- Medical Devices

- Orthodontic Braces Market

Orthodontic Braces Market Size, Share, and Growth Forecast, 2025 - 2032

Orthodontic Braces Market By System Type (Conventional Braces, Self-Ligating Braces), Material (Stainless Steel Braces, Ceramic Braces), Placement (Buccal Braces, Lingual Braces), End-user (Hospitals, Dental Clinics), and Regional Analysis for 2025 - 2032

Orthodontic Braces Market Size and Trends Analysis

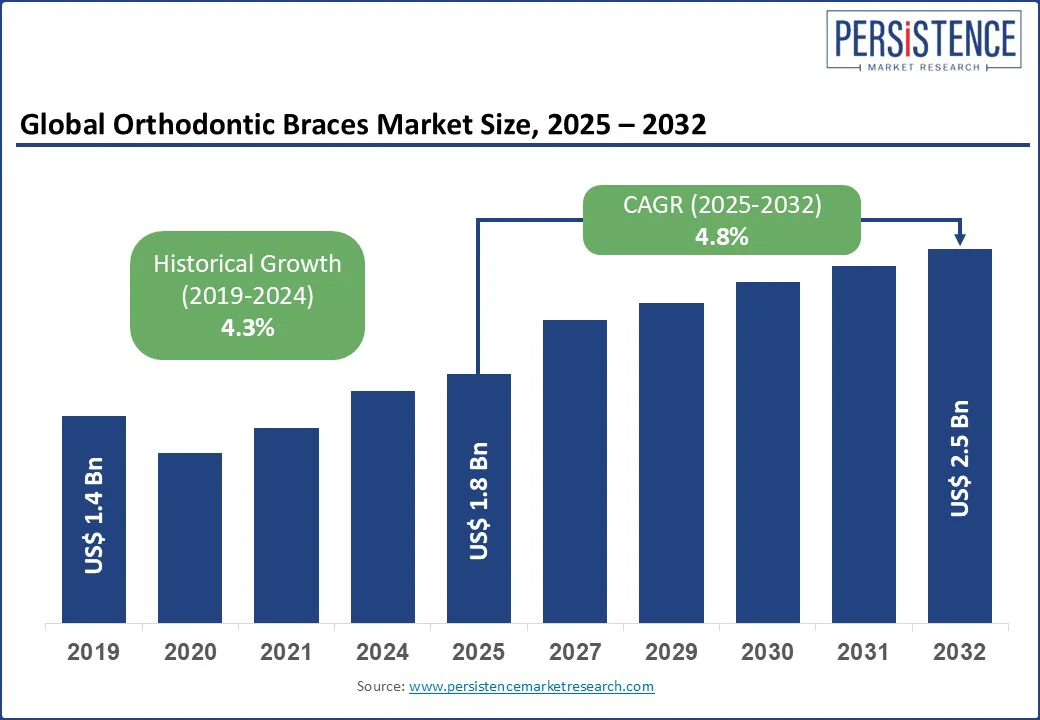

The global orthodontic braces market size is likely to value at US$1.8 Bn in 2025 and is expected to reach US$2.5 Bn by 2032, growing at a CAGR of 4.8% during the forecast period from 2025 to 2032.

The orthodontic braces industry is witnessing steady growth due to the increasing demand for aesthetic dental correction and advancements in self-ligating bracket technology. Rising adoption of orthodontic treatment among adults and growing awareness of malocclusion correction are driving long-term market dynamics.

