- Automotive Components & Materials

- Piston Ring Aftermarket Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Piston Ring Aftermarket Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Piston Ring Aftermarket by Product Type (Compression Ring, Oil Ring), Material Type (Grey Cast Iron, Chromium Steel, Material), Vehicle Type (Two Wheelers, Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle, Off Road Vehicles), and Regional Analysis 2026 - 2033

Piston Ring Aftermarket Share and Trends Analysis

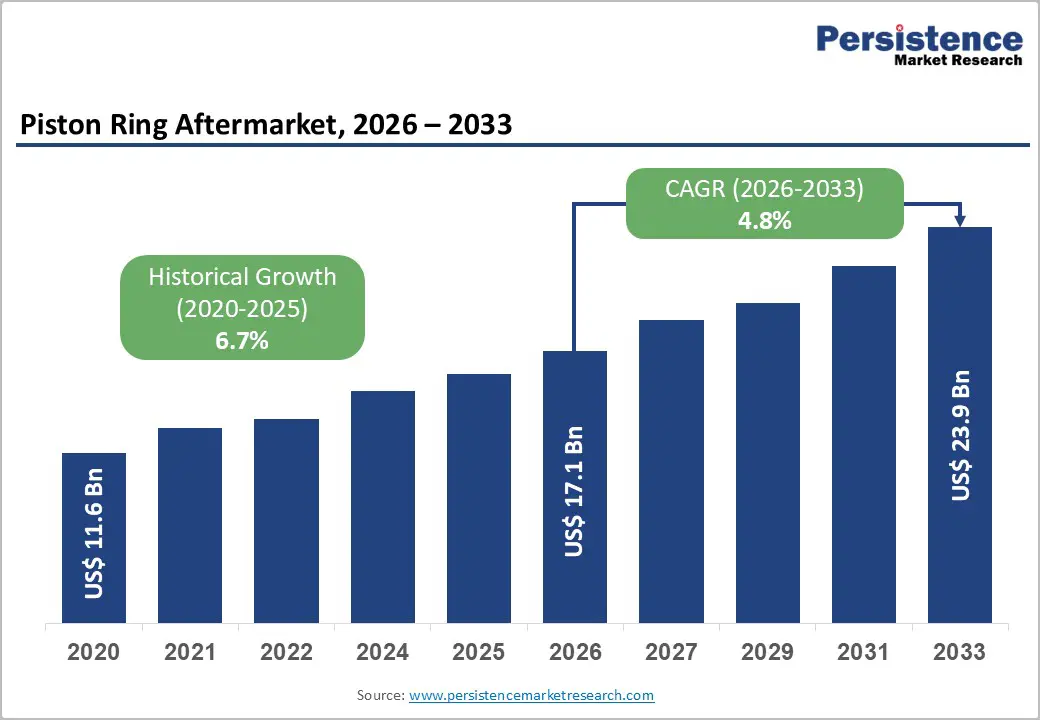

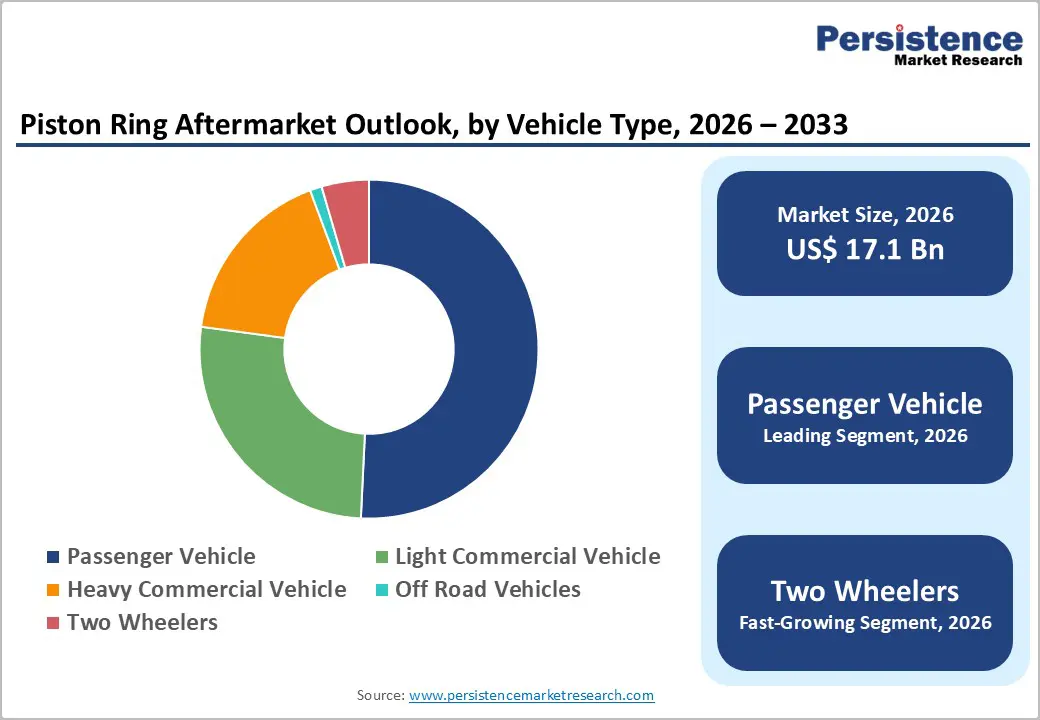

The global piston ring aftermarket size is projected to be valued at US$17.1 billion in 2026 and is anticipated to reach US$23.9 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033.

Market expansion is primarily driven by increasing vehicle fleet age across developed economies, rising global vehicle miles traveled, and stringent emission regulations that necessitate frequent engine maintenance. Growing demand for aftermarket replacement components, coupled with the expansion of automotive service infrastructure in emerging markets, continues to strengthen market fundamentals and revenue growth trajectories.

Key Industry Highlights:

- Compression rings dominate with ~67% market share by volume and revenue, while chromium steel emerges as the fastest-growing material at 7.1% CAGR, reflecting the performance demands of modern engines.

- Passenger vehicles maintain 51% market leadership; two-wheelers exhibit the highest growth at a 5.2% CAGR, driven by Asian market motorization and urbanization trends.

