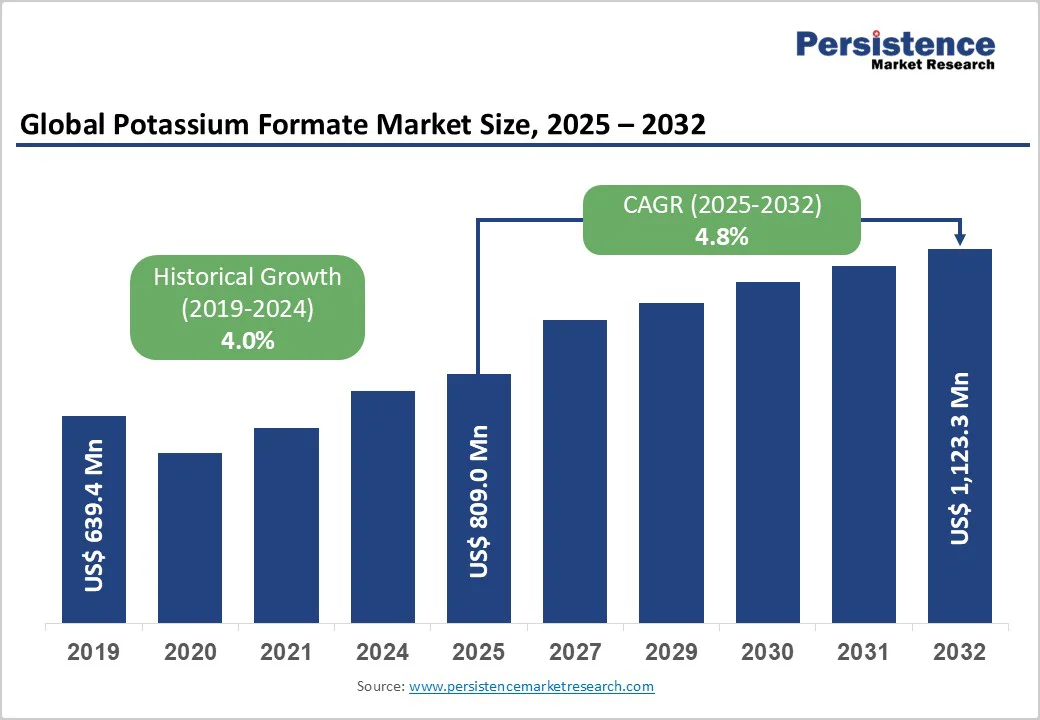

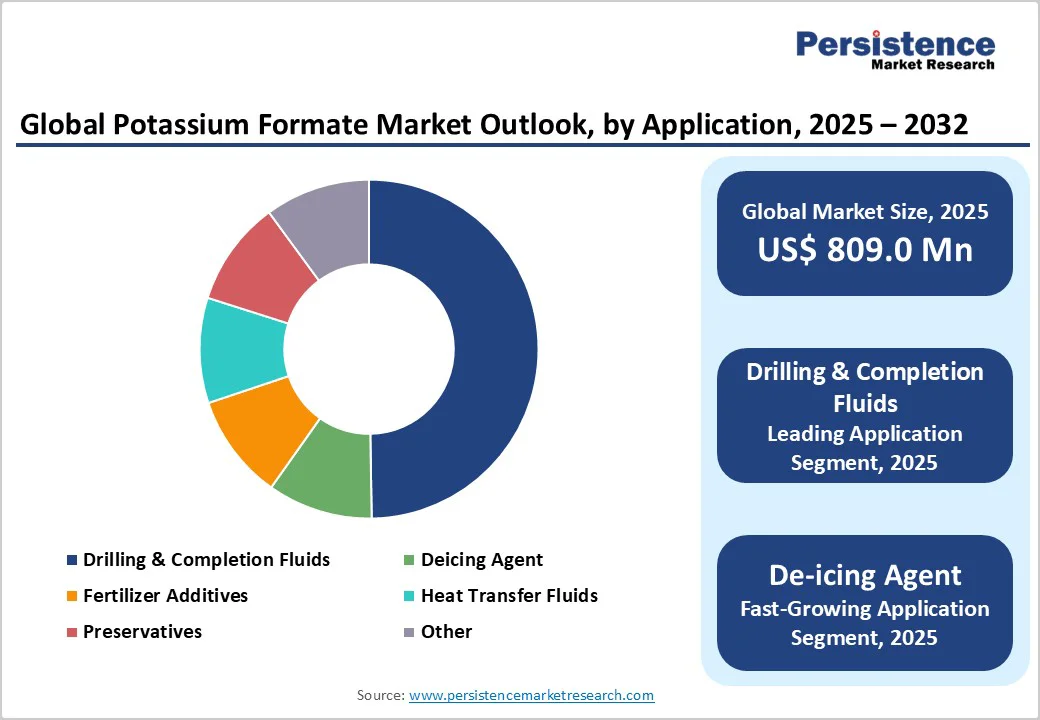

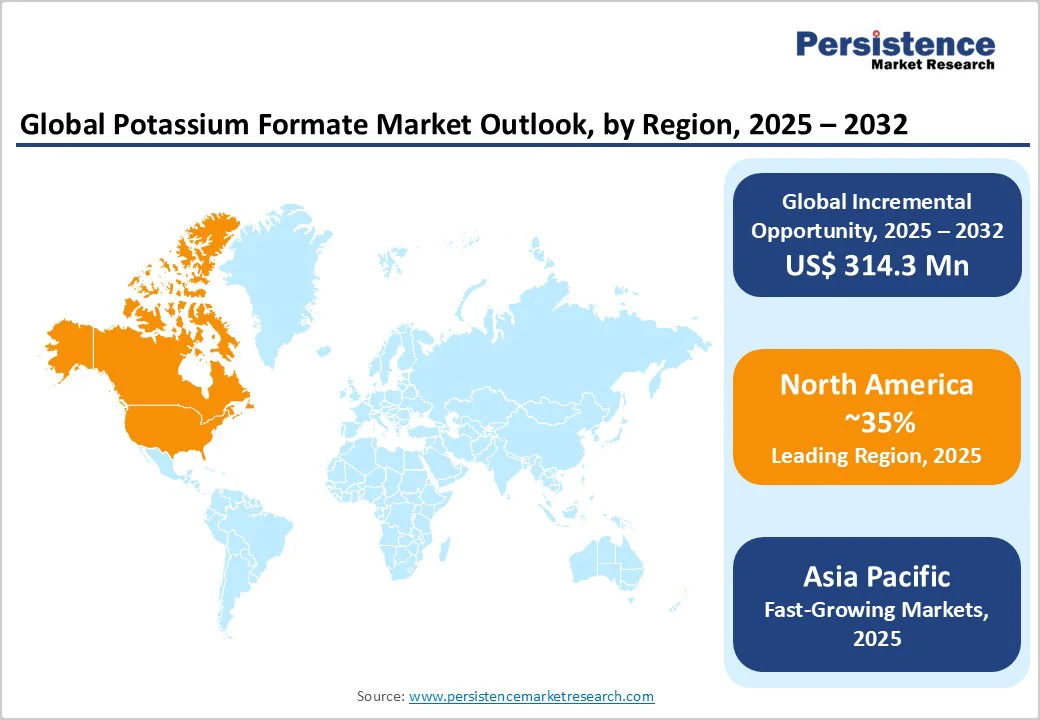

The global potassium formate market size is likely to be valued at US$809.0 Mn in 2025 and is projected to reach US$1,123.3 Mn by 2032, growing at a CAGR of 4.8% between 2025 and 2032.

The market expansion stems from heightened demand for environmentally sustainable chemicals across key sectors like oil and gas extraction and winter infrastructure management.

This growth is underpinned by global drilling activities surging by approximately 5% annually, as reported by energy sector analyses, which favor potassium formate's non-toxic properties over traditional chlorides.

Key Market Highlights:

- Regional Leader: North America leads the Potassium Formate Market due to dominant shale drilling and stringent EPA regulations favoring eco-fluids, capturing over 35% global share with robust U.S. infrastructure support.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, propelled by China's manufacturing surge and India's agricultural subsidies, projecting 6% CAGR through industrial and energy expansions.

- Leading Segment: Liquid form dominates categories with a 70% share, justified by ease in drilling integrations and compliance with API standards for high-density applications.

- Fastest Growing Segment: Drilling & Completion Fluids represent the fastest-growing application, driven by a 15% rise in global exploration, offering superior stability in unconventional wells per IEA trends.

