- Nutraceuticals & Functional Foods

- Fat Replacers Market

Fat Replacers Market Size, Share, and Growth Forecast 2026 - 2033

Fat Replacers Market by Source (Plant, Animal), by Nutrient Type (Carbohydrates, Proteins, Lipids, Others), by Form (Liquid, Powder), by Application (Processed Meat, Bakery & Confectionery, Beverages, Convenience Food), by Regional Analysis, 2026 - 2033

Fat Replacers Market Size and Trend Analysis

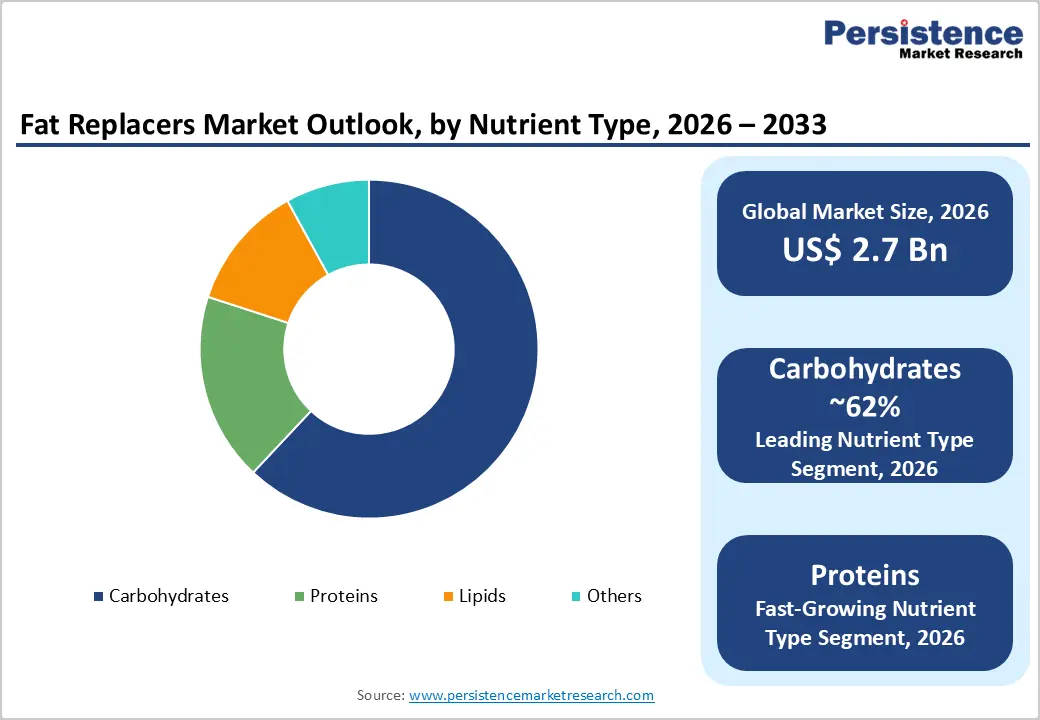

The global fat replacers market size is expected to be valued at US$ 2.7 billion in 2026 and projected to reach US$ 4.0 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

As consumers become more health-conscious, the demand for fat replacers is rising, driven by an increasing desire for healthier, low-fat alternatives in everyday foods. The shift indicates calorie reduction and the growing need for clean-label, natural ingredients.

Food companies are responding with innovative solutions such as plant-based and carbohydrate-based fat replacers that allow consumers to indulge without compromising their health. For example, Barcelona-based Cubiq Foods combines cellular culture technologies, microencapsulation of Omega-3 oils, and advanced oil/water emulsions to create healthier fat alternatives for the food industry. Its innovative approach positions the company as a leader in industrial-scale applications for alternative fats. One of their key products, Go!Drop, offers improved juiciness, full flavor, fewer calories, less saturated fat, and 20% less oil.

Such initiatives by food technology companies are anticipated to create exciting growth opportunities in the forthcoming years.

