- Medical Devices

- U.S. Ophthalmic Photocoagulator Market

U.S. Ophthalmic Photocoagulator Market Market Size, Share, and Growth Forecast, 2026 – 2033

U.S. Ophthalmic Photocoagulator Market by Wavelength (Green Scan Laser, Multicolor Scan Laser, Others), Application (Macular Edema, Retinopathy, Glaucoma, Others), End-user (Hospitals, Ambulatory Surgery Centers, Ophthalmic Clinics), and Zone Analysis 2026 – 2033

U.S. Ophthalmic Photocoagulator Market Share and Trends Analysis

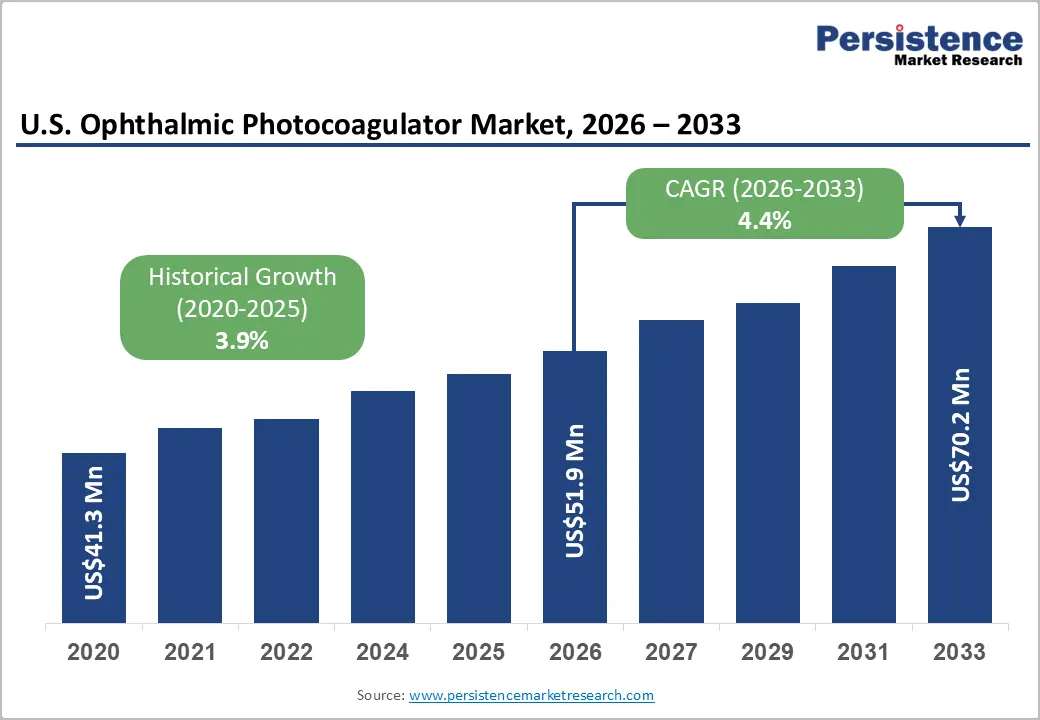

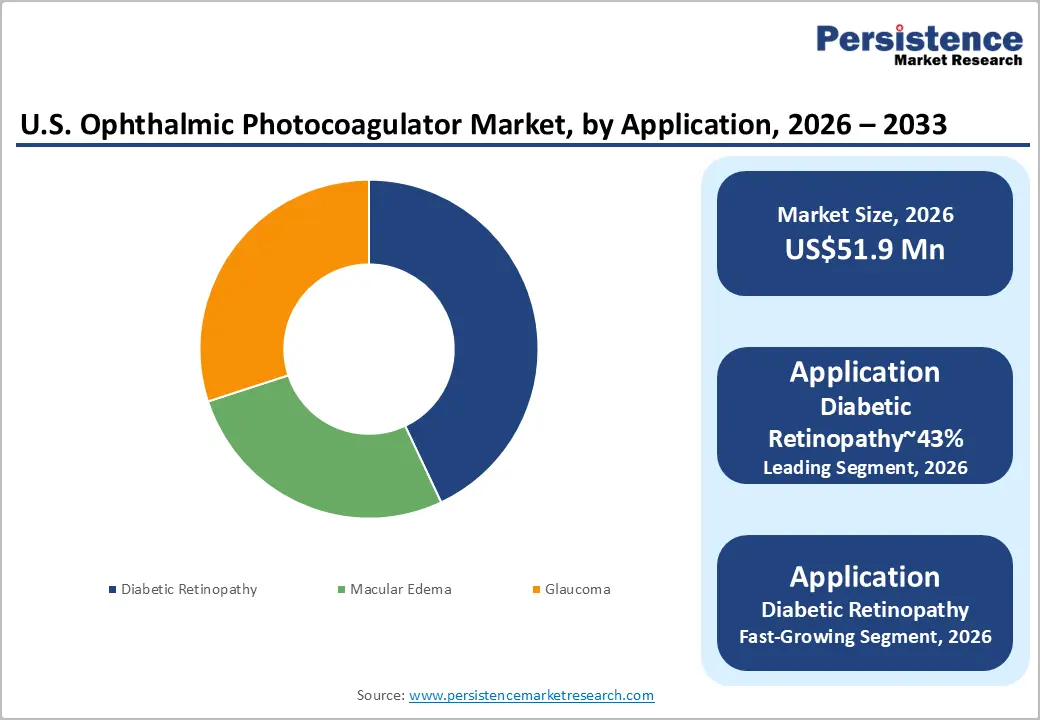

The U.S. ophthalmic photocoagulator market size is likely to be valued at US$51.9 million in 2026 and is projected to reach US$70.2 million by 2033, growing at a CAGR of 4.4% during the forecast period from 2026 to 2033, driven by the escalating clinical burden of diabetic retinopathy (DR) and a structural transition in healthcare delivery toward Ambulatory Surgery Centers (ASCs).

Increasing diagnostic screening rates, coupled with the integration of artificial intelligence (AI)-guided targeting in laser systems, have further optimized treatment throughput. Advancements in multicolor lasers enhance precision, while an aging population increases retinal disorder cases. The rapid adoption of multicolor scan lasers is diversifying therapeutic capabilities, ensuring sustained investments in specialized retinal care infrastructure.

Key Industry Highlights:

- Leading Wavelength: Green scan laser is expected to lead accounting with approximately 49% share in 2026 through clinical adoption, precise hemoglobin absorption, high procedural throughput, and trusted application in retinal vascular treatments.

- Fastest-growing Wavelength: Multicolor scan laser is anticipated to grow fastest due to on-demand wavelength selection, hybrid multi-layer retinal workflows, AI-guided spot placement, and embedding within high-volume ophthalmic enterprises.

- Leading Application: Diabetic retinopathy is projected to dominate for simplicity, clinical necessity, integration with imaging, and procedural efficiency across hospitals and ASCs, holding approximately 43% share in 2026.

- Fastest-growing Application: Diabetic retinopathy is anticipated to grow fastest due to early-intervention protocols, portable device adoption, AI-assisted targeting, and enhanced workflow integration in outpatient and clinic settings.

| Key Insights | Details |