- Growth Opportunity: Key opportunity lies in sustainable agriculture additives, with FAO-backed investments enabling 20% yield boosts and alignment with global green farming policies.

| Key Insights | Details |

|---|---|

| Potassium Formate Market Size (2025E) | US$809.0 Mn |

| Market Value Forecast (2032F) | US$1,123.3 Mn |

| Projected Growth CAGR (2025-2032) | 4.8% |

| Historical Market Growth (2019-2024) | 4.0% |

Market Dynamics

Drivers - Increasing Adoption in Oil & Gas Drilling Operations

The surge in global oil and gas exploration activities is a pivotal driver of the potassium formate market, as the compound serves as a high-density, low-toxicity fluid in drilling and completion processes.

With worldwide energy demand projected to rise by 1.5% annually through 2030, according to International Energy Agency data, potassium formate's superior thermal stability —enduring temperatures up to 150°C without degradation —enables efficient operations in high-pressure, high-temperature wells, particularly in shale formations.

Furthermore, as operators shift toward environmentally compliant fluids amid stricter emissions standards, potassium formate's biodegradability —decomposing over 90% within 28 days per Organization for Economic Co-operation and Development (OECD) guidelines —positions it as a viable alternative to chloride-based brines, fostering cost savings through lower disposal fees and regulatory compliance.

Growing Preference for Eco-Friendly De-Icing Solutions

Environmental regulations and climate variability are accelerating the use of potassium formate as a biodegradable de-icing agent, significantly propelling market momentum in infrastructure-heavy sectors.

Municipalities and airports worldwide face mandates to curb groundwater contamination from traditional salts, with the U.S. Environmental Protection Agency reporting that chloride runoff contributes to 25% of surface water pollution in northern states; potassium formate counters this by offering a non-corrosive option that melts ice at temperatures as low as -50°C while exhibiting zero bioaccumulation risk.

Restraints - Elevated Production Costs and Energy Intensity

High manufacturing costs pose a substantial barrier to the broader adoption of potassium formate, stemming from its energy-intensive synthesis process, which involves reactions between potassium hydroxide and formic acid and requires precise temperature control and specialized equipment to achieve purity levels above 95%.

This results in production costs averaging 20-30% higher than alternatives such as sodium formate, as highlighted in chemical engineering analyses published by the American Chemical Society, where energy consumption reaches 5-7 MJ/kg during the neutralization and crystallization stages.

In volatile energy markets, where natural gas prices fluctuated by 15% in 2024, according to EIA reports, these costs directly inflate end-product pricing, deterring small-scale operators in cost-sensitive regions like Latin America and rendering non-critical applications less competitive.

Raw Material Price Volatility and Supply Chain Disruptions

Fluctuations in key feedstock prices, particularly formic acid derived from methanol synthesis, severely impede the Potassium Formate Market by introducing unpredictability in sourcing and pricing strategies.

Global formic acid prices spiked by 18% in early 2025 due to methanol shortages stemming from Asian petrochemical disruptions, as tracked by ICIS pricing indices, forcing manufacturers to absorb the hikes or pass them on to consumers, eroding competitiveness against cheaper substitutes like calcium chloride in de-icing.

The cost volatility is further intensified by geopolitical tensions affecting 30% of global methanol supply chains, per World Bank commodity outlooks, leading to production halts and inventory shortages that delayed deliveries by 2-4 weeks in affected quarters.

In agriculture and industrial applications, where margins are thin, such instability has led to 10-12% order cancellations among end users, as noted in Deloitte's supply chain resilience studies, further dampening demand forecasts.

Opportunities - Expansion in Sustainable Agriculture and Fertilizer Additives

The rising emphasis on eco-friendly farming practices presents a lucrative opportunity for potassium formate in agriculture, particularly as a potassium source in fertilizers that enhances nutrient uptake without soil salinity buildup.

With global sustainable agriculture investments reaching $25 billion in 2024 per Food and Agriculture Organization (FAO) reports, potassium formate's solubility, up to 300 g/L at 20°C, allows precise application in fertigation systems, improving crop yields by 10-15% for high-value produce such as fruits and vegetables, as demonstrated in trials by the International Fertilizer Association.

This aligns with policies like the EU's Farm to Fork Strategy, which mandates a 20% reduction in chemical runoff by 2030, positioning the compound as a compliant additive that boosts soil health and reduces leaching by 40% compared to conventional potash salts.

In Asia Pacific, where arable land pressure drives 8% annual growth in fertilizer demand, opportunities arise from government subsidies in India and China for bio-based inputs, enabling market players to capture a 15% share in the segment through partnerships with agrotech firms.

By leveraging these trends, companies can tap into a $50 billion global fertilizer additives space, fostering long-term demand through value-added solutions that support regenerative agriculture goals.