Key Market Highlights

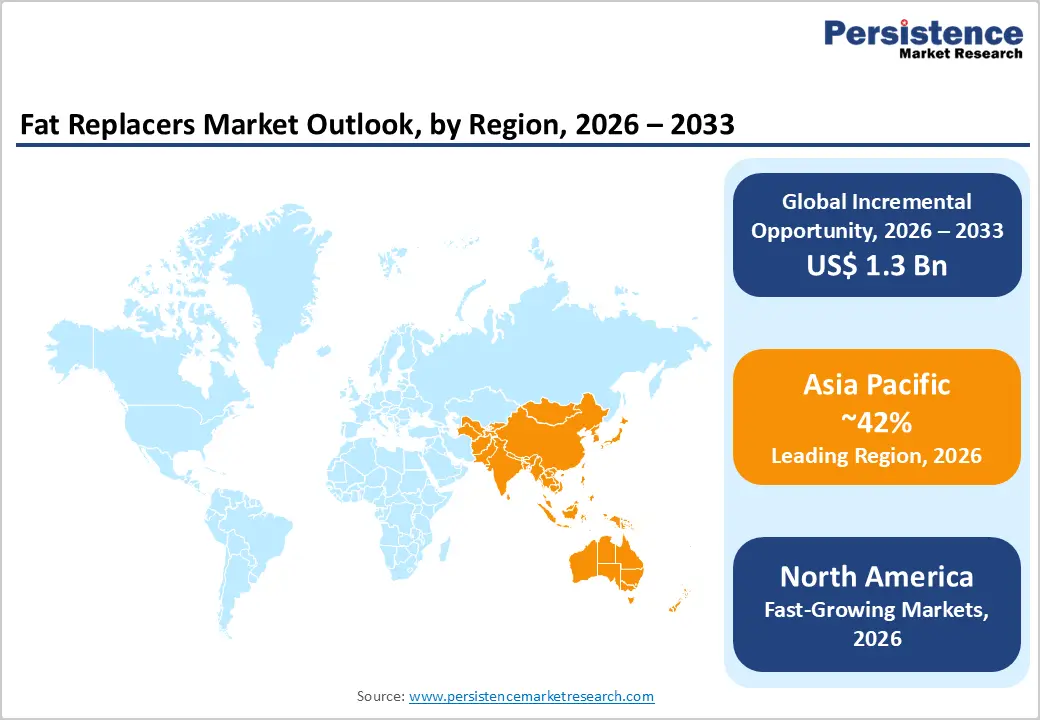

- Asia Pacific leads the fat replacers market, driven by large population, urbanization, and rising obesity in China, India, and ASEAN countries.

- North America is the fastest-growing region due to high obesity prevalence, strong nutrition regulations, and advanced innovation in fat replacer applications.

- Carbohydrate-based fat replacers dominate with about 62% share in 2025, offering bulk, viscosity, and creaminess across bakery, dairy, sauces, and spreads.

- Protein-based fat replacers are the fastest-growing segment, supported by rising demand for high-protein diets, sports nutrition, and fortified dairy and snack products.

- Key opportunities lie in developing integrated fat replacer systems for plant-based, high-protein, and affordable convenience foods across emerging Asia Pacific markets.

| Global Market Attributes | Key Insights |

|---|---|

| Fat Replacers Market Size (2026E) | US$ 2.7 billion |

| Market Value Forecast (2033F) | US$ 4.0 billion |

| Projected Growth CAGR (2026 - 2033) | 5.8% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers - Rising Global Obesity and Lifestyle-Related Diseases

Rising health concerns linked to high-fat diets such as obesity, cardiovascular diseases, stroke, and certain cancers are significantly driving the demand for healthier food alternatives. According to global estimates, more than half of the population is expected to fall into the overweight or obese category in the coming years, with a notable surge in childhood obesity rates. This growing awareness has led consumers to actively seek low-fat and reduced-calorie food options that do not compromise on taste or texture. As a result, food manufacturers are increasingly investing in advanced food technologies to develop innovative fat replacers derived from plant-based proteins, fibers, and carbohydrate-based ingredients, enabling healthier reformulations across various food products.

A key demand driver for the fat replacers market is the rapid increase in obesity and related noncommunicable diseases, prompting both consumers and regulatory bodies to prioritize healthier dietary patterns. According to the World Health Organization, approximately 2.5 billion adults were overweight in 2022, including around 890 million classified as obese, highlighting the scale of the issue. With obesity rates having more than tripled since 1975 and continuing to rise globally, especially in developed regions, the need for reduced-fat food formulations is intensifying. This trend is particularly evident in high-consumption categories such as bakery, dairy, processed meat, and beverages, where fat replacers help lower calorie content while maintaining product quality and consumer appeal.

Restraints - Limited Shelf Life of Certain Fat Replacers to Hinder Market Growth

Certain fat replacers, generally those derived from natural sources such as plant-based proteins or starches, have reduced oxidative stability and prone to microbial spoilage. This creates a problem with products without synthetic stabilizers or preservatives, where shelf-life is limited. For example, dairy alternatives such as oat or pea-based fat replacers require cold chain logistics, leading to high distribution costs and risk of spoilage. Development and production of new fat replacers with longer shelf life and improved stability is often an expensive affair, which include complying with regulatory standards of different regions. Such factors are, therefore, likely to pose a challenge.

