- Automotive Components & Materials

- Passenger Car Sensor Market

Passenger Car Sensor Market Size, Share, and Growth Forecast, 2025 - 2032

Passenger Car Sensor Market by Sensor Type (Temperature Sensors, Position Sensors, Pressure Sensors, NOx Sensors, Radar Sensors, Others), Application (Engine & Drivetrain, Safety & Security, Emission Control, Others), Sales Channel Type (OEM, Aftermarket), and Regional Analysis for 2025 - 2032

Passenger Car Sensor Market Size and Trends Analysis

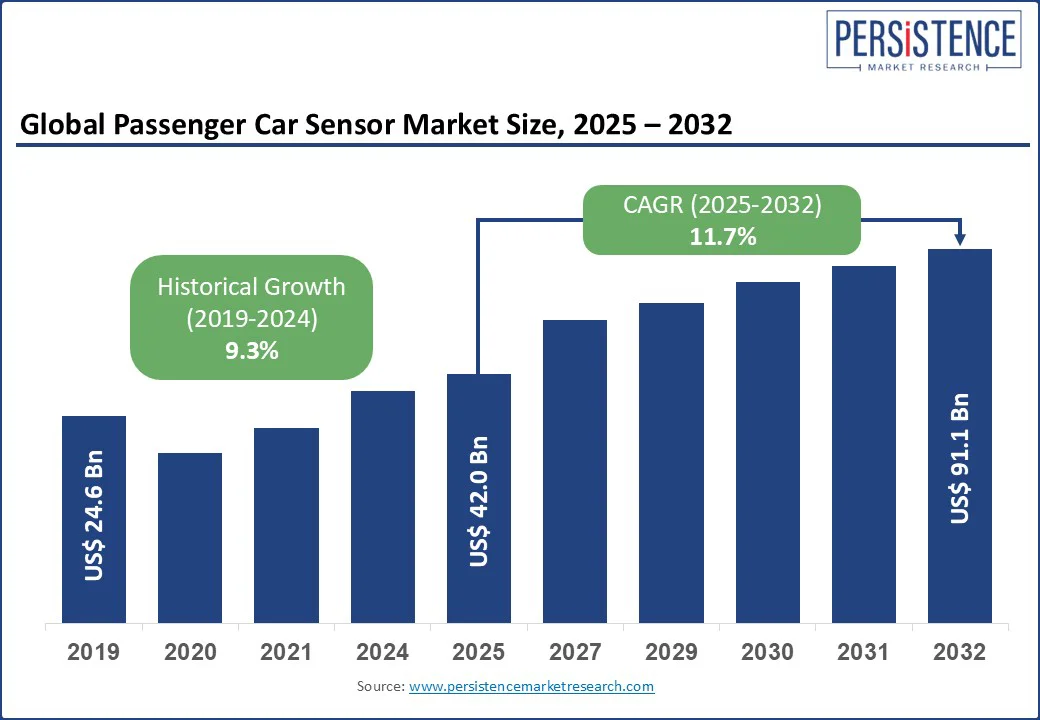

The global Passenger Car Sensor Market size is likely to value at US$ 42.0 Bn in 2025 and is expected to reach US$ 91.1 Bn by 2032, registering a CAGR of 11.7% during the forecast period 2025 - 2032.

The market has experienced robust growth, driven by the increasing adoption of advanced driver assistance systems (ADAS), rising demand for electric vehicles (EVs), and stringent safety and emission regulations.

Key Industry Highlights:

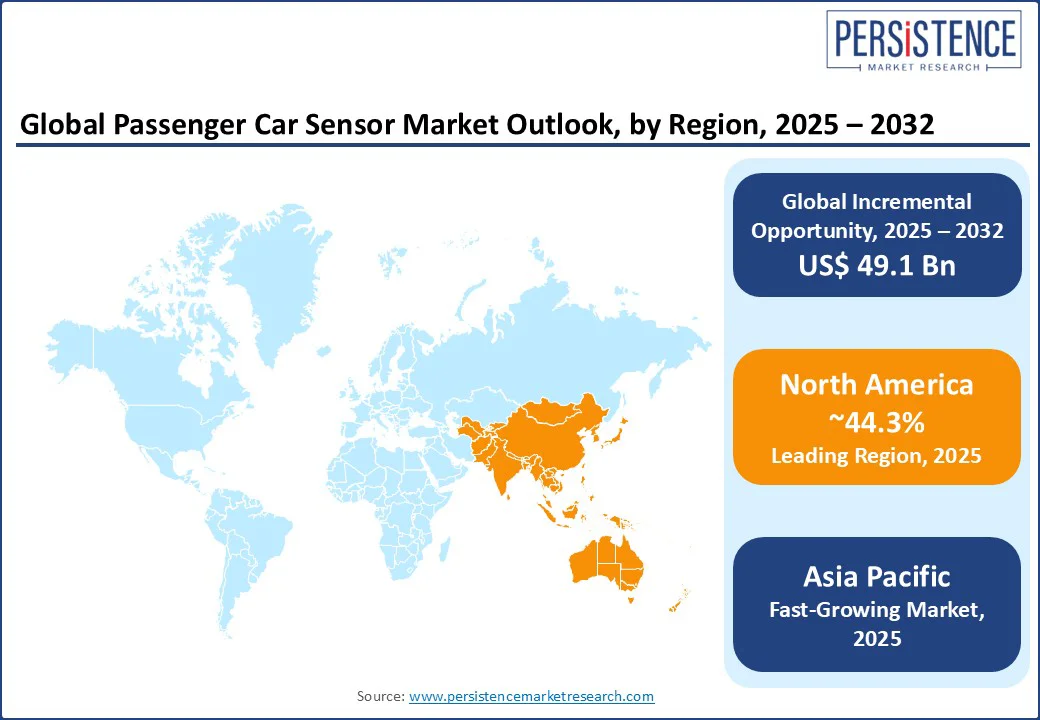

- Leading Region: Asia Pacific holds a 44.3% market share in 2025, supported by robust automotive manufacturing, high EV production, and rapid urbanization in countries like China and India.

- Fastest-growing Region: North America, driven by high adoption of ADAS, increasing EV sales, and strong regulatory focus on vehicle safety.

- Investment Trends: Europe is focusing on sustainable and connected sensor technologies, backed by regulatory frameworks like the EU’s General Safety Regulation and demand for emission control solutions.

- Dominant Sensor Type: Temperature sensors account for nearly 37.5% of the market share, driven by their critical role in engine management and EV battery monitoring.

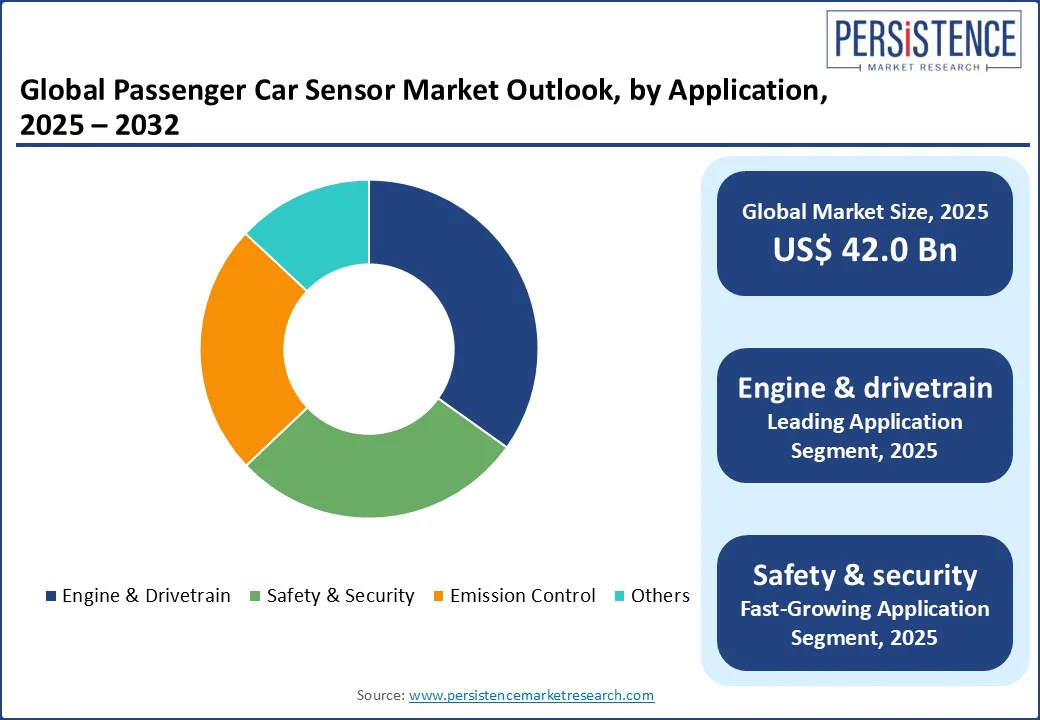

- Leading Application: Engine & drivetrain leads with a 34.8% share, reflecting high demand for sensors in powertrain optimization and efficiency.

