- Non-food Packaging

- Ophthalmic Packaging Market

Ophthalmic Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Ophthalmic Packaging Market by Dose Format (Single-Dose, Multi-Dose), by Packaging Type (Bottles, Tubes, Vials & Ampoules, Syringes / Pre-filled Syringes, Other Ophthalmic Containers), Material (Plastic, Glass, Others), Product Type (Prescription Ophthalmic Products, Over-the-Counter (OTC) Ophthalmic Products), Regional Analysis, 2026 - 2033

Ophthalmic Packaging Market Size and Trend Analysis

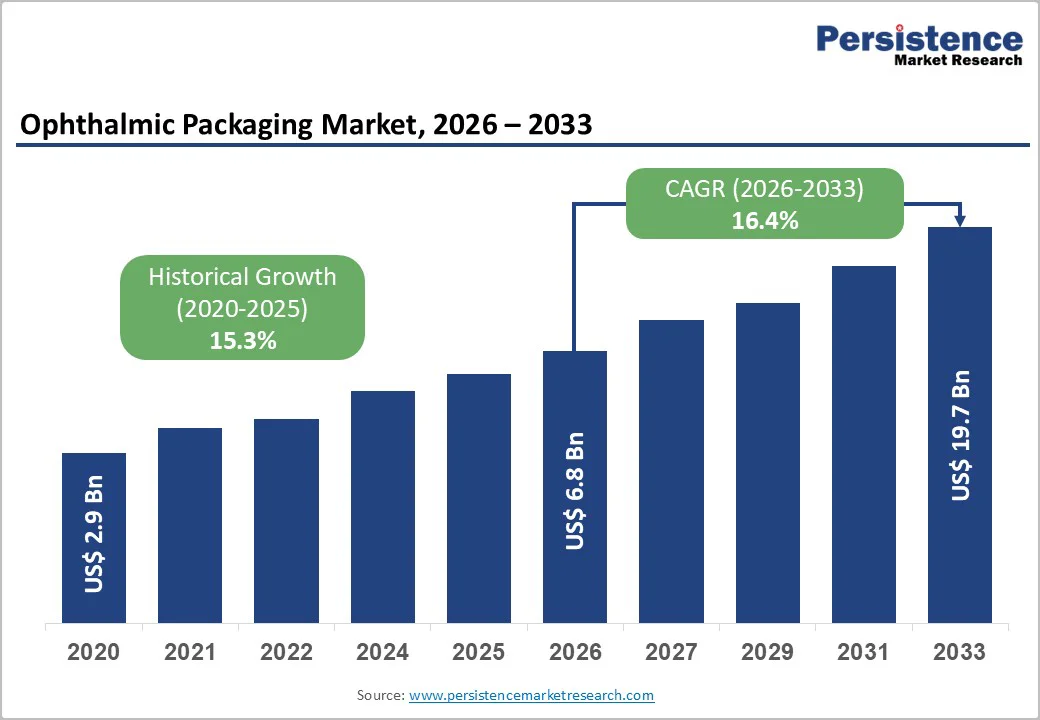

The global ophthalmic packaging market is projected to reach US$ 19.7 billion by 2033, up from US$ 6.8 billion in 2026, driven by a strong CAGR of 16.4%.

Growth is fueled by the rising prevalence of eye disorders, expanding aging populations, and accelerating demand for preservative-free formulations that require advanced, sterile packaging. With the World Health Organization estimating that 2.2 billion people experience vision impairment, over 1 billion of which are preventable, the need for safe, precise, and compliant ophthalmic packaging continues to surge. This expanding patient pool is significantly boosting production and innovation across ophthalmic packaging solutions globally.

Key Market Highlights:

- Leading Region: North America leads the ophthalmic packaging market with 38.4% share, driven by advanced healthcare infrastructure and strong premium packaging adoption.

- Fastest-Growing Region: Asia Pacific accounts for 35.8% share and is the fastest-growing region, due to rising healthcare access, urbanization, and manufacturing cost advantages.

- Leading Packaging Category: Multi-dose bottles dominate the dose-format segment with ~62% market share, favored for therapeutic efficacy, patient convenience, and cost efficiency.

- Fastest-Growing Formulation Type: Preservative-free ophthalmic formulations are expanding 2-3 percentage points faster than preserved alternatives, supported by consumer health consciousness and regulatory emphasis.