Key Industry Highlights:

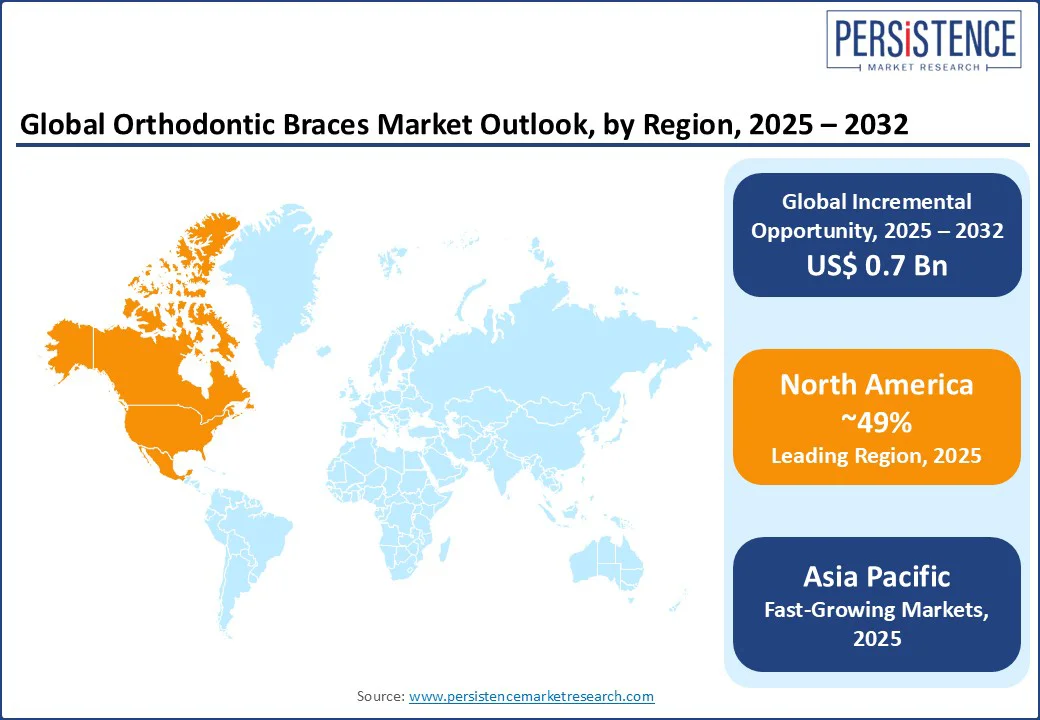

- Leading Region: North America, holding a 49% market share in 2025, driven by early adoption of digital orthodontics, strong presence of adult orthodontic patients, and advanced clinical infrastructure.

- Fastest-Growing Region: Asia Pacific, projected to grow at a CAGR of over 9.8%, fueled by rising dental awareness, AI-assisted treatment adoption, and expanding access to aesthetic braces across China, India, and Southeast Asia.

- Innovation Hotspot: Europe, establishing leadership in precision orthodontics through nano-ceramic composite R&D, cloud-integrated treatment systems, and strong regional manufacturers like Forestadent and DENTAURUM.

- Dominant System Type: Conventional Braces, accounting for over 56% of the market in 2025 due to affordability and widespread clinical adoption across adolescents and public health systems.

