- Medical Devices

- Orthodontic Supplies Market

Orthodontic Supplies Market Size, Share, and Growth Forecast 2026 - 2033

Orthodontic Supplies Market by Product (Brackets, Archwires, Aligners, Bands & Buccal Tubes, Ligatures, Adhesives, Others), Age Group (Children, Teenagers, Adults), End-user (Dental Clinics, Hospitals, Orthodontic Clinics, Dental Laboratories), by Regional Analysis, 2026- 2033

Orthodontic Supplies Market Share and Trends Analysis

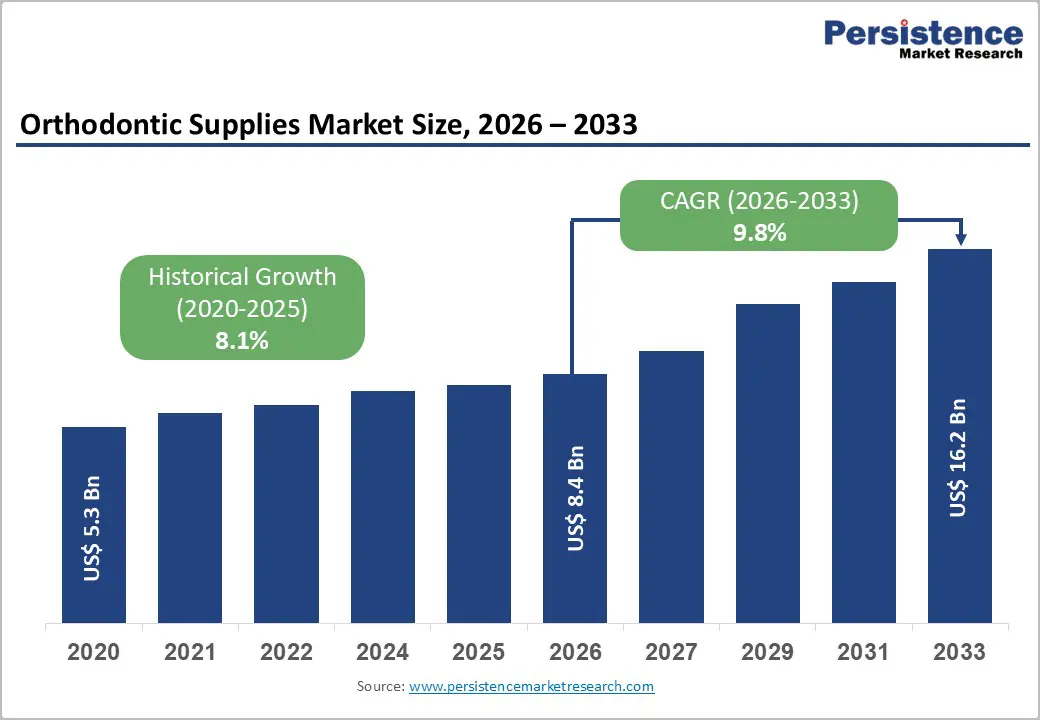

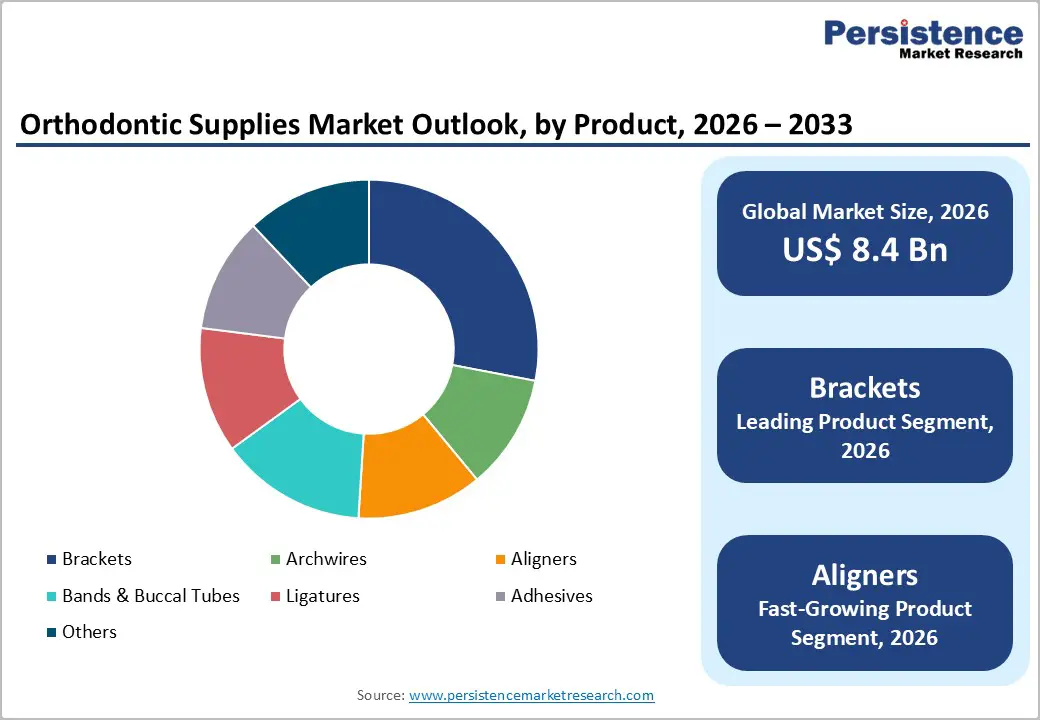

The global orthodontic supplies market size is expected to be valued at US$ 8.4 billion in 2026 and projected to reach US$ 16.2 billion by 2033, growing at a CAGR of 9.8% between 2026 and 2033.

It is witnessing steady growth due to the increasing prevalence of dental malocclusion, rising awareness of oral aesthetics, and growing demand for corrective dental treatments. The market includes products