- Medical Devices

- Ophthalmic Knives Market

Ophthalmic Knives Market Size, Share, and Growth Forecast, 2026 – 2033

Ophthalmic Knives Market by Design (Straight Knives, Crescent Knives, Slit Knives, Others), Product Type (Reusable Ophthalmic Knives, Others), Application (Cataract Surgery, Glaucoma Surgery, Others), and Regional Analysis for 2026 - 2033

Ophthalmic Knives Market Share and Trends Analysis

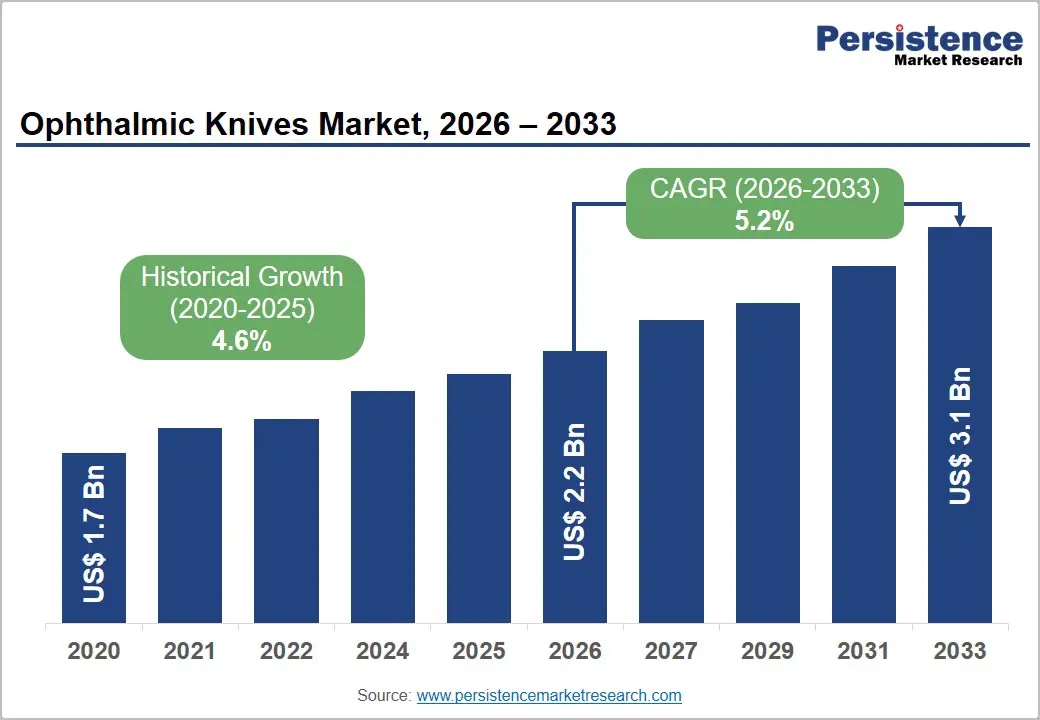

The global ophthalmic knives market size is likely to be valued at US$2.2 billion in 2026 and is estimated to reach US$3.1 billion by 2033, growing at a CAGR of 5.2% during the forecast period from 2026 to 2033, driven by rising ophthalmic surgical volumes, expanding access to specialized eye care services, and increasing adoption of precision surgical instruments.

The market is benefiting from a growing elderly population, which is increasing the incidence of cataracts, glaucoma, and retinal disorders requiring surgical intervention. Regulatory emphasis on surgical safety and infection prevention is accelerating demand for advanced disposable and precision-engineered instruments. Technological advancements in blade materials, micro-incision designs, and ergonomic surgical tools are improving procedural outcomes and supporting wider adoption.

Key Industry Highlights:

- Leading Design: Straight knives are set to hold around 31% revenue share in 2026, driven by widespread adoption in standard anterior segment and cataract surgical procedures.

- Fastest-growing Design: MVR (Micro Vitreoretinal) knives are projected as the fastest-growing segment, supported by accelerating adoption of minimally invasive posterior segment surgery across tertiary ophthalmic centers.