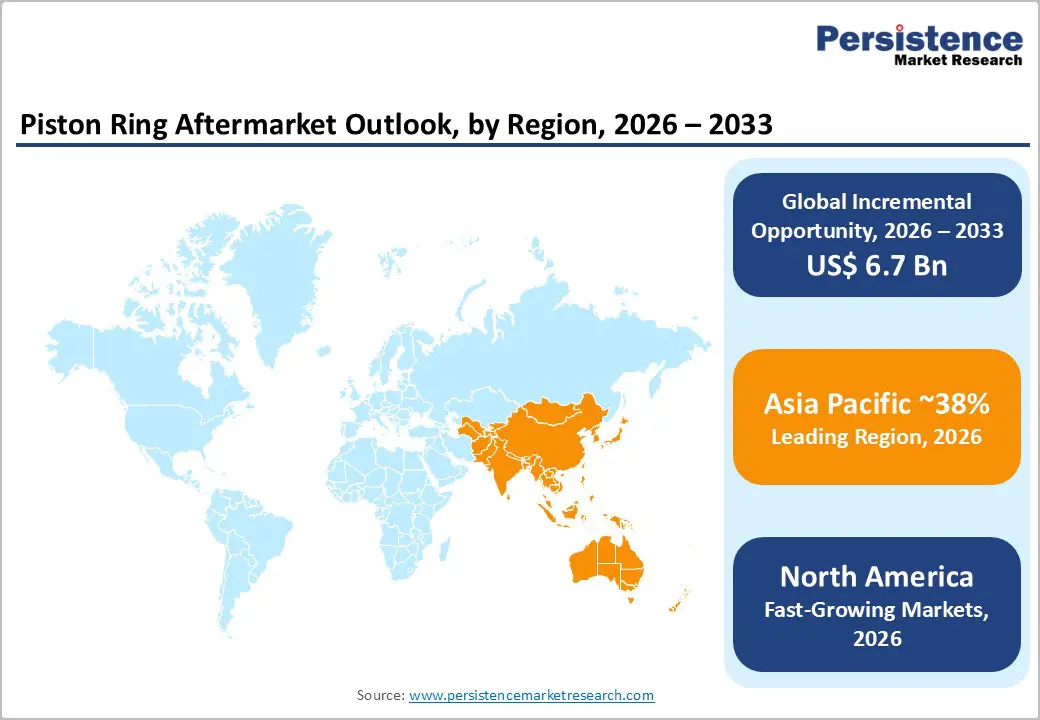

- Asia-Pacific holds a 38% global share as the largest regional market; North America exhibits the strongest growth at a 6.5% CAGR, driven by aging fleet demographics and high utilization intensity.

- Europe commands ~22% of the market, with premium segment strength; stringent emission regulations and comprehensive inspection mandates sustain consistent replacement demand across mature markets.

- Strategic consolidation continues with 6 major capacity expansions and technology partnerships since 2024, focusing on emerging market manufacturing, advanced coating technologies, and electrified powertrain applications.

| Key Insights | Details |

|---|---|

|

Piston Ring Aftermarket Size (2026E) |

US$ 17.1 Billion |

|

Market Value Forecast (2033F) |

US$ 23.9 Billion |

|

Projected Growth CAGR (2026-2033) |

4.8% |

|

Historical Market Growth (2020-2025) |

6.7% |

Market Dynamics Analysis

Drivers - Aging Vehicle Fleet and Extended Vehicle Lifecycle

The average age of vehicles in operation continues to rise globally, with U.S. light vehicles averaging 12.5 years according to S&P Global Mobility data, while European vehicle fleets exceed 11.8 years. This demographic shift drives substantial aftermarket demand as older engines require more frequent piston ring replacements due to wear and compression loss. The International Organization of Motor Vehicle Manufacturers reports over 1.4 billion vehicles (passenger & commercial vehicles) in global operation, with approximately 65% exceeding seven years of age. Extended ownership cycles, influenced by improved vehicle durability and economic considerations, create recurring replacement demand. This trend generates predictable revenue streams for aftermarket suppliers, with maintenance intervals typically occurring between 150,000-200,000 kilometers for passenger vehicles.

Increasing Vehicle Miles Traveled and Utilization Intensity

Global vehicle miles traveled reached around 3.2 trillion miles annually according to Federal Highway Administration statistics, representing consistent year-over-year growth of 1.8-2.3%. Commercial vehicle segments demonstrate higher utilization intensity, with heavy-duty trucks averaging 45,000-65,000 miles annually compared to passenger vehicle averages of 12,000-14,000 miles. The International Road Federation documents infrastructure expansion correlating with increased vehicle usage patterns across emerging economies. Ride-sharing services and commercial fleet operations intensify engine stress, accelerating wear patterns and reducing replacement intervals. Statistical analysis indicates every 10% increase in average annual mileage generates approximately 6-8% incremental demand for engine components, creating substantial market expansion opportunities across all vehicle segments.

Restraints - Advancement in Engine Technology and Extended Component Durability

Modern engine designs incorporating advanced materials, improved lubrication systems, and precision manufacturing techniques significantly extend piston ring service life, reducing replacement frequency. Original equipment manufacturers implement low-friction ring designs with diamond-like carbon coatings and nitriding treatments, achieving operational lifespans exceeding 300,000 kilometers. The Society of Automotive Engineers documents mean time between failures increasing by 35-42% over the past decade. Additionally, synthetic lubricants and enhanced filtration systems minimize abrasive wear, further extending component longevity and compressing aftermarket replacement cycles, thereby constraining market volume growth despite fleet expansion.

