- Medical Devices

- Ophthalmic Dye Market

Ophthalmic Dye Market Size, Share, and Growth Forecast, 2026 - 2033

Ophthalmic Dye Market by Product Type (Fluorescein Dye, Others), Application (Fundus Fluorescein Angiography (FFA), End-user (Hospitals, Ophthalmic Clinics, Ambulatory Surgical Centers, Diagnostic Laboratories), and Regional Analysis for 2026 - 2033

Ophthalmic Dye Market Size and Trends Analysis

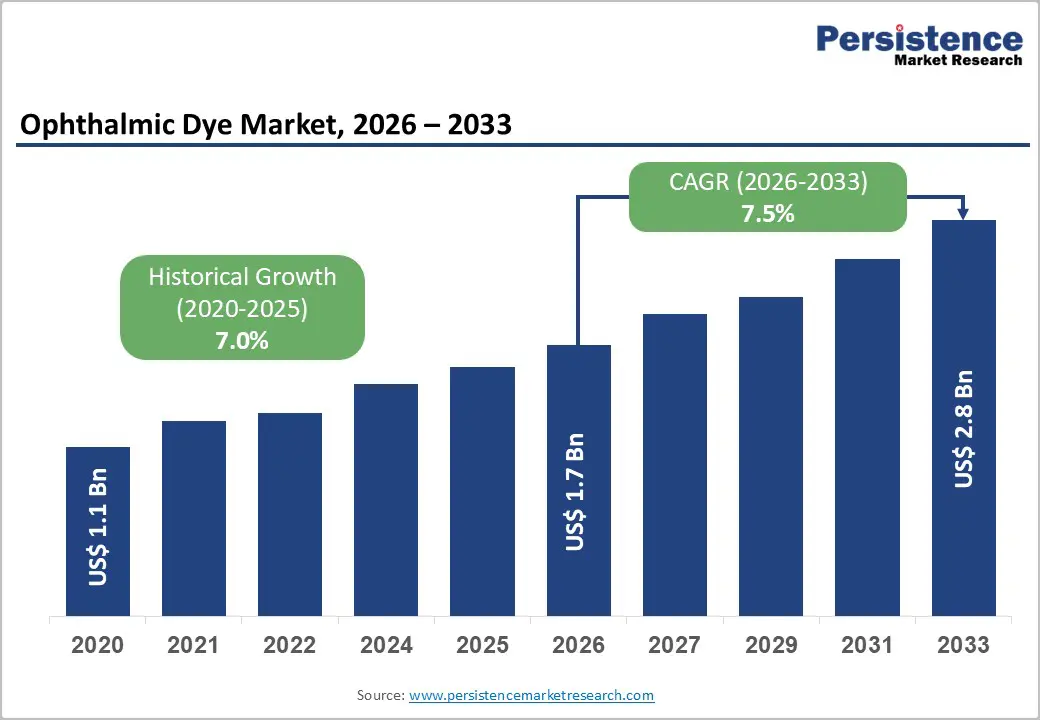

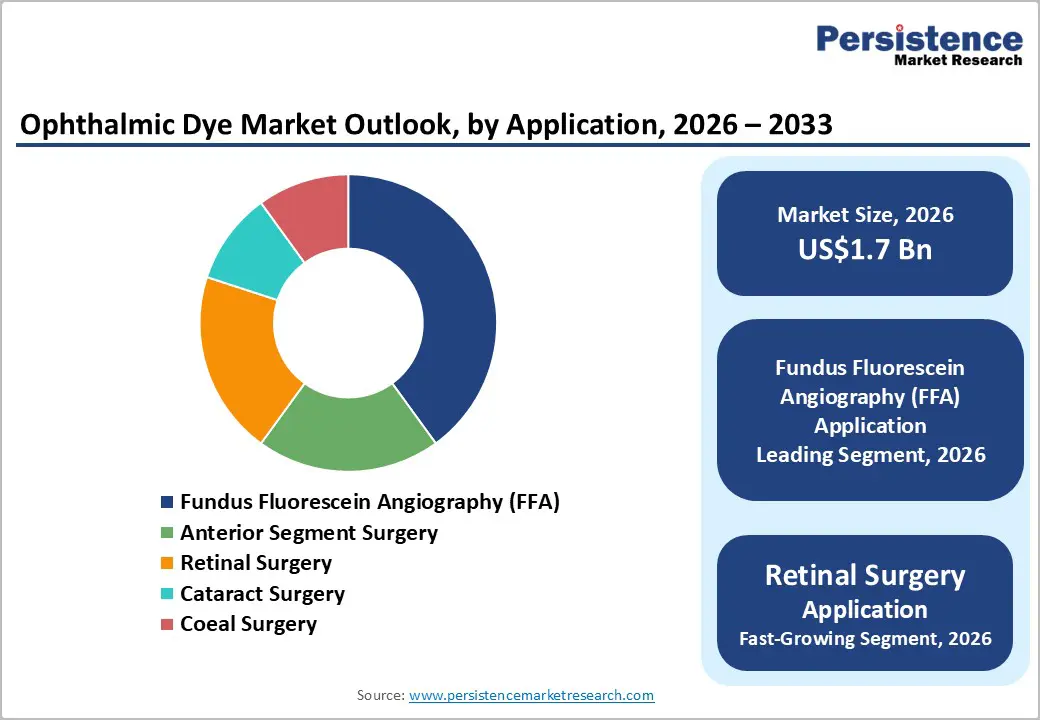

The global ophthalmic dye market size is likely to be valued at US$1.7 billion in 2026, and is expected to reach US$2.8 billion by 2033, growing at a CAGR of 7.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of retinal and corneal disorders, rising demand for precise diagnostic visualization in eye surgeries, and advancements in high-contrast fluorescein and ICG dyes.

Growing demand for reliable, biocompatible ophthalmic dye, especially in fundus fluorescein angiography (FFA) and retinal surgery, is accelerating adoption across applications. Advances in Brilliant Blue G and combination dyes are further boosting uptake by offering safer, more vivid staining. Increasing recognition of ophthalmic dye as critical for improved surgical outcomes and early diagnosis in emerging markets remains a major driver of market growth.

Key Industry Highlights:

