- Specialty & Fine Chemicals

- Phenolic Antioxidants Market

Phenolic Antioxidants Market Size, Share, and Growth Forecast 2025 - 2032

Phenolic Antioxidants Market By Product Type (Mono-phenols, Bi-phenols, Multi-Functional), Application (Fuels & Lubricants, Plastic and Rubber, Food and Feed Additives, Others), Form (Liquid, Granule, Powder), Source (Natural, Synthetic), and Regional Analysis for 2025 - 2032

Phenolic Antioxidants Market Size and Trends Analysis

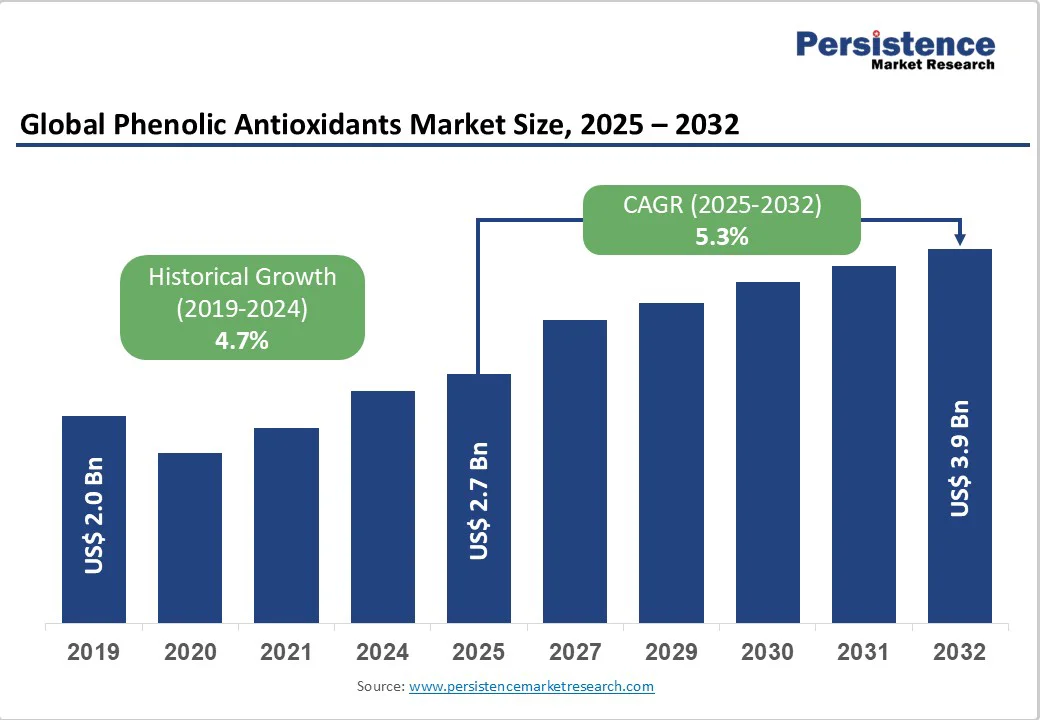

The global phenolic antioxidants market size was valued at US$2.7 Billion in 2025 and is projected to reach US$3.9 Billion by 2032, growing at a CAGR of 5.3% during the forecast period from 2025 to 2032, driven by increasing demand from plastic and rubber industries requiring enhanced thermal stability, growing automotive sector adoption of high-performance lubricants and fuel additives, and rising consumer preference for natural antioxidants in food and personal care applications.

Advances in phenolic formulations, stricter environmental regulations favoring sustainable additives, and rising use in renewable energy and biodegradable packaging applications will also drive market growth.

