- Medical Devices

- Implantable Medical Devices Market

Implantable Medical Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Implantable Medical Devices Market by Product (Cardiovascular Implants, Orthopedic Implants, Ophthalmology Implants, Dental Implants, Aesthetic Implants, Neurology Implants), Biomaterial (Ceramic, Metallic, Polymers, Natural), by End-user (Hospitals & Clinics, Home Monitoring), by Regional Analysis, from 2026 to 2033.

Implantable Medical Devices Market Share and Trends Analysis

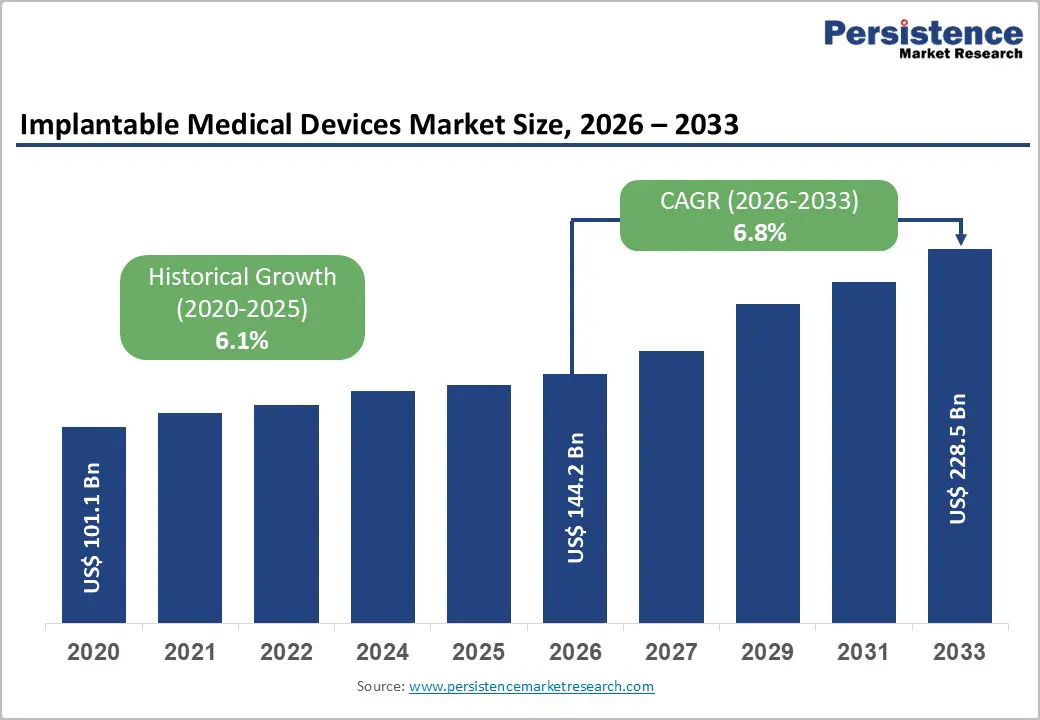

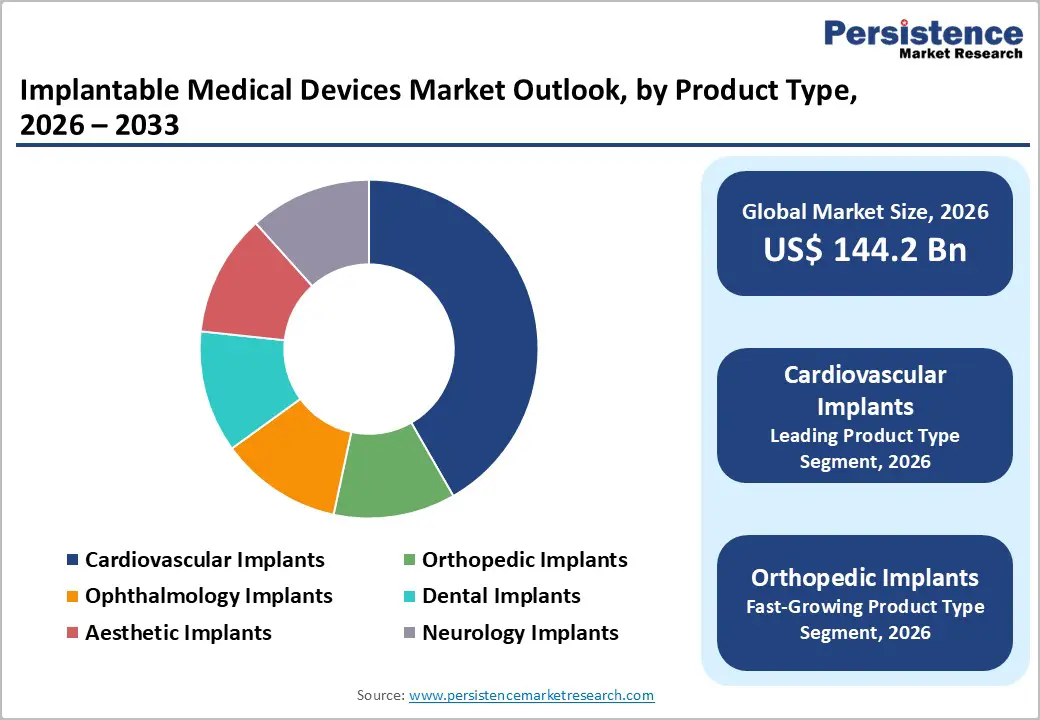

The global implantable medical devices market size is expected to be valued at US$ 144.2 billion in 2026 and projected to reach US$ 228.5 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033. The market is surging due to the increasing prevalence of chronic diseases, advancements in technology, and an aging population. Several notable trends are shaping the implantable medical devices market. There is a significant rise in the incidence of chronic diseases, including cardiovascular and orthopedic conditions, which is driving demand for various implantable devices. The aging population is particularly vulnerable to these health issues, further increasing the need for effective medical solutions.

Healthcare reforms aimed at improving infrastructure and accessibility are enhancing the market landscape. The trend toward less stringent regulations for new product development is also noteworthy, as it encourages manufacturers to introduce cutting-edge technologies more rapidly. Innovations such as biocompatible materials, 3D printing, and smart implantable devices are revolutionizing the industry. Moreover, the shift towards outpatient care and the increasing number of procedures performed in ambulatory surgical centers are contributing to implantable medical devices market growth.

