- Non-food Packaging

- Plantable Packaging Market

Plantable Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Plantable Packaging Market by Materials (Bioplastics, Paper, Others), Packaging Type (Flexible, Bags & Pouches, Others), Applications, and Regional Analysis for 2026 - 2033

Plantable Packaging Market Size and Trends Analysis

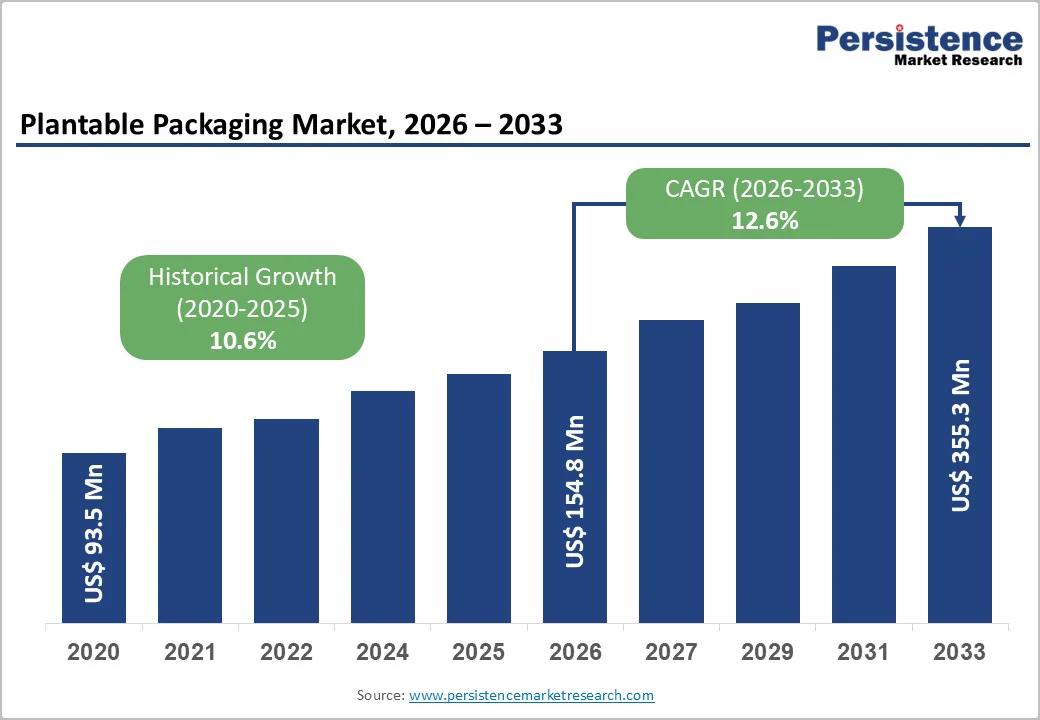

The global plantable packaging market size is likely to be valued at US$154.8 million in 2026 and is expected to reach US$355.3 million by 2033, growing at a CAGR of 12.6% between 2026 and 2033, driven by tightening regulations on single-use plastics, rising consumer demand for circular and regenerative packaging solutions, and ongoing improvements in seed-embedded and bio-based material technologies that enhance functional performance and cost efficiency.

These trends, combined with expanding composting infrastructure in Europe and policy incentives in Asia Pacific and North America, create strong commercialization opportunities alongside structural scaling challenges.