Electric Vehicle Proliferation and Powertrain Transition

The accelerating transition toward electric powertrains fundamentally threatens long-term aftermarket demand for internal combustion engine components. Global electric vehicle sales surpassed 14 million units in 2023 according to the International Energy Agency, representing 18% of total vehicle sales. Government mandates including the European Union's 2035 combustion engine ban and California's Advanced Clean Cars II regulation accelerate adoption curves. Battery electric vehicles eliminate piston ring requirements entirely, while hybrid configurations reduce replacement frequency through decreased engine utilization. Market projections indicate electric vehicles could comprise 45-50% of new vehicle sales by 2033, creating structural headwinds.

Opportunities - Premium Aftermarket Segment and Performance Enhancement Demand

Growing enthusiast communities and performance modification trends create premium pricing opportunities for advanced piston ring technologies. High-performance ring sets incorporating plasma-moly coatings, gas-nitrided steel, and reduced-tension designs command 3-4x price premiums over standard replacements. The Specialty Equipment Market Association estimates the performance parts segment at US$49.8 billion annually, with engine components representing 18-22% of category spending. Racing applications, classic car restoration, and modified vehicle segments demonstrate price insensitivity and prioritize quality over cost. Digital marketplace expansion enables specialized suppliers to reach niche customer segments globally, with e-commerce penetration in the automotive aftermarket projected at 22-25% by 2028, representing a US$4.1-4.9 billion addressable opportunity.

Remanufacturing and Circular Economy Integration

Environmental sustainability mandates and total cost of ownership optimization drive adoption of remanufactured engine components, creating new business model opportunities. The Global Automotive Parts Remanufacturing Market generates approximately $69 billion in revenue, with engine-related parts accounting for 34.6% of the market share. Complete engine remanufacturing requires new piston ring sets regardless of core condition, creating guaranteed demand volumes. Extended producer responsibility regulations in European markets and China's circular economy promotion law incentivize remanufacturing infrastructure development. Fleet operators achieve 40-60% cost savings versus new engine replacements while maintaining performance specifications. Market analysis indicates remanufacturing channels could account for 15-18% of total piston ring demand by 2033.

Category-wise Analysis

Product Type Insights

Compression Ring maintains commanding market leadership with approximately 67% share by volume and revenue, driven by its critical role in cylinder sealing and combustion efficiency. Piston assemblies require multiple compression rings per cylinder, with typical configurations employing two compression rings versus one oil control ring, creating inherently higher unit volumes. The compression ring segment generates sustained demand as these components are sold as complete sets for specific piston specifications, ensuring compatibility and optimal performance. Replacement practices mandate simultaneous installation of all rings regardless of individual component condition, reinforcing the segment's dominant position. Market value reached approximately US$16.3 billion in 2026 across passenger, commercial, and off-road applications.

Oil Ring represents the fastest-growing segment at 4.8% CAGR, despite matching compression ring growth rates, due to its primary role in generating replacement demand cycles. While sharing identical CAGR, oil rings drive the replacement decision-making process as oil consumption issues prompt engine service interventions. Once engines are opened for oil ring replacement due to excessive consumption or blow-by symptoms, compression rings are simultaneously replaced as standard maintenance practice. This segment benefits from increasing oil quality awareness and emission testing protocols that identify oil control deficiencies earlier in the component lifecycle.

Material Type Insights

Grey Cast Iron dominates the material segment with approximately 64% market share, attributed to its optimal combination of cost-effectiveness, thermal stability, and sufficient wear resistance for standard applications. This ferrous material provides adequate service life for most passenger vehicles and light commercial applications while maintaining competitive pricing for aftermarket replacement markets. Grey cast iron's established manufacturing infrastructure, material availability, and proven performance across diverse operating conditions sustain its market leadership. The segment benefits from price-sensitive replacement decisions in developing markets and fleet maintenance operations prioritizing total cost management. Material properties, including vibration damping and machinability, support efficient production scaling and consistent quality delivery across global supply chains.

