- Pharmaceuticals

- Cosmeceuticals Market

Cosmeceuticals Market Size, Share, and Growth Forecast, 2026 - 2033

Cosmeceuticals Market by Product Type (Skin Care Products, Hair Care Products, Oral Care Products, Lip Care, Others), Ingredient Type (Retinoids, Peptides & Proteins, Natural Extracts, Sunscreens, Antioxidants, Hydroxy Acids, Exfoliants, Others), Distribution Channel (Supermarkets & Hypermarkets, Pharmacies, Drug Stores, Specialty Stores, Beauty Retailers, Online Retail Platforms, Salons, Clinics, Others), and Regional Analysis for 2026 - 2033

Cosmeceuticals Market Share and Trends Analysis

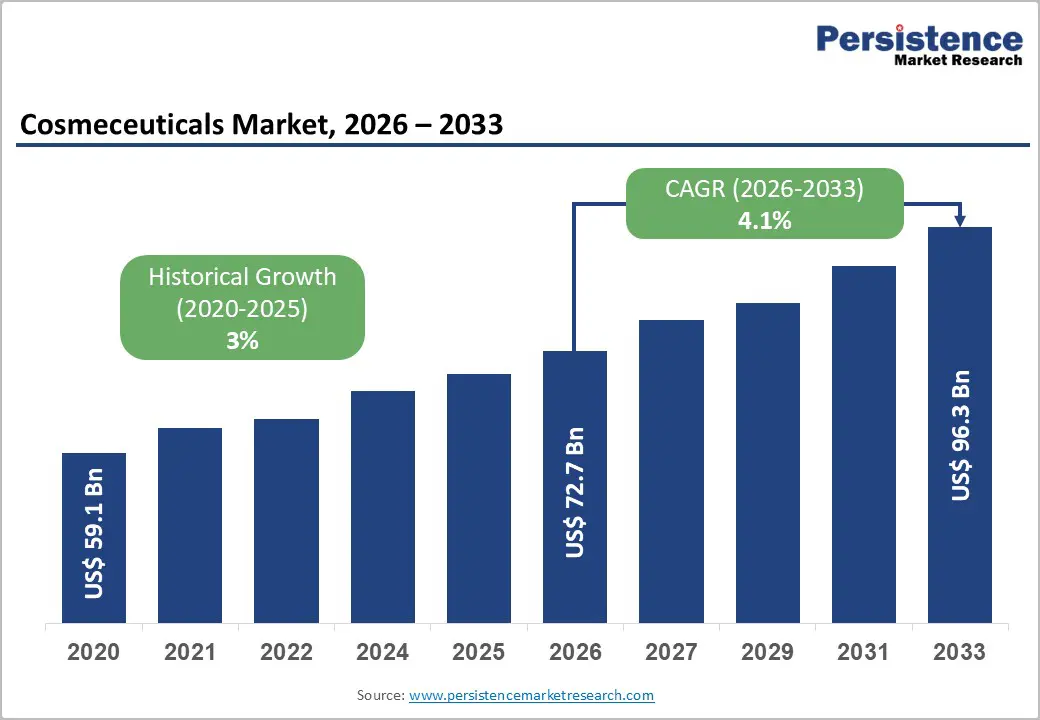

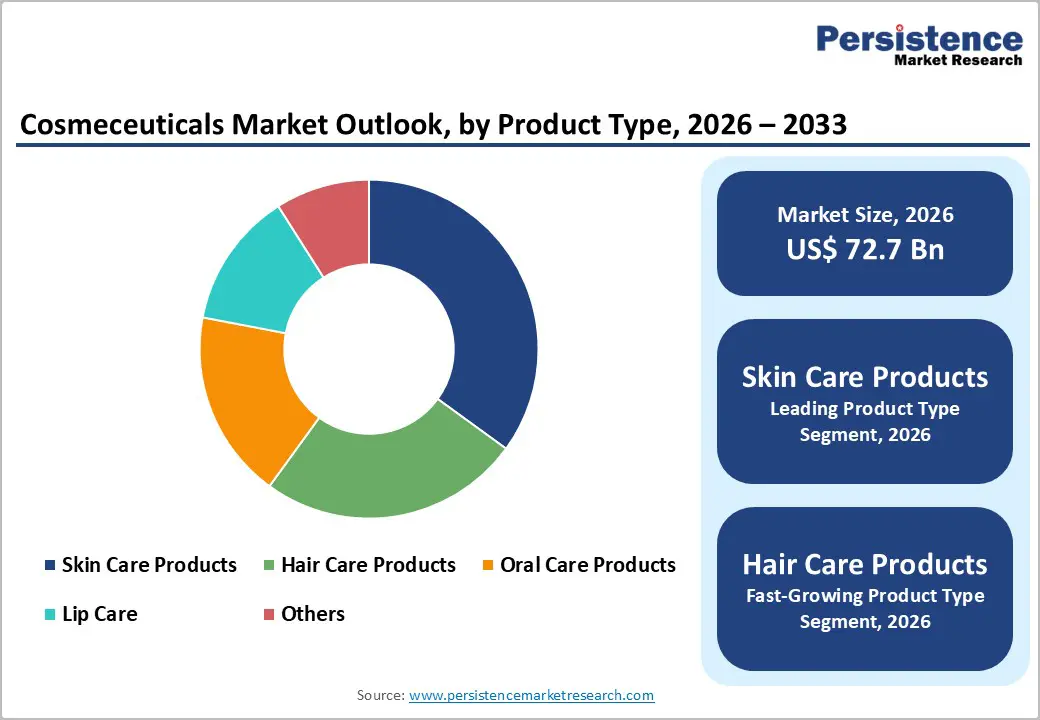

The global cosmeceuticals market size is likely to be valued at US$ 72.7 billion in 2026, and is projected to reach US$ 96.3 billion by 2033, growing at a CAGR of 4.1% during the forecast period 2026−2033. Growth is driven by rising clinical awareness of preventive skincare and integration of advanced cosmeceutical formulations into daily routines.

Evidence-based treatments enhance consumer confidence, increasing acceptance of therapeutic products. Urbanization and an aging population are driving demand for anti-aging and dermatology-focused solutions, while consumers are leveraging digital platforms for education and discovery. The use of bioactive compounds, peptide complexes, and nanotechnology improves efficacy and credibility, thereby supporting wider adoption. Improvements in healthcare infrastructure enable access to professional-grade products, and regulatory oversight ensures safety, reinforcing trust.

Key Industry Highlights

- Leading Product: Skin care products are expected to lead with an estimated 35% revenue share in 2026, due to clinical validation and dermatology endorsements.

- Fastest-Growing Product: Hair care products are likely to represent the fastest-growing segment through 2033, driven by preventive hair health awareness and digital commerce adoption.

- Leading Ingredient Type: Retinoids are poised to lead with around 30% revenue share in 2026, supported by dermatology recommendations and proven efficacy.

- Fastest-Growing Ingredient Type: Peptides & proteins are projected to be the fastest-growing from 2026 to 2033, owing to regenerative benefits and preventive healthcare trends.