Opportunities - Growth in Plant-Based and High-Protein Foods

A major opportunity for market participants lies in the intersection of fat reduction with plant-based and high-protein product innovation. Scientific literature highlights that carbohydrate and protein-based fat replacers from modified starches and inulin to microparticulated whey and plant proteins are being successfully deployed to improve texture and mouthfeel in reduced-fat meat analogues, dairy alternatives, and protein-enriched snacks. As global obesity concerns rise and consumers seek nutrient-dense products, there is strong demand for solutions that simultaneously reduce fat, contribute protein or fiber, and support claims such as "plant-based", "high protein", or "source of fiber". Ingredient innovators that can tailor multifunctional fat replacer systems for emerging categories like plant-based cheeses, hybrid meat products, and fortified beverages are well positioned to capture above-average growth over 2026 - 2033.

Category-wise Insights

Source Analysis

Within the Source category, plant-based fat replacers are expected to account for an estimated leading share of around 75% of the global market in 2026, significantly ahead of animal-derived systems. Carbohydrate and protein-based mimetics derived from plants such as starches, maltodextrins, inulin, and plant proteins are widely used in bakery, dairy, beverage, and meat analogues because they provide viscosity, creaminess, and bulk while fitting clean-label and vegetarian or vegan preferences. Scientific reviews emphasize that such carbohydrate-based replacers can form thermoreversible gels or micro-particulates that mimic fat globules, delivering favorable mouthfeel with lower energy density. By contrast, animal-derived fat replacers, including microparticulated whey or casein systems, play important roles in selected dairy and high-protein applications but face boundaries in markets prioritizing plant-based and lactose-free positioning, supporting the dominance and continued faster growth of plant-based sources.

Nutrient Type Analysis

In the Nutrient Type category, carbohydrate-based fat replacers are estimated to hold a dominant share of around 62% of the market in 2025, reflecting their versatility and cost-effectiveness across multiple food systems. Research shows that starch-based fat replacers and other complex carbohydrates can effectively reduce fat while maintaining viscosity, thickness, and a creamy mouthfeel in reduced-fat yogurts, bakery items, dressings, and spreads. They can also form microstructures that resemble fat droplets, further enhancing sensory attributes and enabling higher replacement levels compared with some protein or lipid systems. Protein-based fat replacers, although smaller in share, are the fastest-growing nutrient type segment due to their dual role in providing structure and contributing to protein-enrichment trends in dairy, snacks, and sports nutrition products.

Application Analysis

Across Application segments, bakery and confectionery products are expected to represent the largest share of the fat replacers market likely above 30% in 2025 as they are particularly sensitive to fat content in terms of texture, volume, and indulgence perception. Studies on fat substitutes in baked goods show that starch-based and protein-based mimetics can reduce saturated fat and total energy intake while maintaining crumb softness, moisture, and palatability, enabling manufacturers to meet emerging dietary guidelines without compromising consumer acceptance. Convenience foods, including ready meals, frozen snacks, and processed meat products, are expected to be among the fastest-growing application segments as urbanization and busy lifestyles drive higher consumption but also heightened concern about calorie density and cardiovascular risk. In these segments, fat replacers that survive thermal processing and freeze-thaw cycles while preserving juiciness and mouthfeel will see particularly strong uptake.

Regional Insights

North America Fat Replacers Market Trends and Insights

In North America, particularly the U.S., the fat replacers market benefits from high awareness of obesity-related health risks, a sophisticated regulatory framework, and a strong innovation ecosystem in food ingredients. The WHO and other epidemiological studies highlight that the Americas region exhibits some of the world’s highest obesity prevalence, with obesity levels continuing to rise over recent decades, which has intensified pressure on food manufacturers to reduce saturated fat and energy density across mainstream categories. The U.S. FDA has issued multiple guidance documents and regulations around trans fats, nutrition labeling, and health claims, prompting reformulation toward healthier fat profiles and encouraging adoption of advanced fat replacer systems that can meet both nutritional and labeling criteria.

