- Food Ingredients & Additives

- Pectin Market

Pectin Market Size, Share, and Growth Forecast, 2026-2033

Pectin Market by Source (Apple, Citrus Fruits, Sugar Beet, Others), Function (Emulsifier, Thickener, Stabilizer, Gelling Agent, Fat Replacer, Coating), Application (Food Products, Pharmaceuticals, Personal Care Products, Industrial Applications), and Regional Forecast for 2026-2033

Pectin Market Share and Trends Analysis

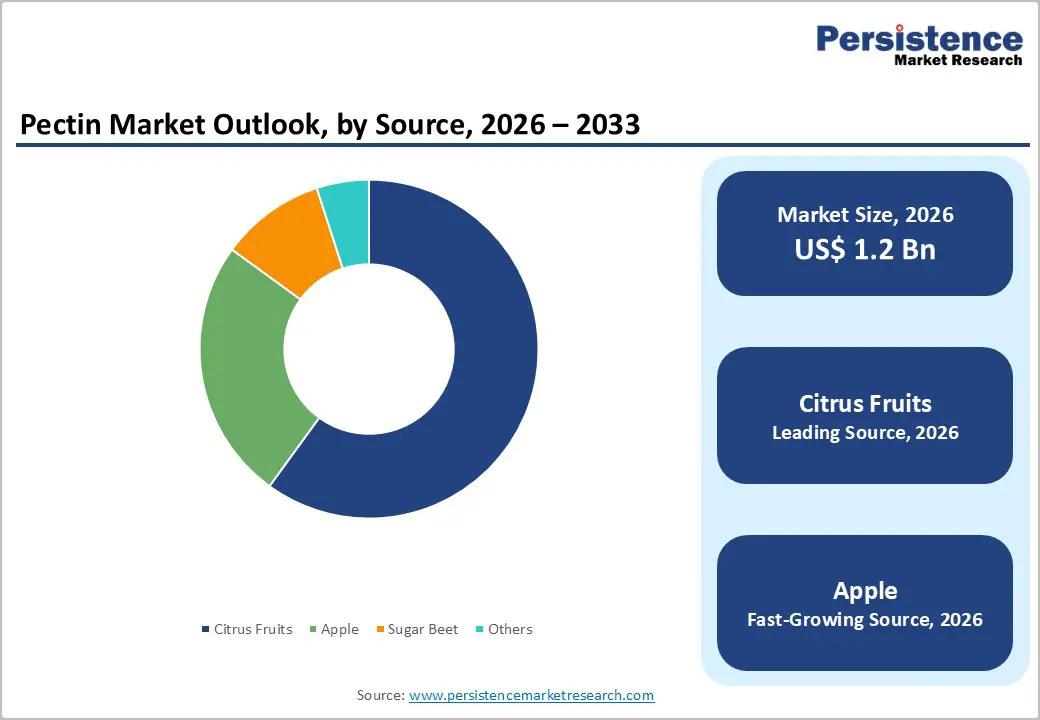

The global pectin market size is likely to be valued at US$ 1.2 billion in 2026, and is projected to reach US$ 1.8 billion by 2033, growing at a CAGR of 6% during the forecast period 2026-2033. This growth is primarily following a sharp rise in consumer demand for clean-label food ingredients and plant-based hydrocolloids. Food and beverage manufacturers are currently replacing synthetic additives with fruit-derived pectin to meet the needs of health-conscious consumers. These dynamics are ensuring that pectin remains a staple ingredient in the formulation of jams, jellies, and dairy alternatives worldwide.

Industrial stakeholders are currently diversifying the application of pectin as a functional excipient in pharmaceutical and personal care formulations. In the medical sector, researchers are using this natural polysaccharide for controlled drug-delivery systems and advanced wound-healing dressings. Simultaneously, personal care brands are incorporating pectin into creams and ointments as a natural texturizer and stabilizer. Manufacturers are also presently optimizing production economics by upcycling fruit-processing by-products, such as citrus peels and apple pomace. These circular-economy practices are expected to stabilize raw-material supplies and support the large-scale adoption of natural additives across multiple industries.

Key Industry Highlights

- Dominant Source Type: Citrus-based pectin is projected to hold around 60% share in 2026, supported by large-scale citrus processing, while apple-based pectin is expected to grow fastest at 7.2% CAGR through 2033, driven by pharmaceutical and nutraceutical uptake.

- Leading Function: Gelling agents are anticipated to dominate with approximately 45% share in 2026, reflecting strong food industry demand, whereas fat replacer applications are likely to expand at 7.8% CAGR due to low-fat reformulation trends.