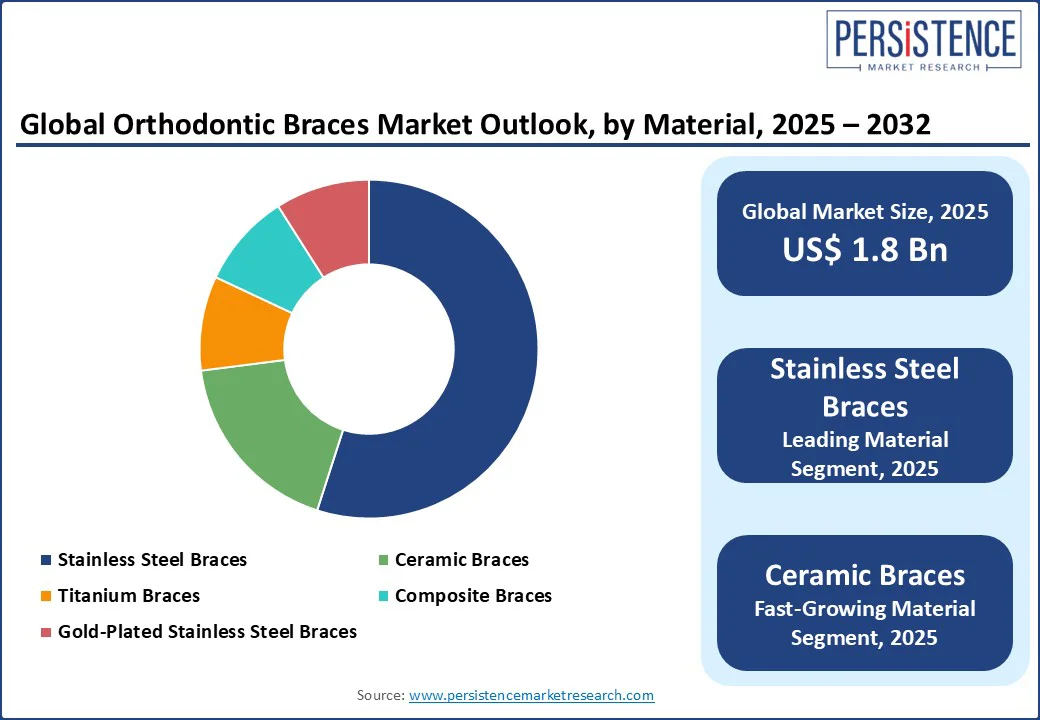

- Leading Material Segment: Stainless Steel Braces, holding the largest share due to cost-effectiveness, durability, and universal acceptance across developing and developed markets.

- Technological Trend: Surge in AI-driven diagnostics, 3D-printed brackets, and remote monitoring tools, shaping competitive differentiation across orthodontic solution providers.

- Strategic Aspect: Leading players such as Align, Ormco, and 3M are focusing on pediatric expansion, aesthetic brackets, and software-enabled treatment workflows through global approvals, AI partnerships, and financing models.

|

Global Market Attribute |

Key Insights |

|

Market Size (2025E) |

US$1.8 Bn |

|

Market Value Forecast (2032F) |

US$2.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.3% |

Market Dynamics

Driver - Digitalization and Rising Demand for Aesthetic, Efficient Orthodontic Treatments

Orthodontists drive demand by integrating 3D printed customized ceramic brackets, which deliver a highly precise fit and reduced adjustment visits. This SureSmile robotic arch wire customization technology accelerates tooth movement and shortens total treatment time. Patients prefer low-friction self-ligating systems that cut chair time and simplify oral hygiene. In emerging markets, the surge in dental tourism for fixed-braces treatment (especially in India and Mexico) is fueling bulk adoption of brackets and wires by cost- and quality-conscious patients.

Rising adolescent and adult interest in fashion-metal braces aesthetic, sparked by influencers embracing colorful metal brackets as style statements, has repositioned traditional braces as trendy accessories. This behavioral shift increases acceptance of nostalgia-driven metal bracket adoption, boosting market growth uniquely among Gen Z and millennial consumers.

At the same time, AI-driven treatment planning software supports personalized force application, improving outcomes in complex cases and reinforcing the adoption of advanced bracket systems by evidence-focused orthodontists.

Restraints - Limited Orthodontic Expertise and Uneven Adoption of Advanced Systems in Emerging Markets

In the case of metal and self-ligating braces, distribution inefficiencies remain a major bottleneck, particularly in non-metro areas. Clinics often deal with inflated distributor markups and long lead times for reorders, especially for advanced self-ligating orthodontic brackets.

This delays treatments and limits the reach of new bracket systems in secondary cities. Furthermore, recurring issues such as self-ligating bracket door failures have triggered discomfort complaints, cheek irritation, and occasional bracket replacements. These malfunctions dent patient trust and reduce repeat use, particularly among adults seeking streamlined and low-maintenance treatment options.