such as brackets, archwires, aligners, ligatures, and adhesives used in fixed and removable orthodontic procedures. Demand for clear aligners and minimally visible treatment options is rapidly increasing among both teenagers and adults. Technological advancements in digital dentistry, including 3D printing and CAD/CAM systems, are improving treatment precision and efficiency. In addition, expanding dental healthcare infrastructure and increasing access to orthodontic care in emerging economies are supporting long-term market expansion globally.

Key Industry Highlights:

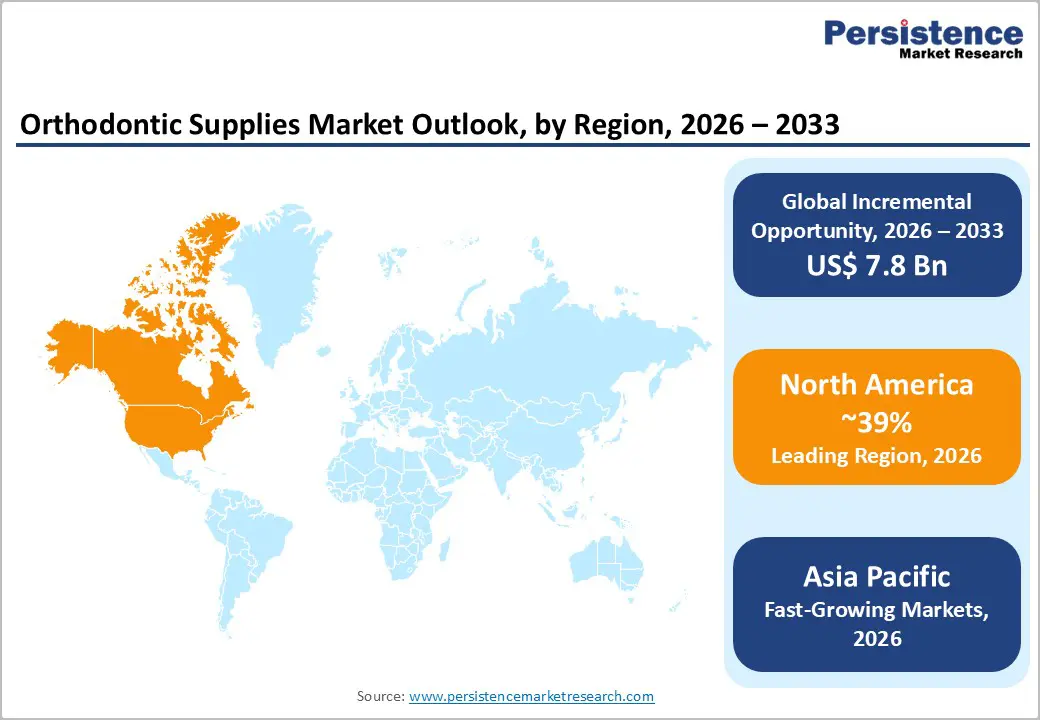

- Leading Region – North America holds approximately 39% of global orthodontic supplies revenues in 2025, anchored by the world's largest clear aligner market, high adult treatment uptake, strong AAO-supported orthodontic practice infrastructure, and headquarters of leading innovators Align Technology and Dentsply Sirona.