- Primary Application Area: Food products are expected to lead with nearly 65% share in 2026, underpinned by clean-label adoption, while pharmaceutical applications are forecast to grow fastest at a 8.1% CAGR through 2033, driven by rising excipient usage.

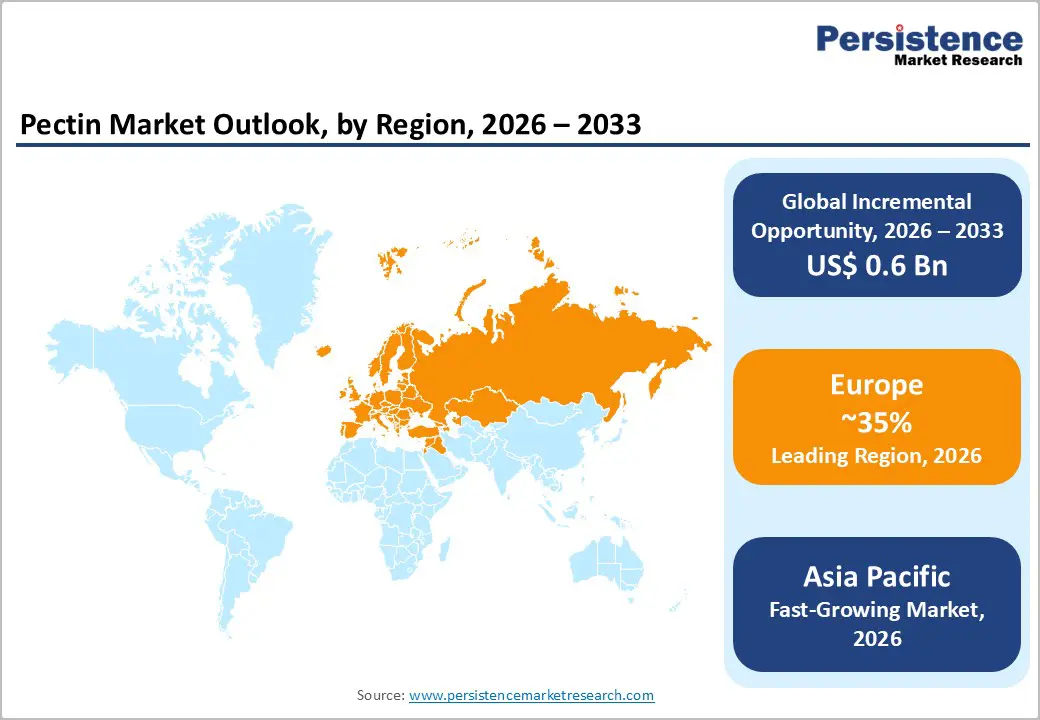

- Regional Leadership: Europe is projected to account for around 35% of global pectin demand in 2026, while the Asia Pacific is set to register the fastest growth at a 7.5% CAGR through 2033, led by expansion in food processing and pharmaceutical manufacturing.

- Competitive Environment: Market competition is characterized by capacity expansions, citrus peel integration, and low-sugar pectin launches, with leading players focusing on specialty grades, regional scale-up, and application-specific innovation.

- April 2025: DSM-Firmenich increased its ownership stake in Yantai DSM Andre Pectin Company Limited to 90.5%, reinforcing its position in the specialty pectin ingredient market.

| Key Insights | Details |

|---|---|

| Pectin Market Size (2026E) | US$ 1.2 Bn |

| Market Value Forecast (2033F) | US$ 1.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory Alignment, Functional Nutrition, and Circular Sourcing Supporting Market Expansion

According to the European Food Safety Authority (EFSA) and the U.S. Food and Drug Administration (FDA), consumer preferences are shifting toward recognizable, plant-derived ingredients, particularly in jams, dairy alternatives, and confectionery. Pectin, derived mainly from citrus peels and apple pomace, aligns with regulatory definitions of natural additives, positioning it as a preferred substitute for synthetic stabilizers. This transition supports reformulation efforts to replace artificial texturizers. As a result, the role of pectin in clean-label food formulations continues to strengthen across both developed and emerging markets.