Key Industry Highlights

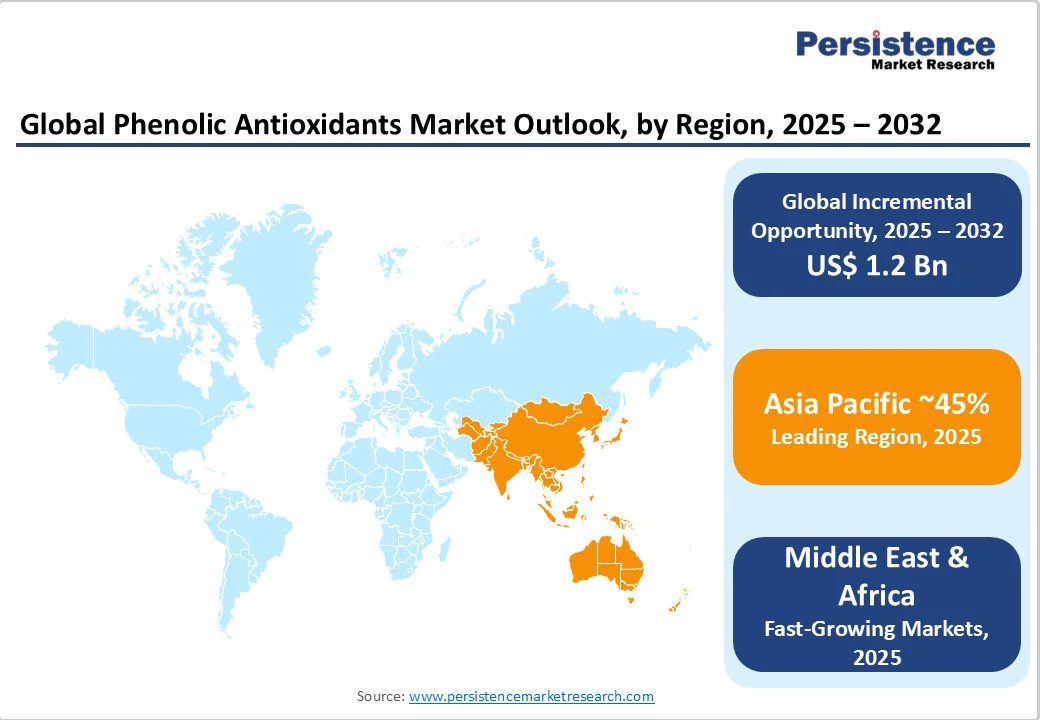

- Leading Region: Asia Pacific leads global phenolic antioxidants consumption with 45% market share, driven by rapid industrialization, massive manufacturing capacity, and growing demand across China, India, and ASEAN countries.

- Growing Region: The Middle East & Africa emerges as the fastest-growing regional market supported by infrastructure development, industrial diversification programs, and expanding chemical manufacturing capabilities, creating new demand opportunities.

- Dominant Segment: Mono-phenols dominate product type segments with 45% market share due to cost-effectiveness, versatility, and excellent performance characteristics across diverse industrial and consumer applications.

- Fastest Growing Segment: Natural antioxidants represent the fastest-growing source segment, expected to dominate by 2032, driven by consumer preference for clean-label products and regulatory support for sustainable alternatives.

- Key Opportunity: Renewable energy applications offer a major growth opportunity supported by the global clean energy transition, advanced material requirements, and long-term durability specifications for solar and wind technologies.

| Key Insights | Details |

|---|---|

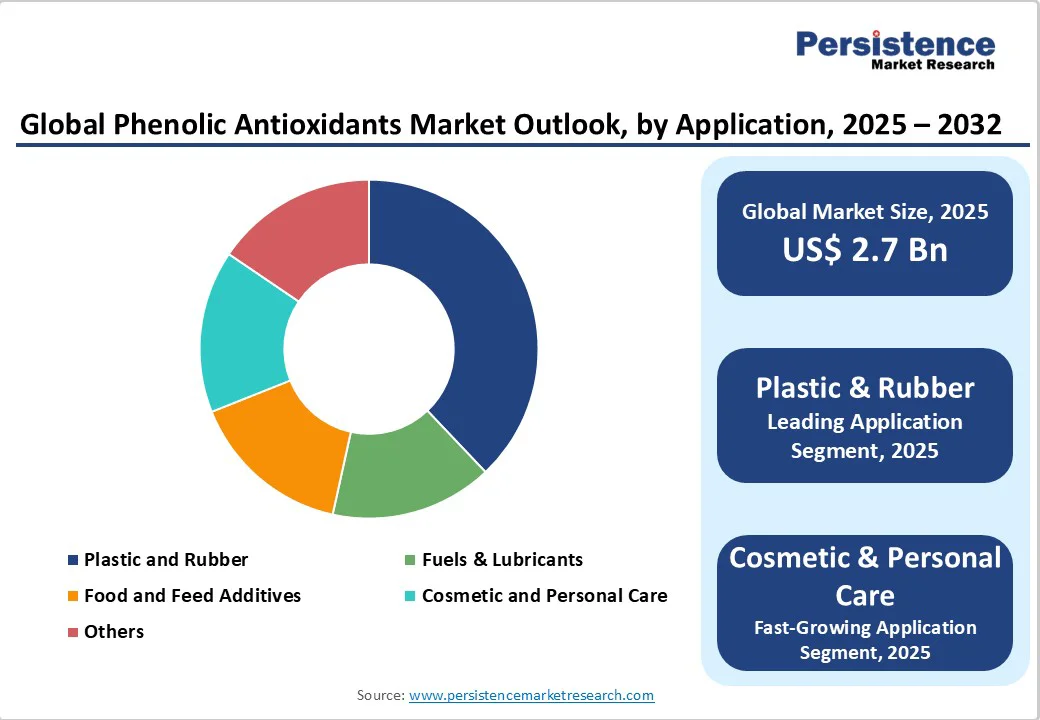

| Phenolic Antioxidants Market Size (2025E) | US$2.7 Bn |

| Market Value Forecast (2032F) | US$3.9 BN |

| Projected Growth CAGR(2025-2032) | 5.3% |

| Historical Market Growth (2019-2024) | 4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Demand from Plastic and Rubber Industries for Enhanced Thermal Stability