- Highest Innovation Opportunity: Intravitreal injection therapies for DME and AMD drive packaging innovation, requiring specialized syringes, depot systems, and integrated needle technologies for extended dosing intervals.

| Key Insights | Details |

|---|---|

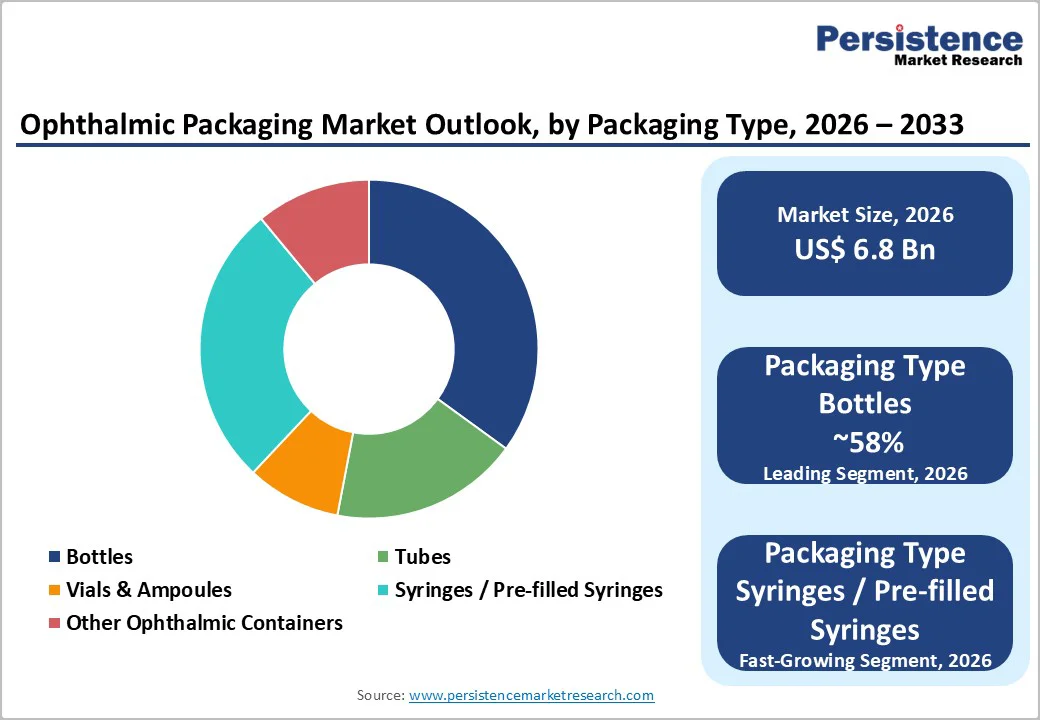

| Ophthalmic Packaging Market Size (2026E) | US$ 6.8 billion |

| Market Value Forecast (2033F) | US$ 19.7 billion |

| Projected Growth CAGR (2026 - 2033) | 16.4% |

| Historical Market Growth (2020 - 2025) | 15.3% |

Market Dynamics

Drivers - Growing Global Burden of Ocular Disorders and Age-Related Vision Impairment

The rising prevalence of eye diseases has become one of the most influential drivers of the ophthalmic packaging market. Diabetic retinopathy already affects around 95 million diabetic patients worldwide, with projections indicating an increase to 161 million by 2045. Alongside this, age-related conditions such as cataracts, glaucoma, and macular degeneration continue to surge, sharply increasing the demand for ophthalmic therapies and their associated packaging solutions.

Simultaneously, the expanding global geriatric population currently the fastest-growing demographic directly contributes to greater consumption of ophthalmic medications. The widespread use of contact lenses further intensifies demand, as users commonly experience dry eye syndrome and other ocular surface issues, increasing the need for complementary eye care products and higher packaging volumes across the pharmaceutical supply chain.

Advancements in Preservative-Free Ophthalmic Packaging and Delivery Systems

The transition toward preservative-free ophthalmic formulations has triggered substantial innovation in packaging technologies. AptarGroup’s Ophthalmic Squeeze Dispenser (OSD) remains a hallmark innovation, enabling multi-dose delivery using a mechanical Tip-Seal system and sterile filters that prevent backflow and contamination. These systems address long-standing concerns associated with preservatives like benzalkonium chloride, which are linked to irritation, allergic responses, and long-term ocular tissue damage among chronic users.