|---|---|

| U.S. Ophthalmic Photocoagulator Market Size (2026E) | US$51.9 Mn |

| Market Value Forecast (2033F) | US$70.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.4% |

| Historical Market Growth (CAGR 2019 to 2025) | 3.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Clinical Burden of Diabetic Retinopathy and Geriatric Demographic Shifts

The U.S. ophthalmic photocoagulator market is fundamentally driven by the increasing prevalence of diabetic retinopathy, a leading cause of vision impairment among working-age adults. Expanding diabetic populations are amplifying clinical demand for effective retinal therapies, embedding photocoagulation devices within standard ophthalmic care protocols. Concurrently, the aging population is experiencing a higher incidence of age-related ocular disorders, reinforcing long-term procedural requirements. This demographic shift necessitates sustained investment in photocoagulator systems capable of reliable and definitive treatment. Healthcare institutions prioritize devices offering consistent clinical outcomes, procedural efficiency, and integration with diagnostic imaging, supporting replacement cycles and capacity expansion. Evolving treatment guidelines emphasize early intervention and multi-laser therapy approaches, further consolidating photocoagulator adoption across hospital networks and specialized ophthalmology centers. Operational priorities include system reliability, safety compliance, and clinical throughput optimization, all shaping procurement and investment patterns in the sector.

The structural impact of demographic and disease trends extends to market economics and technology adoption dynamics. Photocoagulator manufacturers face pressure to align device design with aging-patient ergonomics, clinician training, and outpatient application requirements. Integration with multimodal imaging systems enhances treatment precision, improving patient outcomes while reducing procedural risk. Regulatory compliance reinforces preference for validated, high-performance platforms, indirectly influencing margin structures across entry-level and premium devices. Infrastructure adaptation, including space and energy considerations in ambulatory and hospital settings, guides strategic deployment of laser systems. This creates a stable, long-term demand foundation for ophthalmic photocoagulators, establishing predictable adoption patterns.