- Fastest Growing Region – Asia Pacific is the fastest-growing orthodontic supplies market through 2033, driven by China's domestic aligner industry, India's expanding dental clinic network, growing aesthetic dental awareness across ASEAN, and government oral health initiatives supporting malocclusion treatment access.

- Dominant Segment – Brackets lead the product category with approximately 28% market share in 2025, sustained by the clinical necessity of fixed appliances for complex malocclusion cases and continued premium pricing of self-ligating systems such as Damon (Ormco) and SmartClip (3M).

- Fastest Growing Segment – Clear aligners are the fastest-growing orthodontic product through 2033, propelled by Invisalign's 17+ million global case milestone, competitive entry from SureSmile, Spark, and regional brands, and surging adult patient demand for aesthetic, discreet orthodontic treatment worldwide.

Market Dynamics

Drivers – Surge in Adult Orthodontic Treatment Uptake Expanding the Addressable Market

Historically concentrated in the adolescent demographic, orthodontic treatment is experiencing rapid uptake among adults, a structural shift that is significantly expanding the addressable patient population. The American Association of Orthodontists (AAO) reported that adults now represent approximately one in three orthodontic patients in the United States, a share that has grown consistently over the past decade. This trend is primarily driven by the proliferation of aesthetic treatment options, particularly clear aligners that minimize visible appliances.

According to the British Orthodontic Society (BOS), adult patient inquiries for clear aligner treatment increased by over 30% between 2019 and 2023 in the UK. The growing working-age population's investment in professional appearance, supported by higher disposable incomes in high-income markets is sustaining this multi-decade trend and delivering premium revenue growth to orthodontic supply manufacturers.

Digital Orthodontics and 3D Printing: Transforming the Clinical Workflow

The digitalization of orthodontic practice, encompassing intraoral scanning, AI-powered treatment planning, and 3D-printed appliances, is creating a powerful demand multiplier for advanced orthodontic supplies. The adoption of intraoral digital scanners has grown exponentially, with the Journal of Clinical Orthodontics estimating that over 60% of U.S. orthodontic practices now use digital impressions as a primary workflow tool.

Digital workflows accelerate treatment planning, improve precision for bracket placement and aligner fabrication, and reduce chairside time, incentivizing practices to upgrade their appliance portfolios. Align Technology's iTero scanner ecosystem and Dentsply Sirona's Orthodontic Studio platform exemplify how technology integration is driving consumable pull-through, enabling manufacturers to capture recurring revenue across both hardware and supplies.

Restraints - High Treatment Costs and Limited Insurance Coverage Suppress Treatment Rates

Orthodontic treatment remains one of the most out-of-pocket healthcare expenditures for families globally. In the United States, comprehensive orthodontic treatment costs range from US$ 3,000 to US$ 10,000 per case, with premium clear aligner treatments often at the higher end. The American Dental Association (ADA) notes that orthodontic coverage is excluded from many dental insurance plans or subject to lifetime caps that cover only a fraction of treatment costs. In emerging markets, the absence of structured dental insurance compounds affordability constraints, suppressing treatment penetration rates and moderating market growth below demographic and need-based potential.

Shortage of Trained Orthodontic Specialists Constraining Service Delivery Capacity

A structural shortage of trained orthodontic specialists in many geographies limits the capacity of the market to deliver treatments at scale. The AAO estimates that there are approximately 11,000 practicing orthodontists in the United States serving a population of over 330 million. In low- and middle-income countries, the ratio is far more constrained. This specialist scarcity creates bottlenecks in treatment access, particularly in rural and peri-urban areas, limiting the volume of orthodontic supplies consumed and moderating overall market penetration rates despite high unmet demand.

Opportunities - Clear Aligners: The Fastest-Growing Product Category Redefining Market Economics

Clear aligners represent the single largest growth opportunity in the orthodontic supplies market, driven by patient preference for invisible treatment, shorter chair time per visit, and premium pricing power for manufacturers. Align Technology's Invisalign system, with over 17 million patients treated globally as of 2023 has validated the mass-market potential of aligner therapy. Competitive entry from Dentsply Sirona (SureSmile), Envista (Spark Aligners), and multiple direct-to-consumer and lab-fabricated aligner brands is broadening access and driving volume growth.

According to the AAO, aligner-only practices are one of the fastest-growing orthodontic practice models in the U.S. The global expansion of aligner manufacturing capacity and growing adoption in the Asia Pacific and Latin America markets position this segment for the highest CAGR among all orthodontic product types through 2033.