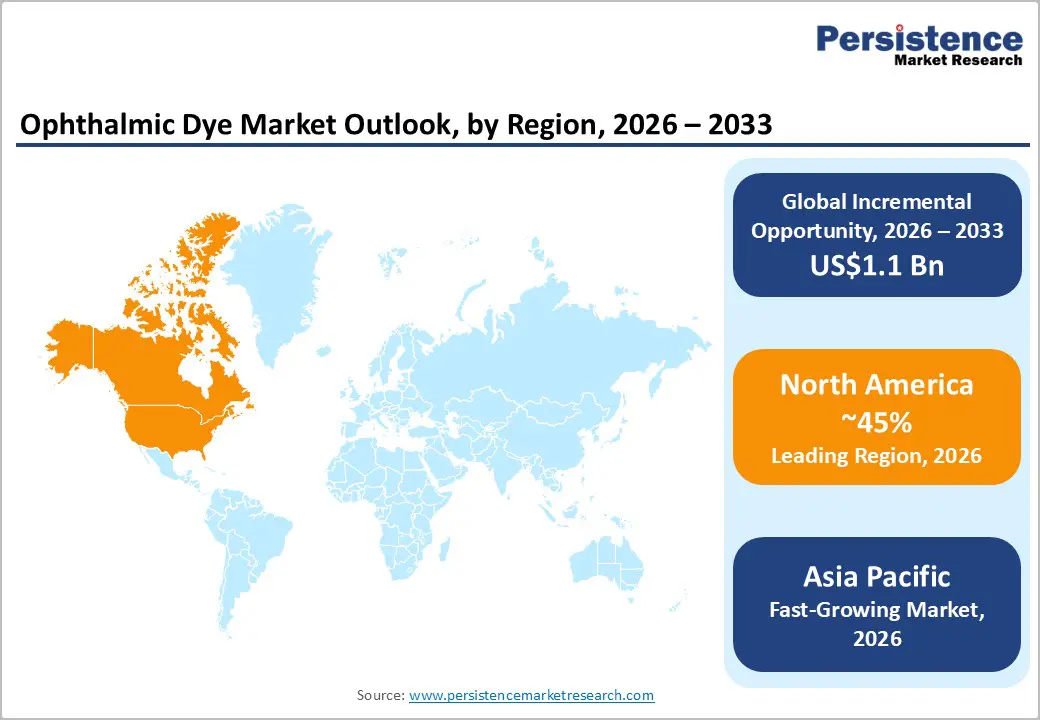

- Leading Region: North America, to account for a 45% market share in 2026, driven by advanced ophthalmic infrastructure, high diagnostic rates, and strong innovation in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising eye disease burden, expanding surgical volumes, and growing investments in eye care in China and India.

- Dominant Product Type: Fluorescein dye, to hold approximately 50% of the market share, as it is the standard for FFA and anterior segment procedures.

- Leading Application: Fundus fluorescein angiography (FFA), to account for over 40% of the market revenue, due to widespread use in retinal diagnostics.

- Leading End-user: Hospitals, to contribute nearly 45% of the market revenue in 2026, due to high surgical volumes and specialized equipment.

| Key Insights | Details |

|---|---|

| Ophthalmic Dye Market Size (2026E) | US$1.7 Bn |

| Market Value Forecast (2033F) | US$2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Retinal and Corneal Disorders

The rising prevalence of retinal and corneal disorders is becoming a major global health concern, driven by demographic, lifestyle, and environmental factors. Aging populations significantly contribute to this trend, as conditions such as age-related macular degeneration, diabetic retinopathy, and cataract-related corneal complications become more common with advancing age. The increasing incidence of diabetes and hypertension worldwide has led to a higher burden of retinal diseases, particularly diabetic retinopathy, which can result in vision impairment if not managed early.

Lifestyle changes also play a crucial role. Prolonged screen exposure, reduced outdoor activities, and increased digital device usage contribute to eye strain, dry eye syndrome, and corneal surface damage. Urbanization and air pollution further aggravate ocular surface disorders, increasing the risk of corneal inflammation and infections. The widespread use of contact lenses, especially without proper hygiene, has raised the incidence of corneal abrasions and microbial keratitis. Limited access to timely eye care in developing regions exacerbates disease progression, leading to higher rates of preventable vision loss.

High Development and Regulatory Costs

High development and regulatory costs present a significant barrier for companies advancing next-generation ophthalmic dyes and novel formulations. Developing innovative grades such as high-contrast ICG, low-toxicity Brilliant Blue G, or multi-modal dyes requires extensive research, biocompatibility testing, and advanced synthesis technologies that are far more expensive than standard fluorescein. Safety is an even greater challenge: many refined variants, low-irritant lots, and stability-enhanced products are sensitive to pH, light degradation, and tissue toxicity, requiring rigorous optimization to ensure they remain safe throughout use. Achieving long-term performance often involves costly clinical trials, sophisticated HPLC testing, and the use of high-grade precursors, which significantly increase R&D expenditures.

Meeting stringent regulatory expectations for ocular safety, sterility, and batch consistency requires multiple validation studies under various conditions and across several patient cohorts. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled sterile facilities, specialized filling lines, and quality-assurance systems, further driving up overall costs. For smaller players, these challenges can limit innovation or delay commercialization.

