- Beauty & Personal Care

- Perfume Market

Perfume Market Size, Share, Trends, Growth, and Forecasts, 2025 - 2032

Perfume Market By Product Type (Eau De Fraiche (EDF, Eau De Cologne (EDC)), Price Range (Mass, Prestige, Luxury), Nature (Natural, Synthetic), Consumer (Men, Women, Unisex), Sales Channel, Regional Analysis from 2025 to 2032

Perfume Market Share and Trends Analysis

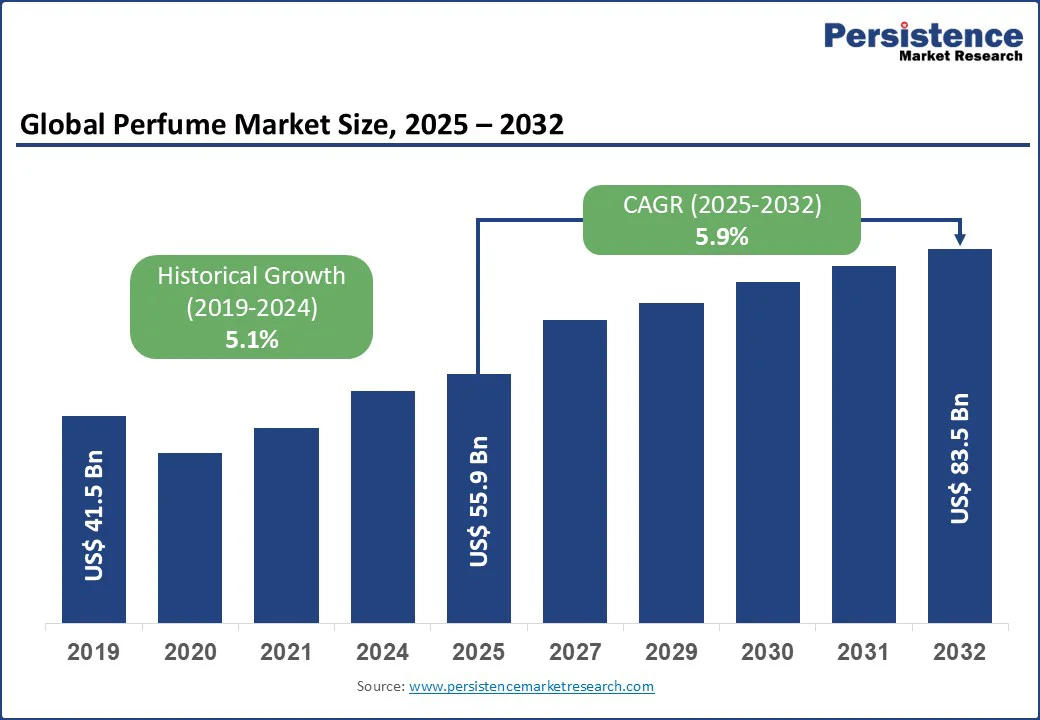

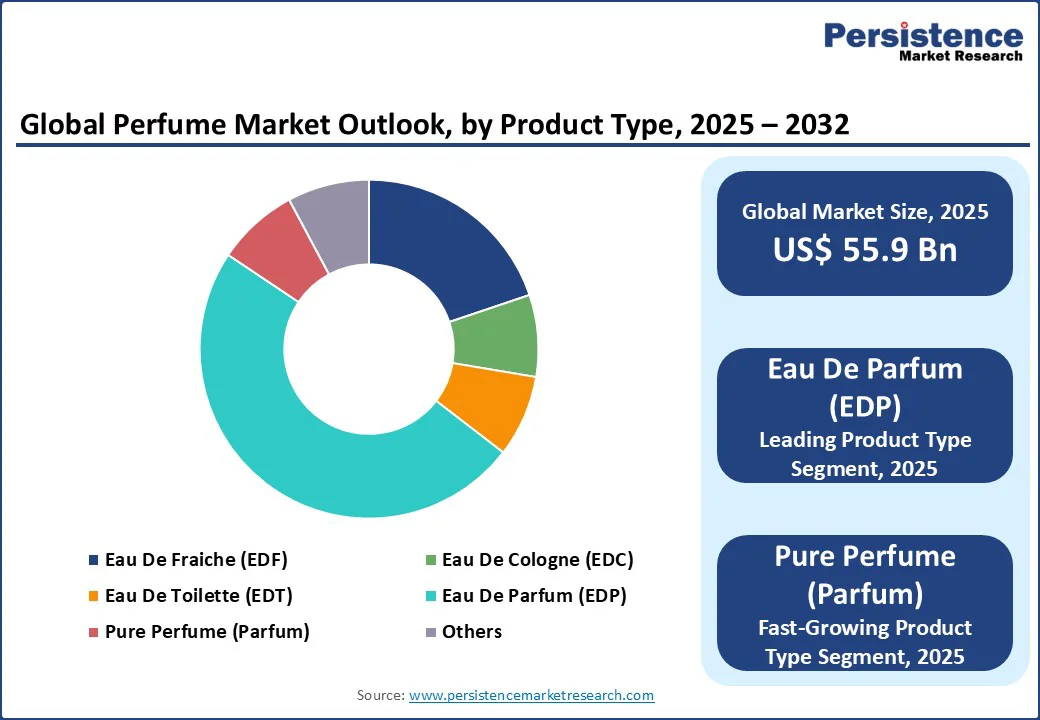

The global perfume market size was valued at US$ 55.9 Bn in 2025 and is projected to reach US$ 83.5 Bn by 2032, growing at a CAGR of 5.9% between 2025 and 2032 due to a shift in consumer preferences towards premium/luxury