The World Health Organization (WHO) emphasizes dietary fiber intake as a public health priority, directly supporting pectin demand as a soluble fiber ingredient. According to Codex Alimentarius standards, pectin is approved globally as a functional fiber ingredient, enabling broad international commercialization. Pharmaceutical manufacturers also utilize pectin as a controlled-release excipient due to its gel-forming properties, expanding its role beyond food applications. The Food and Agriculture Organization (FAO) also highlights that citrus and apple processing generates significant peel and pomace waste. This strengthens pectin’s position as a sustainable, circular ingredient with long-term raw material availability advantages.

Supply Chain Sensitivity and Competitive Substitution Limiting Pricing Stability

Pectin production depends heavily on citrus fruits and apples, both of which are subject to seasonal yield variability and climate-related disruptions. Irregular harvest patterns driven by droughts, excessive rainfall, and disease pressure have led to uneven citrus processing volumes, directly affecting the availability of peel by-products used for pectin extraction. The shifts in juice consumption patterns in mature markets have prompted processors to adjust throughput levels, resulting in inconsistent peel generation across seasons. These conditions limit manufacturers’ ability to secure stable long-term feedstock contracts and increase reliance on spot sourcing. As a result, raw material price volatility continues to introduce uncertainty into pectin producers' supply planning and margin management.

The global hydrocolloids market presents sustained competitive pressure from alternative ingredients such as xanthan gum, carrageenan, and guar gum. Some substitutes offer viscosity comparable to or higher than that of the original at lower inclusion rates, particularly in cost-sensitive and industrial formulations. Variability in regulatory treatment across regions increases formulation switching risk for manufacturers seeking pricing stability. These competitive dynamics constrain pectin suppliers' ability to fully pass through raw-material cost increases, especially in commodity food applications. These supply chain sensitivity and substitution risk structurally limit pricing stability despite steady end-use demand.

Health-Led Reformulation and Emerging-Market Processing Infrastructure Creating Scalable Demand

WHO sugar-reduction guidelines have accelerated reformulation across jams, beverages, and confectionery, increasing the need for functional ingredients that support lower sugar content without compromising texture. Low-methoxyl pectin enables gel formation with reduced sugar content, making it critical for sugar-free and diabetic-friendly foods. Food manufacturers increasingly depend on pectin to maintain product consistency while meeting evolving nutritional targets. This reformulation trend supports incremental demand across premium and functional food categories. Adoption is strongest where health labeling and dietary awareness influence purchasing decisions. As reformulation accelerates, pectin’s functional relevance continues to strengthen.

Regulatory acceptance and infrastructure development are expanding pectin’s application footprint. Approvals from the U.S. FDA and European Pharmacopoeia support its use in oral formulations, strengthening demand in pharmaceutical excipient applications. Growth in generic drug manufacturing further reinforces this opportunity. In parallel, government-backed food parks and agri-processing clusters in India and Southeast Asia improve the efficiency of ingredient sourcing. For example, Wilmar International, a leading agribusiness in Singapore, has expanded processing and value-added food production across ASEAN, enabling higher utilization of natural stabilizers such as pectin. These developments reduce logistics inefficiencies and support scalable demand for pectin across bakery, fruit preparation, and dairy alternative applications.

Category-wise Analysis

Source Insights

Citrus fruits are projected to remain the leading source segment, accounting for an estimated 60% of the pectin market revenue share in 2026, supported by robust juice processing industries that generate abundant citrus peel by-products for pectin extraction. Citrus pectin’s high galacturonic acid content ensures consistent gel strength, making it the default choice in jams, fruit fillings, and other clean-label products. Südzucker expanded its processing footprint by acquiring Hindustan Pectin’s citrus peel facility in India, reinforcing supply continuity and feedstock access for its global pectin operations. This acquisition enhances its ability to meet demand from food and beverage formulators in Asia and Europe. Regulatory acceptance and enhanced processing technologies further anchor citrus pectin’s leadership. Downstream food manufacturers benefit from this stable raw material base.

Apple-derived pectin is the fastest-growing source segment with a projected 7.2% CAGR through 2033, driven by increasing apple processing output and adoption where cleaner flavor profiles are vital. Cargill has been actively upcycling apple pomace and citrus peels into versatile texturizers, broadening its food-grade pectin solutions for reduced-sugar and plant-based applications. This supports expansion into the nutraceutical and functional food segments, where taste neutrality and clean-label status are key. Advances in sustainable extraction technologies increase yield efficiency and reduce waste. The diversification of source streams also mitigates seasonal citrus supply risks, further bolstering apple pectin’s growth prospects.