For ceramic and lingual bracket systems, patient hesitancy stems from persistent usability concerns. Many users report visible discoloration and ceramic bracket staining due to dietary pigments, despite using aesthetic wires. This undermines their appeal among adults choosing braces for cosmetic discretion. Lingual systems, though more advanced, carry their drawbacks. Patients frequently experience tongue ulcers from lingual bracket placements and speech disturbances during the adaptation phase. Despite CAD/CAM advances, speech clarity and tongue comfort remain unresolved pain points.

Opportunity - Expansion of AI-Driven Early Intervention Systems and Ceramic Braces in Adult Population

Orthodontic clinics can capitalize on 3D printed customized ceramic brackets that offer patient-specific adaptation and superior comfort. Digital workflows such as AI-guided indirect bonding systems (e.g., ORTHOSELECT DIBS AI) speed up bonding appointments and improve bracket placement accuracy, reducing chair time and improving outcomes.

Growing interest in self-ligating ceramic brackets integrated with CAD/CAM digital workflows, especially in Asia Pacific and Latin America clinics, open niches for localized manufacturing partnerships and digital-first product launches.

Advances in AI-powered orthodontic treatment simulation and virtual outcome visualization tools (e.g., OrthoGAN-style frontal face VTO) can enhance patient engagement and conversion for braces plans. Additionally, expanding direct-to-consumer fixed braces impression kits with virtual remote monitoring creates a disruptive path in cost-sensitive emerging markets, enabling clinics to reach underserved geographies via e-commerce channels efficiently.

Category-wise Analysis

System Type Insights

The largest segment in the orthodontic braces market by system type is conventional braces, accounting for approximately 56% of the global market share in 2025. These braces continue to dominate primarily due to their affordability, widespread clinical use, and suitability for a wide range of malocclusion cases. Orthodontists favor conventional systems in high-volume practices and public dental health programs, particularly in emerging economies where budget constraints remain significant. Their mechanical simplicity and lower up-front cost make them the default option for adolescent and teenage patients, who constitute a major user base.

In contrast, self-ligating braces represent the fastest-growing system type, expected to expand at a CAGR of 7.6% through 2031. These brackets eliminate the need for elastic or metal ties by using an internal mechanism to hold the archwire, resulting in reduced friction and fewer adjustment visits. Among self-ligating systems, passive self-ligating brackets currently accounts for the largest sub-segment share due to their ability to deliver gentle and continuous force, which improves patient comfort. Meanwhile, active self-ligating braces are gaining momentum for their enhanced torque control and suitability for complex tooth movements. This growth is driven by increased adoption in urban clinics and private practices that prioritize shorter treatment cycles, improved biomechanics, and patient satisfaction.

Material Insights

Stainless steel braces are the leading material type, holding an estimated 61% share of the global orthodontic braces market in 2025. Their dominance stems from superior strength, durability, and cost-efficiency, making them the material of choice for both standard and complex orthodontic cases. These metal braces are extensively used in institutional settings, such as school-based dental programs and government-subsidized clinics. Despite their visibility, their functional reliability and low breakage rates ensure they remain the backbone of large-scale orthodontic treatments worldwide.

Ceramic braces are emerging as the fastest-growing material segment, projected to grow at a CAGR of 7.1% through 2032. These braces offer the benefit of aesthetics with their tooth-colored or transparent brackets, making them particularly appealing to adult patients who seek discreet orthodontic solutions. Among them, self-ligating ceramic braces are gaining traction by combining the visual subtlety of ceramic with the mechanical efficiency of self-ligation.

This growth is most prominent in urban markets and among adults aged 25 to 40 who prioritize appearance without compromising functionality. Improvements in material strength, along with the integration of CAD/CAM and 3D printing in ceramic bracket customization, are further propelling this segment’s momentum, especially in premium and digital-forward orthodontic practices.