Untapped Demand in Asia Pacific and Emerging Markets Offering Scale Opportunity

Asia Pacific and particularly China, India, and Southeast Asia represent a structural growth opportunity of immense scale for orthodontic supply manufacturers. The WHO estimates that malocclusion affects approximately 56% of children globally, with a significant proportion in developing countries remaining untreated due to limited access and awareness. In China, the National Health Commission (NHC) has prioritized oral health in its national health plans, and domestic clear aligner companies—including Angelalign have emerged as significant regional players. Rapid urbanization, rising disposable incomes, and growing aesthetic consciousness among millennials and Gen Z populations across Southeast Asia are building a large, first-generation orthodontic treatment cohort that represents a multi-decade commercial opportunity for both international and domestic supply brands.

Category-wise Analysis

Product Insights

Brackets remain the leading product segment in the orthodontic supplies market, capturing approximately 28% of global revenues in 2026. Metal and ceramic brackets continue to form the backbone of traditional fixed appliance orthodontics, which, despite the aligner revolution, remains the preferred treatment modality for complex malocclusions, severe crowding, and skeletal discrepancies requiring comprehensive tooth movement. The Journal of Clinical Orthodontics annual practice survey consistently identifies fixed appliances as the dominant treatment modality in use among orthodontists globally. Self-ligating bracket systems such as Damon (Ormco Corporation) and SmartClip (3M) command premium pricing and continued clinician loyalty, reinforcing the bracket segment's revenue leadership despite the rapid rise of clear aligner alternatives.

Age Group Analysis

Teenagers represent the leading age group segment in the orthodontic supplies market, accounting for approximately 45% of global revenues in 2026. The adolescent demographic has historically been and remains the core orthodontic patient cohort, as the teenage years represent the optimal window for orthodontic intervention during active jaw development and tooth eruption. School-based dental screening programs in countries including the United States, Germany, and Japan systematically identify and refer teenagers for orthodontic evaluation. The AAO recommends an orthodontic evaluation by age seven, with treatment typically commencing between ages 11 and 15. Both traditional bracket systems and teen-specific aligner products, such as Invisalign Teen, are purpose-designed for this segment, sustaining its commercial dominance.

End-user Insights

Orthodontic clinics represent the leading end-user segment in the orthodontic supplies market, accounting for approximately 52% of global revenues in 2025. Dedicated orthodontic practices staffed by specialist orthodontists consume the highest volumes of precision supplies, including self-ligating brackets, premium archwires, clear aligners, and digital workflow tools, commanding premium pricing relative to general dental clinics. The AAO reports over 10,000 member orthodontic practices in the United States alone, each consuming an extensive inventory of consumables per patient case. The rise of orthodontic group practices and DSOs (Dental Service Organizations) consolidating specialty orthodontic clinics is further concentrating purchasing power and driving volume-based procurement agreements with major orthodontic supply manufacturers.

Regional Insights

North America Orthodontic Supplies Market Trends and Insights

North America leads the global orthodontic supplies market with approximately 39% revenue share in 2025, driven by high orthodontic treatment penetration rates, strong consumer awareness of aesthetics, widespread clear aligner adoption, and a mature dental insurance infrastructure that partially offsets treatment costs. The region is the global innovation hub for digital orthodontics, with leading companies such as Align Technology and Dentsply Sirona headquartered in the U.S.

U.S. Orthodontic Supplies Market Size

The United States accounts for approximately 82% of North American orthodontic supply revenues in 2026, supported by over 4 million Americans beginning orthodontic treatment annually per AAO estimates. Strong Invisalign penetration, growing adult patient volumes, and the expansion of DSO-affiliated orthodontic networks collectively sustain the U.S. market's position as the world's single largest national orthodontic supply market.

Europe Orthodontic Supplies Market Trends and Insights

Europe is the second-largest orthodontic supplies market, with Germany, the U.K., and France as the primary revenue contributors. The region benefits from comprehensive dental education infrastructure, high orthodontist density in Western Europe, and growing consumer adoption of clear aligners. Regulatory harmonization under EU MDR 2017/745 is reshaping product registration for orthodontic devices across member states.

Germany Orthodontic Supplies Market Size

Germany is the largest European orthodontic supplies market, contributing approximately 21% of regional revenues in 2026. Germany's statutory health insurance (GKV) provides partial orthodontic coverage for children and teenagers with severe malocclusions, driving high treatment volumes. Home to Dentaurum GmbH & Co. KG and DB Orthodontics, Germany has a strong domestic manufacturing heritage in brackets and archwires.

UK Orthodontic Supplies Market Size

UK represents approximately 14% of European orthodontic revenues in 2026. The NHS provides orthodontic treatment for children with clinical need, creating a substantial publicly funded demand base. Private orthodontic treatment particularly clear aligners is growing rapidly, with the British Orthodontic Society (BOS) reporting consistent growth in adult private patient enquiries, driven by aesthetic treatment preference.