Function Insights

Gelling agents are expected to maintain dominance, with an estimated 45% share of the pectin market in 2026, driven by their foundational use in fruit preserves, jams, bakery fillings, and other food products where texture and stability are essential. Pectin’s inherent gelling properties complement clean-label and plant-based formulation trends, enabling manufacturers to reduce reliance on synthetic stabilizers. DuPont Nutrition & Biosciences launched a new pectin-derived texturizer tailored for vegan gummies and yogurts, reinforcing gelling pectin’s core functional role in emerging categories. Ingredient developers continue investing in performance consistency and customization for gelling applications. This sustains broad manufacturer adoption across diverse food segments. Electronic traceability programs also enhance supply chain transparency for gelling functionalities.

The functions of fat replacer and stabilizer are expected to grow at the fastest rate, 7.8% CAGR, through 2033, as demand surges for low-fat dairy alternatives and plant-based beverages. Recent grade innovations enable pectin to enhance mouthfeel and emulsification in complex matrices such as vegan cheeses, creamy beverages, and fat-reduced sauces. CP Kelco introduced organically derived pectin powders with tailored functionalities that improve stabilizing performance in dairy and non-dairy drink applications, supporting this shift. These enhanced functional blends allow formulators to optimize sensory quality and texture without synthetic additives, accelerating adoption in growing health-oriented segments and premium product lines.

Application Insights

Food products are projected to remain the largest application segment with about 65% revenue share in 2026, driven by ongoing demand from processed fruit products, bakery fillings, reduced-sugar spreads, and confectionery. Clean-label initiatives and natural texture preferences underpin this dominance as food manufacturers increasingly seek plant-derived functional ingredients. Cargill reopened its Singapore innovation center to accelerate food product development using pectin, enabling regional food companies to complete formulation work more quickly. This strategic move supports greater utilization of pectin across consumer food lines, as health and sustainability claims evolve. Better traceability and ESG alignment reinforce pectin’s role in global food portfolios. Ongoing product innovations continue to enhance performance in jams, vegan desserts, and reduced-sugar applications.

Pharmaceutical applications are expected to register the fastest growth, 8.1% CAGR through 2033, propelled by rising excipient demand and advanced controlled-release systems benefiting from pectin’s biocompatibility and gel-forming properties. Regulatory approvals for natural excipients in major markets enable broader use of pectin in oral and targeted drug delivery formats. Cargill expanded its pharmaceutical pectin offering with UniPECTINE® grades engineered for controlled-release and film-forming performance, supporting advanced oral formulations adaptable for colon-targeted delivery. This expansion strengthens pectin’s role in high-value, pharmaceutical applications. As formulators increasingly prioritize natural and functional excipients, pectin’s strategic importance continues to widen, complementing its core food applications.

Regional Insights

North America Pectin Market Trends

North America is a key market for pectin, led by the United States, where advanced food processing infrastructure and strong consumer demand for clean-label products continue to drive adoption. Regulatory frameworks that emphasize natural ingredients support replacing synthetic stabilizers in jams, beverages, and plant-based foods. High penetration of low-sugar and functional food products further reinforces this trend. The U.S. Department of Agriculture (USDA) awarded competitive grants under its Specialty Crop Research Initiative to support sustainable ingredient development, including projects that enhance the processing efficiency of functional ingredients, thereby indirectly benefiting pectin utilization in food and beverage manufacturing.

The competitive landscape remains moderately consolidated, with strong R&D investment in specialty pectin grades tailored for texture, stability, and mouthfeel. Partnerships between ingredient innovators and food manufacturers accelerated, bringing new reduced-sugar products to market with improved clean-label profiles. North America’s integrated supply chains and formulation expertise support continued demand for pectin in both traditional and emerging end uses. Focus on sustainable extraction technologies and ingredient traceability aligns with consumer and regulatory expectations, further strengthening regional leadership in functional and clean-label ingredients.

Europe Pectin Market Trends

Europe is expected to remain the leading yet innovation-driven market for pectin, with an estimated 35% share of global demand in 2026. Strong food safety and clean-label regulations support the use of natural additives in processed foods, beverages, and nutraceuticals, reinforcing pectin’s presence across multiple categories. Europe’s established citrus processing industry also ensures a dependable raw material base. The European Commission adopted updated food ingredient guidelines to streamline approval pathways for plant-derived emulsifiers and stabilizers, reinforcing natural hydrocolloid adoption in cross-border food supply chains and providing clearer regulatory certainty for pectin suppliers and users.