Developments in High-Contrast and Low-Toxicity Delivery Platforms

Developments in high-contrast and low-toxicity ophthalmic dye delivery platforms are transforming the global eye care landscape by addressing two major challenges, visualization barriers and safety concerns. High-contrast platforms are engineered to achieve vivid staining, reducing reliance on high doses and enabling clearer intraoperative views. Innovations, such as nanoparticle encapsulation, fluorescent tagging, pH-sensitive release, and combination dyes, significantly improve contrast and reduce toxicity, lowering surgical risks for providers and patient campaigns.

Progress in low-toxicity platforms, including non-irritant fluorescein, biodegradable ICG, safe Brilliant Blue G, and dye-free alternatives, supports more patient-friendly procedures by minimizing inflammation, the therapy’s first line of defense against complications. These formats eliminate adverse reactions, enhance recovery, and allow versatile use without prolonged exposure, making them highly suitable for mass cataract programs. New technologies such as bio-adhesive dyes, VLP-based carriers, and AI-guided dosing further enhance precision and response.

Category-wise Analysis

Product Type Insights

Fluorescein dye is anticipated to dominate the market, accounting for approximately 50% of the market share in 2026. Its dominance is driven by established use in FFA, high visibility, and cost-effectiveness, making it preferred for retinal diagnostics. Fluorescein dye provides rapid staining, ensures clarity, and contributes to reliability, making it suitable for large-scale diagnostic campaigns. Guangzhou Baiyunshan Mingxing Pharmaceutical Co. Ltd., a leading pharmaceutical manufacturer in China, produces fluorescein sodium injection used extensively in fundus fluorescein angiography (FFA) for retinal diagnostics. In clinical studies, sodium fluorescein from this company has been used to obtain high-contrast angiograms of retinal and choroidal vasculature, helping ophthalmologists assess conditions such as diabetic retinopathy and macular degeneration with clear visualization and rapid staining during imaging procedures.

Indocyanine green (ICG) represents the fastest-growing segment, due to its deep tissue penetration and expanding use in retinal surgery. Its vascular profile makes it ideal for targeted choroidal imaging, reducing diagnostic errors. Continuous innovations in formulation are further strengthening its appeal, driving rapid adoption across North America and Europe, where demand for advanced imaging is accelerating. Diagnostic Green GmbH is a prominent manufacturer of Indocyanine Green (ICG) diagnostic dye sold under the brand name IC-Green® in the U.S. and Verdye in Europe, widely used in advanced ophthalmic diagnostics. ICG’s near-infrared fluorescence properties allow deeper penetration through retinal layers and better visualization of the choroidal circulation compared with fluorescein, making it particularly valuable for imaging conditions such as choroidal neovascularization and macular degeneration.

Application Insights

Fundus fluorescein angiography (FFA) is anticipated to lead the market, holding approximately 40% of the share in 2026, driven by diagnostic needs, large retinal programs, and strong global demand for vascular mapping. Their dominance continues as screening expands. Rising adoption of retinal surgery and expanded cataract campaigns highlight the growing focus on multi-application benefits. Carl Zeiss Meditec, Inc., a leading manufacturer of ophthalmic imaging technology, is widely used in fundus fluorescein angiography (FFA) systems deployed in large hospital retinal screening programs and specialty eye clinics worldwide. Zeiss FFA units, such as those integrated into multi-modality fundus cameras, provide high-resolution vascular mapping that helps clinicians diagnose and monitor diabetic retinopathy, age-related macular degeneration, and other retinal vascular diseases.

Retinal surgery is the fastest-growing segment, due to strong momentum in intraoperative use and expanding inclusion in macular procedures. The growing shift toward visualization platforms, along with better outcomes, accelerates the adoption. Advancements in ICG staining and the continued progress of Brilliant Blue G entering surgical trials drive market growth. DORC International demonstrates how advancements in surgical dyes, such as Brilliant Blue G, are strengthening intraoperative capabilities for retinal surgeons and supporting the fastest-growing status of the retinal surgery market segment due to improved visualization, better outcomes, and broader clinical adoption.