fragrances, increasing disposable incomes globally, and evolving personal grooming trends across demographic segments.

Key Report Highlights: What Will Set the Pace Through 2032

- Leading Product: Eau De Parfum holds 54.3% market share in 2025, while the Pure Perfume segment is expected to depict fast-paced growth, reflecting consumer premiumization trends and preference for higher-concentration formulations

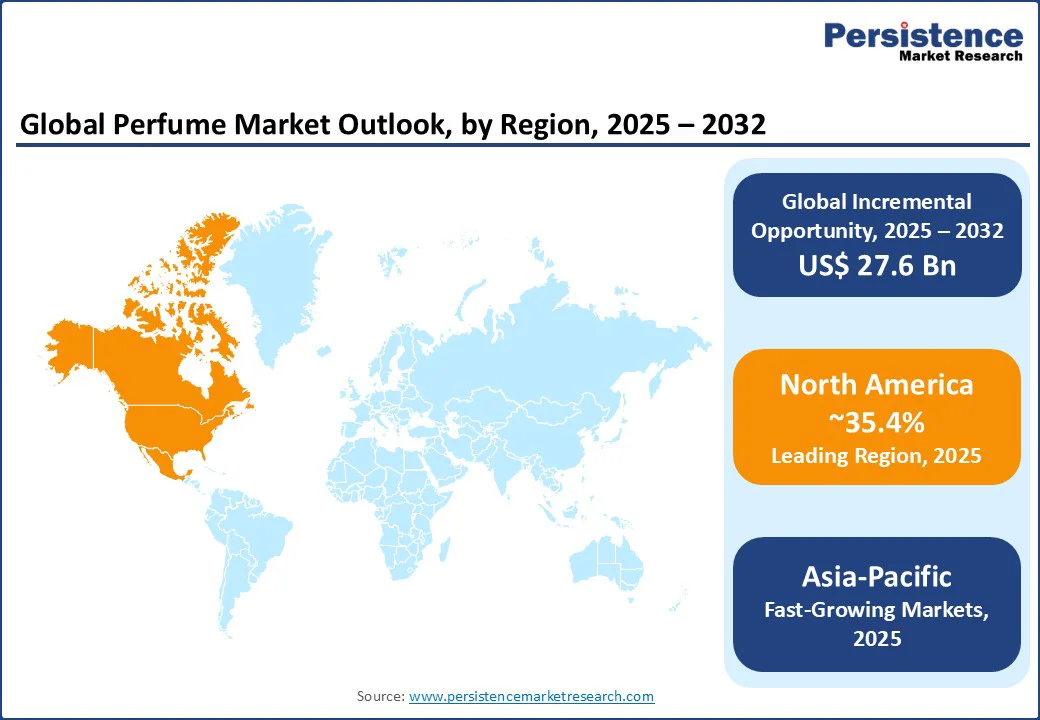

- Regional Leadership: North America leads with projected 35.5% share, while Asia Pacific emerges as the fast-growing region with 6.9% CAGR, driven by rising disposable incomes and expanding middle-class populations in emerging markets