This shift is further amplified by stricter regulatory expectations from agencies such as the FDA and EMA, which increasingly favor preservative-free therapeutic options. As a result, manufacturers are investing heavily in advanced packaging platforms designed to maintain sterility without chemical preservatives. The preservative-free packaging segment continues to demonstrate strong momentum, recording growth rates exceeding 8.8% and driving modernization across ophthalmic packaging infrastructure.

Restraints - Stringent Regulatory Requirements and Complex Material Compatibility Constraints

The ophthalmic packaging industry operates under highly rigorous regulatory frameworks that demand extensive material-formulation compatibility testing. Agencies such as the FDA require comprehensive container closure system (CCS) evaluations to ensure that packaging components do not leach substances or interact adversely with active ingredients. While LDPE is widely used for aqueous solutions, it can absorb lipophilic formulations, whereas glass packaging introduces risks related to thermal expansion and breakage. Cyclosporine-based products, for example, are known to interact with PVC, necessitating costlier alternatives.

These requirements significantly extend development timelines, with approval cycles for new container systems often ranging from 18 to 36 months. Additionally, manufacturers must maintain GMP-compliant sterile packaging facilities equipped with clean rooms, sterilization systems, and stringent quality controls. Such technical and regulatory barriers heighten entry challenges for smaller players while reinforcing the dominance of established global manufacturers.

Rising Production Costs, Raw Material Volatility, and Material Availability Issues

The ophthalmic packaging sector faces ongoing cost pressures due to its dependency on specialized raw materials. Pharmaceutical-grade polymers such as HDPE and LDPE account for up to 45% of production costs, with price fluctuations tied closely to crude oil markets. Glass packaging manufacturers, particularly producers of Type I borosilicate containers, operate with limited capacity, resulting in periodic shortages when pharmaceutical demand spikes. Competition for resin supplies across multiple industries further exacerbates material scarcity, creating procurement instability for packaging companies.

Moreover, manufacturers must adapt to increasingly stringent environmental regulations that promote reduced plastic usage and the adoption of sustainable alternatives. Transitioning to eco-friendly materials requires extensive capital investments and production line upgrades. These financial constraints disproportionately impact small and mid-sized pharmaceutical firms in cost-sensitive regions, potentially limiting broader market growth and slowing adoption of advanced ophthalmic packaging solutions.

Opportunity - Growing Demand for Intravitreal Injection Therapies and Advanced Anti-VEGF Packaging Solutions

Intravitreal injections for AMD, DME, and retinal vein occlusions have become the fastest-growing therapeutic category in ophthalmology. Anti-VEGF drugs continue to expand rapidly, with growth estimates exceeding 9-12% through 2033. These therapies require highly specialized packaging systems including sterile vials, prefilled syringes, and integrated drug-delivery devices engineered to protect formulation stability and minimize contamination risks. Innovations such as micro-needle injectors and long-acting depot systems are further transforming treatment standards by extending dosing intervals and improving patient adherence.

As demand for sterile, ready-to-use injection kits rises, packaging solutions integrating vials, syringes, needles, and safety components are seeing strong adoption in clinical and surgical settings. Companies with advanced sterile manufacturing capabilities and expertise in precision injection packaging are well positioned to capture substantial value from this rapidly expanding therapeutic segment.

Rising OTC Ophthalmic Product Consumption and Accelerated Self-Care Adoption Globally

The over-the-counter (OTC) ophthalmic product market is expanding at a significantly faster pace than prescription-based therapeutics, supported by growing consumer awareness and widespread availability through pharmacies and retail channels. Increasing cases of dry eye disease affecting nearly 290 million people worldwide along with high incidence among contact lens users, are fueling demand for lubricating drops, anti-allergy solutions, and daily-use eye care products. This shift toward self-care is particularly strong in emerging economies such as India, Brazil, and Mexico, where rising middle-class populations are driving higher healthcare spending.

These trends create substantial opportunities for innovative, consumer-friendly packaging designed for portability, ease of use, and enhanced shelf appeal. Packaging formats that support preservative-free formulations and natural ingredient-based products align with growing health-conscious consumer preferences. Manufacturers offering ergonomic droppers, single-dose units, and premium aesthetic designs are well positioned to secure greater share in the booming global OTC ophthalmic segment.