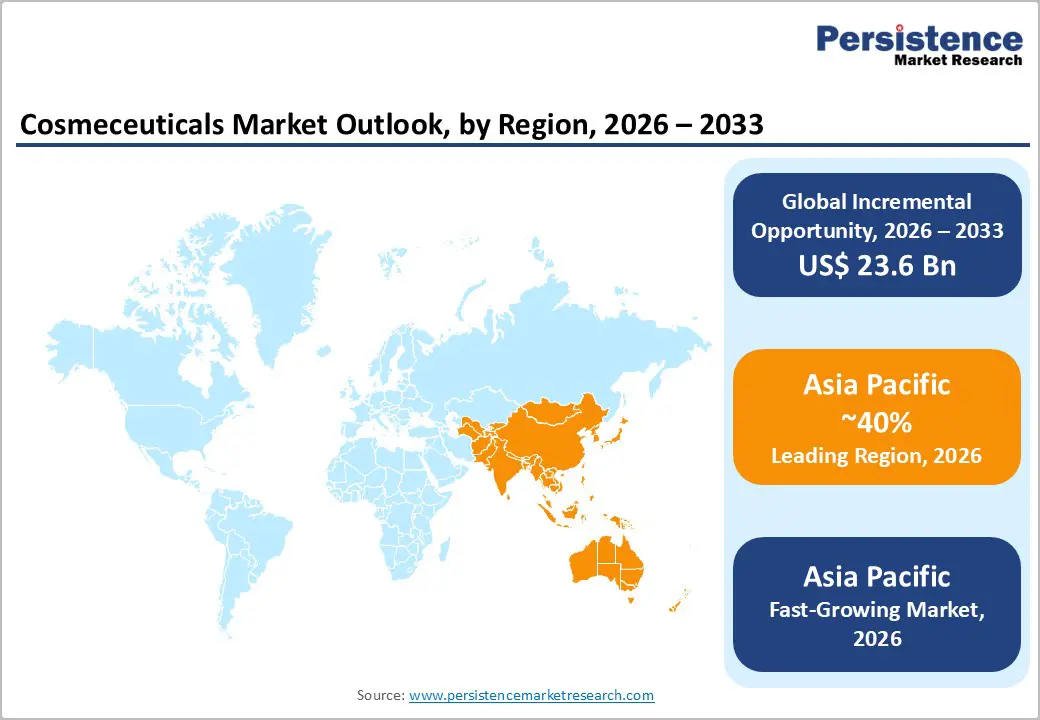

- Regional Insights: Asia Pacific is anticipated to dominate with roughly 38% market share in 2026, and the market here is set to grow the fastest, powered by higher discretionary spending and evolving regulatory frameworks.

- March 2026: Obagi Medical launched NU-GEN™ Cellular Renewal Serum, a clinically backed anti-aging formulation targeting skin tone, hydration, and visible signs of aging.

| Key Insights | Details |

|---|---|

|

Cosmeceuticals Market Size (2026E) |

US$ 72.7 Bn |

|

Market Value Forecast (2033F) |

US$ 96.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.5% |

DRO Analysis

Increasing Clinical Awareness and Preventive Skincare Adoption

Clinical awareness and the adoption of preventive skincare drive demand as more consumers seek professional guidance on skin health. Regular dermatological checkups and education help detect early signs of issues such as sun damage and pre-cancerous conditions, encouraging the use of targeted products. Rising health literacy leads individuals to invest in products with proven benefits rather than general cosmetics. Awareness of dermatology care supports informed decisions on protection against UV exposure and on the treatment of chronic conditions, shifting spending toward products that deliver measurable outcomes.

Federal health data show that routine wellness visits among U.S. adults were 76.2% in 2022, underscoring widespread engagement in preventive care practices, including skin health screening. Preventive skincare aligns with public health priorities by reducing long-term treatment costs related to chronic skin conditions and cancers. As more people adopt preventive health behaviors, demand grows for formulations supported by clinical evidence. Professional validation enhances confidence in product efficacy, supporting higher adoption rates of science-based skin therapies and protective regimens.

Technological Integration and Digital Commerce Expansion

Digital commerce is reshaping consumer buying patterns by enabling wider product reach and convenient transactions. Online platforms allow brands to sell products at scale without the limitations of store footprints. Consumers increasingly prefer shopping online due to ease of browsing, direct-to-consumer engagement and access to detailed product information. Digital channels also support social commerce and mobile purchases, rapidly converting browsing into sales. U.S. retail e-commerce sales in 2025 accounted for 16.4% of total retail sales, reflecting a sustained consumer shift toward online buying and higher digital engagement.

Technology integration improves product discovery and customer experience across digital touchpoints. Tools such as artificial intelligence (AI)-driven recommendations, virtual try-ons, and personalized skincare assessments help match users with tailored solutions. Data analytics enable precise targeting of consumer segments and optimize marketing spend. Advanced fulfilment technologies and secure payment systems reduce friction in checkout and support repeat purchases. These innovations strengthen brand loyalty and lower acquisition cost, encouraging companies to invest in digital ecosystems that drive sales growth and competitive differentiation.

