- Specialty & Fine Chemicals

- Nitro Aromatics Market

Nitro Aromatics Market Size, Share, and Growth Forecast 2026 - 2033

Nitro Aromatics Market by Product Type (Nitrobenzene, Nitrochlorobenzene, Dinitrotoluene, Other), Application (Explosives, Agrochemicals, Fertilizers, Dyes & Pigments, Pharmaceuticals, Other), and Regional Analysis for 2026-2033

Nitro Aromatics Market Size and Trend Analysis

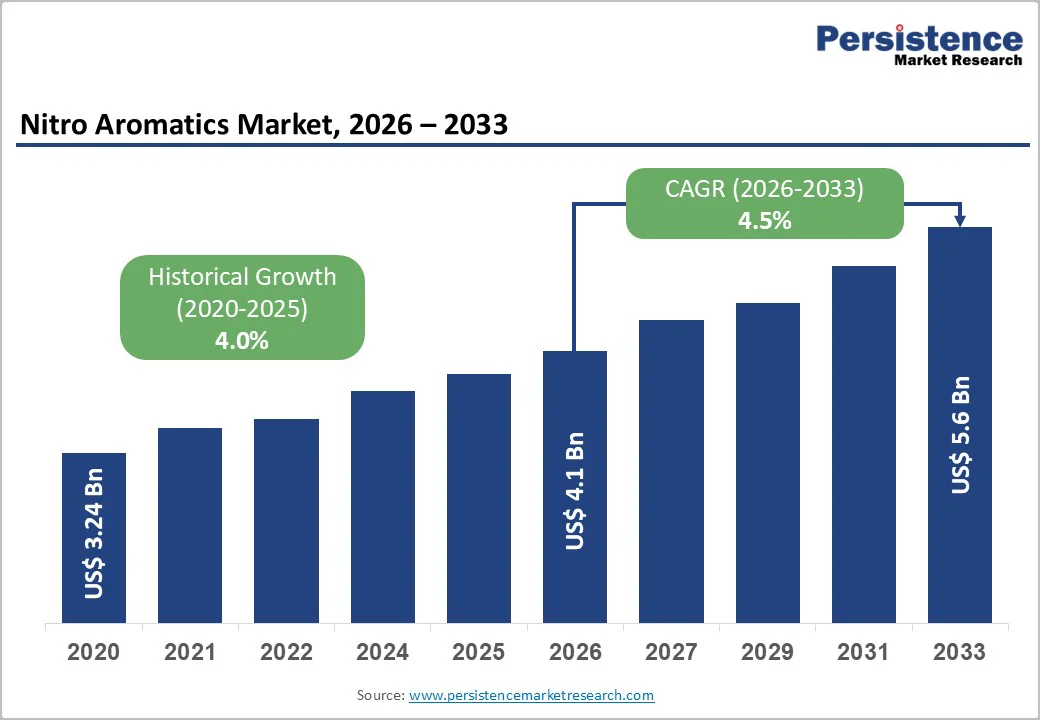

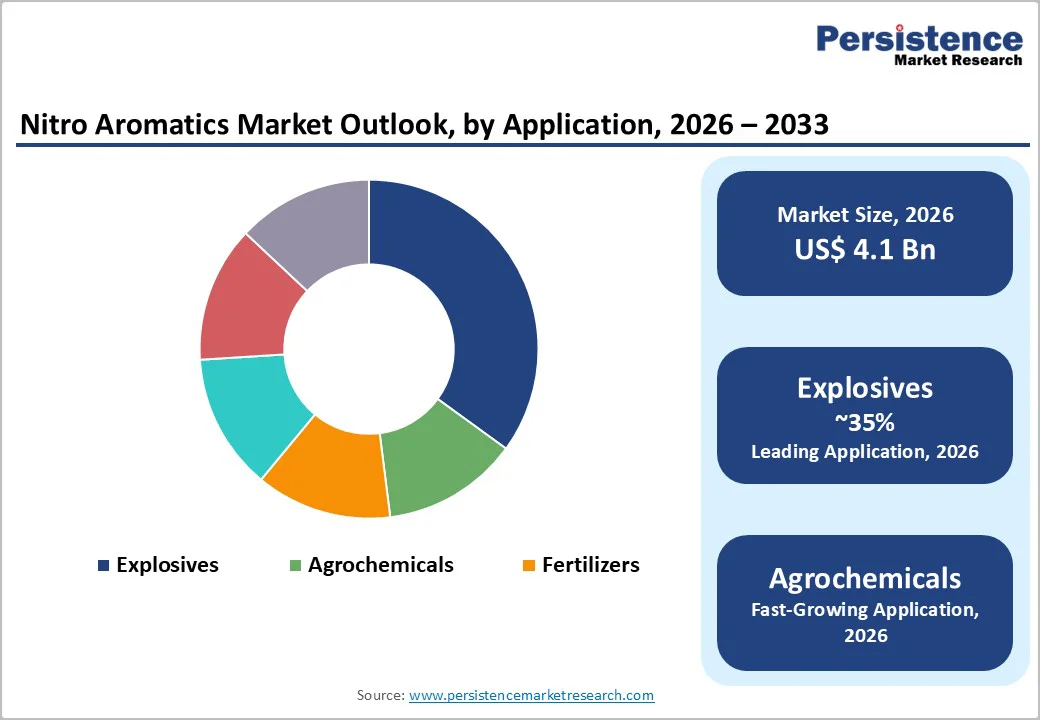

The global Nitro Aromatics market size is supposed to be valued at US$ 4.1 Bn in 2026 and is projected to reach US$ 5.6 Bn by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

The market expansion is driven by rising demand from the polyurethane and agrochemical sectors, particularly in emerging