- Industrial Machinery

- Mud Valves Market

Mud Valves Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Mud Valves Market by Product Type (Gate Valves, Globe Valves, Butterfly Valves, Ball Valves, Others), Application (Oil & Gas, Chemical, Water Treatment, Mining, Others), and Regional Analysis for 2025 - 2032

Mud Valves Market Size and Trend Analysis

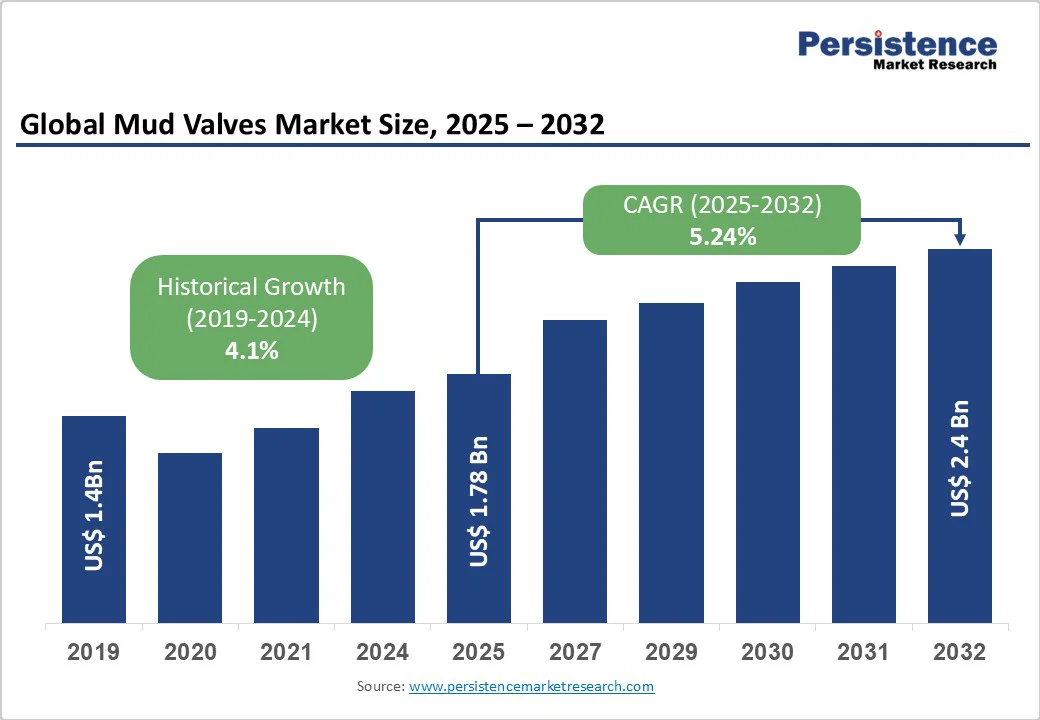

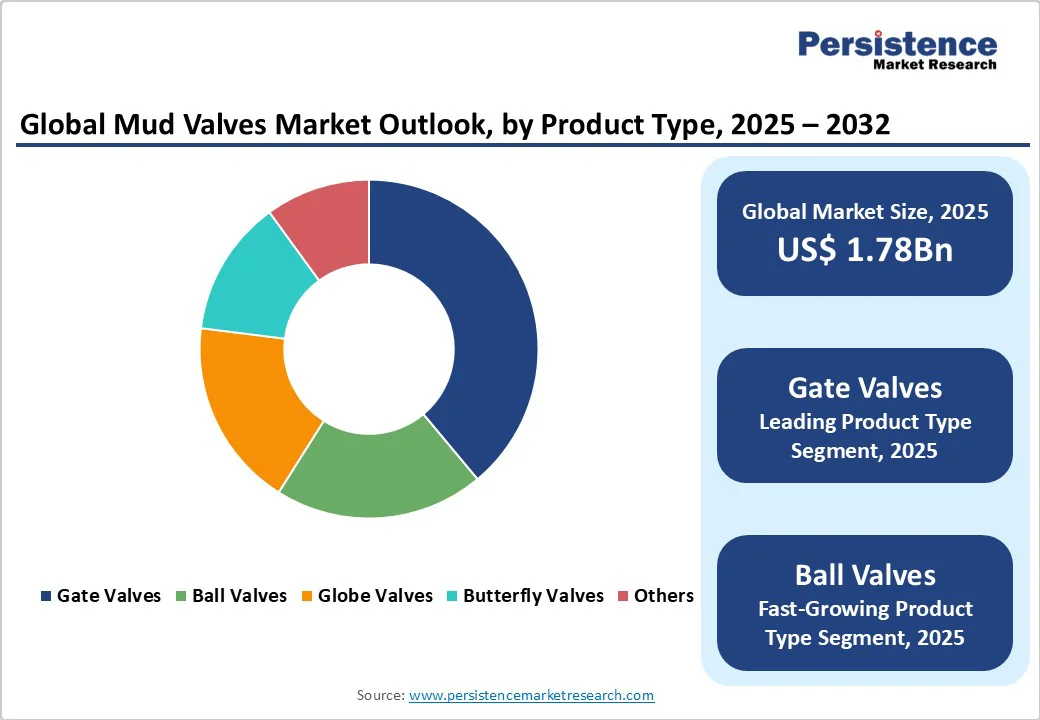

The global mud valves market size is likely to be value at US$1.78 Bn in 2025 and reach US$2.48 Bn by 2032, growing at a CAGR of 5.24% during the forecast period from 2025 to 2032. The mud valves market is witnessing steady growth, driven by increasing demand from key industries such as oil & gas, water treatment, and mining, where high durability and resistance to abrasion are critical.