Key Industry Highlights

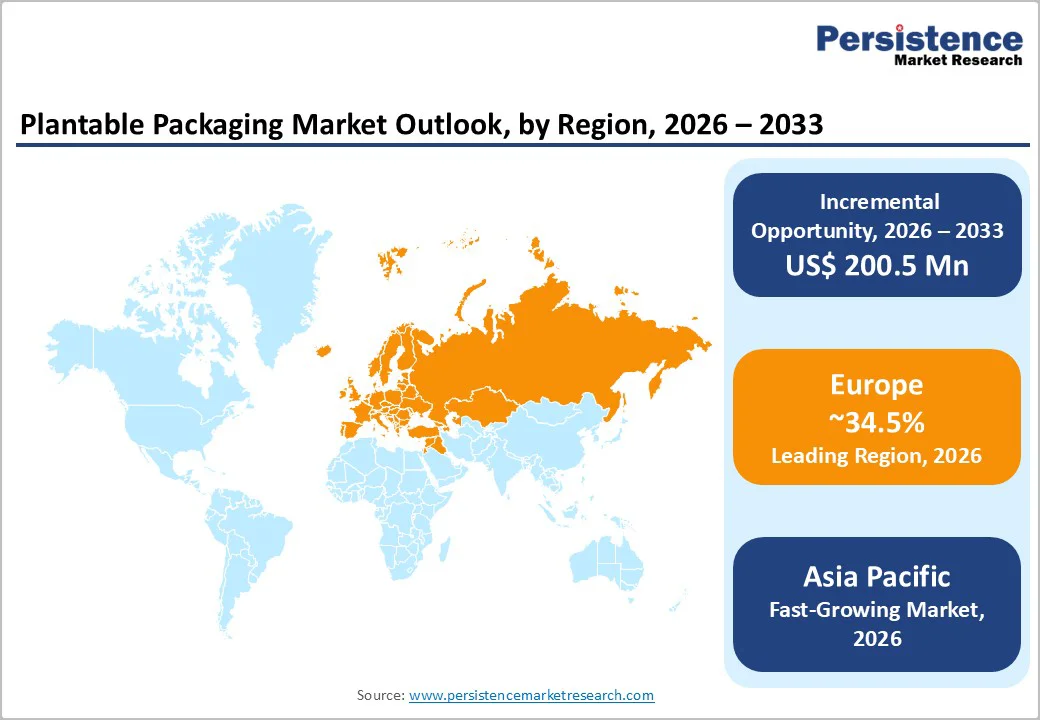

- Leading Region: Europe, projected to account for approximately 34.5% of the global market, driven by strong regulatory frameworks, advanced composting infrastructure, and early adoption of circular packaging mandates.

- Fastest-growing Region: Asia Pacific, estimated to register the highest CAGR, supported by manufacturing scale, access to low-cost biomass, and government-led initiatives to reduce single-use plastic waste.

- Investment Plans: Increasing investments in bio-material innovation and converting capacity, particularly in seaweed-based films and bioplastic compounding. Capacity expansions and partnerships in APAC and Europe are focused on cost reduction and commercial-scale production, with pilot-to-commercial transitions accelerating post-2026.

- Dominant Materials: Bioplastics are anticipated to lead with an estimated 36.4% revenue share, due to strong performance characteristics, scalability, and compatibility with the existing packaging infrastructure.

- Leading Applications: Food and beverage applications, anticipated to hold the largest share at approximately 41.3% of the revenue, driven by high packaging intensity, sustainability commitments, and consumer-facing visibility.

| Key Insights | Details |

|---|---|

| Plantable Packaging Market Size (2026E) | US$154.8 Mn |

| Market Value Forecast (2033F) | US$355.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 12.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Pressure and Circular-Economy Mandates

Regulatory action targeting packaging waste reduction remains a primary driver of plantable packaging adoption. Policies aimed at limiting single-use plastics and improving packaging recyclability and compostability are reshaping procurement priorities across food, retail, and personal care sectors.

Circular-economy frameworks increasingly favor regenerative materials that return value to ecosystems after use, positioning plantable packaging as a compliance-aligned alternative. In Europe, accelerated regulatory timelines are shortening adoption cycles and encouraging early replacement of conventional materials in premium packaging formats.

Market impact includes faster product conversions, increased pilot programs, and broader use of plantable solutions in flexible packaging, gifting, and promotional applications.

Consumer Demand for Traceable, Experiential Sustainability

Consumers are increasingly favoring packaging that delivers visible and verifiable environmental outcomes. Plantable packaging offers a direct sustainability experience by enabling post-use planting, which strengthens emotional engagement and brand trust. Retail and e-commerce data indicate higher conversion rates and repeat purchases for brands incorporating plantable elements into packaging.