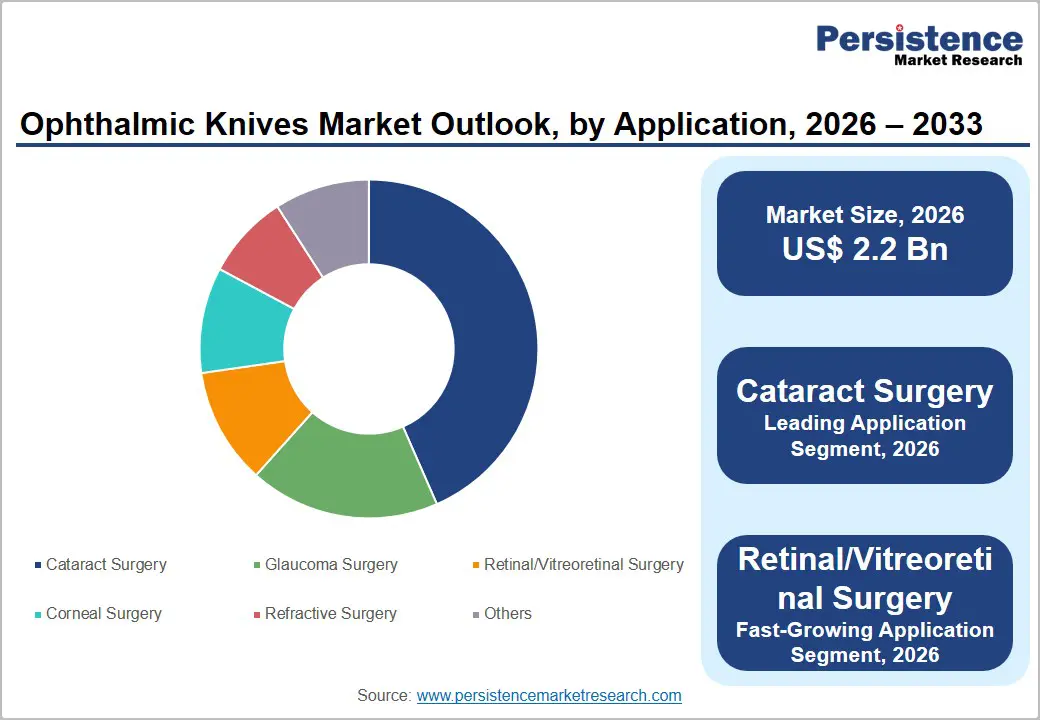

- Leading Application: Cataract surgery is estimated to hold roughly a 43% revenue share in 2026, due to unmatched global procedural volume driven by the cataract disease burden and expanding public surgical programs.

- Fastest-growing Application: Retinal/Vitreoretinal surgery is forecast to record the fastest growth, driven by rising diabetic retinopathy prevalence and increasing surgical complexity across posterior segment ophthalmic care.