France Orthodontic Supplies Market Size

France accounts for approximately 11% of European orthodontic supply revenues in 2025. The French social security system (Assurance Maladie) provides reimbursement for orthodontic treatment in children, supporting high treatment initiation rates. Growing private-pay adult aligner market demand and increasing adoption of digital orthodontic workflows by French orthodontists are driving above-average growth in premium supply categories.

Asia Pacific Orthodontic Supplies Market Trends and Insights

Asia Pacific is the fast-growing orthodontic supplies market, with China as the dominant and most dynamic country, where domestic aligner brands such as Angelalign are rapidly scaling alongside international players. Rising disposable incomes, growing aesthetic dental awareness, and expanding orthodontist training programs across the region are the primary demand drivers. Governments in Japan, South Korea, and China are investing in oral health infrastructure, supporting market expansion.

India Orthodontic Supplies Market Size

India's orthodontic supplies market is valued at approximately US$ 180 million in 2025 and is growing rapidly, driven by a large adolescent population, rising dental health awareness, and expanding private dental clinic networks. Government initiatives such as the National Oral Health Programme (NOHP) are improving awareness of dental conditions, including malocclusion, and building a pipeline of future orthodontic treatment demand.

Competitive Landscape

The orthodontic supplies market is highly competitive and driven by continuous advancements in digital dentistry, aesthetic orthodontic treatments, and customized treatment solutions. Companies are focusing on expanding clear aligner offerings, improving bracket technologies, and introducing patient-friendly orthodontic products to strengthen their market position. Increasing adoption of CAD/CAM technology, 3D printing, and AI-based treatment planning is further intensifying competition across the industry. Market participants are also emphasizing strategic collaborations, product launches, and regional expansion to increase customer reach.

Key Developments:

- In January 2026, Cx Orthodontic Supply launched the reusable Cx Precoat Box, a streamlined orthodontic bracket storage system designed to improve clinical efficiency and reduce chair time. The product was developed to help orthodontic assistants preload brackets with adhesive during downtime, enabling faster bracket placement during patient appointments.

- In April 2026, LightForce Orthodontics launched LightBracket Metal, a patient-specific 3D-printed metal bracket system designed for orthodontic patients choosing metal braces. The company introduced the product to expand personalized digital orthodontic treatment beyond ceramic brackets and improve treatment precision, patient comfort, and workflow efficiency.

- In March 2026, Carestream Dental launched the CS 1300 Intraoral Camera, designed to deliver high-definition imaging and improve clinical workflow integration. The device featured enhanced optics, a wide focal range, LED illumination, and direct integration with CS Imaging v8 software for efficient image management.

Companies Covered in Orthodontic Supplies Market

- Align Technology, Inc.

- 3M Company

- Dentsply Sirona Inc.

- Envista Holdings Corporation

- Henry Schein, Inc.

- American Orthodontics

- GC Corporation

- TP Orthodontics, Inc.

- Rocky Mountain Orthodontics

- Ormco Corporation

- Dentaurum GmbH & Co. KG

- Straumann Group

- DB Orthodontics Ltd.

Frequently Asked Questions

The global orthodontic supplies market is projected to be valued at US$ 8.4 billion in 2026.

The primary demand drivers in the orthodontic supplies market include the rising prevalence of malocclusion and dental misalignment, growing awareness regarding dental aesthetics, and increasing demand for cosmetic dentistry procedures.

North America leads with approximately 39% market share in 2025. The United States is the dominant country, representing ~82% of North American revenues, anchored by over 4 million annual orthodontic treatment starts, the world's highest Invisalign adoption rates, a mature orthodontic specialist network of over 11,000 orthodontists, and the global headquarters of leading innovators Align Technology and Dentsply Sirona.

Key market opportunities in the orthodontic supplies market include the growing adoption of clear aligners and aesthetic orthodontic treatments among adults seeking minimally visible dental correction solutions. Increasing integration of digital dentistry technologies such as 3D printing, CAD/CAM systems, intraoral scanners, and AI-based treatment planning is creating opportunities for advanced and customized orthodontic products.

The leading companies include Align Technology, Inc. (Invisalign, iTero), Dentsply Sirona Inc. (SureSmile, Primescan), 3M Company (SmartClip, Unitek), Envista Holdings (Spark Aligners, Ormco), Straumann Group (ClearCorrect), Henry Schein, Inc., American Orthodontics, Dentaurum GmbH, GC Corporation, and DB Orthodontics Ltd.