The rapid expansion of the global plastic and rubber industries is driving strong demand for phenolic antioxidants, essential for enhancing thermal stability and oxidation resistance. Global plastic production surpassed 399 million tons in 2024, fueling the need for additives that prevent degradation and extend product lifecycles.

Phenolic antioxidants such as BHT and Irganox 1010 offer superior protection at temperatures above 200°C, supporting high-performance applications in automotive, construction, and packaging. With vehicles now containing over 300 kg of plastic on average, the automotive sector’s shift toward lightweight materials further accelerates demand for advanced antioxidant solutions, ensuring durability and safety.

Growing Consumer Preference for Natural Antioxidants in Food and Personal Care Applications

Rising health consciousness and regulatory restrictions on synthetic additives are fueling demand for natural phenolic antioxidants derived from sources such as rosemary extract, green tea polyphenols, and tocopherols. Consumer preference for clean-label products has surged 71% since 2020, driving manufacturers to replace BHA and BHT with natural alternatives.

Stricter EU regulations further boost this shift, creating strong market opportunities. Though priced 3-5 times higher, natural antioxidants offer superior sustainability and compliance advantages. The personal care sector increasingly adopts these compounds in anti-aging, sun care, and hair formulations, with global cosmetic antioxidant consumption reaching 28,000 tons in 2024.

Barrier Analysis - High Production Costs and Raw Material Price Volatility

Phenolic antioxidant manufacturing faces strong cost pressures from volatile raw material prices, with phenol, cresol, and butylated compounds rising 16% between 2022 and 2024. Complex synthesis processes requiring specialized equipment and strict quality control further elevate costs.

Natural phenolic antioxidants face greater challenges due to agricultural supply chain dependencies, complex extraction methods, and certification requirements, resulting in production costs 3-5 times higher than synthetic alternatives, limiting their widespread commercial adoption.

Stringent Regulatory Requirements and Environmental Compliance

The phenolic antioxidants industry faces increasing regulatory scrutiny from agencies, including the EPA, ECHA, and Asian regulatory bodies, that impose strict guidelines on production, handling, and application due to potential environmental and health impacts.

Compliance with evolving regulations requires substantial investments in monitoring systems, documentation protocols, and quality assurance measures that increase operational complexity and associated costs. The growing shift toward PFAS-free formulations and sustainable chemistry principles creates additional challenges for manufacturers who must reformulate existing products while maintaining performance characteristics and competitive pricing structures.

Opportunity Analysis - Expanding Applications in Renewable Energy Components and Sustainable Materials

The rapidly growing renewable energy sector presents significant opportunities for phenolic antioxidant applications in solar panel components, wind turbine materials, and energy storage systems that require long-term durability under extreme environmental conditions.

Solar panel manufacturers utilize phenolic antioxidants in EVA (Ethylene Vinyl Acetate) encapsulants and backsheet materials to prevent UV-induced degradation and maintain 25-year performance warranties, with global solar installations projected to reach 200 GW annually by 2025.

Wind turbine components, including composite blades, lubricants, and electrical systems, require specialized phenolic antioxidants that provide protection against ozone exposure, thermal cycling, and mechanical stress over 20-25 year operational lifespans. The energy storage industry increasingly adopts phenolic antioxidants in battery separators, electrolyte additives, and thermal management systems to enhance the safety and longevity of lithium-ion and flow battery technologies.

Advanced Automotive Applications and High-Performance Lubricant Systems

The automotive industry’s evolution toward electric vehicles, hybrid powertrains, and advanced engine technologies creates substantial opportunities for specialized phenolic antioxidant formulations that meet demanding performance requirements.

Electric vehicle battery systems require phenolic antioxidants in thermal interface materials, cooling fluids, and high-voltage cable insulation to ensure safety and longevity under extreme operating conditions, with global EV production projected to exceed 30 million units by 2025.