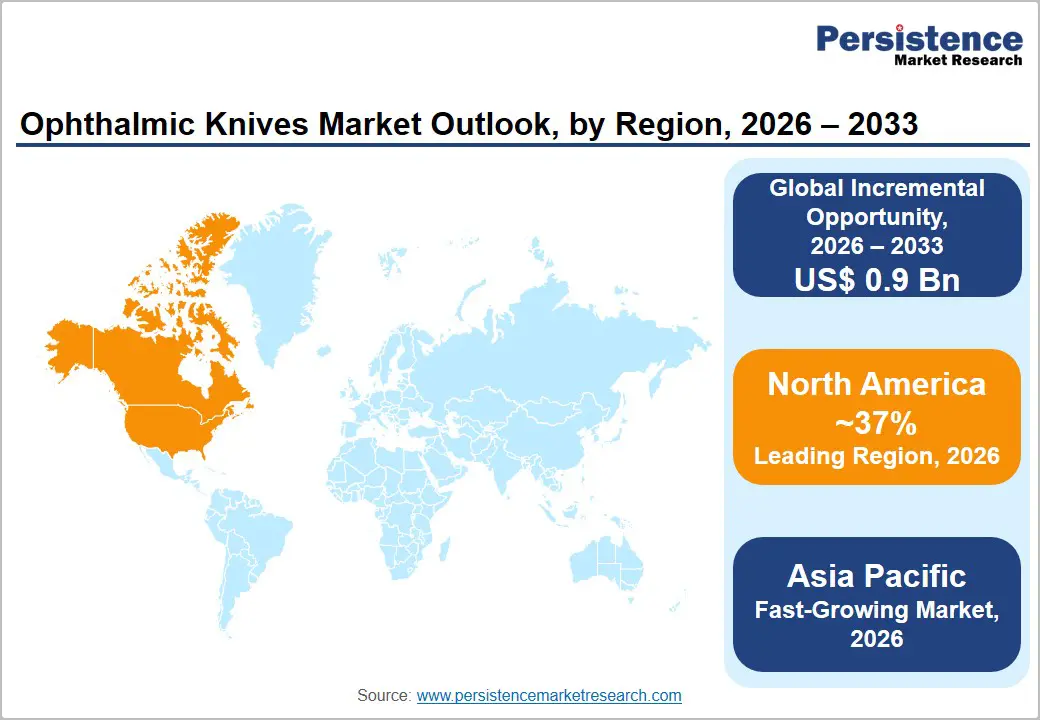

- Regional Leadership: North America is projected to capture roughly 37% of the market share by 2026, driven by advanced ophthalmic surgical infrastructure.

- Competitive Environment: The market reflects a moderately fragmented structure, with companies including Alcon, BVI Medical, and MANI Inc. driven by product precision and surgical specialization.

DRO Analysis

Driver - Rising Prevalence of Age-Related Ocular Pathologies

The systematic expansion of the global geriatric population directly correlates with escalating incidences of age-related cataracts, glaucoma, and vitreoretinal disorders. According to the World Health Organization 2025 statistical database, over 2.2 billion individuals globally experience near or distance vision impairment, with the majority concentrated in demographics aged 60 years and older. This demographic shift generates an expanding volume of essential surgical interventions globally.

The resultant procedural volume strains existing ophthalmic infrastructure, mandating high-efficiency surgical workflows. Microsurgeons require dependable instruments that minimize mechanical resistance during complex ocular penetration. Ophthalmic knives market growth remains tethered to this clinical reality, as consistent blade sharpness reduces incision-related complications like endothelial cell loss or wound leakage.

Restraint - Dependence on Specialized Manufacturing and Raw Materials

Production of ophthalmic knives requires highly specialized grinding, coating, and precision-engineering processes. Strict dimensional tolerances increase manufacturing complexity and raise production costs. Dependence on premium-grade stainless steel, diamond-coated materials, and advanced blade technologies creates supply-chain vulnerabilities that can limit scalability during periods of procurement disruption.

Extended qualification procedures for suppliers increase lead times and inventory requirements. Cost fluctuations in specialty materials can compress manufacturer margins, particularly for companies serving price-sensitive healthcare providers. Production bottlenecks may reduce responsiveness to demand surges and limit expansion opportunities.

Opportunity - Growing Adoption of Single-Use Surgical Instruments

Healthcare providers are increasing their focus on infection prevention and procedural standardization. Single-use ophthalmic knives eliminate reprocessing requirements and reduce contamination risks, creating opportunities for manufacturers to expand disposable product portfolios. Demand is particularly strong in facilities seeking improved surgical workflow efficiency and compliance with infection-control protocols.

A strategic growth pathway involves the development of premium disposable instruments with enhanced blade sharpness, ergonomic handles, and procedure-specific designs. Regulatory support for patient safety initiatives is encouraging wider acceptance of sterile, ready-to-use surgical tools. Product differentiation through advanced materials and precision manufacturing can strengthen market penetration and recurring revenue generation.