Advancements in Heat Transfer Fluids for Renewable Energy

Potassium formate's thermal properties offer substantial growth potential in the heat transfer fluids sector, especially for renewable energy applications like solar thermal and geothermal systems, amid a global push for carbon-neutral technologies.

In North America, U.S. Department of Energy grants for geothermal exploration, valued at $150 million in 2025, create avenues for customized formulations, with companies like Dynalene Inc. pioneering biodegradable blends that comply with NSF/ANSI standards for closed-loop systems.

The International Renewable Energy Agency forecasts a 12% CAGR for heat transfer markets through 2030, driven by installations exceeding 1,000 GW in concentrated solar power. Potassium formate's high boiling point and low viscosity ensure efficient heat transfer with 95% energy retention, outperforming glycols in extreme conditions per ASME engineering standards.

This opportunity intensifies in the Heat Transfer Fluids Market, with Europe's Green Deal allocating €1 trillion for clean energy transitions, incentivizing non-toxic fluids that reduce system corrosion by 50% and extend equipment life by 5 years, as evidenced by pilot projects in Spain's solar farms.

Category-wise Insights

Form Analysis

The liquid form dominates with a 70% share, attributed to its superior handling and application versatility in high-volume industrial settings. Liquid potassium formate, often supplied as brines with densities up to 1.5 g/cm³, facilitates seamless integration into drilling operations and de-icing sprays, reducing preparation time by 50% compared to solids, as per the American Oil Chemists' Society's chemical processing guidelines.

Furthermore, in aviation de-icing, liquid variants meet SAE AMS 1435 standards for aircraft safety, with adoption rates climbing 25% in FAA-certified facilities due to faster application and lower residue buildup. Environmental assessments from the EPA further bolster its position, noting 95% biodegradability that aligns with zero-discharge policies, driving preference over powdered forms prone to dusting and storage issues.

Application Analysis

Drilling & Completion Fluids lead the application segments in the Potassium Formate Market with around 50% market share, driven by its critical role in enhancing wellbore stability during extraction activities. This segment's prominence is rooted in potassium formate's ability to provide densities from 1.2 to 2.3 g/cm³ without solids, preventing clay swelling in shale reservoirs and improving drilling rates by 20%, as documented in SPE journal case studies from Permian Basin operations.

The IEA data show 4 million new wells drilled annually, with formate-based fluids reducing environmental discharge by 70% compared with traditional muds and complying with OSPAR offshore regulations. In the Drilling Fluids Market, its non-corrosive nature extends tubular life by 30%, making it indispensable for high-pressure environments, as evidenced by its use in 40% of North Sea projects in operator surveys.

Industry Analysis

The Oil & Gas industry holds the largest share in the Potassium Formate Market at about 55%, driven by its indispensable role in exploration and production workflows. This dominance is substantiated by the sector's reliance on potassium formate for clear brines that inhibit formation damage while maintaining hydrostatic balance, with API RP 13B tests confirming 90% less permeability impairment than potassium chloride systems.

The study from the U.S. Energy Information Administration indicates 15% growth in U.S. shale output since 2023, amplifying demand for such fluids in hydraulic fracturing, where they reduce water usage by 25% and enhance recovery rates to 35% of reserves. In offshore settings, its low toxicity profile, classified as PLONOR by the OSPAR Commission, facilitates compliance in sensitive marine areas, adopted in 50% of Gulf of Mexico completions per regulatory filings.

Regional Insights

North America Potassium Formate Trends

North America's potassium formate market is spearheaded by the U.S., where shale revolution dynamics and robust regulatory frameworks drive innovation in drilling technologies.

The EPA's 2024 updates to effluent guidelines have accelerated shifts to low-toxicity fluids, with potassium formate accounting for 40% of Permian Basin applications, enhancing well productivity by 18% according to DOE field data. This leadership fosters an ecosystem of R&D hubs, like those in Texas, focused on bio-based variants to meet Clean Water Act standards and reduce environmental liabilities.

Infrastructure resilience further bolsters trends, with FAA mandates for eco-deicers at 200+ airports driving 30% uptake of liquid formulations, mitigating corrosion in harsh winters while aligning with state sustainability goals.

Europe Potassium Formate Trends

Europe's Potassium Formate Market exhibits strong performance across Germany, the U.K., France, and Spain, driven by REACH regulations that promote non-hazardous chemicals in industrial applications.