Seed-embedded materials also generate social engagement through user-shared planting results, reinforcing brand visibility. This experiential dimension supports premium pricing, particularly in cosmetics, specialty foods, and direct-to-consumer channels, accelerating adoption among value-driven consumer segments.

Material and Processing Technology Improvements

Advancements in bio-material formulation and manufacturing processes are improving the commercial viability of plantable packaging. Innovations such as seaweed-based films, bio-binders, and improved seed-paper lamination techniques have enhanced moisture resistance, mechanical strength, and storage stability. These improvements have reduced failure rates and expanded use cases beyond novelty items.

Enhanced durability and predictable germination performance now enable plantable materials to be tested in functional packaging formats such as pouches, trays, and wraps, supporting higher-volume commercial trials and long-term supplier contracts.

Barrier Analysis - Scale and Cost Gaps versus Conventional Materials

Despite technological progress, plantable packaging remains more expensive than traditional plastics and paperboard at large production volumes. Higher raw material costs, specialized seed-embedding equipment, and quality control requirements increase capital intensity.

Early adopters report unit costs that remain meaningfully above conventional alternatives, particularly for customized formats. While costs decline with scale, price sensitivity in mass-market and low-margin categories continues to limit widespread adoption, confining most current demand to premium segments.

Certification, Labeling, and End-Of-Life Clarity

Differences between compostable, biodegradable, and plantable claims create complexity for both brands and consumers. Inconsistent standards across regions complicate labeling and disposal instructions, increasing the risk of misinterpretation or regulatory scrutiny.

Brands must invest in third-party validation and clear communication to avoid greenwashing concerns. Failure to address end-of-life clarity can undermine consumer trust and expose companies to reputational and compliance risks, particularly in highly regulated food-contact applications.

Opportunity Analysis - Premium Food and Beverage Substitution

With food and beverage representing the largest application share, plantable packaging offers a clear substitution opportunity in premium product lines. Selective conversion of gift packaging, sample sachets, and specialty product formats can generate meaningful incremental demand.

Even modest penetration within premium FMCG packaging over the forecast period translates into a substantial addressable market. Actionable opportunities lie in targeting high-margin SKUs where sustainability enhances brand value and price sensitivity is lower.

White-Label and B2B Service Models

Brands increasingly seek turnkey solutions rather than developing in-house plantable packaging capabilities. This creates demand for white-label converters offering pre-printed pouches, seed-paper liners, and custom mailers with validated germination performance.

Service-oriented models that combine material supply, printing, certification, and fulfillment can command pricing premiums. Recurring contracts and design services offer attractive margin potential and strengthen long-term brand relationships.

Geographic Expansion in Asia Pacific and Emerging Markets

Asia Pacific presents strong growth potential due to abundant biomass resources, cost-efficient manufacturing, and rising consumer awareness of sustainable packaging. Investments in regional converting hubs and local seed sourcing can significantly reduce costs while improving supply chain resilience.

Establishing production closer to end markets supports faster adoption, particularly in fast-growing retail and foodservice sectors across India, China, and Southeast Asia.

Category-wise Analysis

Materials Insights

Bioplastics are anticipated to be the leading material segment, projected to account for approximately 36.4% of the revenue share in 2026, driven by their strong balance of mechanical performance, scalability, and compatibility with the existing packaging infrastructure. PLA blends and starch-based composites are widely deployed in flexible films, pouches, and coated seed-paper laminates, particularly in food and personal care packaging.

Their near-parity processing requirements allow converters to retrofit conventional extrusion and lamination lines rather than invest in entirely new equipment, reducing capital risk for large brands. This material leadership is reinforced by reliable barrier properties, consistent germination performance when combined with seed layers, and established bio-polymer supply chains.

For example, premium snack brands and direct-to-consumer food startups increasingly use bioplastic-based plantable pouches to balance shelf-life requirements with sustainability goals.