- Consumer Segment Evolution: Women's fragrances maintain nearly 61.7% share while men's segment experiences the highest growth rate at 6.6% CAGR, supported by evolving grooming habits and reduced fragrance usage stigma among male consumers

- Distribution Channel Transformation: Offline channels are likely to dominate with 77.4% share while online platforms are likely to deliver substantial growth, supported by AI-driven personalization, virtual try-on technologies, and influencer marketing strategies

- Trends in Sustainability and Innovation: Natural fragrance ingredients to grow with 95% ingredient traceability through blockchain technology, reflecting consumer demand for transparency and environmentally conscious luxury products

- Strategic Market Developments: Major product launches, including Coty's Burberry Goddess and technology partnerships for AI-driven scent profiling, demonstrate industry innovation, focus on personalization, sustainability, and digital transformation initiatives.

| Key Insights | Details |

|---|---|

| Perfume Market Estimated Market Size (2025E) | US$ 55.9 Bn |

| Perfume Market Projected Market Value (2032F) | US$ 83.5 Bn |

| Value CAGR (2025 to 2032) | 5.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.1% |

Market Factors - Growth, Challenges, and Opportunity Analysis

Drivers - Rising Disposable Incomes are Fueling Luxury Appetite, Driving the Premium Consumption Trends

The increasing global disposable income, particularly in emerging markets (around 15% over the last five years) across the Asia Pacific, Latin America, and the Middle East & Africa, is driving the adoption of premium fragrances.

Consumer spending on luxury personal care products has risen significantly, with millennials and Gen Z consumers prioritizing fragrance as part of their lifestyle expression. Consumer preferences are shifting toward luxury and personalized fragrance experiences, with growing emphasis on natural ingredients and sustainability initiatives.

According to industry analysis, over 60% of consumers in developed markets now prefer investing in single high-quality fragrances rather than multiple cheaper alternatives, indicating sustained premiumization trends. This shift toward premium consumption is supported by rising urbanization rates and growing middle-income population in key emerging economies, creating substantial opportunities for perfume market expansion.

Increasing Innovation in Natural and Sustainable Perfume Formulations to Carve a Path for Competitive Advantage

Growing consumer awareness regarding ingredient safety and environmental impact has accelerated demand for natural and sustainable fragrance formulations. The natural fragrance segment is experiencing robust growth, driven by consumer preferences for clean beauty products and ethical sourcing practices.

Leading brands are investing in biotechnology innovations, upcycled ingredients, and refillable packaging solutions to meet evolving consumer expectations. Blockchain technology enables 95% ingredient traceability across major fragrance houses, addressing transparency demands while supporting premium positioning strategies.

Challenges - Regulatory Maze: Navigating Complex Compliance in Global Markets

Stringent regulatory frameworks governing fragrance formulations, particularly in Europe and North America, create significant compliance costs for manufacturers. New safety regulations require extensive reformulation processes and testing protocols, impacting time-to-market for new product launches.

The increasing restrictions on certain natural ingredients due to sustainability concerns and the complex approval processes for synthetic alternatives create operational challenges for fragrance houses, potentially limiting innovation speed and increasing development costs.

Authenticity Under Siege: Combat Strategies Against Counterfeit Erosion

The proliferation of counterfeit "dupe" fragrances poses significant threats to brand equity and market share for premium fragrance manufacturers. These imitation products erode brand positioning and reduce consumer willingness to pay premium prices, suppressing industry growth by nearly two percentage points, according to recent analysis.

The difficulty in protecting scent compositions legally, combined with sophisticated counterfeit manufacturing capabilities, requires substantial brand protection investments from legitimate manufacturers.

Market Opportunities

Technology-Enabled Personalization and Customization

Advances in AI-driven scent matching, personalized fragrance creation platforms, and data analytics create opportunities for brands to offer highly customized fragrance experiences. The growing demand for bespoke and limited-edition fragrances, particularly among affluent consumers, supports premium pricing strategies and enhanced brand loyalty.