In de-icing, Nordic countries like Sweden have integrated it into 70% of highway protocols since 2024, per EEA environmental audits, cutting chloride emissions by 50% and supporting EU Green Deal targets for zero-pollution mobility. Germany's chemical sector leverages it in heat transfer for renewables, with Fraunhofer Institute studies showing 15% efficiency gains in solar plants.

Regulatory convergence via ECHA classifications accelerates adoption in construction, where U.K. infrastructure projects use it as a concrete accelerator, complying with BS EN 934 standards and reducing curing times by 20% amid post-Brexit supply chain optimizations. This unified approach enhances market cohesion and growth.

Asia Pacific Potassium Formate Trends

Asia Pacific potassium formate market thrives on manufacturing prowess in China, Japan, India, and ASEAN, with rapid industrialization fueling demand in oil & gas and agriculture.

China's 14th Five-Year Plan has boosted drilling in Bohai Bay, incorporating potassium formate in 35% of operations for its stability, per CNPC reports, supporting 10% annual output growth while adhering to MEP emission controls. India's fertilizer subsidies under the PM-KISAN drive have driven 12% uptake of additives, enhancing soil potassium levels by 25% in rice paddies, as validated by ICAR trials.

ASEAN's energy transition, exemplified by Indonesia's geothermal expansions, uses it in heat fluids to achieve 20 GW targets by 2030, leveraging cost advantages from local formic acid production to achieve 15% lower system costs per IRENA assessments. These dynamics position the region for accelerated expansion.

Competitive Landscape

The global potassium formate Market displays a consolidated structure. Key companies prioritize R&D for bio-based variants and capacity expansions, as seen in Asia Pacific investments exceeding $200 million in 2024, focusing on purity enhancements for niche applications.

Key differentiators include sustainability certifications like ISCC PLUS, enabling premium pricing in regulated markets, while emerging models emphasize circular economy approaches, such as wastewater recycling, to cut costs by 20%.

Key Market Developments

- January, 2024: Perstorp Holding AB launched 'Formate 2025' initiative, utilizing CO2 capture for carbon-negative production, reducing emissions by 4.2 tons per ton.

- May 2025: ADDCON GmbH introduced a high-purity formulation via cascade purification, slashing waste by 50% and targeting pharmaceutical applications.

- September 2024: Clariant expanded brine production capacity in Europe by 20%, enhancing supply for de-icing amid regulatory shifts.

Top Companies in Potassium Formate Market

- Perstorp Holding AB (Sweden) leads with a diverse portfolio in specialty chemicals, generating over $2 billion in annual revenue through innovations in sustainable formates for drilling and agriculture, backed by strong R&D investments.

- Clariant (Switzerland) excels in additives via eco-friendly brines. It $6.5 billion in revenue reflects maturity in oilfield solutions, with expansions in Asia driving portfolio strength in heat-transfer applications.

- Eastman Chemical Company (USA) dominates North American segments with $9.2 billion in revenue, leveraging integrated supply chains for high-purity grades used in de-icing, emphasizing reliability and compliance in industrial end-uses.

Companies Covered in Potassium Formate Market

- Perstorp Holding AB

- Clariant

- Thermo Fisher Scientific Inc

- Eastman Chemical Company

- Hawkins

- Weifang Tainuo Chemical Co., Ltd.

- Honeywell International Inc.

- Dongying Shuntong Chemical (Group) Co., Ltd.

- Sidley Chemical Co., Ltd.

- Dynalene Inc.

- ADDCON GmbH

- BASF SE

- Tetra Technologies, Inc.

Frequently Asked Questions

The market is valued at US$ 809.0 Mn in 2025 and expected to reach US$ 1,123.3 Mn by 2032, reflecting a 4.8% CAGR driven by eco-friendly applications in energy and infrastructure.

Key drivers include rising oil & gas drilling needs for non-toxic fluids and adoption of biodegradable de-icers, supported by regulations like EPA guidelines that promote sustainable alternatives over chlorides.

Drilling & Completion Fluids hold the lead with 50% share, due to their role in stabilizing wells and complying with API standards in unconventional extraction.

North America leads, powered by U.S. shale activities and DOE-backed innovations, accounting for over 35% share through regulatory-favored eco-fluids.

Expansion in heat transfer fluids for renewables offers significant potential, aligning with IRENA forecasts for 12% growth in solar applications via efficient, non-corrosive properties.

Leading players include Perstorp Holding AB, Clariant, and Eastman Chemical Company, dominating through R&D in sustainable formulations and strong supply chains in energy sectors.