Regulatory Complexity and Compliance Costs

Regulatory frameworks in major markets require companies to register manufacturing sites, list every product and ingredient, report serious adverse events, and update safety substantiation and labelling information under rules such as the U.S. Modernization of Cosmetics Regulation Act (MoCRA) enforced in 2025. These obligations demand legal review, documentation, scientific testing, and ongoing reporting workflows. Facilities must renew registrations, maintain records, and adjust products to comply with updated U.S. Food and Drug Administration (FDA) guidance for cosmetics and claims. The binary classification between cosmetic and therapeutic categories forces firms to invest in regulatory teams to prevent costly misclassification under government standards.

Meeting these multiple compliance requirements increases operational complexity and costs notably. Firms must align formulations, packaging, and promotional claims with statute and rulebooks that vary across regions. In the United States, full product listing, adverse event reporting and evolving Good Manufacturing Practice (GMP) expectations add administrative burden and expense to innovation and product launches. Organizations often need specialized regulatory staff or consultants, which elevates fixed expense and divert resources from marketing and R&D. With enforcement moving from voluntary to mandatory in 2025, non-compliance risk has grown materially under official policy.

Raw Material Dependency

Supply networks for key ingredients are complex and regulated. Many raw inputs originate overseas and lack domestic alternatives, forcing producers to import supplies through global channels. This reliance increases exposure to trade disruptions, currency volatility, logistics constraints, and regulatory divergence. Laws such as the Cosmetic Supply Chain Transparency Act of 2025 aim to improve upstream visibility of ingredient sources and safety data, signaling a policy response to supply chain gaps. Limited local sourcing options restrict flexibility in production planning and heighten vulnerability to external shocks, affecting overall operational efficiency and product availability.

Global sourcing also intensifies cost pressures. Suppliers must comply with multiple national frameworks for ingredient safety and classification, reducing the pool of approved materials and extending lead times. Natural actives often face seasonal availability and ecological constraints, while synthetic specialty molecules require advanced facilities concentrated in specific regions. Complex customs processes and tariff regimes further compound these issues, increasing pricing risk for manufacturers. Regulatory compliance and import dependency limit formulation options and can delay product launches, impacting market responsiveness and competitiveness.

Heightening Demand for Natural and Organic Cosmeceuticals

Consumer preference for certified organic ingredients in personal care is supported by independent government-related survey findings showing that roughly 74% of U.S. consumers in 2025 consider organic ingredients important in skincare and related products sold in the market. This strong consumer sentiment reflects rising awareness of product contents and demand for ingredient transparency. Publicly governed standards under the U.S. Department of Agriculture (USDA) National Organic Program define strict conditions under which agricultural ingredients can be labeled organic for consumer products. These standards require third-party certification before a product can claim organic status on packaging, creating a regulated basis for consumer trust.

The regulatory framework for organic labeling by the USDA reinforces the commercial appeal of natural formulations by providing clear criteria that producers must follow for organic claims to be recognized. This encourages manufacturers to reformulate or market products using organic components that comply with these federal rules. Increased consumer focus on ingredient sourcing, safety, and environmental stewardship has encouraged brands to highlight compliance with USDA organic requirements to attract discerning buyers seeking perceived quality and reduced exposure to synthetic additives. Such regulated labeling practices provide a foundation for long-term product differentiation aligned with evolving buyer expectations.

Integration of AI and Personalized Skincare

AI-driven personalization in skincare unlocks precise recommendations tailored to individual profiles. Data from U.S. federal sources show that the FDA actively tracks and authorizes AI-enabled tools that learn from large datasets to improve performance and assist decision making across regulated products, highlighting the broader trend toward customizing digital health solutions. This regulatory support encourages companies to embed machine learning into diagnostic systems that analyze user skin types, conditions, and responses. In 2025 alone, hundreds of FDA-authorized AI solutions demonstrate the rapid expansion of trusted algorithmic tools across health sectors.

Consumers are increasingly expecting individualized experiences, and AI delivers this by processing complex input like genetics, environment, and lifestyle to generate tailored regimens. Recent consumer research shows a majority of users say they prefer personalized recommendations powered by algorithms compared with generic advice. This shift drives stronger engagement and higher conversion rates for brands that implement data-driven personalization. The combination of regulatory momentum and clear consumer preference makes intelligent personalization a strategic growth opportunity for development and differentiation in the sector.