End-user Insights

Hospitals are projected to dominate the market in 2026, accounting for nearly 45% of revenue, as they continue to serve as the primary centers for surgical procedures, comprehensive ophthalmic programs, and management of diverse patients requiring dye-enhanced imaging. Their robust integration, highly trained surgeons, and capacity to manage high-volume or complex cases drive higher utilization. Hospitals are at the forefront of FFA implementations and play a leading role in administering emerging retinal clinical trials. For example, the Bascom Palmer Eye Institute (University of Miami Health System) is consistently ranked among the top ophthalmology hospitals worldwide, treating hundreds of thousands of patients annually, including those with complex retinal diseases needing dye-based imaging such as fundus fluorescein angiography (FFA) and indocyanine green angiography (ICG) for vascular mapping and surgical planning. Its specialized retinal services routinely integrate advanced imaging systems for diagnosing diabetic retinopathy, macular degeneration, and other posterior segment disorders, illustrating how major hospitals remain the central hub for high-volume ophthalmic diagnostics and surgeries.

Ophthalmic clinics represent the fastest-growing segment, fueled by their strong outpatient presence and expanding role in diagnostic imaging. They offer convenient, rapid, and accessible procedures, appealing to patients who prefer specialized care with minimal waiting times. Increased outreach initiatives, screening programs, and broader availability of both routine and premium dyes further accelerate adoption, driving growth across urban and semi-urban areas. Optegra Eye Care Clinics, a large network of ophthalmic outpatient facilities across the UK, the Czech Republic, Poland, Slovakia, and the Netherlands, provides accessible eye care services, including retinal imaging, OCT scans, and fluorescein angiography as part of routine diagnostic screenings. Clinics such as Optegra’s are rapidly expanding, delivering advanced imaging in quick, outpatient settings that attract patients seeking specialized care without the delays typically associated with hospitals.

Regional Insights

North America Ophthalmic Dye Market Trends

North America is projected to lead the ophthalmic dye market, accounting for nearly 45% of the global share in 2026. This growth is supported by the region’s advanced eye care infrastructure, robust research and development capabilities, and high public awareness of the diagnostic advantages of ophthalmic dyes. In the U.S. and Canada, treatment systems offer extensive support for imaging programs, ensuring broad accessibility of dyes across fluorescein angiography (FFA), retinal surgery, and cataract procedures. Rising demand for high-contrast, convenient, and easy-to-use formulations is further driving adoption, as these formats enhance precision and reduce the limitations associated with traditional methods.

Technological innovations, such as stable indocyanine green (ICG), improved delivery of Brilliant Blue G, and targeted visualization enhancements, are attracting substantial investment from both public and private sectors. Government initiatives and Medicare campaigns continue to encourage their use to mitigate diagnostic delays, surgical risks, and emerging retinal conditions, sustaining market demand. The increasing emphasis on retinal grading and specialized applications, particularly in corneal procedures, is expanding the potential uses for ophthalmic dyes.

Europe Ophthalmic Dye Market Trends

Europe’s ophthalmic dye market is driven by rising awareness of diagnostic benefits, strong healthcare infrastructure, and government-supported eye care programs. Countries such as Germany, France, and the U.K. have well-established systems that facilitate routine dye use and promote the adoption of innovative delivery methods. High-contrast formulations are particularly valued by retinal specialists, regulation-conscious practitioners, and cataract care providers, enhancing clinical outcomes and coverage rates.

Advances in ophthalmic dye technology, including improved stability, targeted delivery, and enhanced safety profiles, are further expanding market opportunities. European authorities are increasingly backing research and clinical trials for both routine and specialized applications, reinforcing confidence in the market. The region’s focus on preventive eye care and complication reduction aligns with the growing demand for convenient, low-toxicity options. Public awareness campaigns are broadening reach across urban and rural populations, while suppliers are investing in novel formulations and synthesis methods to improve efficacy and performance.