Technology integration in retail experiences, including virtual try-on capabilities and interactive scent discovery platforms, enables brands to differentiate their offerings and improve conversion rates across digital and physical channels.

Circular Economy Leadership: Sustainability as a Strategic Differentiator

The growing emphasis on sustainability creates opportunities for brands that successfully integrate eco-friendly practices throughout their value chains. Refillable packaging systems, biotechnology-derived ingredients, and circular economy principles are becoming competitive differentiators that command premium pricing.

Companies that invest in renewable carbon solutions, green chemistry, and transparent supply chain practices are positioned to capture growing market share among environmentally conscious consumers while meeting evolving regulatory requirements.

Category-wise Analysis

Product Type Analysis - Concentration Supremacy: Why Eau De Parfum (EDP) Commands the Premium Throne

Eau De Parfum commands the largest market share at 54.3% of total market revenue in 2025, reflecting consumer preferences for longer-lasting, higher-concentration fragrances.

The EDP segment benefits from premium positioning and superior performance characteristics, with fragrances typically lasting 6-8 hours compared to lighter concentrations. This dominance is supported by consumer willingness to invest in higher-quality formulations that offer enhanced longevity and projection.

The EDP segment's leadership position is reinforced by successful product launches from major brands, including notable successes such as Coty's Burberry Goddess fragrance, which achieved record sales across multiple markets following its August 2023 launch. Consumer education regarding fragrance concentrations has evolved significantly, with marketing strategies emphasizing scent longevity and projection as key value propositions.

The pure perfume segment is experiencing rapid growth outpacing other concentration categories as consumers are increasingly seeking ultra-premium fragrance experiences. This growth reflects the market's shift toward luxury positioning, with consumers willing to pay premium prices for the highest concentration and most exclusive formulations. The segment benefits from limited-edition releases and artisanal positioning strategies that emphasize craftsmanship and exclusivity.

Price Range Analysis - Luxury Perfumes Unstoppable Ascent: Premium Positioning Drives Profitability

The luxury price segment is likely to account for 37.5% share in 2025, demonstrating robust consumer demand for premium fragrance experiences. The luxury perfume market is projected to grow over US$ 40 Bn by 2032, significantly outpacing mass market growth rates. This performance is driven by affluent consumer segments seeking exclusive, high-quality fragrances that reflect personal identity and social status.

Luxury brands are successfully leveraging heritage storytelling, celebrity endorsements, and limited-edition collections to maintain premium positioning. The segment benefits from expanding affluent populations in emerging markets, particularly in China and India, where luxury fragrance adoption is accelerating rapidly among younger demographics.

Mass Perfume Market's Resilient Foundation Strategy Makes It Volume Champion

While luxury segments command premium pricing, the mass market segment maintains significant volume leadership and accessibility for broader consumer segments. Mass market fragrances benefit from widespread retail distribution, aggressive promotional strategies, and celebrity brand partnerships that drive volume sales across diverse demographic groups.

Consumer Segmentation Analysis

Women's Perfume Maintains Leadership Through Innovation

Women's fragrances represent 61.7% of total perfume market revenue, maintaining traditional leadership in fragrance consumption patterns. The women's segment benefits from diverse product offerings spanning multiple fragrance families, seasonal collections, and occasion-specific formulations that encourage multiple purchases per consumer.

Recent launches in the women's segment, including Carolina Herrera's Good Girl variants and YSL's Libre collection, have achieved strong double-digit growth rates, demonstrating continued vitality in this core market segment. The segment's strength is supported by sophisticated marketing campaigns, influencer partnerships, and emotional branding strategies that resonate with female consumers across age groups.

The Male Grooming Revolution: Capturing Emerging Masculine Luxury

The men's fragrance segment is experiencing the highest growth rates driven by evolving grooming habits and increased fragrance adoption among younger male consumers. Male teens have increased perfume spending by 26% year-over-year, with preferences favoring sophisticated scents from premium brands including Jean Paul Gaultier, Valentino, and Dior Sauvage.

This growth reflects changing masculine identity concepts and reduced stigma around fragrance usage among men. The segment benefits from targeted marketing campaigns, sports celebrity endorsements, and product formulations designed specifically for male preferences, including woody, spicy, and fresh fragrance profiles.