Regional Insights

North America Orthodontic Braces Market Trends

North America continues to dominate the global orthodontic braces market, accounting for nearly 49% of global revenue, driven by advanced clinical infrastructure, early technology adoption, and high consumer awareness. The United States, in particular, remains the core growth engine of the region. With over 9 million active orthodontic cases annually, the U.S. braces segment benefits from widespread adoption of AI-powered diagnostics, 3D-printed custom brackets, and self-ligating systems.

Clinics are increasingly shifting toward personalized treatment protocols that minimize chair time and enhance comfort, appealing to both adolescent and adult patients. Companies like 3M Oral Care and Ormco have been expanding their product lines to include low-friction, aesthetic systems that integrate seamlessly with digital workflows. Furthermore, the rise in adult orthodontic cases, which now account for nearly 30% of all new patients, has fueled demand for ceramic and lingual braces, especially in metropolitan areas like New York and Los Angeles.

In Canada, the orthodontic braces market is experiencing a structural transformation following the rollout of the Canadian Dental Care Plan (CDCP) in 2023. This national program is expanding access to essential orthodontic care for low- and middle-income groups, thereby boosting procedural volume in public and private clinics. Canadian providers are also showing growing interest in aesthetic fixed appliances, particularly ceramic self-ligating brackets, as adult patients seek discreet, professional-grade solutions.

Additionally, tele-orthodontic consultations and virtual monitoring tools have gained popularity across provinces, helping remote and underserved populations access orthodontic services without frequent in-person visits. This digital adoption trend positions Canada as a key secondary market within North America with high growth potential.

Asia Pacific Orthodontic Braces Market Trends

Asia Pacific is emerging as the fastest-growing region in the global orthodontic braces market, with a projected CAGR of over 9.8% from 2025 to 2032. This growth is powered by increasing dental awareness, rising disposable incomes, and a significant prevalence of malocclusion in young populations. In China, more than 45% of children and teenagers reportedly suffer from some form of dental misalignment, making the country a lucrative target for orthodontic solutions.

Urban middle-class consumers are showing increased preference for aesthetic fixed options, particularly tooth-colored ceramic and gold-plated stainless-steel brackets. The Chinese government’s push for healthcare modernization, through policies like volume-based procurement (VBP), has created more price competition, encouraging both domestic and foreign players to expand within the fixed braces segment. In 2024, leading global suppliers like Straumann and Dentsply Sirona reported double-digit growth in China, citing surging demand for aesthetic orthodontic solutions and digital bracket systems.

India is another high-potential market within the region, where over 35% of adolescents are estimated to require orthodontic intervention. The rapid growth of dental tourism, combined with increasing adoption of CAD/CAM-based ceramic bracket systems, is significantly transforming the market landscape.

In 2023, Align Technology opened its Align Innovation Centre in Hyderabad, reinforcing the country’s growing relevance as both a consumer and innovation hub for orthodontic care. Urban dental chains such as Clove Dental and Sabka Dentist are now offering digitally assisted fixed-brace treatments across Tier-1 and Tier-2 cities. Moreover, younger adults in India are increasingly opting for self-ligating and lingual braces, thanks to improved awareness, aesthetic concerns, and flexible financing options. The proliferation of e-commerce-based dental services and teleconsultation platforms also enables greater access in semi-urban markets.

Europe Orthodontic Braces Market Trends

Europe ranks as the second-largest regional market, supported by strong reimbursement policies, a well-trained orthodontic workforce, and widespread availability of advanced treatment systems. Germany, the region’s largest market, benefits from high dental expenditure per capita and a robust orthodontic infrastructure.

German manufacturers such as DENTAURUM and Forestadent are continuously innovating in self-ligating and ceramic bracket technologies, both for domestic use and export. Clinical preference in Germany leans toward precision-engineered passive self-ligating systems, which improve treatment control while reducing chairside visits. Germany is also among the first in Europe to implement cloud-based orthodontic record systems, which allow efficient treatment tracking and remote monitoring.