Category-wise Analysis

Design Insights

Straight knives are anticipated to secure around 31% of the ophthalmic knives market share in 2026, reflecting widespread adoption in standard anterior segment procedures due to ease of handling and consistent incision geometry. Alcon Laboratories has integrated straight knife designs into its cataract surgery instrument kits as a standard configuration. Surgeons across high-volume centers in Asia Pacific and North America continue to prefer straight blade profiles for primary corneal incisions, given their predictable tissue behavior.

MVR (Micro Vitreoretinal) knives are expected to be the fastest-growing segment, propelled by the accelerating adoption of minimally invasive posterior segment surgery and sutureless vitreoretinal procedures. DORC International has expanded its MVR knife portfolio to support 23-gauge and 25-gauge vitrectomy platforms. The shift toward smaller-gauge surgical systems in leading tertiary centers in the U.S. and Germany is reinforcing the demand for precision micro vitreoretinal blades capable of sub-millimeter incision performance.

Product Type Insights

Single-use (Disposable) ophthalmic knives are poised to dominate with a forecast market share of over 62% in 2026, powered by infection control mandates and the global adoption of evidence-based sterility protocols in ophthalmic operating environments. Beaver-Visitec International markets extensive single-use blade ranges to acute care facilities worldwide. Regulatory guidance from the U.S. FDA and the European Centre for Disease Prevention and Control reinforces single-use preference as the clinical standard in surgical settings.

Reusable ophthalmic knives are estimated to be the fastest-growing segment, fueled by cost-containment priorities in public sector ophthalmic surgical programs across low- and middle-income countries. Katena Products has developed reusable titanium blade systems validated for multiple sterilization cycles. Procurement agencies in sub-Saharan Africa and South Asia are prioritizing reusable instruments under health technology assessment frameworks that weigh lifecycle cost against single-use consumable expenditure.

Application Insights

Cataract surgery is likely to be the leading segment with a projected 43% of the ophthalmic knives market share in 2026 due to the unmatched procedural volume driven by the global cataract burden and expanding public surgical programs. Carl Zeiss Meditec supplies instrument sets including corneal incision knives specifically configured for phacoemulsification workflows. The volume density of cataract procedures relative to all other ophthalmic indications ensures this segment retains a dominant share across the forecast period.

Retinal/vitreoretinal surgery is anticipated to be the fastest-growing segment, fueled by the rising prevalence of diabetic retinopathy and age-related macular degeneration necessitating complex posterior segment interventions. Synergetics USA has positioned its MVR blade range specifically for vitreoretinal platforms adopted by leading retinal surgery centers in Japan and the United Kingdom. Demographic aging and increasing diabetes incidence are together expanding the retinal surgical caseload at a rate exceeding all other ophthalmic subspecialties.

Regional Insights

North America Ophthalmic Knives Market Trends

North America is expected to lead with an estimated 37% of the ophthalmic knives market share in 2026, supported by advanced ophthalmic surgical infrastructure, high cataract surgery volumes, widespread adoption of microsurgical technologies, and the strong presence of leading manufacturers. Growth in ambulatory ophthalmic surgery centers is increasing demand for disposable and precision-engineered ophthalmic knives.

U.S. Ophthalmic Knives Market Insights

The U.S. is projected to account for nearly 78% of North America's revenue in 2026, supported by a large ophthalmic patient base, extensive outpatient surgical networks, and rapid adoption of advanced cataract and retinal surgical technologies. FDA-approved ophthalmic innovations and strong commercialization activities from companies such as Alcon and BVI Medical are strengthening product availability and procedural efficiency.

Canada Ophthalmic Knives Market Insights

Canada is forecast to contribute approximately 14% of North America's revenue in 2026, supported by expanding access to ophthalmic care and growing demand for cataract interventions. Investments in hospital modernization and surgical efficiency programs are encouraging the adoption of disposable ophthalmic instruments. Rising focus on infection prevention is supporting the procurement of single-use surgical knives.