Chromium steel is the fastest-growing piston ring material with a 7.1% CAGR, driven by superior wear resistance, longer service life, and performance required by modern high-efficiency engines. Advanced designs with higher specific output, elevated temperatures, and longer oil change intervals demand materials beyond cast iron. Chromium steel rings use plasma spraying and physical vapor deposition, achieving two to three times the durability. Adoption accelerates in turbocharged and diesel vehicles as pricing declines through manufacturing efficiencies and scale.

Vehicle Type Insights

The passenger vehicle segment maintains market leadership with approximately 51% share, reflecting the sheer volume of the global passenger car fleet comprising over 1.1 billion units in operation worldwide. This segment benefits from predictable replacement cycles averaging 8-12 years depending on usage patterns and maintenance practices. Passenger vehicle engines typically operate within moderate stress parameters, generating consistent aftermarket demand without extreme performance requirements. The segment encompasses diverse powertrain configurations from small-displacement naturally aspirated engines to turbocharged performance variants, creating broad product requirements. Market dynamics reflect aging fleet demographics, particularly in developed economies, where vehicles exceeding ten years of age represent primary replacement demand drivers. Regional variations in maintenance culture significantly influence replacement frequencies and brand preferences.

Two-wheelers represents the fastest-growing vehicle segment at 5.2% CAGR, propelled by explosive motorcycle and scooter adoption across Asian markets, particularly India, Indonesia, Vietnam, and Thailand. This segment benefits from lower absolute vehicle costs, driving higher replacement component affordability and more frequent service interventions. Two-wheeler engines experience higher-stress operating conditions, including elevated engine speeds, aggressive throttle application, and varied maintenance quality, reducing component service life compared to passenger vehicles. Urbanization trends and last-mile connectivity solutions accelerate two-wheeler utilization, particularly in congested metropolitan areas where motorcycles offer mobility advantages.

Regional Market Insights

North America Piston Ring Aftermarket Trends

North America demonstrates robust market performance with 6.5% CAGR, driven by the region's aging vehicle fleet averaging 12.5 years and high annual mileage accumulation patterns. The United States dominates regional demand, accounting for approximately 85% of North American aftermarket volumes, supported by 280 million registered passenger & commercial vehicles and extensive highway infrastructure generating 3.2 trillion vehicle miles annually. Canada contributes steady growth through harsh operating conditions accelerating component wear, while Mexico benefits from expanding automotive manufacturing presence and rising vehicle ownership rates. Stringent emission inspection programs across major metropolitan areas mandate proper engine maintenance, creating regulatory-driven replacement demand. The region's established distribution networks, strong independent repair shop presence, and DIY culture support healthy aftermarket channels.

Key growth drivers include pickup truck and SUV segment dominance requiring larger-displacement engines with multiple cylinder configurations, regulatory compliance requirements through state-level emission testing programs, and professional fleet management practices emphasizing preventive maintenance. Investment trends favor distribution infrastructure modernization and e-commerce platform development, enhancing parts availability and customer convenience.

Europe Piston Ring Aftermarket Trends

Europe commands a considerable market share of approximately 22% of the global aftermarket, characterized by sophisticated regulatory frameworks and mature automotive markets. Germany, the United Kingdom, France, Italy, and Spain collectively represent ~62% of regional demand, driven by extensive vehicle fleets averaging 11.8 years and comprehensive emission testing mandates. The region demonstrates the highest replacement component quality standards, with substantial premium segment penetration and brand loyalty toward established suppliers. European Union regulatory harmonization, including Euro 6d standards and periodic technical inspection requirements create consistent replacement cycles across member states. Market dynamics reflect diesel powertrain prevalence, requiring specialized ring specifications and premium materials. Regional consolidation among independent aftermarket distributors strengthens supply chain efficiency while creating barriers to new market entrants.