Market growth remains steady, supported by sustainable manufacturing programs and premium-experience product launches. The regional food manufacturers accelerated reformulation efforts that capitalized on pectin’s functional versatility, particularly in reduced-sugar spreads and plant-based yogurts, enabling stronger product differentiation. Government-led sustainability incentives and circular-economy mandates also promote the valorization of agri-waste streams, thereby contributing to raw-material efficiency and competitive positioning. These factors sustain demand for pectin as a natural, multi-functional ingredient throughout Europe.

Asia Pacific Pectin Market Trends

Asia Pacific is projected to be the fastest-growing regional market, with an anticipated 7.5% CAGR through 2033, driven by rapid expansion in food processing, pharmaceutical manufacturing, and contract formulation services. China, India, and Japan are key growth engines, buoyed by rising consumer demand for clean-label, reduced-sugar, and functional products. Japan’s Ministry of Agriculture, Forestry and Fisheries (MAFF) launched a targeted support program for functional food ingredient innovation, providing funding for pilot extraction technologies and supply chain modernization, broadening opportunities for plant-derived ingredients like pectin in both domestic and export markets.

Cost-competitive production and expanding agri-processing clusters further enhance the region’s strategic appeal. India’s Ministry of Food Processing Industries expanded its Agri-Infrastructure Fund to include support for value-added ingredient extraction facilities, enabling domestic pectin manufacturing capabilities and reducing import dependence. These policies strengthen the ecosystem for locally sourced functional ingredients while attracting global supplier investment. With rising domestic consumption and formulation innovation, these developments position the Asia Pacific as a central focus for pectin market growth through the forecast period.

Competitive Landscape

The global pectin market structure is moderately consolidated, with leading players such as Cargill, CP Kelco, DuPont Nutrition & Biosciences, Südzucker, and Ingredion controlling a significant share of global capacity and revenue. These companies leverage strong relationships with food and pharmaceutical manufacturers, integrated extraction and formulation capabilities, and extensive raw material sourcing networks. Heavy R&D investment supports specialty pectin grades for clean-label, low-sugar, and multi-functional applications, maintaining leadership across traditional and emerging end uses.

Regional and niche competitors, including Yantai Andre Pectin, Herbstreith & Fox, and Ceamsa, focus on localized supply and tailored technical solutions, retaining strongholds in domestic markets. Barriers such as raw material seasonality, regulatory compliance, and capital-intensive processing limit new entrants. Digitalization and process analytics are enabling manufacturers to optimize traceability, quality control, and supply chain efficiency. Market consolidation is expected to rise as leading companies pursue acquisitions and strategic partnerships to expand geographic reach and technology offerings.

Key Industry Developments

- In January 2026, CP Kelco began expanding pectin production at its Limeira, Brazil facility by about 30% to meet rising global demand for this natural food ingredient used in beverages, confectionery, and dairy products. The investment builds on previous capacity increases and strengthens the company’s ability to support customer growth across developed and emerging markets.

- In January 2026, USDA Agricultural Research Service (ARS) scientists developed a low-cost, high-quality pectin that can successfully gel in low-sugar food and drink products and is scalable for commercial production. This innovation uses a high-pressure processing (HPP) pre-treatment of orange peels to extract pectin with desirable structural properties for low-sugar applications.

- In September 2025, Pectin 360 secured a grant worth AU$ 2.1 million under the Cooperative Research Centres Projects (CRC-P) from the Australian Government to establish the country’s first onshore pectin and fiber production capability, reducing total reliance on imported supply. The funding will support a pilot-scale facility that converts fruit waste into high-quality pectin and fiber through a zero-waste process, enhancing food security and sustainable manufacturing.

Companies Covered in Pectin Market

- CP Kelco

- Cargill Incorporated

- DuPont Nutrition & Health

- Herbstreith & Fox KG

- Ingredion Incorporated

- Tate & Lyle PLC

- DSM-Firmenich

- Naturex

- Yantai Andre Pectin

- Ceamsa

- Silvateam

- Lucid Colloids

Frequently Asked Questions

The global pectin market is projected to reach US$ 1.2 billion in 2026.

Rising demand for clean-label and natural ingredients, expansion of low-sugar and functional food formulations, and increasing pharmaceutical and nutraceutical applications are key growth drivers.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

Expansion of food processing infrastructure in Asia Pacific and Latin America, government incentives for agri-processing and circular economy adoption, and innovation in low-sugar, fat-reduced, and functional formulations represent key opportunities.

Cargill, CP Kelco, DuPont Nutrition & Biosciences, Südzucker, Ingredion, Yantai Andre Pectin, Herbstreith & Fox, and Ceamsa are some of the leading players.