economies, where accelerating infrastructure development is increasing industrial consumption. Additionally, the growing pharmaceutical and dye industries continue to leverage nitro aromatics as essential intermediates for complex molecular synthesis, supported by technological advancements in manufacturing processes that enhance production efficiency and reduce environmental impact.

Key Market Highlights

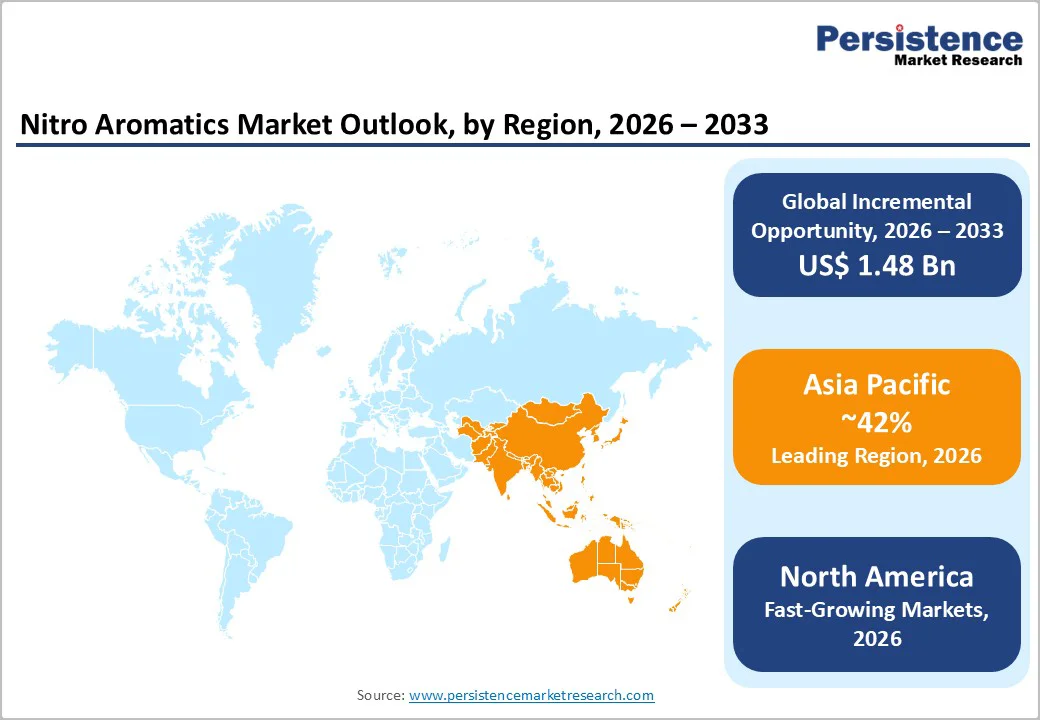

- Leading Region: Asia-Pacific dominates the global Nitro Aromatics market, accounting for 42% of global market share, driven by rapid industrialization, expansive infrastructure investments, and cost-effective manufacturing capabilities. China produces over 50% of global aniline, and India is emerging as a critical growth market.