Category-wise Analysis

Dose Format Insights

The multi-dose segment holds approximately 62% share, making it the dominant dose format in ophthalmic packaging. Its leadership is driven by suitability for chronic therapies such as glaucoma, antibiotics, and anti-inflammatory treatments. Multi-dose containers provide cost efficiency, reduced packaging waste, and long-term usability over 2-4 weeks. They incorporate preservation mechanisms such as benzalkonium chloride, antimicrobial-resistant technologies, and precision filtration to maintain sterility across the product lifecycle.

Single-dose packaging, although smaller in share, is rapidly gaining momentum due to its sterility advantages and critical role in preservative-free formulations. These units eliminate contamination risks inherent in repeated handling, improving safety for immunocompromised or long-term therapy patients. Their precise, sterile, one-time-use format makes them increasingly preferred for sensitive ophthalmic formulations.

Packaging Type Insights

Bottles account for approximately 58% of the ophthalmic packaging market, making them the leading packaging type for liquid formulations like eye drops, ointments, and suspensions. LDPE-based ophthalmic bottles provide optimal squeezability and controlled drop dispensing, making them ideal for elderly patients and those with limited hand strength. Features such as specialized droppers, tamper-evident closures, and secure sealing systems ensure product integrity and consistent therapeutic performance.

Pre-filled syringes are witnessing rapid adoption due to their strong role in intravitreal injections and the increasing shift toward patient-friendly administration formats. They provide superior sterility assurance and dosing accuracy in clinical environments. Vials and ampoules continue to serve essential roles in surgical and institutional settings where controlled handling and specialized drug delivery are prioritized.

Material Insights

Plastic materials represent approximately 65.7% of total ophthalmic packaging use, driven primarily by LDPE and HDPE applications. LDPE enables excellent drop-control performance and flexibility essential for eye drop bottles, while HDPE provides enhanced rigidity for vial and cartridge formats. Plastics are widely favored for their chemical resistance, cost efficiency, and adaptability across a wide array of pharmaceutical formulations.

Glass materials particularly borosilicate and de-alkalized soda-lime variants remain critical for sensitive or specialty ophthalmic drugs requiring high chemical stability. These materials are preferred for formulations prone to absorption or interaction with plastics, such as cyclosporine or high-potency antibiotic suspensions. Their role remains especially strong in biologics and institutional ophthalmic applications.

Product Type Insights

Prescription ophthalmic products capture approximately 60% of market share, supported by their therapeutic complexity and the regulatory precision required to maintain safety and efficacy. This segment includes glaucoma medications, corticosteroids, NSAIDs, and broad-spectrum ophthalmic antibiotics. Packaging solutions must ensure chemical stability, precise dosing, tamper resistance, and contamination control across varied storage and usage conditions.

OTC ophthalmic products continue to expand rapidly, driven by rising consumer preference for self-care and the increasing prevalence of dry eye, allergies, and daily-use eye discomfort. User-friendly packaging emphasizing portability, ergonomics, and aesthetic appeal plays a key role in OTC adoption. Innovations in preservative-free and natural formulations further reinforce demand for modern, consumer-centric packaging designs.

Regional Insights

North America Ophthalmic Packaging Market Trends

North America leads the global ophthalmic packaging landscape with a 38.4% market share, supported by advanced healthcare infrastructure, strong pharmaceutical consumption rates, and continuous regulatory-led innovation. The U.S. drives most of the demand, with growing adoption of smart packaging technologies including real-time stability monitoring and serialization-enabled traceability systems. Aging demographics further reinforce market strength, as the 65+ population continues expanding at approximately 3.2% annually. High contact lens usage, covering around 14% of the population, also fuels increased demand for dry eye and ocular surface therapies.

The FDA’s stringent container closure system requirements shape regional technological advancements and global industry standards. Updated regulatory guidelines related to drop size accuracy (20-70 microliters), sterility assurance, and tamper-evident designs ensure high-quality manufacturing practices. These regulatory benchmarks give North American manufacturers competitive advantages and position the region as a global leader in ophthalmic packaging innovation.

Europe Ophthalmic Packaging Market Trends

Europe demonstrates robust growth momentum with a 13.8% CAGR, driven by EMA-harmonized regulatory frameworks, strong public healthcare systems, and widespread adoption of advanced ophthalmic technologies. Germany remains the region’s manufacturing anchor, strengthened by Gerresheimer’s acquisition of Bormioli Pharma in late 2024, which expanded its integrated packaging systems capabilities. Countries such as the U.K., France, and Spain show consistent demand growth supported by their emphasis on preventive eye care and improved accessibility to ophthalmic therapeutics.