Regional Market Insights

North America Perfume Market Trends

North America represents the largest regional market with over 35.0% global market share in 2025. The region demonstrates mature market characteristics with sophisticated distribution networks, high per-capita fragrance consumption, and strong brand loyalty patterns.

U.S. Perfume Market Trends

The U.S. Perfume Market is projected to surpass US$ 25 Bn by 2032, driven by affluent consumer spending and a well-established luxury retail infrastructure. The U.S. market benefits from premiumization trends, with consumers increasingly investing in higher-concentration fragrances and luxury brands.

For instance, InterParfums Inc. reported 85% sales growth in North America during 2024 compared to 2019 levels, reflecting robust demand recovery and consumer preference shifts toward prestigious brands, including Chanel, Dior, and Tom Ford.

Direct-to-consumer (DTC) business models gained significant traction during the pandemic and continue expanding through digital marketing strategies and subscription services. Major retailers, including Sephora, have expanded luxury fragrance offerings with expectations for business doubling in the coming years, supported by growing consumer interest in premium personal care products.

Consumer's education initiatives regarding fragrance layering and personalization have created opportunities for premium product positioning and multiple product purchases.

Europe Perfume Market Trends

Europe maintains its position as the heritage center of global perfumery. The region demonstrates the most mature market characteristics globally, with sophisticated consumer bases that drive quality and innovation standards worldwide.

France, Germany, Italy, Spain, and the U.K. represent the core markets in the European perfume industry, with France exporting over US$10 billion annually, leading the global perfume exports.

European fragrance houses successfully balance traditional perfumery craftsmanship with modern consumer demands for sustainability and transparency. The region's luxury brands leverage heritage storytelling and artisanal positioning to maintain premium pricing while investing in digital technologies and omnichannel retail experiences.

France Perfume Market Trends: Niche Brand Experiencing Robust Demand

Niche perfume brands in France are experiencing particularly strong growth, supported by consumer preferences for unique and personalized fragrance experiences. Premiumization trends in France are strongly evident. Over 60% consumers prefer premium fragrance investments. The region benefits from well-established specialty retail networks, department store partnerships, and growing e-commerce platforms that support both heritage and emerging brands.

Leading brands have achieved 95% ingredient traceability through blockchain technology and invest significantly in eco-friendly packaging solutions, including refillable systems and recycled materials. Europe leads global sustainability initiatives in fragrance manufacturing, with the European Commission's Horizon 2020 Strategy promoting natural ingredient production and consumption across the chemical and personal care sectors.

Asia Pacific Perfume Market Trends

Asia Pacific emerges as the fastest-growing regional market with over 6.0% CAGR projected through 2032, driven by rapid economic development, urbanization, and evolving consumer preferences across diverse cultural markets.

The region represents significant untapped potential, with current fragrance penetration rates substantially below those of developed markets, creating substantial expansion opportunities for both international and domestic brands. The region's diverse cultural landscape requires customized marketing approaches and product formulations that resonate with local preferences while maintaining global brand consistency.

Successful brands in the Asia Pacific region implement sophisticated localization strategies that incorporate regional cultural preferences and climate considerations. Chinese consumers favor luxury brands and giftable fragrances, while Indian preferences shift toward light floral scents appropriate for tropical climates.

Japan and South Korea maintain sophisticated markets with preferences for fresh, floral, and fruity scent profiles, while India presents substantial growth opportunities with rising urban populations and increasing personal grooming awareness.

China Perfume Market: Regional Dominance Continues with the Adoption of Luxury Products

China dominates regional market leadership, representing the largest individual country market within Asia Pacific, supported by expanding middle-class populations and growing disposable incomes. The Chinese market demonstrates strength in luxury fragrance adoption, with consumers showing strong preferences for international premium brands and giftable fragrance products.

India Perfume Market: On a Track for Dynamic Double-digit Growth

India's perfume market is experiencing rapid growth, with revenues projected to exceed US$3.1 billion by 2032. Key growth drivers include rising disposable incomes, urbanization, and an aspirational middle class, especially millennials and Gen Z, who increasingly view fragrances as expressions of identity and lifestyle rather than mere luxury items.