- Fastest-Growing Region: North America has the fastest projected growth rate for Nitrobenzene applications, driven by expanding building and automotive sectors, robust demand for pharmaceutical intermediates, and strategic investments in sustainable manufacturing technologies.

- Dominant Segment: Nitrobenzene accounts for approximately 40% of the total nitro-aromatics market value, driven by its essential role in aniline production for polyurethane, dyes, pharmaceuticals, and agrochemical applications.

- Fastest-Growing Segment: Agrochemicals are the fastest-growing application segment, driven by global population growth requiring enhanced crop productivity, climate change-induced pest and disease pressures, adoption of precision agriculture, and increasing investments in modern farming practices across developing nations.

- Key Market Opportunity: Asia-Pacific infrastructure mega-projects and military modernization programs present substantial opportunities for explosives-grade nitro-aromatic manufacturers, with defense budget increases guaranteeing sustained demand throughout the forecast period.

| Key Insights | Details |

|---|---|

| Nitro Aromatics Market Size (2026E) | US$ 4.1 Bn |

| Market Value Forecast (2033F) | US$ 5.6 Bn |

| Projected Growth CAGR (2026-2033) | 4.5% |

| Historical Market Growth (2020-2025) | 4.0% |

Market Dynamics

Market Growth Drivers

Expanding Polyurethane Foam Manufacturing and Construction Boom

Nitro aromatics, particularly nitrobenzene and dinitrotoluene (DNT), serve as critical intermediates in polyurethane production, with MDI (methylene diphenyl diisocyanate) being the predominant isocyanate utilized in foam synthesis. Asia Pacific's rapid urbanization is a pivotal growth driver, with countries like China accounting for approximately 66% of the Asia-Pacific polyurethane market, supported by its extensive manufacturing infrastructure and massive construction activities. India is positioned to become the third-largest construction market by 2030 due to government initiatives promoting affordable housing and smart city projects, while China's construction industry accounts for 25%- 33% of global construction output.

The demand for energy-efficient building materials, driven by initiatives such as LEED certification and India's ECBC norms, creates sustained demand for rigid polyurethane insulation foams containing nitro aromatic intermediates. Furthermore, the burgeoning e-commerce sector, which accounted for USD 28.08 trillion in B2B transactions globally in 2024, necessitates protective packaging solutions utilizing polyurethane foams.

Pharmaceutical and Agrochemical Innovation

The global pharmaceutical market continues to expand, with paracetamol, the world's most widely used medicine, synthesized from nitrobenzene, which is reduced to aniline, a critical intermediate in pharmaceutical formulations. China, Germany, and India are the leading countries in paracetamol manufacturing, with India emerging as a major pharmaceutical production hub for both branded and generic medicines. The aniline derivatives market is driven by expanding applications in textiles, automotive, and pharmaceutical sectors.

Furthermore, the global agrochemicals market is experiencing strong growth, with nitrogen fertilizers, herbicides, and fungicides representing key applications for nitro compounds. Countries in the Asia-Pacific, particularly China, India, and Indonesia, are increasing investments in agricultural modernization, with precision agriculture adoption expected to grow by 20% over the next five years, thereby escalating the consumption of nitroaromatic-based pesticides and fungicides.

Market Restraints

Stringent Environmental and Regulatory Compliance

The production and use of nitro aromatics face escalating regulatory scrutiny globally, particularly in developed regions that implement the European Union's REACH Regulation, which mandates comprehensive safety data and risk assessment for chemical substances exceeding 1 tonne per year per company. Nitroaromatic compounds, including 2,4-dinitrotoluene (2,4-DNT), are designated as EPA Priority Pollutants with strict soil screening levels of 1.6 mg/kg for residential and 5.5 mg/kg for industrial use, and stringent groundwater risk-based screening levels of 2.8 × 10 mg/kg.