Innovation in North America is driven by leading ingredient companies and research institutions that develop carbohydrate-, protein-, and lipid-based fat mimetics tailored to local preferences for clean-label, high-protein, and convenient foods. Players such as Tate & Lyle, Ingredion, and Cargill emphasize portfolios that reduce sugar, calories, and fat while enhancing texture and stability, and consumer trend data from Ingredion show that a growing share of North American shoppers carefully examine labels for fat, sugar, and ingredient lists. These factors position North America as the fastest-growing regional market for fat replacers, supported by strong demand in bakery, snacks, beverages, and plant-based meat alternatives.

Europe Fat Replacers Market Trends and Insights

In Europe, the fat replacers market is shaped by long-standing public-health initiatives, robust regulatory harmonization, and country-specific nutrition strategies in Germany, the U.K., France, Spain, and other EU member states. Epidemiological assessments indicate that nearly 60% of adults in the WHO European Region are overweight or obese, prompting continuous efforts to reduce saturated fats, sugar, and overall energy intake through product reformulation and front of pack labeling schemes. The European Food Safety Authority (EFSA) provides scientific opinions on food additives and substitutes, including fat replacers such as sucrose polyesters, shaping admissible use levels and reinforcing cautious use of synthetic fat substitutes while supporting broader adoption of carbohydrate and protein-based systems.

Consumer and retailer pressure in Europe has driven rapid growth of clean-label, organic, and plant-based foods, creating a favorable environment for plant-derived fat mimetics and fiber-based bulking agents in bakery, dairy, and meat substitute products. Countries such as Germany and the U.K. have seen strong innovation in reduced-fat bakery and savory snacks, while France and Spain are key markets for yogurts and dairy desserts using fat replacers to align with national nutrition plans. Harmonized EU rules on nutrition and health claims, combined with retailer-led reformulation programs, will continue to support steady growth in fat replacer adoption, albeit at a more mature pace than in rapidly developing regions.

Asia Pacific Fat Replacers Market Trends and Insights

Asia Pacific is projected to account for a 42% market share in 2025 and further dominate during the forecast period. The dominance of the region is attributed to supportive government initiatives, growing awareness regarding functional benefits of fat replacers in food applications, and rising cases of coronary heart diseases. As per studies, by 2050, coronary heart disease cases in Asia Pacific are anticipated to hit 729.5 million, doubling from 2025 figures. Consumers in this region are seeking low-fat and low-calorie food products which is anticipated to boost the demand for fat replacers during the forecast period.

China is the largest producer and consumer of food products globally. In 2024, China’s agri-food industry output surpassed US$ 1.8 trillion, fueled by significant domestic demand and supportive government policies for food security. China’s shift towards convenient, processed, and functional food is likely to fuel demand for healthier options such as low-fat, fortified, and plant-based products.

Competitive Landscape

The global fat replacers market is characterized by the presence of both established companies and innovative new entrants. To meet evolving consumer expectations, companies are investing heavily in research and development activities to introduce innovative fat substitute ingredients that closely replicate the texture and flavor of traditional fats, primarily using plant-based and protein-based alternatives. For instance, in March 2023, Shiru launched OleoPro, a plant-protein-based fat ingredient designed for alternative protein food products, boasting 90% less saturated fat.

Beyond innovation, companies are strengthening their market positions through strategic collaborations, partnerships, mergers, and acquisitions. These efforts aim to accelerate product development and expand technological capabilities to maintain their dominance during the forecast period.

Key Market Developments

- In February 2025, Ulrick & Short announced its partnership with Nordmann, a distributor of food ingredients, to improve distribution of clean label ingredients across Europe. The aim of the partnership is to offer consumers clean innovative products that meet current market demands.

- In October 2024, MicroLub, a deep-tech spinoff from the University of Leeds, announced that it has received a Euro 3.5 million seed investment led by Northern Gritstone. The new capital is likely to support tech scaling, team expansion, and product development.?

Companies Covered in Fat Replacers Market

- Cargill

- Archer Daniels Midland Company

- CP Kelco

- Fiberstar, Inc.

- FMC Corporation

- Ingredion

- Kerry Group

- Lonza Group

- Palsgaard

- Tate & Lyle

- Z Trim Holdings, Inc.

- Others

Frequently Asked Questions

The global fat replacers market is expected to reach around US$ 2.7 billion in 2026.

The market is driven by increasing demand for clean-labeled food products and technology innovation in food formulations.

The Asia Pacific region leads the global fat replacers market, accounting for an estimated 42% share of revenues in 2025.

Increasing focus on regulatory expertise and growing demand for functional food products are the key market opportunities.

Major players in the fat replacers industry include Cargill, FMC Corporation, ADM Company, Agritech Worldwide, Inc., and Kerry Group.