Advanced engine lubricants utilizing synthetic base oils and extended drain intervals require phenolic antioxidant packages that provide oxidation stability at temperatures exceeding 150°C while maintaining viscosity control and deposit prevention over 15,000-25,000-mile service intervals.

The growing adoption of turbocharged engines, direct injection systems, and alternative fuel vehicles demands specialized antioxidant formulations that address unique oxidation challenges and performance requirements.

Category-wise Analysis

Product Type Insights

Mono-phenols dominate the market with approximately 45% market share in 2025, primarily due to their cost-effectiveness, versatility, and excellent performance characteristics across diverse industrial applications.

Mono-phenolic compounds such as BHT (Butylated Hydroxytoluene), BHA (Butylated Hydroxyanisole), and TBHQ (Tertiary Butylhydroquinone) demonstrate superior compatibility with processing conditions and end-use requirements while maintaining competitive pricing advantages over more complex formulations.

The segment’s dominance is reinforced by its essential role in commodity plastic applications, where cost-effectiveness is paramount, with mono-phenols typically providing 80-90% of the antioxidant protection required for standard polyethylene and polypropylene applications.

Manufacturing advantages include streamlined synthesis routes, high-yield production processes, and established supply chain infrastructure that enable consistent product availability and quality control across global markets.

Application Insights

Plastic and Rubber applications represent the dominant market segment with 64% market share in 2025, reflecting the essential role of phenolic antioxidants in preventing thermo-oxidative degradation and extending the service life of polymer materials across automotive, construction, and packaging industries.

The segment benefits from growing global plastic production, which exceeded 399 million tons in 2024, with phenolic antioxidants representing 0.1-0.5% by weight of total polymer formulations but providing disproportionate value through performance enhancement and lifecycle extension.

Rubber applications particularly benefit from phenolic antioxidants’ ability to prevent ozone cracking, thermal aging, and flex fatigue that can compromise performance in automotive tires, industrial seals, and consumer products requiring long-term durability. The segment’s growth is further supported by increasing adoption of high-performance plastics in aerospace, electronics, and medical applications, where oxidative stability is critical for safety and reliability.

Form Insights

Liquid form phenolic antioxidants maintain market leadership due to their superior handling characteristics, processing advantages, and uniform distribution capabilities in polymer and industrial applications. Liquid antioxidants offer easy incorporation into manufacturing processes, reduced dust exposure for worker safety, and improved dispersion in polymer melts compared to solid alternatives.

The segment benefits from applications requiring precise dosing, automated feeding systems, and consistent performance, where liquid formulations provide superior control and repeatability. Liquid phenolic antioxidants such as Irganox 1135 and AO-80 demonstrate excellent compatibility with polymer processing equipment and enable in-line addition during extrusion and molding operations without requiring pre-mixing or masterbatch preparation.

Source Insights

Synthetic phenolic antioxidants currently hold approximately 55% market share in 2025, but natural alternatives are experiencing rapid growth and are expected to dominate by 2032 as consumer preferences shift toward clean-label and sustainable solutions. The natural segment benefits from regulatory support, premium pricing, and consumer willingness to pay 15-25% premiums for products containing plant-derived antioxidants.

Natural phenolic compounds from rosemary extract, green tea, and grape seed offer equivalent or superior antioxidant performance while providing marketing advantages and regulatory compliance benefits in food and personal care applications.

The transition toward natural sources is supported by technological advances in extraction processes, standardization methods, and stability enhancement that address historical limitations of natural antioxidants, including color development, odor issues, and processing compatibility.

Regional Insights

North America Phenolic Antioxidants Market Trends

North America demonstrates steady market growth supported by advanced manufacturing infrastructure, stringent regulatory frameworks promoting product safety, and strong innovation ecosystems driving technological advancement in antioxidant applications.

The U.S. leads regional consumption through diverse industrial applications, including automotive, aerospace, food processing, and personal care, with market leadership reinforced by the presence of major manufacturers such as Eastman Chemical Company, Lubrizol Corporation, and Dover Chemical Corporation.

The region benefits from established R&D capabilities and university partnerships that foster innovation in sustainable antioxidant technologies and advanced application development.

The U.S. FDA’s GRAS (Generally Recognized as Safe) approval processes and EPA environmental regulations create comprehensive frameworks that ensure product safety while facilitating market access for compliant formulations.

Advanced manufacturing technologies, including continuous processing, automated quality control, and digital monitoring systems, enable North American producers to maintain competitive advantages through improved efficiency, consistency, and custom product development capabilities.

The region’s emphasis on sustainability and clean-label products creates opportunities for natural phenolic antioxidants that meet consumer demands while providing technical performance equivalent to synthetic alternatives.