Key Industry Highlights

- North America's robust healthcare infrastructure boosts the region’s revenue generation.

- Europe is predicted to become the second-largest market for implantable medical devices globally.

- Increased prevalence of chronic diseases contributes to the market’s growth over the forecast period.

- Favorable reimbursement policies for pacemaker implantation contribute to the market’s growth.

- The growing adoption of digital health technology creates a pool of opportunities for the market players.

- Orthopedic implants cater to the growing demand for implantable medical devices.

| Global Market Attributes | Key Insights |

|---|---|

| Implantable Medical Devices Market Size (2026E) | US$ 144.2 Bn |

| Market Value Forecast (2033F) | US$ 228.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Dynamics

Driver – Increasing Cardiovascular Disease Rates and Minimally Invasive Procedures

The rising prevalence of cardiovascular diseases (CVDs) is a major driver of the implantable medical devices market. Conditions such as coronary artery disease, arrhythmias, and heart failure continue to increase globally, placing significant pressure on healthcare systems. Cardiovascular diseases account for approximately 17.9 million deaths each year, making them the leading cause of mortality worldwide. This growing disease burden highlights the urgent need for effective long-term treatment options, including pacemakers, implantable cardioverter defibrillators, stents, and cardiac valves. Implantable devices play a critical role in disease management by improving survival rates, enhancing quality of life, and reducing hospital readmissions.