Regulatory Backing and Expanding Clinical Prevalence Driving Photocoagulator Adoption

The U.S. ophthalmic photocoagulator market is largely driven by the substantial clinical burden of conditions such as diabetic retinopathy, glaucoma, and macular edema. Targeted retinal treatments using green scan lasers are increasingly favored due to their effective absorption properties, influencing device preferences across hospitals and outpatient care facilities. The growing incidence of retinal disorders among the aging population further strengthens demand for dependable photocoagulation procedures, integrating these systems into standard ophthalmic treatment practices. Healthcare providers increasingly seek devices that ensure consistent clinical performance while supporting higher patient volumes and efficient procedural workflows. The incorporation of advanced imaging capabilities and precise laser control improves treatment accuracy and operational efficiency. As demographic shifts and disease prevalence continue to rise, procedural demand remains steady, reinforcing the role of photocoagulator systems in routine ophthalmology care.

Regulatory structures, particularly approval pathways from the U.S. Food and Drug Administration, support quicker market entry for new laser photocoagulator technologies, influencing investment decisions and procurement strategies. Compliance standards also encourage the adoption of devices with proven safety and performance profiles, indirectly shaping cost dynamics and market margins. Market uptake is further supported by expanding use in outpatient facilities and ambulatory surgical centers, where compact and multifunctional laser platforms help address infrastructure limitations. Technological progress, including multicolor laser integration and improved targeting precision, broadens clinical applications while maintaining high safety standards. Collectively, regulatory support, strong clinical demand, and continuous technological advancements continue to drive the development and adoption of ophthalmic photocoagulator systems in the U.S.

Barrier Analysis – High Capital Expenditure and Variable Reimbursement Landscapes

The U.S. ophthalmic photocoagulator market faces structural adoption barriers due to substantial initial investment requirements for advanced laser systems. High upfront costs, combined with ongoing maintenance and specialized service obligations, limit deployment in smaller private practices and rural clinics. Capital intensity constrains procurement cycles and delays integration of the latest laser technologies, creating a heterogeneous adoption landscape. Providers weigh device cost against procedural throughput and clinical demand, influencing replacement frequency and upgrade patterns. Operational budgets and hospital allocation strategies are heavily impacted by these expenditure pressures. The necessity for predictable performance and compliance with safety standards further amplifies procurement complexity.

Variable reimbursement dynamics exacerbate adoption constraints, as fluctuating coverage rates from Medicare and private insurers affect procedural economics. When reimbursement for laser photocoagulation procedures fails to align with equipment costs, providers experience reduced ROI, prompting prolonged device lifecycles. This introduces structural inertia in the new-sales pipeline and influences investment prioritization across healthcare networks. Combined with capital intensity, reimbursement variability shapes market segmentation between high-volume hospitals and smaller ophthalmology clinics. These dynamics create a conservative financial environment that tempers rapid expansion.

Competition from Anti-VEGF Therapies

The U.S. ophthalmic photocoagulator market encounters significant competitive pressure from anti-VEGF injection therapies, which are increasingly utilized for macular edema management. These pharmacologic interventions provide non-thermal treatment alternatives, reducing reliance on laser-based procedures across clinical settings. Their adoption influences procedural volumes, particularly in age-related macular degeneration cases, and shifts patient management protocols toward pharmacologic rather than device-based intervention. Hospitals and outpatient centers adjust procurement priorities and operational workflows in response to this substitution effect. The integration of anti-VEGF treatments also alters treatment scheduling, resource allocation, and clinician time utilization, indirectly affecting photocoagulator utilization rates.

Supply chain constraints for laser components further compound market challenges by increasing cost volatility and procurement complexity. Device manufacturers face pressure to maintain availability while managing component shortages and fluctuating material costs. These structural limitations, combined with pharmacologic competition, influence margin structures, investment planning, and technology adoption strategies. The convergence of procedural substitution and supply chain pressures creates a restrained growth environment, necessitating careful alignment of clinical utility, cost structures, and operational deployment for ophthalmic laser systems.

Opportunity Analysis – Integration of AI and Automated Image-Guided Targeting

The U.S. ophthalmic photocoagulator market is positioned to benefit from the integration of artificial intelligence and automated image-guided laser targeting. Systems combining OCT imaging with laser delivery enable precise identification and treatment of microaneurysms and leaking retinal vessels, minimizing procedural errors and enhancing patient safety. This convergence supports navigated photocoagulation approaches that reduce risk to sensitive regions such as the fovea, strengthening clinical adoption across hospitals and specialized eye centers. Providers increasingly prioritize devices that combine imaging, data analytics, and automated treatment guidance, embedding AI-enabled platforms within standard ophthalmic workflows.