- Consumer Trend: Radar and position sensors are gaining traction, driven by demand for ADAS features such as automatic emergency braking and lane-keeping assistance.

|

Global Market Attribute |

Key Insights |

|

Passenger Car Sensor Market Size (2025E) |

US$ 42.0 Bn |

|

Market Value Forecast (2032F) |

US$ 91.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

11.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.3% |

Market Dynamics

Driver- Rising ADAS Adoption and Electric Vehicle Growth Push Demand

The global rise in advanced driver assistance systems (ADAS) adoption is a key driver of the passenger car sensor market. Growing road safety concerns are prompting governments to mandate ADAS features in vehicles. According to the National Highway Traffic Safety Administration (NHTSA), these technologies have the potential to significantly reduce the number of road accidents, which in turn is boosting demand for radar and position sensors. In the United States, the increasing presence of ADAS-equipped vehicles highlights a clear shift in consumer preference toward safety-oriented innovations such as adaptive cruise control and automatic emergency braking. This trend underscores the broader move toward integrating advanced sensing technologies into passenger cars, driven by both regulatory measures and market demand for enhanced safety and driving comfort.

The rapid growth of electric vehicles (EVs) also fuels market expansion. EVs require advanced sensors for battery management, thermal regulation, and drivetrain efficiency. A 2023 study by the International Energy Agency (IEA) reported global EV sales reaching 14 million, a 35% increase from 2022, boosting demand for temperature and pressure sensors. In China, rapid growth in electric vehicle (EV) production is driving increased integration of sensors to enhance battery performance and efficiency.

Government regulations focused on emissions reduction and vehicle safety are further amplifying demand for advanced sensor technologies. Across the Asia Pacific, China’s New Energy Vehicle (NEV) mandate is a key policy promoting EV adoption, resulting in wider use of sensors for energy management and safety applications. In Europe, the EU’s General Safety Regulation is set to require the inclusion of ADAS features in all new vehicles, supporting the adoption of technologies such as NOx sensors and radar systems. These developments collectively reflect a global shift toward cleaner, safer, and more technologically advanced vehicles, with sensors playing a central role in enabling compliance, performance optimization, and enhanced driver assistance capabilities.

Restraint- High Costs and Supply Chain Disruptions Restrict Adoption

High costs of advanced sensors remain a major obstacle to the widespread growth of the passenger car sensor market, especially in emerging economies. Technologies such as radar and position sensors used in ADAS are relatively expensive, and their integration significantly increases overall vehicle production costs. This makes it challenging for manufacturers to introduce these features in price-sensitive markets, particularly in rural regions of India and parts of Latin America, where consumers often prioritize affordability over advanced safety or performance capabilities. As a result, manufacturers in these areas tend to focus on cost-effective alternatives that can deliver acceptable functionality at a lower price point.

In addition to cost concerns, supply chain constraints continue to create challenges for the market. The global semiconductor shortage in recent years disrupted automotive production, delaying the delivery of essential electronic components, including sensors. This has directly impacted the availability of advanced vehicle technologies.

For instance, according to the Ministry of Heavy Industries (India), under the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme, automakers have raised concerns that high costs of imported semiconductor-based sensors and related integration expenses make it challenging to equip budget EV models with advanced driver assistance features, particularly for rural and cost-sensitive markets.

Opportunity- Innovation in Autonomous Vehicles and Smart Sensors Boosts Consumption

The development of autonomous vehicles is creating substantial opportunities for the passenger car sensor market, as these vehicles require sophisticated sensor fusion technologies. The integration of radar and LiDAR for higher levels of autonomy is reshaping industry dynamics, enabling more precise navigation, obstacle detection, and safety. Companies can strategically benefit by focusing on cost-effective radar and position sensors tailored for mass-market vehicles, making advanced features accessible beyond premium segments.

Smart and connected sensors present another promising growth path. With the rise of IoT-enabled systems, these sensors facilitate real-time diagnostics and predictive maintenance, enhancing operational efficiency and vehicle reliability. In North America, several companies are exploring AI-driven position sensors that improve durability and lower maintenance requirements.

For instance, DriveOhio is an initiative by the Ohio Department of Transportation (ODOT) that serves as the state's centralized hub for smart vehicle projects, including autonomous and connected vehicles. It facilitates collaboration among policymakers, researchers, and technology providers and supports testing of vehicle-to-infrastructure communication systems.

Additionally, the increasing use of e-commerce for aftermarket sensor sales is expanding market reach. Digital platforms allow manufacturers to connect directly with specific customer groups, such as electric vehicle owners and fleet operators, using targeted marketing and B2B channels to drive adoption and strengthen market presence.

Category-wise Analysis

By Sensor Type

The passenger car sensor market is segmented into Temperature Sensors, Position Sensors, Pressure Sensors, NOx Sensors, Radar Sensors, and Others. Temperature sensors dominate, holding approximately 37.5% of the market share in 2025, due to their critical role in engine management and EV battery monitoring. Brands like Siemens have solidified their position with high-precision temperature sensors for hybrid and electric vehicles.

Radar sensors are the fastest-growing segment, fueled by increasing demand for ADAS features. Radar systems, such as those from Hitachi Energy, offer long-range detection, making them essential for safety features like adaptive cruise control and collision avoidance.