The U.S. Environmental Protection Agency has implemented rigorous VOC emission standards under 40 CFR 59, with state-level regulations such as those in California imposing even stricter controls through CARB standards. Compliance with these regulations necessitates substantial capital investments in advanced waste treatment technologies, including wet air oxidation systems and environmental monitoring infrastructure, thereby increasing operational costs for manufacturers. The persistence of nitro aromatic residues in soil and groundwater at contaminated munitions manufacturing sites and military installations across the United States, encompassing more than 24 million acres, creates long-term environmental liabilities and potential corporate accountability challenges.

Volatility in Raw Material Costs and Supply Chain Disruptions

The production of nitro aromatics fundamentally depends on stable supplies of benzene, toluene, and xylene (BTX aromatics), as well as on critical chemical inputs, including nitric acid and chlorobenzene, whose prices are subject to considerable fluctuations in the petroleum market. During Q4 2024, PNCB (para-nitro chloro benzene) prices in China declined to USD 988/MT, reflecting a 4.82% drop from Q3, while in September 2025, prices fell an additional 7.29%, driven by subdued international inquiries and elevated inventory levels. The global supply chain disruptions precipitated by geopolitical tensions and pandemic-related logistics challenges have constrained the reliable availability of specialty chemicals.

Manufacturing facilities require sophisticated engineering capabilities for nitration, chlorination, and hydrogenation processes, limiting the number of capable producers globally. The historical production concentrations in China, India, Europe, and the United States create geographic risks, as supply disruptions in any major region can significantly affect global availability and pricing, particularly for downstream customers in the pharmaceuticals and agrochemicals sectors that rely on just-in-time inventory models.

Market Opportunities

Rising Demand from the Electric Vehicle and Battery Manufacturing Sectors

The global electric vehicle market represents an extraordinary growth opportunity for nitro aromatic manufacturers, with China alone accounting for over 55% of global EV production, supported by aggressive government incentives and the expansion of battery manufacturing facilities. The polyurethane foam applications in EV battery thermal insulation, acoustic control, and lightweight interior components are rapidly expanding, creating incremental demand for MDI-based systems derived from nitro aromatic intermediates. India's electric vehicle market is experiencing exponential growth driven by government mandates and corporate commitments to sustainable mobility, with investments in charging infrastructure and battery manufacturing plants proliferating across major industrial zones.

The rise of lithium-ion battery production, where polyurethane foams provide critical thermal management and structural support, directly correlates with increased consumption of MDI and aniline-based polyols. Industry leaders such as Wanhua Chemical have announced ambitious expansion plans, with the company planning to add 400,000 tons/year MDI production capacity in the United States while maintaining its position as the global leader with potential capacity exceeding 35% of global market share. Furthermore, renewable energy systems, including solar panels and wind turbine components, increasingly use polyurethane foams for insulation and structural applications, creating demand streams beyond the traditional automotive and construction sectors.

Transition Toward Bio-Based and Sustainable Nitro Compound Production

The chemical industry is experiencing a paradigm shift toward sustainability, with major manufacturers investing in renewable feedstock technologies and green chemistry initiatives to address environmental concerns and regulatory pressures. Bio-based alternatives to conventional nitro aromatics, derived from lignocellulosic biomass, agricultural waste, and non-food feedstocks, are being developed through advanced processes including catalytic fast pyrolysis and Diels-Alder cycloaddition reactions. The European Union's Green Building Standards and government incentives, such as LEED certification programs and Brazil's World Bank-supported sustainable construction initiatives, are creating premium market segments for eco-friendly chemical products.

Manufacturers implementing bio-based polyols and low-VOC formulations can capture growing market share among environmentally conscious customers in North America and Europe, where sustainability credentials provide competitive advantages and command price premiums. The pharmaceutical and personal care industries are increasingly demanding sustainably sourced chemical intermediates, and companies are implementing blockchain-based supply chain transparency to ensure ethical sourcing and manufacturing practices.