Asia Pacific Ophthalmic Dye Market Trends

Asia Pacific is set to be the fastest-growing ophthalmic dye market in 2026, fueled by increasing awareness of eye disorders, expanding government initiatives, and the growth of application programs across the region. Countries including India, China, Japan, and Southeast Asian nations are actively promoting dye use to address rising cataract prevalence and emerging retinal conditions. Ophthalmic dyes are particularly appealing in these markets due to their cost-effectiveness, scalability, and suitability for large-scale surgical programs in both urban and rural settings.

Technological innovations are driving the development of stable, effective, and user-friendly ophthalmic dyes capable of performing under challenging conditions while minimizing toxicity. These advancements are essential for extending access to remote facilities and improving overall visualization outcomes. Rising demand across fluorescein angiography (FFA), retinal surgery, and cataract applications is further supporting market growth. Public-private partnerships, increased eye care spending, and investments in research and production capacity are accelerating adoption. The combination of convenient delivery, enhanced contrast, and reduced complication risks reinforces ophthalmic dyes as a preferred choice in the region.

Competitive Landscape

The global ophthalmic dye market features competition between established pharma leaders and specialized eye care companies. In North America and Europe, Novartis AG and Alcon lead through strong R&D, distribution networks, and clinical ties, bolstered by innovative grades and diagnostic programs. In Asia Pacific, local suppliers advance with localized solutions, enhancing accessibility. High-contrast delivery boosts visualization, cuts surgical risks, and enables mass integration across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Low-toxicity formulations solve safety issues, aiding penetration in sensitive areas.

Key Industry Developments

- In October 2025, EssilorLuxottica announced the successful acquisition of Optegra from MidEuropa. Operating under the Optegra, Lexum, and Iris brands, Optegra is a rapidly growing, fully integrated ophthalmology platform, managing a network of more than 70 eye hospitals and diagnostic centers across five major European markets: the U.K., the Czech Republic, Poland, Slovakia, and the Netherlands.

- In June 2025, the L V Prasad Eye Institute (LVPEI) at the Mithu Tulsi Chanrai (MTC) campus in Bhubaneswar inaugurated a dedicated Inherited Retinal Dystrophy (IRD) Clinic to provide specialized care for patients with genetic retinal disorders. The clinic offers in-house genetic testing, enhancing access to advanced diagnostics for patients across Odisha and neighboring states, and helping bridge gaps in the early diagnosis and management of hereditary eye diseases in the region.

- In April 2025, Bausch + Lomb announced the US launch of Arise, a lens fitting system that uses intelligent, cloud-based technology to streamline the orthokeratology lens design process. Arise syncs directly with topographers to create precise lens designs in seconds to treat myopia. These lenses include the first orthokeratology lens design with toric peripheral curves approved by the FDA to treat myopia overnight.

Companies Covered in Ophthalmic Dye Market

- Novartis AG

- Alcon

- Bausch Health Companies Inc.

- Santen Pharmaceutical Co. Ltd.

- Akorn Inc.

- Heidelberg Engineering Inc.

- Hoya Corporation

- Carl Zeiss Meditec AG

- Fluoron GmbH

- Acucela Inc.

- Vitreq B.V.

- Haag-Streit AG

- Oculus Surgical Inc.

- Medicel AG

- Oculus Optikgeräte GmbH

- Altaire Pharmaceuticals Inc.

- Johnson & Johnson

- HUB Pharmaceuticals, LLC

- Topcon Corporation

- Nomax Inc.

Frequently Asked Questions

The global ophthalmic dye market is projected to reach US$1.7 billion in 2026.

The ophthalmic dye market is primarily driven by the increasing prevalence of retinal and corneal disorders, coupled with the growing demand for accurate and precise diagnostic visualization.

The ophthalmic dye market is poised to witness a CAGR of 7.5% from 2026 to 2033.

The ophthalmic dye market presents significant opportunities through the development of high-contrast, low-toxicity ophthalmic dye delivery platforms.

Alcon, Novartis AG, Bausch Health Companies Inc., Santen Pharmaceutical Co. Ltd., and Carl Zeiss Meditec AG are the key players.