The adoption of AI-integrated systems creates high-value revenue opportunities for manufacturers, as clinical and operational benefits justify premium pricing strategies. Precision targeting reduces retreatment rates, procedural time, and clinician workload, influencing operational efficiency and margin structures. Digital health integration further allows interoperability with electronic medical records and teleophthalmology platforms, extending device utility across multiple care settings. These factors collectively enhance the market appeal of advanced photocoagulators, positioning AI-enabled technologies as a differentiating growth vector in the U.S. retinal therapy landscape.

Portable and Multicolor Laser Adoption

The U.S. ophthalmic photocoagulator market is increasingly shaped by demand for compact, portable laser systems suitable for clinic and ambulatory settings. Smaller footprints enable broader deployment across outpatient and specialized ophthalmology centers, enhancing procedural accessibility and operational flexibility. Multicolor laser technology addresses complex, layered retinal treatment requirements, allowing clinicians to selectively target different tissue types with optimized wavelength absorption. This capability improves treatment precision, reduces collateral tissue damage, and supports adoption in advanced retinal therapy protocols. Policy incentives for outpatient procedures further encourage investment in versatile, portable platforms, aligning financial and clinical objectives within hospital and clinic networks.

The convergence of portability and multicolor functionality generates a differentiated value proposition, influencing procurement priorities and technology upgrade cycles. Devices that integrate multiple wavelengths with ergonomic design reduce procedural complexity and enhance throughput, reinforcing operational efficiency. Supply chain alignment, component reliability, and maintenance considerations shape deployment strategies and cost structures. Collectively, these factors create a high-value growth segment, expanding adoption potential across diverse clinical environments while embedding technological sophistication into mainstream ophthalmic laser practice.

Category-wise Analysis

Wavelength Insights

Green scan laser is expected to lead, accounting for approximately 49% share in 2026, underpinned by its entrenched role as the clinical standard for retinal vascular treatments. Adoption remains anchored by precise hemoglobin and melanin absorption, preserving healthy tissue and minimizing procedural complications. Ongoing platform evolution, including AI-assisted imaging, auto-forward scanning, and compact designs for ambulatory surgery centers, continues to reinforce replacement cycles and utilization intensity.

Key brands such as NIDEK CO., LTD. with the GYC-500 series, Alcon Inc. through the Unity platform, and IRIDEX Corporation with PASCAL and MicroPulse technologies have locked in enterprise workflows and clinical trust. This combination of mature infrastructure, ecosystem integration, and predictable procedural demand sustains the Green Scan segment’s dominance within structured U.S. ophthalmic deployment models.

Multicolor scan laser is expected to be the fastest-growing segment, driven by emerging clinical needs for multi-layered retinal therapies and workflow flexibility across diabetic retinopathy, macular edema, and age-related macular degeneration. Growth is catalyzed by the integration of green, yellow, and red wavelengths within a single system, improving treatment precision, reducing complications, and enhancing patient throughput. Accelerating adoption is supported by AI-guided spot placement, pattern scanning, and modular wavelength upgrades.

Leading brands, including NIDEK with MC-500 Vixi, IRIDEX with PASCAL Synthesis, and Quantel Medical with EasyRet, are embedding multicolor platforms into clinical workflows. As clinical validation, ergonomic interfaces, and ASC-focused deployment improve, the segment is expected to outpace overall market growth over the forecast period.

Application Insights

Diabetic retinopathy is expected to lead, accounting for approximately 43% share in 2026, underpinned by its entrenched role as the primary indication for pan-retinal photocoagulation across hospitals and ambulatory surgery centers. Adoption remains anchored by clinical necessity to prevent vision loss, with providers prioritizing procedural reliability, throughput, and integration with imaging platforms in both public and private care settings. Ongoing platform evolution, including AI-assisted lesion detection, multi-spot pattern scanning, and sub-threshold MicroPulse protocols, continues to reinforce treatment efficiency and safety.

Leading brands such as IRIDEX with PASCAL Synthesis, NIDEK with GYC-500, and Alcon through Unity workstations have embedded their devices within clinical workflows. This combination of established clinical trust, technological sophistication, and procedural standardization sustains the segment’s dominance.