In parallel, the growing adoption of minimally invasive procedures is further accelerating market growth. These procedures offer advantages such as shorter recovery times, reduced surgical trauma, and lower complication rates compared to open surgeries. Implantable cardiovascular devices are increasingly used in minimally invasive interventions, resulting in less postoperative pain and improved patient satisfaction. Reduced infection risk and shorter hospital stays also make these procedures more appealing to both patients and healthcare providers. Together, the rising burden of cardiovascular diseases and the preference for minimally invasive treatments continue to drive strong demand for implantable medical devices worldwide.

Restraints – High Cost and Stringent Regulatory Policies

The high cost associated with implantable medical devices remains a significant restraint on market growth. Implantable devices often involve substantial expenses related to product manufacturing, surgical procedures, hospitalization, and post-operative care. These costs can limit accessibility, particularly in low- and middle-income countries where healthcare budgets and insurance coverage are limited. Even in developed regions, insufficient reimbursement policies can result in high out-of-pocket expenses for patients, discouraging adoption and restricting market penetration.

In addition to cost challenges, strict regulatory requirements present another major barrier. Regulatory authorities such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) enforce rigorous approval processes to ensure device safety and efficacy. These processes require extensive clinical trials, documentation, and long evaluation timelines, significantly increasing development costs for manufacturers. Compliance with quality standards, post-market surveillance, and regulatory audits further adds to operational complexity. Delays in regulatory approvals can slow product launches and limit the availability of innovative devices. Collectively, high financial barriers and stringent regulatory frameworks continue to constrain market expansion and innovation in the implantable medical devices industry.

Opportunity – Digital Health Integration and Minimally Invasive Innovation

The integration of digital health technologies represents a major opportunity in the implantable medical devices market. Manufacturers are increasingly incorporating features such as wireless connectivity, remote patient monitoring, and advanced data analytics into implantable devices. These capabilities allow healthcare providers to monitor patient health in real time, detect complications early, and adjust treatment plans more effectively. Digital integration improves patient engagement, enhances adherence to therapy, and supports proactive management of chronic conditions, ultimately leading to better clinical outcomes and reduced healthcare costs.

Another significant opportunity lies in the growing demand for minimally invasive procedures. Patients and healthcare providers are increasingly favoring treatments that reduce recovery time, minimize surgical risks, and shorten hospital stays. This shift creates strong demand for smaller, more efficient implants and advanced delivery systems designed for minimally invasive use. Innovations in biocompatible materials, miniaturization, and precision engineering enable manufacturers to develop next-generation implantable devices that align with these clinical needs. By focusing on minimally invasive solutions and digital innovation, companies can expand their product portfolios, strengthen market presence, and improve patient satisfaction in a rapidly evolving healthcare environment.

Category-wise Analysis

By Product Type Insights

The cardiovascular implants segment is projected to account for the largest revenue share of around 31% in 2026, supported by its essential role in the treatment and long-term management of cardiovascular disorders. This segment comprises pacemakers, implantable cardioverter defibrillators (ICDs), cardiac stents, valves, and cardiac monitoring devices. Cardiovascular diseases such as coronary artery disease, heart failure, and arrhythmias remain among the leading causes of morbidity and mortality worldwide.

According to multiple secondary sources, heart failure alone affects more than 84 million individuals globally, creating sustained demand for implantable cardiac solutions. Continuous technological advancements and regulatory approvals further strengthen this segment. For example, in July 2023, Abbott secured U.S. FDA approval for its AVEIR dual-chamber leadless pacemaker, the first system of its kind designed to treat abnormal or slow heart rhythms. Such innovations enhance clinical outcomes, expand treatment options, and reinforce the dominance of cardiovascular implants within the overall implantable medical devices market.