Category-wise Insights

Product Type Analysis

Nitrobenzene commands the largest market share among nitro aromatic product types, estimated at approximately 40% of the global market, driven by its critical role as a precursor for aniline production, which serves multiple high-value downstream industries. Nitrobenzene's utilization as a solvent in cellulose ether processing, metal polishing, floor treatments, and shoe polish formulations provides diverse non-aniline application channels, ensuring consistent baseline demand. The synthesis pathway from nitrobenzene to aniline derivatives has achieved industrial maturity with highly optimized catalytic hydrogenation processes, enabling cost-competitive production across Asia-Pacific, Europe, and North America.

Wanhua Chemical, the global market leader in MDI production with a capacity of 3.5 million tons per year, has aggressively expanded nitrobenzene and related intermediate capacity, with completion of capacity build-up at its Yantai facility in March 2025. BASF, Covestro, and Huntsman have similarly invested in expanding nitrobenzene production to support downstream aniline and MDI manufacturing, reflecting sustained structural demand from automotive lightweighting and energy-efficient building standards.

Application Analysis

The explosives segment maintains the largest application share within the nitro aromatics market, accounting for approximately 35% of total consumption, driven by sustained defense spending and military modernization programs globally. Dinitrotoluene (DNT) and trinitrotoluene (TNT) are essential explosive compounds used in military munitions, artillery shells, missiles, and controlled demolition applications, with demand fluctuating with geopolitical tensions and defense budgets. North America accounts for approximately 40% of the global military explosives market, with the United States government substantially increasing defense expenditure to develop advanced propulsion systems and weaponry.

The Asia-Pacific region is expected to dominate TNT production and consumption during the forecast period, with India, China, and Japan significantly increasing defense spending to strengthen national security and counter emerging threats. The double-base propellant segment, comprising nitrocellulose and nitroglycerin derivatives, is experiencing the fastest growth due to superior performance characteristics that deliver higher energy output than single-base formulations, making it essential for next-generation military applications.

Regional Insights

North America Nitro Aromatics Trends

North America emerges as a mature and strategically significant market for nitro aromatics, with the United States accounting for nearly 30% of global nitro aromatics consumption in 2023. The region's chemical manufacturing infrastructure is concentrated in Louisiana's petrochemical corridor, where major producers have established integrated facilities combining nitration, hydrogenation, and chemical synthesis capabilities. BASF's Geismar, Louisiana, facility is undergoing substantial expansion, with completion of the third-stage MDI production capacity expansion projected by 2025, increasing total MDI production by approximately one-third through upstream unit enhancements.

The pharmaceutical sector is a dominant application driver, with paracetamol production facilities major consumers of nitrobenzene and aniline derivatives, supported by North America's stringent FDA regulations that ensure product quality and supply chain reliability. The defense sector contributes substantially to explosives demand, with U.S. government defense budgets supporting production of munitions containing dinitrotoluene and other nitro aromatics for military modernization initiatives.

Europe Nitro Aromatics Trends

Europe represents a well-established market characterized by stringent regulatory frameworks and advanced manufacturing capabilities, particularly in Germany, France, and the United Kingdom. The European basic chemical, fertilizer, and nitrogen compound manufacturing industry is showing robust industrial growth, underpinning nitroaromatic consumption. Germany leads European production and consumption, leveraging its world-class chemical infrastructure and BASF's extensive operations, which include integrated nitration and isocyanate production facilities.

The European Union's REACH Regulation mandates comprehensive chemical safety assessments and limits on substances of very great concern, driving investment in sustainable production technologies and bio-based alternatives. The pharmaceutical and dyes industries remain significant consumers, with Europe's traditional textile and leather sectors supporting steady demand for nitro aromatic-derived dyes and pigments.

Asia-Pacific Nitro Aromatics Trends

Asia-Pacific dominates global nitro aromatics production and consumption, with 42% market share. China maintains preeminence through its vast manufacturing base, cost-competitive production, and substantial downstream industry integration. The Wanhua Chemical Group, headquartered in China, has emerged as the global MDI leader with current production capacity of 2.3 million tons/year and planned expansions reaching 4.85 million tons/year, positioning the company to exceed 35% of global market share upon project completion.

India is the fastest-growing market in the region, driven by rapid industrialization, government initiatives promoting manufacturing through the "Make in India" program, and expanding applications across the agrochemicals, pharmaceuticals, and dyes sectors. Aarti Industries Limited, a leading Indian specialty chemical manufacturer, commands a market share of approximately 25-40% for its nitro aromatic product categories and has commissioned new nitro toluene production facilities with 400 crore rupees sales potential, while securing multi-year contracts valued at 40,000 crore rupees with global agrochemical companies.