Europe’s regulatory environment increasingly prioritizes preservative-free and single-use formats, accelerating demand for sterile, high-precision packaging systems. The region also leads global efforts in sustainable pharmaceutical packaging, investing heavily in bioplastics, recycled polymer-based designs, and low-emission manufacturing processes. These sustainability-driven innovations allow European manufacturers to differentiate themselves in environmentally conscious pharmaceutical markets.

Asia Pacific Ophthalmic Packaging Market Trends

Asia Pacific holds a significant 35.8% share of the global ophthalmic packaging market, emerging as the fastest-growing regional cluster due to rapidly expanding populations, improving healthcare accessibility, and a strong pharmaceutical manufacturing base. China dominates regional output with integrated production chains spanning glass tubing to automated filling and cartoning. SGD Pharma’s recent furnace modernization in Zhanjiang highlights ongoing investment in sterile injectable-grade packaging materials aligned with national serialization requirements.

India, Japan, and ASEAN markets collectively reinforce regional momentum through expanding manufacturing capabilities and increasing ophthalmology care demand. India continues to scale its packaging production due to favorable labor economics and rapid technology modernization. Japan stands out for its advanced intravitreal and biologics packaging systems, shaped by aging demographics and precision-driven healthcare needs. Meanwhile, Southeast Asian markets including Vietnam, Thailand, and Indonesia show accelerating growth as healthcare infrastructure and ophthalmic service penetration increase across the region.

Competitive Landscape

The ophthalmic packaging market is moderately consolidated, with the top tier of manufacturers accounting for roughly 45-50% of global revenue. Market leaders maintain dominance through broad product portfolios, advanced proprietary dispensing and polymer technologies, and strong global supply capabilities. Their competitive edge is reinforced by continuous investments in innovation, sterile manufacturing, and compliance infrastructure.

A second tier of emerging players is gaining traction through specialization in sustainable materials, high-precision components, and cost-efficient regional production. These companies focus on preservative-free compatible formats, eco-friendly substrates, and integrated device-drug delivery solutions. The landscape increasingly prioritizes reliability, material science, and regulatory excellence.

Key Market Developments

- In December 2024, Gerresheimer AG finalized its strategic acquisition of Blitz LuxCo Sarl, the holding company for Bormioli Pharma Group, substantially expanding European manufacturing footprint and complementary product portfolio capabilities across pharmaceutical glass and plastic containment solutions.

- In October 2024, AptarGroup Inc. continued advancing its Ophthalmic Squeeze Dispenser (OSD) technology platform through enhanced customization solutions and partnerships with leading ophthalmic pharmaceutical manufacturers seeking to commercialize preservative-free formulations.

- In November 2023, West Pharmaceutical Services Inc. launched enhanced elastomer formulations including FluroTec 5-10 mL cartridge plungers designed to support large-volume injectable biologic therapies, addressing emerging requirements for complex drug delivery systems in ophthalmology.

Companies Covered in Ophthalmic Packaging Market

- Gerresheimer AG

- AptarGroup Inc.

- Amcor plc

- Schott AG

- West Pharmaceutical Services Inc.

- Berry Global Inc.

- Bormioli Pharma S.p.A.

- Nolato AB

- Vetter Pharma

- SGD Pharma

- Tekni-Plex Inc.

- Recipharm AB

- ALPLA Group

- Hoffmann Neopac

- Nemera

Frequently Asked Questions

The global ophthalmic packaging market is expected to reach US$ 19.7 billion by 2033, up from US$ 6.8 billion in 2026, growing at 16.4% CAGR.

Market growth is fueled by rising diabetic retinopathy cases, expanding geriatric populations, and increasing adoption of preservative-free formulations.

Multi-dose bottles lead with ~62% market share, preferred for therapeutic products due to cost efficiency, patient convenience, and extended treatment coverage.

North America commands 38.4% share, supported by advanced healthcare systems, regulatory frameworks, and premium product adoption.

Intravitreal injection therapies for DME and AMD represent the fastest-growing segment, requiring specialized pre-filled syringes and depot systems, with projected 9-12% CAGR.

Leading market participants include Gerresheimer AG, AptarGroup Inc., Amcor plc, Schott AG, and West Pharmaceutical Services Inc.