E-commerce adoption and digital-first discovery, leveraging AI personalization tools and influencer marketing, are reshaping purchase patterns, making premium perfumes and customized fragrances more accessible across urban and semi-urban centers.

Demographically, India’s young population and expanding middle class, notably the 26-35 age group, power this surge, with women leading luxury perfume consumption and a notable rise in the unisex and men’s segment demand.

Competitive Landscape

The perfume market competitive landscape reflects a hybrid market structure where established luxury perfume houses compete alongside mass market manufacturers and emerging niche brands. Leading players, including Coty Inc., Estée Lauder, Chanel, Shiseido Co. Ltd., L'Oréal, and LVMH (Moët Hennessy Louis Vuitton), maintain dominant positions through extensive brand portfolios, global distribution networks, and substantial marketing investments.

Market leadership is maintained through continuous innovation, strategic acquisitions, and premium brand positioning strategies that command higher margins and consumer loyalty. Digital-native challenger brands are disrupting traditional distribution models through direct-to-consumer platforms, subscription services, and social media marketing strategies that appeal particularly to younger demographic segments.

The perfume industry's leading companies employ diversified strategic approaches emphasizing innovation, sustainability, and digital transformation to maintain competitive positioning. Dominant strategic themes include premiumization through higher-concentration formulations, expansion of natural and organic product lines, and investment in direct-to-consumer digital platforms that enable personalized customer experiences.

Innovation and customization represent key differentiators, with market leaders investing substantially in AI-driven scent matching, biotechnology-derived ingredients, and personalized fragrance creation platforms. These investments enable premium pricing strategies while building stronger consumer relationships through unique, tailored fragrance experiences that encourage brand loyalty and repeat purchases.

Recent Developments:

- In January 2025, Estée Lauder Companies entered an exclusive partnership with Exuud Inc. to integrate Soliqaire™ smart fragrance expression hardware into its fragrance portfolio by late 2025. The innovation includes biodegradable plant polymers to deliver precise, customizable, and sustainable fragrance experiences across ELC’s luxury range.

- In August 2025, Chanel launched BLEU DE CHANEL L’EXCLUSIF, crafted by Olivier Polge. The fragrance emphasizes an amber-woody, sandalwood-rich trail with sustainable sourcing from Maré, New Caledonia, reinforcing both olfactory uniqueness and ethical practices.

- In November 2024, Parfums Christian Dior opened its first fragrance and beauty boutique in SoHo, New York. The store features La Collection Privée Christian Dior, along with iconic fragrances, skincare, and makeup. It includes a Haute Parfumerie by Francis Kurkdjian and offers personalized fragrance and makeup consultations.

- In July 2024, Hermès reported 15% revenue growth at constant rates in 1H 2024, driven by successful fragrance introductions. Recurring operating income reached £2.6 billion (€3.1 billion). Perfume and beauty grew by 5%, strengthening Hermès’ strategy of innovative fragrance launches.

Companies Covered in Perfume Market

- LVMH (Moët Hennessy Louis Vuitton)

- The Estée Lauder Companies Inc.

- Shiseido Co. Ltd.

- Chanel

- Hermès

- Giorgio Armani S.p.A.

- L’Oréal Luxe

- Kering Beauté

- Puig S.P.A.

- Coty Inc.

- Richemont Group

- Amouage

- Parfums de Marly

- Diptyque

- Penhaligon’s

Frequently Asked Questions

The Global Perfume Market is projected to be valued at US$55.9 Bn in 2025.

Eau De Parfum (EDP) is expected to hold a 54.3% market share in 2025, driven by its balance of long-lasting scent and premium positioning.

The perfume market is poised to witness a CAGR of 5.9% from 2025 to 2032.

E-commerce disruption, powered by AI-driven scent profiling, social media influence, and virtual shopping tools, is redefining fragrance discovery and boosting online sales.

Technology-enabled personalization and circular economy leadership creates opportunities for customized, sustainable, and premium-positioned fragrances.

The key market players in the global perfume market include LVMH (Moët Hennessy Louis Vuitton), The Estée Lauder Companies Inc., Kering Beauté, L’Oréal Luxe, Chanel S.p.A., Hermès, etc.