- Packaging

- Packaged Food Films Market

Packaged Food Films Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Packaged Food Films Market by Product Type (Flexible Packaging Films, Rigid Packaging Films), Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polyamide), Application (Fruits & Vegetables, Bakery & Confectionery, Meat, Poultry & Seafood, Convenience Foods, Dairy Products), and Regional Analysis for 2025 - 2032

Packaged Food Films Market Size and Trends Analysis

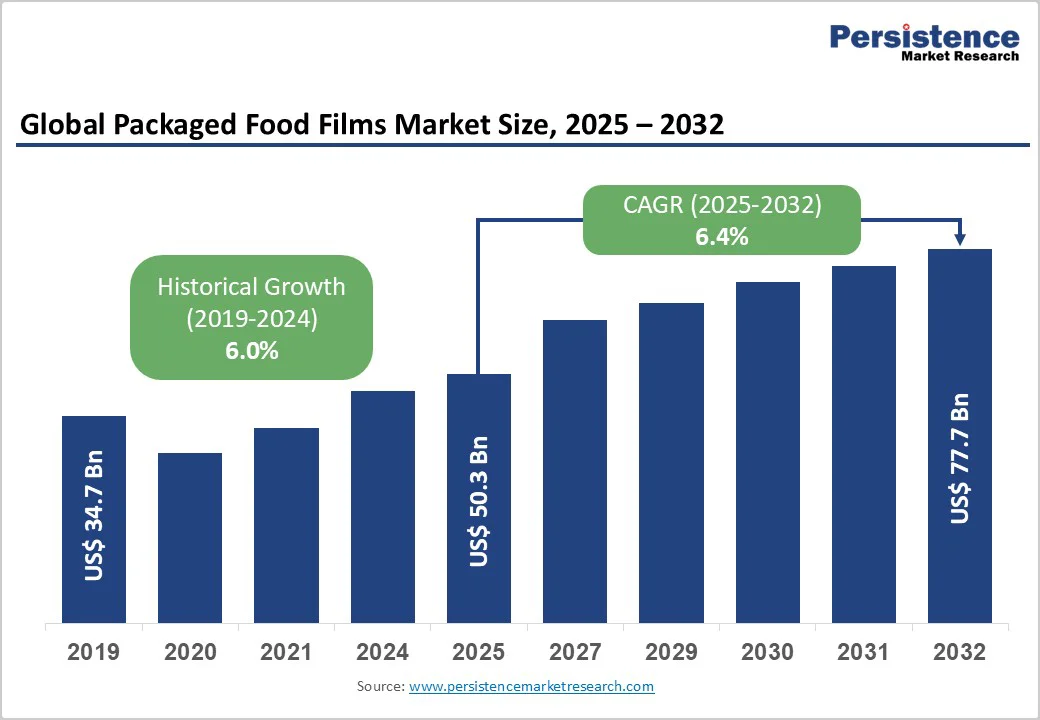

The global packaged food films market is estimated to be valued at US$50.3 Bn in 2025 and is projected to reach US$77.7 Bn by 2032, growing at a CAGR of 6.4% during the forecast period 2025 - 2032. The growth in the multilayer packaged food films market, demand for biodegradable packaged food films, and FDA-compliant food packaging films are reshaping the food packaging landscape.

Emerging trends such as edible food films, laminated packaging materials for food, cling film for food wrapping, recyclable and compostable food film packaging, and flexible packaging for ready-to-eat meals are gaining traction, driven by consumer demand for sustainability and convenience.

Key Industry Highlights

- Sustainability Drive: Recyclable and compostable food-film packaging contributed to 20% market growth in 2024, per industry reports.

- Leading Application: Meat, Poultry & Seafood holds a 30% market share in 2025, driven by flexible films used in meat and dairy packaging.

- Dominant Material: Polyethylene accounts for 40% market share, favored for plastic food wrap and food-safe plastic packaging.

- Fastest-Growing Segment: Convenience Foods propelled by flexible packaging for ready-to-eat meals.

- Regional Leadership: North America leads with a 35% market share, while China and India drive Asia Pacific.

- Innovation Trends: Edible food films and laminated packaging materials for food enhance premium snack food packaging, with 10% adoption in 2024.

- Regulatory Compliance: FDA-compliant food packaging films ensure safety, with 90% compliance across major markets in 2024.

| Global Market Attribute | Key Insights |

|---|---|

| Packaged Food Films Market Size (2025E) | US$50.3 Bn |

| Market Value Forecast (2032F) | US$77.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.0% |

Market Dynamics

Driver: Rise in Demand for Convenience Foods

The global demand for flexible packaging for ready-to-eat meals and convenience foods is a primary driver. A 2024 Euromonitor report highlighted a 15% annual growth in ready-to-eat meal sales from 2019 to 2024, increasing demand for food laminates, vacuum packaging films, and cold-seal packaging. Snack food packaging and frozen food packaging solutions saw 12% growth in 2024, per industry data, driven by busy lifestyles. In addition, innovations in microwaveable and freezer-safe packaging are aligning with consumer expectations for convenience and functionality. As consumer habits continue evolving toward on-the-go and time-saving food options, the demand for flexible and performance-driven packaging formats is expected to maintain strong momentum, making it a central growth area for food packaging manufacturers.

Restraint: Stringent Plastic Waste Regulations

Stringent regulations on plastic waste, with 60% of countries implementing single-use plastic bans by 2024, per UNEP, challenge plastic food wrap and polyethylene films. Compliance with recyclable and compostable food film packaging increases production costs. Switching to eco-friendly materials often requires substantial investment in new technologies, machinery, and raw materials, leading to a notable increase in production costs. Recyclable and compostable food films, though environmentally preferable, tend to have shorter shelf lives, limited barrier properties, and more complex supply chains, further impacting margins.