Europe Phenolic Antioxidants Market Trends

European phenolic antioxidants markets exhibit steady growth as a mature market with well-established applications across automotive, chemical, and food industries, supported by comprehensive EU regulatory harmonization and strong emphasis on environmental sustainability.

The European Chemicals Agency (ECHA) provides standardized REACH registration requirements that ensure consistent safety standards while facilitating cross-border trade and market access. Germany, France, and the U.K. lead regional consumption through advanced chemical industries, automotive manufacturing, and food processing sectors that demand high-quality antioxidant solutions.

The region’s focus on circular economy principles and sustainable chemistry encourages the development of bio-based and renewable phenolic antioxidants that align with the EU Green Deal environmental objectives. European manufacturers are investing in green chemistry initiatives and carbon footprint reduction programs that support market positioning for environmentally responsible products.

Progressive regulatory frameworks, including EU food additive regulations and cosmetic ingredient directives, create opportunities for natural phenolic antioxidants while maintaining strict safety and performance standards that benefit established market participants.

Asia Pacific Phenolic Antioxidants Market Trends

Asia Pacific dominates the market with a 45% market share in 2025, driven by rapid industrialization, massive manufacturing capacity, and growing consumption across China, India, Japan, and ASEAN countries.

China represents the largest regional market, contributing over 30% of global consumption through extensive plastic production, automotive manufacturing, and chemical processing industries that require substantial antioxidant inputs. The country’s Belt and Road Initiative continues driving infrastructure investments that create sustained demand for construction materials and industrial chemicals.

India’s rapidly expanding economy and manufacturing sector growth, supported by Make in India initiatives, drive substantial demand for phenolic antioxidants across automotive, textiles, and food processing applications.

The region’s manufacturing cost advantages, including competitive raw material access, skilled technical workforce, and established supply chain networks, support both domestic consumption and export capabilities to global markets. Japan maintains technological leadership in high-performance antioxidant development and specialty applications that command premium pricing and drive innovation across the regional market.

Competitive Landscape

The global phenolic antioxidants market is moderately consolidated, dominated by multinational players such as BASF SE, Clariant International AG, and Eastman Chemical Company, leveraging advanced manufacturing capabilities and global distribution networks. Market concentration stems from high capital investment needs, complex synthesis expertise, and stringent regulatory requirements that limit new entrants.

Growth strategies center on capacity expansion, regional penetration, strategic acquisitions, and sustainable formulation development. Innovation emphasizes natural antioxidants, eco-friendly chemistries, and specialized solutions for high-performance sectors, including renewable energy, advanced materials, and premium consumer products.

Key Market Developments

- March 2025: BASF SE announced a US$50 Million investments to increase production capacity for aminic antioxidants at its Puebla, Mexico facility, addressing growing global demand for long-life lubricants and high-performance automotive applications, with completion scheduled for 2026.

- April 2025: BASF SE launched three natural-based innovations for personal care applications at in-cosmetics Global 2025, including Verdessence Maize styling polymer and biodegradable alternatives that enable sustainable formulations without performance compromise.

Companies Covered in Phenolic Antioxidants Market

- BASF SE

- Adeka Corporation

- Clariant International AG

- Dorf Ketal

- Dover Chemical Corporation

- Eastman Chemical Company

- Lanxess AG

- Lubrizol Corporation

- Mayzo Inc

- OXIRIS

- SI Group

- Songwon Industrial

- Afton Chemical

- Krishna Antioxidants Pvt. Ltd.

- Addivant

Frequently Asked Questions

The phenolic antioxidants market was valued at US$2.7 Billion in 2025 and is projected to reach US$3.9 Billion by 2032, representing a compound annual growth rate of 5.3% during the forecast period.

Key growth drivers include increasing demand from plastic and rubber industries for enhanced thermal stability, growing consumer preference for natural antioxidants in food and personal care applications, and expanding applications in renewable energy components and sustainable materials.

Mono-phenols dominate the market with approximately 45% market share in 2025, driven by their cost-effectiveness, versatility, and excellent performance characteristics across diverse industrial and consumer applications.

Asia Pacific leads the phenolic antioxidants market with 45% market share in 2025, primarily driven by rapid industrialization, massive manufacturing capacity, and growing demand across China, India, Japan, and ASEAN countries.

Renewable energy applications represent a significant growth opportunity, supported by global clean energy transition, advanced material requirements for solar and wind technologies, and long-term durability specifications requiring specialized antioxidant protection.

Major market players include BASF SE, Clariant International AG, Eastman Chemical Company, Lubrizol Corporation, Lanxess AG, SI Group, Songwon Industrial, Adeka Corporation, Dover Chemical Corporation, and Addivant.