The United Kingdom is witnessing a rapid surge in demand for aesthetic orthodontics, especially among adults aged 25 to 45. This is driven by a cultural shift toward cosmetic dentistry and a willingness to invest in low-visibility options such as lingual and ceramic braces. While the NHS covers basic orthodontic care for children, adult patients are increasingly turning to private clinics for personalized and aesthetic treatments.

Clinics across London, Manchester, and Birmingham are reporting a growing number of patients opting for self-ligating ceramic braces with AI-integrated treatment planning, citing faster results and better visual appeal. Furthermore, the UK has witnessed a rise in subscription-based dental financing and partnerships between private providers and insurance platforms, making high-end orthodontic solutions more accessible. Ongoing R&D in nano-ceramic composites and frictionless bracket designs further adds to the UK’s position as an innovation-forward orthodontic braces market.

Competitive Landscape

The global orthodontic braces market is moderately consolidated, with a few dominant players controlling a large share, but with rising competition from regional manufacturers, dental chains, and startups leveraging digital innovation. The market is led by giants such as 3M Company, Ormco (Envista Holdings), and DENTSPLY SIRONA. These companies have maintained leadership through robust R&D investments, expansive product portfolios, and global distribution networks.

Companies are increasingly integrating AI-driven treatment planning, 3D-printed brackets, and remote monitoring tools to stay ahead. Simultaneously, demand for aesthetic-driven solutions, such as self-ligating ceramic brackets, low-profile buccal systems, and stain-resistant composites, is reshaping product development. In high-growth regions such as China, India, Brazil, and Turkey, regional manufacturers are gaining ground with cost-effective, customized brackets, challenging global incumbents. To maintain their edge, major players are accelerating strategic acquisitions and partnerships with digital health startups, as seen in Envista’s recent expansion into AI-powered planning platforms.

Key Industry Developments:

- In July 2025, Align further expanded access by receiving CDSCO approval in India, making the Invisalign Palatal Expander commercially available there. This approval covers both children and adults and reinforces Align’s digital-first early - treatment approach in a market with rapidly growing demand.

- In May 2025, Align Technology received NMPA approval in China for its Invisalign® Palatal Expander System, enabling its launch in mid-2025 as a 3D printed early intervention appliance targeting pediatric skeletal and dental expansion. This milestone positions Align as the first mover in China’s Phase - 1 orthodontic segment.

Companies Covered in Orthodontic Braces Market

- 3M Company

- Ormco Corporation (Envista Holdings)

- DENTSPLY SIRONA

- Align Technology, Inc.

- Forestadent

- American Orthodontics

- GC Orthodontics

- G&H Orthodontics

- Rocky Mountain Orthodontics (RMO)

- TP Orthodontics, Inc.

- Henry Schein Orthodontics

- DENTAURUM GmbH & Co.

- DB Orthodontics

- Leone S.p.A.

- Hangzhou Xingchen 3B Dental Instrument

- Modern Orthodontics

- Ortho Classic

- Tomy Inc.

- Zhejiang Protect Medical Equipment Co.

- Shanghai Ebrace Medical Technology

Frequently Asked Questions

The global orthodontic braces market is estimated to reach approximately US$1.8 billion in 2025.

The orthodontic braces market is projected to grow to around US$2.5 billion by 2032.

Major trends include rising adoption of AI-powered digital orthodontics and 3D-printed brackets, and the growth of self-ligating systems due to reduced friction and shorter treatment times.

By material, stainless steel metal braces remain the largest segment due to their affordability and wide application, holding over 61% market share in 2025.

The orthodontic braces market is expected to grow at a CAGR of 4.8% from 2025 to 2032, driven by rising dental awareness, expanding digital capabilities, and increasing investments in pediatric and adult orthodontic care.

Leading players with strong product portfolios include 3M Company, Ormco (Envista Holdings), Dentsply Sirona, Forestadent, and American Orthodontics.