Category-wise Analysis

Product Type Insights

Skin care products are likely to dominate with an estimated 35% of the cosmeceuticals market revenue share in 2026, driven by widespread consumer adoption of anti-aging and dermatology-focused formulations. Clinical efficacy of moisturizers, serums, and topical treatments reinforces provider and consumer trust. Urban populations with disposable income prioritize preventive skincare, increasing demand for clinically validated products. Dermatology clinics and beauty retailers act as key distribution channels, strengthening accessibility and credibility. The integration of peptides, antioxidants, and bioactive compounds enhances therapeutic outcomes and increases adherence to treatment regimens.

Hair care products are expected to grow the fastest between 2026 and 2033, driven by rising awareness of preventive hair health and the increasing adoption of therapeutic shampoos, serums, and topical treatments. Consumers are proactively addressing hair loss, scalp health, and hair aging, leveraging digital platforms for product discovery and clinical guidance. Products that incorporate peptides, vitamins, and botanical extracts deliver measurable benefits, thereby enhancing consumer trust. Distribution expansion through e-commerce, salons, and specialty stores facilitates access to professional-grade formulations.

Ingredient Type Insights

Retinoids are poised to lead by capturing approximately 30% of the cosmeceuticals market share in 2026, owing to widespread clinical endorsement and proven efficacy in anti-aging and acne treatments. Dermatologists frequently recommend retinoid-based formulations, creating strong professional credibility. Consumers perceive retinoids as effective for long-term skin health, enhancing trust and willingness to invest in these products. Retail penetration through pharmacies, specialty stores, and online platforms ensures availability across urban and semi-urban regions. Preventive healthcare adoption drives repeat purchases and adherence, while product innovation in concentration and delivery systems improves tolerability and efficacy.

Peptides & proteins are anticipated to be the fastest-growing segment between 2026 and 2033, driven by rising consumer interest in regenerative and anti-aging solutions. These ingredients offer measurable benefits in collagen synthesis, skin elasticity, and overall skin health, supported by emerging clinical studies. Cultural acceptance of functional skincare and preventive health further amplifies adoption. Digital commerce platforms facilitate awareness and product discovery, while personalized formulations support greater adherence. The expansion of dermatology clinics and salons that incorporate peptide-based treatments creates additional distribution channels.

Regional Insights

Asia Pacific Cosmeceuticals Market Trends and Insights

Asia Pacific is expected to lead with an estimated 38% of the cosmeceuticals market value in 2026, supported by rising demand for advanced skin treatments and cosmetic active ingredient formulations addressing aging and pigmentation concerns. Urban consumers show preference for multifunctional products combining cosmetic appeal with measurable efficacy, driving higher transaction values. Expansion of digital retail channels improves access in tier 2 and tier 3 cities. Domestic brands leverage local ingredients and clinical positioning to capture share from global players. Professional dermatology channels further support sales of clinical-grade actives.

Asia Pacific is forecasted to be the fastest-growing market for cosmeceuticals between 2026 and 2033, stimulated by the rapid adoption of personalized treatment regimens and advanced active technologies. Peptides and botanicals tailored to specific conditions are gaining traction with consumers and practitioners. Influencer-led education increases awareness of product performance, boosting trial rates. Middle-income growth expands the addressable consumer base for premium offerings. Younger demographics show strong engagement with science-driven solutions, accelerating adoption and fostering faster annual uptake.

North America Cosmeceuticals Market Trends and Insights

North America has a substantial presence in the cosmeceuticals market, capturing a significant share due to strong research and development and robust regulatory infrastructure. Consumer focus on anti-aging and wellness-driven skincare drives demand for premium formulations with peptides, antioxidants, and botanicals. Dermatology and aesthetic channels provide reliable distribution for clinical-grade products. Digital marketing platforms enable consumer education on efficacy and safety. Collaborations between biotech and skincare companies accelerate innovation. Professional settings, including clinics and spas, reinforce the adoption of specialized treatment solutions, supporting overall market stability.