Diabetic retinopathy is expected to be the fastest-growing segment, driven by the increasing prevalence of diabetes and earlier intervention protocols that expand the patient pool for laser therapy. Growth is catalyzed by AI-guided targeting, real-time OCT integration, and multi-spot scanning, which materially improve treatment precision, reduce procedural time, and lower clinician workload. Accelerating adoption is supported by portable and clinic-friendly photocoagulator designs, pattern scanning, and integration with digital health workflows.

Brands including IRIDEX, NIDEK, and Topcon Healthcare are leveraging advanced platforms and ergonomic interfaces to capture early-cycle demand. As multi-layer retinal targeting, telemedicine integration, and procedural efficiency continue to improve, the segment is expected to outpace overall market growth throughout the forecast period.

Competitive Landscape

The U.S. Ophthalmic Photocoagulator market is moderately consolidated, with the top five players, Alcon, Carl Zeiss Meditec, NIDEK, IRIDEX, and Topcon, controlling a significant portion of total revenue. Market leadership is anchored in technological differentiation, particularly in high-speed pattern scanning, multi-wavelength integration, and AI-assisted targeting for complex retinal procedures. Large conglomerates dominate comprehensive “all-in-one” platforms, while specialized firms such as OD-OS (Navilas) maintain niche positions with navigated and portable laser solutions.

Industry behavior reflects incremental platform evolution, including MicroPulse adoption, multi-modal versatility, and ergonomic clinic-focused designs. Fragmentation among smaller players encourages innovation in targeted segments, and ecosystem consolidation among leading vendors reinforces operational stickiness. Overall, competitive positioning is defined by the ability to integrate advanced optics, software, and service models, enabling providers to optimize procedural efficiency, safety, and throughput across hospitals, ambulatory surgery centers, and high-volume ophthalmic clinics.

Key Industry Developments:

- In February 2026, Alcon reported strong 2025 growth driven by the successful global launch of its Unity platform. The Unity platform’s integrated vitreoretinal and cataract capabilities enhance surgical workflow and device ROI for high-volume ophthalmic clinics.

- In January 2026, IRIDEX Corporation reported a preliminary 8% year-over-year revenue growth for 2025, reaching over $52 million. Sustained growth in retinal laser system sales, particularly the PASCAL series, underscores the increasing demand for precision photocoagulation in the U.S.

- In September 2025, Alcon launched "Intelligent Service Solutions" to enable remote diagnostics and software updates for its global device fleet. Remote monitoring reduces downtime for photocoagulators and other surgical lasers, ensuring higher patient throughput in busy surgical centers.

Companies Covered in U.S. Ophthalmic Photocoagulator Market

- Alcon Inc.

- Carl Zeiss Meditec AG

- NIDEK CO., LTD.

- IRIDEX Corporation

- TOPCON CORPORATION

- Lumenis Ltd.

- Lumibird Medical (Quantel Medical & Ellex)

- Bausch + Lomb Incorporated

- OD-OS GmbH

- Valon Lasers

- Johnson & Johnson Vision Care, Inc.

- Norlase

- Meridian Medical Group

- A.R.C. Laser GmbH

- MEDA Co., Ltd.

- Lab Medica Systems

Frequently Asked Questions

The U.S. ophthalmic photocoagulator market is projected to be valued at US$51.9 million in 2026 and is expected to reach US$70.2 million by 2033, driven by the rising prevalence of diabetic retinopathy, the adoption of multicolor lasers, and a shift toward ambulatory surgery centers.

Diabetic retinopathy creates sustained procedural demand, as early intervention with pan-retinal photocoagulation prevents vision loss. Increasing diabetes prevalence, integration of AI-guided targeting, and multi-spot scanning technologies enhance treatment precision and throughput, motivating hospitals and clinics to adopt advanced laser systems.

The market is forecast to grow at a CAGR of 4.4% from 2026 to 2033, supported by multicolor laser adoption, demographic shifts toward aging populations, and rising outpatient and ASC-based procedural volumes.

Green scan lasers lead the wavelength segment due to established clinical efficacy, while diabetic retinopathy dominates application demand, reflecting its role as the primary indication for pan-retinal photocoagulation across hospitals and ambulatory centers.

The U.S. ophthalmic photocoagulator market is moderately consolidated, with key players including Alcon Inc., Carl Zeiss Meditec AG, NIDEK CO., LTD., IRIDEX Corporation, TOPCON CORPORATION, Lumenis Ltd., Lumibird Medical, Bausch + Lomb, OD-OS GmbH, Valon Lasers, Johnson & Johnson Vision Care, Norlase, Meridian Medical Group, A.R.C. Laser GmbH, and MEDA Co., Ltd.