Paper-based plantable materials are likely to represent the fastest-growing segment in the market, supported by low production complexity, high customization potential, and strong consumer appeal. Seed-embedded paper is commonly used in boxes, sleeves, hang tags, inserts, and secondary packaging formats, particularly in gifting, promotional campaigns, and e-commerce shipments.

These materials are easy to print, cut, and assemble using conventional paper-processing equipment, making them accessible to small and mid-sized converters. The segment benefits from high storytelling value, as consumers can directly recycle the packaging after use, reinforcing sustainability claims.

Artisanal food producers, cosmetic sample kits, and eco-conscious subscription brands frequently adopt seed paper for limited-edition launches and seasonal promotions, where emotional engagement and brand differentiation are critical.

Applications Insights

The food and beverage segment is expected to lead, accounting for approximately 41.3% of revenue share, owing to the sector’s high packaging intensity and growing pressure to reduce plastic visibility. Plantable packaging is increasingly used for premium food items such as specialty teas, spices, confectionery, and single-serve condiments, where packaging plays a direct role in brand perception.

Sustainability commitments from food brands and retailers have accelerated trials of seed-embedded cartons, flexible pouches, and secondary wraps. Advances in food-safe bioplastics and seaweed-based films are addressing earlier limitations related to moisture resistance and shelf stability, enabling broader adoption in specialty and premium food categories. Gift packs and promotional bundles remain key entry points for plantable solutions in this segment.

Personal care and cosmetics represent the fastest-growing application segment, driven by strong alignment between sustainability branding and consumer purchasing behavior. Brands increasingly use plantable packaging for outer cartons, sample sachets, tissue wraps, and promotional inserts to reinforce clean-beauty and natural product positioning.

This segment benefits from higher willingness to pay, lower functional barrier requirements compared with food packaging, and strong visual storytelling opportunities.

Premium skincare and cosmetic brands often incorporate seed-paper elements in limited-edition launches and influencer kits, enhancing engagement while supporting ESG commitments. Retailers and specialty beauty platforms also favor plantable packaging as part of broader green procurement policies, further accelerating adoption across this application segment.

Regional Insights

North America Plantable Packaging Market Trends - Brand-Led Pilots, Regulatory Guidance, and Premium Adoption

North America is a major growth market for plantable packaging, led by the U.S., where adoption is driven by corporate sustainability targets, foodservice pilots, and growing interest in compostable and regenerative packaging alternatives. Large consumer brands and retailers are increasingly testing seed-embedded paper inserts, plantable secondary cartons, and bioplastic-based formats for promotional and premium product lines.

Companies such as Target, Whole Foods Market, and Etsy-based DTC brands have incorporated plantable packaging elements into seasonal campaigns and private-label initiatives, helping normalize consumer interaction with post-use planting concepts.

Regulatory guidance from agencies such as the U.S. Food and Drug Administration (FDA) on food-contact materials, along with Federal Trade Commission (FTC) Green Guides governing environmental claims, is shaping product design, labeling accuracy, and material selection.

Investment activity is rising across biomaterial startups and converting partnerships, particularly in California and the Pacific Northwest, where sustainability-focused packaging incubators and university spin-offs are active. These combined factors support a sustained double-digit growth outlook, especially in premium food, gifting, and personal care segments.

Europe Plantable Packaging Market Trends - EPR-Backed Retail Adoption and Regulatory Maturity

Europe is expected to lead the market, accounting for approximately 34.5% of the market share, supported by advanced regulatory frameworks, established composting infrastructure, and high consumer awareness of circular economy principles.

Germany and the U.K. are at the forefront of adoption, driven by strong retailer commitments and extended producer responsibility (EPR) enforcement. Major European retailers such as Tesco, Aldi, and REWE Group have expanded trials of plantable paper packaging for private-label products, promotional inserts, and seasonal gifting formats.