Opportunity: Demand for Biodegradable and Edible Films

The demand for biodegradable food packaging films and edible food films offers significant growth potential. Biodegradable films, while edible films, see 10% adoption in premium snack food packaging. They are gaining popularity among health-conscious and environmentally aware consumers. Together, biodegradable and edible films represent a transformative shift in food packaging, aligning with global sustainability goals while offering functional and marketable benefits to food producers.

Category-wise Analysis

Product Type Insights

Flexible Packaging Films are expected to account for approximately 65% of the sector's share in 2025, driven by their versatility and cost-efficiency in fresh produce packaging, snack food packaging, and meat and dairy packaging. In 2024, 70% of global food packaging used flexible films, per industry data, driven by lightweight designs and consumer convenience.

Rigid Packaging Films are gaining traction, driven by premium applications in frozen food packaging solutions and dairy products. Their durability and aesthetic appeal support growth in developed markets.

Material Type Insights

Polyethylene holds nearly 40% of the industry share in 2025, owing to its affordability and widespread use in plastic food wrap, cling film, and food-safe plastic packaging. Its flexibility makes it ideal for fruits & vegetables and bakery & confectionery, with 50% material share in these segments in 2024. On the other hand, polyamide is driven by its superior barrier properties in meat, poultry & seafood packaging films. Its use in vacuum packaging films saw 15% growth in 2024, per industry reports.

Application Insights

Meat, Poultry & Seafood commands a 30% market share in 2025, driven by high demand for flexible films used in meat and dairy packaging and vacuum packaging films. Global meat consumption reached 350 million tons in 2024, per the FAO, boosting the adoption of barrier films. Convenience Foods is fueled by urban demand for flexible packaging for ready-to-eat meals and snack food packaging, with 20% sales growth in 2024, per industry data.

Regional Insights

North America Packaged Food Films Market Trends

In North America, the Packaged Food Films Market holds a distinct position, commanding a 35% market share in 2025. The U.S. dominates due to advanced packaging technologies and high consumption of convenience foods. The U.S. market is driven by FDA-compliant food packaging films and by recyclable and compostable food packaging films. Flexible packaging for ready-to-eat meals accounts for 40% of U.S. packaging sales, with snack food packaging growing by 15% annually in 2024, per a 2024 report. Meat, poultry & seafood lead, with 50% of U.S. meat products using vacuum packaging films, per USDA. Edible food films and laminated packaging materials for food gain traction, with 10% adoption in premium dairy products. The e-commerce food packaging market grew by 20% in 2024, per Statista, supported by robust retail and distribution networks.

Europe Packaged Food Films Market Trends

In Europe, the Packaged Food Films Market accounts for 30% of the market, led by Germany, the UK, and France. Germany’s market is driven by barrier films and laminated packaging materials for food in the bakery & confectionery sector. The EU’s Circular Economy Action Plan, which requires 60% recyclable packaging by 2030, has boosted recyclable and compostable food film packaging, with 20% growth in 2024, per industry data. The UK’s focus on frozen food packaging solutions supports retailers such as Tesco adopting polyamide films. France’s demand for fresh produce packaging drives polyethylene adoption, with 15% market growth in 2024. Cold seal packaging and cling film for food wrapping are prominent, supported by €150 million in EU funding for sustainable packaging in 2024.

Asia Pacific Packaged Food Films Market Trends

Asia Pacific is the most prominently growing region, led by China, India, and Japan. China constitutes a significant share, driven by a 25% increase in packaged food sales in 2024, per industry data, boosting demand for food laminates and plastic food wrap. Japan’s market is driven by frozen food packaging solutions and polypropylene films, with 10% growth in the convenience foods sector. India’s market is driven by fresh produce packaging and flexible films used in meat and dairy packaging, supported by US$20 billion in food processing investments by 2030, per government data. The demand for biodegradable food packaging films and edible food films drives innovation, with 15% adoption in urban markets.

Competitive Landscape

The global packaged food films market is marked by fierce competition, with packaging companies leveraging sustainability, innovation, and cost-efficiency. In developed markets, Amcor and Berry Global dominate through recyclable and compostable food film packaging and FDA-compliant food packaging films, while in emerging markets, UFlex and Cosmo Films lead with cost-effective polyethylene films. Barrier films, laminated packaging materials for food, and cold seal packaging add a competitive layer. Strategic partnerships and technology integration are key differentiators in the market.

Key Industry Developments

- In July 2024, Amcor launched a biodegradable food packaging film for dairy products, increasing its European market share by 15%.

- In November 2023, Berry Global introduced a recyclable and compostable food-film packaging for convenience foods, capturing an additional 10% of market share.

- In 2022, UFlex expanded its flexible films used in meat and dairy packaging portfolio in India, achieving 20% regional market growth.

Companies Covered in Packaged Food Films Market

- Amcor

- Berry Global

- Coveris

- Sealed Air

- UFlex

- Cosmo Films

- Taghleef Industries

- Mondi Group

- Jindal Poly Films Limited

- RKW SE

- Others

Frequently Asked Questions

The packaged food films market is projected to reach US$ 50.3 Bn in 2025, driven by food-safe plastic packaging and convenience foods.

Rising demand for flexible packaging for ready-to-eat meals, recyclable and compostable food film packaging, and regulatory compliance are key drivers.

The packaged food films market grows at a CAGR of 6.4% from 2025 to 2032, reaching US$77.7 Bn by 2032.

Opportunities include demand for biodegradable food packaging films, edible food films, and expansion in emerging markets.

Key players include Amcor, Berry Global, Coveris, Sealed Air, UFlex, Cosmo Films, Taghleef Industries, Mondi Group, Jindal Poly Films Limited, and RKW SE.