By Application Type

By application, the market is divided into Engine & Drivetrain, Safety & Security, Emission Control, and Others. Engine & drivetrain leads, accounting for 34.8% of the market share in 2025, driven by demand for sensors in powertrain optimization and fuel efficiency. Temperature and pressure sensors are critical for hybrid and EV drivetrains.

Safety & security is the fastest-growing segment, fueled by regulatory mandates and ADAS adoption. Position and radar sensors are gaining traction for features like lane-keeping assistance and automatic emergency braking, particularly in North America and Europe.

By Sales Channel Type

The market is segmented into OEM and Aftermarket. OEM leads with a 70% share in 2025, reflecting the integration of sensors in new vehicles. Major automakers like Toyota and Volkswagen prefer OEM sensors for reliability and compatibility.

Aftermarket is the fastest-growing segment, driven by vehicle maintenance and upgrades. E-commerce platforms have boosted aftermarket sales for NOx and pressure sensors, particularly for older vehicles requiring emission compliance.

Regional Insights

North America Passenger Car Sensor Market Trends

In North America, the U.S. stands out as the fastest-growing market for passenger car sensors, fueled by expanding electric vehicle adoption and stringent safety regulations. Demand for temperature and radar sensors is rising alongside the integration of advanced driver-assistance systems (ADAS), enhancing capabilities such as lane-keeping and collision prevention.

Consumer preferences increasingly favor connected and smart sensors, with major brands adopting IoT-enabled technologies to improve performance, diagnostics, and predictive maintenance. Regulatory mandates from the National Highway Traffic Safety Administration, coupled with substantial infrastructure investments and government incentives for EV adoption, are further accelerating the growth and technological advancement of the U.S. market.

Europe Passenger Car Sensor Market Trends

Europe’s passenger car sensor market is dominated by Germany, the U.K., and France, driven by stringent emission regulations and the rapid expansion of electric vehicles. Germany remains a key hub, supported by strong manufacturing capabilities and the presence of global players such as Siemens and ABB, with a focus on advanced radar and emission-control sensors.

The EU’s General Safety Regulation is boosting the adoption of NOx and radar sensors, enhancing safety and environmental compliance. In the U.K., rising demand for ADAS technologies, particularly radar-based safety systems, drives market momentum. France shows notable growth in drivetrain sensors for EVs, aided by companies like Schneider Electric, with regulatory initiatives promoting sustainable automotive innovations across the region.

Asia Pacific Passenger Car Sensor Market Trends

Asia Pacific dominates with a 44.3% market share in 2025, led by China, India, and Japan. In India, supportive government policies for electric vehicles and programs like Bharat NCAP are fueling demand for advanced temperature and safety sensors, with companies such as Hitachi Energy playing a leading role. Initiatives like the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme encourage wider EV adoption, boosting sensor requirements across vehicle segments.

In China, large-scale EV production drives demand for radar and position sensors, with major players like KEPCO catering to autonomous vehicle technologies. Japan emphasizes high-precision sensors for safety and emission control, where companies like Denso are expanding their presence. Across the region, rapid urbanization and the rise of digital procurement platforms further accelerate market growth.

Competitive Landscape

The passenger car sensor market is highly competitive, with global players vying for market share through innovation, partnerships, and acquisitions. The rise of ADAS and EV technologies intensifies competition, as companies focus on developing high-precision, cost-effective sensors. Strategic collaborations and R&D investments are key differentiators in this dynamic market.

Key Developments

- In Jul 2025, Siemens Digital Industry Software and AnteMotion formed a strategic partnership to redefine sensor simulation for ADAS and autonomous vehicle development. This collaboration enables the integration of Siemens’ high-fidelity, physics-based sensor models originating from the Simcenter Prescan environment directly into AnteMotion’s real-time, Unreal Engine-based rendering platform, Midgard.

- In May 2024, Samsung Electronics Co. and KEPCPO signed a memorandum of understanding (MOU), which calls for the companies to share technologies for diagnosing and assessing power facilities. AI-based power facility condition assessment and operations are expected to be shared by both businesses.

Companies Covered in Passenger Car Sensor Market

- Power Grid Corporation of India Limited (POWERGRID)

- MYR Group Inc.

- KEPCO

- Hitachi Energy Ltd.

- Siemens

- General Electric Company

- Cisco Systems Inc.

- Schneider Electric SE

- ABB

- Eaton

- Others

Frequently Asked Questions

The market is projected to reach US$ 42.0 Bn in 2025.

Rising ADAS adoption, electric vehicle growth, and stringent safety regulations are the key market drivers.

The market is poised to witness a CAGR of 11.7% from 2025 to 2032.

Innovation in autonomous vehicle sensors and smart, connected sensors are the key market opportunities.

Siemens, Hitachi Energy, and ABB are among the key market players.