France and Spain are showing increasing engagement as national bans on certain single-use plastics and stricter waste-sorting mandates encourage experimentation with regenerative materials. EU-wide policies under the European Green Deal and Packaging and Packaging Waste Regulation (PPWR) are accelerating regulatory harmonization, giving manufacturers clearer compliance pathways.

European packaging converters and material innovators are investing in scalable seed-paper production and bio-coatings, enabling commercialization across cartons, sleeves, and wraps. This regulatory clarity and retail pull continue to position Europe as the most mature and structurally supportive market for plantable packaging.

Asia Pacific Plantable Packaging Market Trends - Biomass-Driven Scaling and Cost-Efficient Manufacturing

Asia Pacific is likely to be the fastest-growing regional market for plantable packaging, driven by manufacturing scale, access to low-cost biomass, and government initiatives to reduce plastic waste.

China and India are key demand centers, supported by rising e-commerce volumes, sustainability commitments from domestic brands, and tightening restrictions on conventional plastic packaging. Indian startups and packaging converters are increasingly producing seed-embedded paper mailers and cartons for natural food, ayurvedic, and personal care brands, aligning sustainability with local agricultural narratives.

Southeast Asia is emerging as a strategic production hub, particularly for seaweed-based and fiber-based materials, with countries such as Indonesia and the Philippines leveraging abundant marine biomass. Companies such as Evoware in Indonesia have drawn global attention to seaweed-derived packaging solutions, influencing regional R&D investment and export opportunities.

Japan contributes through material science innovation and premium packaging design, while ASEAN manufacturing capacity supports global cost reduction. Collectively, the region plays a critical role in scaling supply, lowering unit costs, and expanding global adoption of plantable packaging solutions.

Competitive Landscape

The global plantable packaging market remains fragmented, characterized by numerous small innovators and a growing number of mid-sized converters. No single company holds a dominant share, though early consolidation is emerging as larger packaging firms pursue partnerships and acquisitions. Competitive advantage is increasingly defined by material performance, certification credibility, and the ability to scale production efficiently.

Recent strategic activity includes the expansion of seaweed-based product lines, regulatory-driven pilot programs in Europe, and partnerships between converters and bio-material startups in Asia Pacific. These developments reflect a shift from experimentation toward scalable commercialization and cost optimization.

Leading players emphasize material innovation, vertical integration, white-label services, and geographic expansion. Differentiation is achieved through validated germination performance, compliance with food-contact requirements, and integrated sustainability storytelling.

Key Industry Developments

- In June 2025, Graphic Packaging International introduced the PaperSeal® Pressed MAP Tray to reduce plastic usage in modified atmosphere packaging, reinforcing the trend toward fiber-based and plantable-aligned packaging technologies.

- In April 2025, Novolex completed its acquisition of Steward Packaging to broaden its plantable and seed-paper packaging capabilities, strengthening its portfolio of compostable packaging solutions.

Companies Covered in Plantable Packaging Market

- Botanical PaperWorks

- Notpla

- Evoware

- Seed Paper India

- Bloomin

- Pangea Organics

- Green Field Paper Company

- The Mend

- EcoEnclose

- Packhelp

- Searo

- Earthly Goods

- FlexSea

- Releaf Paper

- Seeded Paper

- Plantables

- Growing Paper

- Eco Marketing Solutions

- PaperWise

Frequently Asked Questions

The global plantable packaging market is estimated to be valued at US$154.8 million in 2026.

By 2033, the plantable packaging market is forecast to reach US$355.3 million.

Key trends include increased use of seed-embedded paper, growing adoption of bioplastic-based plantable formats, expansion of premium and promotional packaging use cases, and stronger alignment with corporate ESG and circular economy commitments.

The food and beverage application segment leads the market, accounting for the largest share due to high packaging volumes, sustainability commitments from brands, and strong consumer visibility.

The plantable packaging market is projected to grow at a CAGR of 12.6% between 2026 and 2033.

Major players include Pangea Organics, Seed Paper India, Botanical PaperWorks, Bloomin, and Evoware.