Germany leads absolute volumes through its extensive vehicle fleet and strong commercial vehicle presence, while the UK markets demonstrate robust online channel adoption. Regulatory environment impact remains substantial with emission zone implementations and enhanced inspection protocols driving maintenance compliance. Investment focuses on sustainable remanufacturing infrastructure and circular economy integration.

Asia Pacific Piston Ring Aftermarket Trends

Asia Pacific holds a significant market share of approximately 38%, representing the largest regional market, though growth rates in the aftermarket remain moderate compared to Europe and North America due to relatively lower replacement frequencies. China, Japan, India, and ASEAN nations comprise this diverse market, with China accounting for approximately 45% of regional volumes despite newer fleet demographics. Japan demonstrates the highest per-vehicle replacement rates through a rigorous maintenance culture and a stringent Shaken inspection system requiring comprehensive engine condition assessment. India exhibits accelerating growth driven by an expanding vehicle fleet, surpassing 320 million registered units and increasing motorization rates in tier-2 and tier-3 cities. ASEAN markets including Indonesia, Thailand, Vietnam, and Philippines, demonstrate robust growth particularly in two-wheeler and light commercial vehicle segments.

Manufacturing advantages including proximity to raw material sources, established production capabilities, and competitive labor costs position the region as global production hub. Regional growth dynamics reflect urbanization, infrastructure development, and rising middle-class populations driving vehicle ownership expansion.

Competitive Landscape

Market leaders in the piston ring aftermarket prioritize innovation using advanced materials and coatings to reduce friction and extend service life. Expansion into emerging markets through local manufacturing builds cost advantages. Multi-channel strategies, vertical integration, OEM partnerships, and diversified portfolios strengthen competitiveness while capturing cross-segment growth opportunities globally.

Strategic Developments

- In October 2023, Nippon Piston Ring Co., Ltd. and Riken Corporation merged to establish NPR-RIKEN CORPORATION, combining their piston ring technologies and capacities to enhance product offerings and innovation in critical internal combustion engine components.

- In November 2024, MAHLE GmbH secured a contract with MAN Truck & Bus to supply piston rings for a hydrogen-powered truck engine. This development highlights growing demand for advanced piston ring technologies in hydrogen and renewable-fuel engines, reinforcing new growth opportunities for the piston ring market beyond conventional internal combustion applications.

Companies Covered in Piston Ring Aftermarket Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

- Mahle GmbH

- Tenneco Inc. (Federal-Mogul Motorparts)

- Nippon Piston Ring Co., Ltd.

- Riken Corporation

- TPR Co., Ltd.

- ASIMCO Technologies

- Shriram Pistons & Rings Ltd.

- Art Piston Rings

- Hastings Manufacturing Company

- ZYNP Corporation

- Indian Piston Limited

- Perfect Circle (Dana Incorporated)

Frequently Asked Questions

The global piston ring aftermarket is projected at US$17.12 billion in 2026, expanding to US$23.85 billion by 2033, representing substantial growth driven by 1.4 billion vehicles in operation globally and increasing maintenance requirements across aging fleet demographics.

Primary drivers include aging global vehicle fleet averaging 11-12.5 years, increasing annual vehicle miles traveled exceeding 3.2 trillion miles globally, and expanding motorization across emerging economies, generating replacement component demand.

The market is projected to grow at a 4.8% CAGR between 2026 and 2033.

Emerging market motorization is driving strong growth, premium performance commands significantly higher value, and remanufacturing is unlocking new revenue through the circular economy and fleet cost optimization.

Market leaders include Mahle GmbH, Tenneco Inc., Nippon Piston Ring Co., Riken Corporation, with some other players TPR Co., ASIMCO Technologies, Shriram Pistons & Rings, with strong regional presence from Art Piston Rings, Hastings Manufacturing, and emerging manufacturers across Asian markets.