North America is expected to maintain steady growth in cosmeceuticals, influenced by demand for scientifically validated products and preventive skincare. AI-driven diagnostic tools allow customization for diverse skin types, improving satisfaction and repeat purchases. Health-conscious lifestyles increase preference for clean, toxin-free formulations. Insurance frameworks support integration of high-efficacy products in clinical practice. Consumer willingness to invest in evidence-backed solutions encourages innovation in delivery systems. Online channels and professional endorsements strengthen brand reach and loyalty.

Europe Cosmeceuticals Market Trends and Insights

Europe maintains a significant position in the cosmeceuticals market, driven by established healthcare infrastructure and strong consumer awareness of preventive skincare solutions. Premium and clinical-grade formulations lead sales through pharmacies, dermatology clinics, and specialized retail chains. Regulatory frameworks ensure safety and efficacy, boosting confidence in advanced actives such as peptides, antioxidants, and retinoids. Aging populations and rising demand for anti-aging products support steady revenue growth. Professional aesthetic treatments enhance brand visibility. Collaboration between research institutions and cosmetic firms drives the development of innovative formulations targeting specific skin concerns.

Market expansion is supported by demand for sustainable and natural formulations appealing to environmentally conscious consumers. Eco-friendly sourcing and transparent labeling differentiate products in competitive markets. Digital engagement and e-commerce platforms improve product discovery and educational content delivery, enhancing consumer trust in high-efficacy solutions. Affluent consumers seek personalized products tailored to skin type and lifestyle. Investment in clinical trials and dermatology partnerships strengthens credibility. Younger demographics show growing interest in preventive and corrective skincare, driving continuous demand growth.

Competitive Landscape

The global cosmeceuticals market exhibits a moderately consolidated structure, with leading players capturing an estimated 50% of total market share. Key companies include L’Oréal, Estée Lauder Companies, Shiseido Company, Limited, Procter & Gamble (P&G), and Unilever. These companies dominate through strong brand recognition, extensive research and development capabilities, and established global distribution networks. Their focus on clinical validation and patented bioactive formulations ensures credibility and product differentiation in premium and mass-premium segments.

Remaining market share is held by regional and emerging manufacturers, creating opportunities for niche product development. Competitive strategies emphasize innovation in active ingredients, integration of digital commerce platforms, and targeted marketing. Multi-channel distribution, including professional dermatology channels and online platforms, supports consumer reach. Endorsements from dermatologists and clinical evidence further strengthen positioning.

Key Industry Developments

- In January 2026, L’Oréal Groupe unveiled breakthrough infrared light-based hair and skin devices at CES 2026, showcasing new beauty-tech innovations recognized with CES Innovation Awards that bring advanced light technology into performance-oriented cosmeceutical applications.

- In August 2025, Alkem Laboratories announced the launch of Olesoft Trucera, a next-generation ceramide-boosting moisturizing lotion designed for skin barrier repair with science-backed actives targeting hydration and barrier strength in clinical-grade skincare solutions.

- In July 2025, P&G launched Gemz, a water-activated, single-dose solid shampoo and conditioner line at Target aimed at simplifying routines and delivering high-performance, active-focused hair care.

Companies Covered in Cosmeceuticals Market

- L’Oréal

- Estée Lauder Companies

- Shiseido Company, Limited

- Procter & Gamble (P&G)

- Unilever

- Johnson & Johnson Consumer Health

- Amorepacific Corporation

- Beiersdorf AG

- Kao Corporation

- Rohto Pharmaceutical Co., Ltd.

- GlaxoSmithKline (GSK) Consumer Healthcare

- Coty Inc.

- Pierre Fabre Group

- Alkem Laboratories

- Hindustan Unilever Limited (HUL)

Frequently Asked Questions

The global cosmeceuticals market is projected to reach US$ 72.7 billion in 2026.

Rising demand for anti-aging, preventive skincare, and clinically validated active-ingredient products is driving the market.

The market is poised to witness a CAGR of 4.1% from 2026 to 2033.

Growth in personalized skincare, natural and organic formulations, and AI-driven solutions presents key market opportunities.

Some of the key market players include L’Oréal, Estée Lauder Companies, Shiseido Company, P&G, and Unilever.