By Biomaterial Insights

Based on biomaterial type, the metallic segment held the largest revenue share of 47% in 2025, driven by the widespread use of metals such as titanium alloys, stainless steel, and cobalt-chromium alloys in implantable devices. These materials are valued for their superior mechanical strength, corrosion resistance, durability, and proven biocompatibility, making them suitable for long-term implantation. Metallic biomaterials can also be engineered into complex shapes and sizes, enabling the development of patient-specific implants that improve anatomical fit and functional performance. As a result, they are extensively used across orthopedic, cardiovascular, and dental applications.

Meanwhile, the natural biomaterial segment is anticipated to register the fastest CAGR of 6.6% during the forecast period. Growing patient preference for biologically derived and biocompatible materials, along with advances in tissue engineering and regenerative medicine, is supporting this growth. Improved integration with human tissue and favorable regulatory acceptance further encourage adoption of natural biomaterial-based implants.

Region-wise Insights

North America Implantable Medical Devices Market Trends

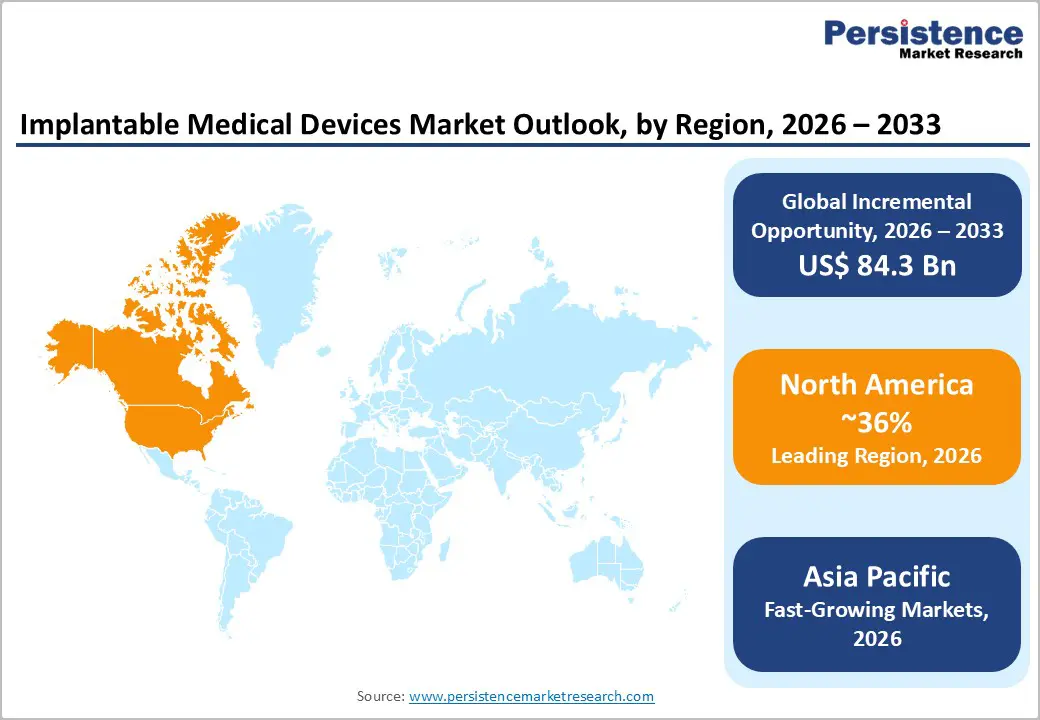

North America is projected to account for nearly 36% of the global implantable medical devices market in 2026, supported by its advanced healthcare ecosystem and high healthcare expenditure. The region benefits from early adoption of innovative medical technologies, strong reimbursement frameworks, and a well-established regulatory environment that supports the commercialization of high-value implantable devices. Hospitals and specialty clinics are equipped with advanced surgical infrastructure, enabling the widespread use of cardiovascular, orthopedic, and neurostimulation implants.