Europe Ophthalmic Knives Market Trends

Europe is estimated to hold approximately 29% of the ophthalmic knives market share in 2026, supported by established healthcare infrastructure, strong ophthalmology networks, and increasing adoption of minimally invasive eye surgery techniques. Regulatory standards emphasizing patient safety are encouraging the utilization of precision surgical instruments.

Germany Ophthalmic Knives Market Insights

Germany is expected to account for nearly 22% of Europe's revenue in 2026, driven by advanced surgical infrastructure, high ophthalmology procedure volumes, and continuous investment in medical technology. Expansion of vitreoretinal and cataract surgery capabilities is strengthening demand for specialized ophthalmic knives. Companies such as Geuder AG maintain a significant presence within the country.

U.K. Ophthalmic Knives Market Insights

The U.K. is projected to contribute approximately 17% of Europe's revenue in 2026, supported by growing cataract treatment demand and modernization of ophthalmology services. Expansion of outpatient surgery models is increasing utilization of disposable surgical products. Procurement strategies focused on efficiency and infection prevention continue to support demand for advanced ophthalmic knives.

Asia Pacific Ophthalmic Knives Market Trends

Asia Pacific is forecast to be the fastest-growing market for ophthalmic knives, stimulated by an estimated 25% market share in 2026, expanding healthcare infrastructure, increasing ophthalmic surgery volumes, and rising awareness of treatable visual impairment. Growth in specialized eye hospitals and government-supported blindness prevention programs is creating strong demand for ophthalmic surgical instruments.

China Ophthalmic Knives Market Insights

China is expected to account for nearly 35% of Asia Pacific revenue in 2026, supported by expanding ophthalmology infrastructure and rising cataract surgery volumes. Government healthcare investments and growth in specialized eye care facilities are increasing the utilization of ophthalmic surgical instruments. Domestic manufacturing development is improving supply availability and supporting wider adoption of precision surgical tools.

India Ophthalmic Knives Market Insights

The India market is projected to contribute approximately 18% of Asia Pacific revenue in 2026, driven by increasing eye care accessibility, growing prevalence of cataracts, and expansion of ophthalmic hospital networks. Organizations such as Aurolab and Appasamy Associates are strengthening domestic manufacturing capabilities. Rising surgical outreach initiatives are supporting long-term procedural growth.

Competitive Landscape

The global ophthalmic knives market is moderately fragmented, characterized by the presence of international ophthalmic device manufacturers and specialized surgical instrument suppliers. Competition is driven by blade precision, product quality, sterilization standards, and surgeon preference. Key participants include Alcon, BVI Medical, MANI Inc., Geuder AG, and Aurolab.

Companies focus on product innovation, manufacturing quality, and distribution expansion to strengthen competitive positioning. Strategic emphasis remains centered on disposable instruments, micro-incision technologies, and ophthalmic procedure specialization. Partnerships with surgical centers and ophthalmology institutions support product adoption while reinforcing long-term customer relationships and procurement stability.

Companies Covered in Ophthalmic Knives Market

- Alcon

- BVI Medical

- MANI Inc.

- Geuder AG

- Aurolab

- Appasamy Associates

- Surgistar

- Beaver-Visitec International

- Feather Safety Razor Co., Ltd.

- Kai Corporation

- HAI Laboratories

- Accutome

- Rumex International

- Storz Ophthalmic Instruments

- Diamatrix Ltd.

Frequently Asked Questions

The global ophthalmic knives market is projected to reach US$2.2 billion in 2026.

Rising cataract and retinal surgery volumes, driven by an aging population and increasing adoption of precision microsurgical ophthalmic procedures, are driving growth in the ophthalmic knives market.

The ophthalmic knives market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Growing adoption of single-use ophthalmic knives and increasing demand for advanced micro-incision instruments in minimally invasive eye surgeries are creating significant market opportunities.

Some of the key market players include Alcon, BVI Medical, MANI Inc., Geuder AG, and Aurolab.