Competitive Landscape

The global nitro aromatics market exhibits a moderately concentrated competitive structure, characterized by the dominance of a few multinational chemical conglomerates controlling substantial production capacity alongside a significant number of regional and specialty chemical manufacturers. Market differentiation strategies emphasize process chemistry expertise, with companies such as Aarti Industries leveraging specialization in nitration, chlorination, and hydrogenation technologies to serve global customers across 60 countries. The competitive environment is being reshaped by sustainability imperatives, with leading companies investing in bio-based production technologies, low-VOC formulations, and circular economy initiatives to comply with environmental regulations and capture premium-priced market segments.

Key Market Developments

- March 2025: Wanhua Chemical completed capacity build-up for nitrobenzene and MDI production at its Yantai facility, supporting polyurethane raw material supply across Asia-Pacific and global markets.

- February 2025: Covestro AG announced strategic research and development projects focused on developing low-emission nitrobenzene derivatives, advancing sustainable chemistry practices and circular economy integration.

- December 2024: BASF's Chongqing polyurethane MDI optimization project entered the trial operation phase, with plans to expand nitrobenzene and related intermediate facilities to enhance production efficiency.

Top Companies in Nitro Aromatics Market

Wanhua Chemical Group Co., Ltd. (China) operates as the global leader in MDI production with integrated capacity of 4.2 million tons per year and substantial aniline and nitrobenzene production facilities. The company maintains strategic geographic diversification across China, supporting both domestic demand and international export markets. Wanhua's technological leadership in polyurethane intermediate manufacturing and aggressive capacity expansion strategy position it to capture disproportionate market share gains.

BASF SE (Germany) operates an integrated global chemical production network with MDI capacity of 2.02 million tons per year distributed across Europe, North America, and Asia-Pacific. The company maintains technological leadership in sustainable manufacturing and continues strategic investments in low-emission production processes.

Covestro AG (Germany) manages 1.77 million tons per year of MDI production capacity and has announced targeted investments in specialty chemical development and sustainable production innovation. The company's strategic focus on circular economy integration and differentiated product offerings positions it competitively within premium market segments.

Companies Covered in Nitro Aromatics Market

- BASF SE

- Huntsman Corporation

- Wanhua Chemical Group Co., Ltd.

- Covestro AG

- Dow Inc.

- SABIC

- Mitsubishi Chemical Company

- LG Chem

- Eastman Chemical Company

- Chemours Company

- Aarti Industries Ltd.

Frequently Asked Questions

The global Nitro Aromatics market is projected to reach US$ 5.6 Bn by 2033, growing from US$ 4.1 Bn in 2026 at a CAGR of 4.5%, driven by sustained demand from mining, construction, agrochemical, and pharmaceutical industries across developed and emerging markets.

Primary demand drivers include escalating mining and construction activities requiring explosives (representing 34% of DNT market share), rising agrochemical consumption driven by 70% global pesticide usage increase, pharmaceutical industry growth with nitrochlorobenzene capturing 38.6% of pharmaceutical intermediate demand, and accelerating infrastructure development in Asia-Pacific.

Nitrobenzene commands the leading product segment, capturing approximately 40% market share, owing to its critical role as the primary intermediate for aniline production, which serves diverse downstream industries including pharmaceuticals, dyes, polymers, and agrochemicals with established industrial-scale manufacturing processes.

Asia-Pacific dominates the global Nitro Aromatics market with 42% market share, driven by rapid industrialization, unprecedented infrastructure investments, low-cost manufacturing advantages, China's dominance in producing over 50% of global aniline, and emerging pharmaceutical manufacturing hubs in India.

Electric vehicle battery manufacturing and thermal management systems represent the most compelling growth opportunity, with China producing 55% of global EVs and battery production expanding rapidly, creating escalating demand for MDI-based polyurethane foams used in thermal insulation, acoustic control, and lightweight interior components.

Leading market players include Wanhua Chemical Group, BASF SE, Covestro AG, Huntsman Corporation, Dow Inc., and Aarti Industries Ltd.