The United States remains the primary contributor within the region, driven by a high burden of chronic diseases such as cardiovascular disorders and arthritis. According to the CDC, heart disease continues to be the leading cause of death in the U.S., reinforcing demand for implantable cardiac devices. In addition, the presence of major medical device manufacturers, strong R&D investments, and continuous clinical trials accelerate product innovation. These factors collectively position North America as a mature yet innovation-driven market for implantable medical devices.

Europe Implantable Medical Devices Market Trends

Europe represents the second-largest regional market for implantable medical devices, supported by a rising incidence of chronic and age-related diseases. The region has a rapidly aging population, with Eurostat reporting that over 21% of the EU population was aged 65 years or older in 2023. This demographic trend significantly increases demand for implantable solutions addressing cardiovascular diseases, orthopedic degeneration, and neurological conditions.

European countries maintain strong public healthcare systems with consistent healthcare funding, enabling access to advanced implantable technologies. High clinical standards and a focus on patient safety support the adoption of well-established and clinically validated devices. In addition, regulatory oversight under the EU Medical Device Regulation (MDR) emphasizes quality and performance, encouraging manufacturers to deliver reliable and innovative implants. Growing procedural volumes in countries such as Germany, France, and the UK, combined with increasing awareness of minimally invasive treatments, continue to support steady market growth across the region.

Asia Pacific Implantable Medical Devices Market Trends

Asia Pacific implantable medical devices market is expected to witness robust growth, driven by a large patient pool, rising chronic disease prevalence, and improving healthcare access. Rapid urbanization and lifestyle changes have led to a sharp increase in cardiovascular diseases, diabetes, and orthopedic disorders across countries such as China and India. According to the Global Burden of Disease study, India reports a cardiovascular disease mortality rate of approximately 272 deaths per 100,000 population, exceeding the global average.

Healthcare infrastructure development and increased government spending are strengthening hospital capabilities across emerging economies. In addition, relatively favorable regulatory pathways and growing domestic manufacturing encourage faster product introductions. Rising medical tourism in countries such as India, Thailand, and Malaysia further supports procedural volumes for implantable devices. Increasing awareness, expanding insurance coverage, and improving affordability are collectively positioning Asia Pacific as a high-growth region within the global implantable medical devices market.

Competitive Landscape

The market is witnessing significant growth reflecting its dynamic landscape as indicated by the latest market report. Players in the industry are actively launching new products and integrating innovative technologies to create new opportunities within the sector.

Companies in the market are adopting crucial business strategies to broaden their product lines, increase market share across various regions, invest in research and development and optimize supply chains to enhance market value.

Key Industry Developments:

- June 2024, Researchers from the Beijing Institute of Technology and Rutgers University have developed innovative electrospinning techniques that could revolutionize the creation and implementation of nano/microrobots, wearable/implantable biosensors, and organ-on-chip systems. The research aims to overcome the limitations of traditional electrospinning methods, such as limited material compatibility and low production scalability

- July 2024, The World Health Organization (WHO) launched the Medical Devices Information System (MeDevIS) to standardize information about over 10,000 medical devices. MeDevIS includes 2,301 types of medical devices, ranging from single-use syringes to imaging radiology technologies. The platform aims to provide a "one-stop shop of international information" to help stakeholders find appropriate equipment.

Companies Covered in Implantable Medical Devices Market

- Medtronic

- Abbott Laboratories

- Johnson and Johnson

- Boston Scientific Corporation

- Smith & Nephew plc

- Stryker

- Cochlear Limited

- Integra LifeSciences

- LivaNova PLC

- Biotronik SE and Co. KG

- Others

Frequently Asked Questions

The global implantable medical devices market is projected to be valued at US$ 144.2 Bn in 2026.

Rising chronic diseases, aging population, technological advancements, and increasing demand for minimally invasive and long-term therapeutic solutions.

The global market is expected to witness a CAGR of 6.8% between 2026 and 2033.

Innovation in biocompatible materials, smart implants, and expansion into emerging healthcare markets with improved surgical infrastructure.

North America is the leading region in the global implantable medical devices market.