Mud valves, known for their robustness, reliability, and ability to handle viscous and sediment-laden fluids, are essential for flow control, sludge management, and drilling operations. The rise in global infrastructure projects, coupled with advancements in manufacturing technologies, supports market expansion.

Key Industry Highlights

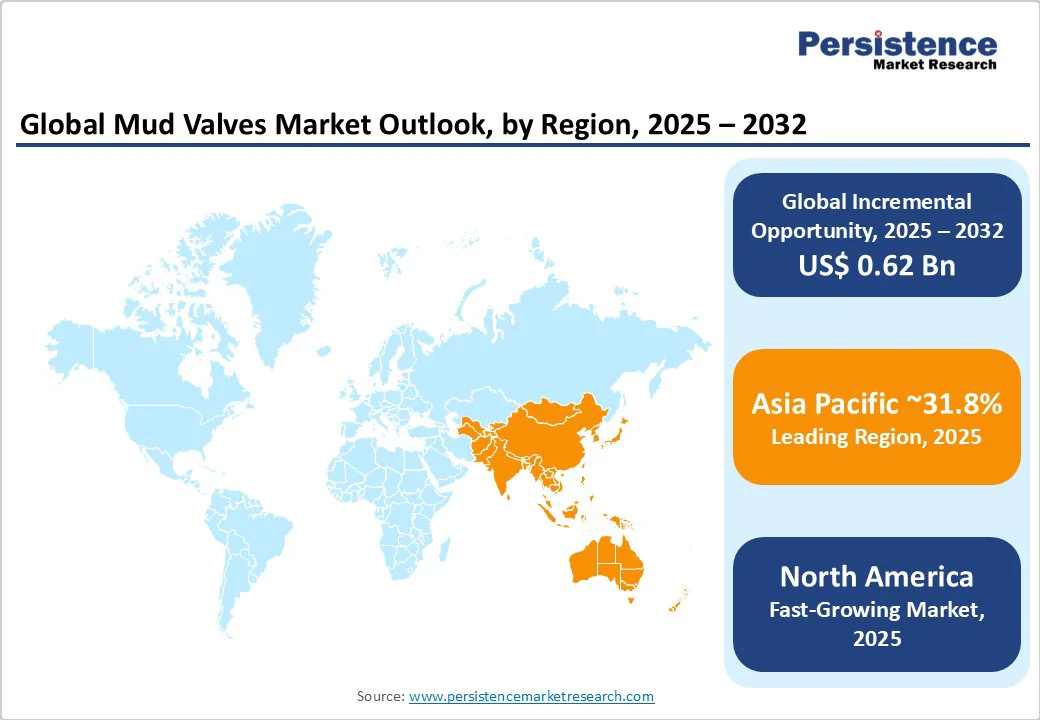

- Leading Region: Asia Pacific holds 31.8% market share of the mud valves market in 2025, propelled by rapid urbanization, infrastructure investments, and high drilling activities in countries such as China and India.

- Fastest-growing Region: North America is the fastest-growing region, driven by robust oil & gas and mining sectors in the U.S. and Canada, supported by advanced industrial infrastructure.

- Scalability: China’s National Development and Reform Commission announced a 2022 plan to construct 461,000 km of highways by 2035, boosting demand for mud valves in mining and construction applications.

- Dominant Product Type: Gate Valves, accounting for nearly 38.9% of the mud valves market share, due to their cost-effectiveness and high sealing capability for heavy-duty applications.

- Leading Application: Oil & Gas, contributing over 29.8% of market revenue, driven by global exploration and production trends.

| Key Insights | Details |

|---|---|

| Mud Valves Market Size (2025E) | US$ 1.78Bn |

| Market Value Forecast (2032F) | US$ 2.4Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.24% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.1% |

Market Dynamics

Driver: Growing Infrastructure and Construction Activities Fuel Market Expansion

The global mud valves market is experiencing significant growth due to the surge in infrastructure and construction activities worldwide. Mud valves are critical in mining and water treatment for managing slurry flows, sediment drainage, and pressure control in heavy-duty systems. According to the World Bank, global infrastructure investment needs are expected to reach $94 trillion by 2040, with a significant portion allocated to emerging economies.

In the Asia Pacific, China’s Belt and Road Initiative and India’s Smart Cities Mission drive demand for high-strength mud valves in mining applications. The American Society of Civil Engineers reports that 623,000 U.S. bridges require repair or replacement, further increasing the need for durable mud valves.

Companies such as Flowserve Corporation reported a sales increase in mud valve products for industrial applications in 2024. Government-led initiatives and rising urbanization ensure sustained demand, positioning construction as a key driver for market growth through 2032.

This expansion is further supported by the International Energy Agency's projection that global renewable energy capacity will grow by 2.7 times by 2030, indirectly boosting mud valve usage in related infrastructure, such as water treatment facilities for sustainable projects.

The integration of mud valves in automated systems enhances operational efficiency, reducing downtime and maintenance costs, which aligns with the broader push for resilient supply chains in volatile global markets. As urbanization accelerates, particularly in densely populated regions, the demand for efficient fluid management solutions becomes imperative, solidifying mud valves' role in long-term market stability.

Restraint: Volatility in Raw Material Prices and Competition from Synthetic Valves

The mud valves market faces challenges due to fluctuating raw material prices and growing competition from synthetic valves. Production relies heavily on metals such as stainless steel and cast iron, both subject to price volatility. In 2023, iron ore prices fluctuated by up to 20%, impacting production costs for manufacturers. This volatility increases pricing pressures, particularly for smaller players, limiting their ability to compete.

Additionally, synthetic valves, such as those made from composite materials, are gaining traction due to their lighter weight and corrosion resistance. Limited standardization in some regions and concerns over abrasion in harsh environments further hinder adoption, particularly in cost-sensitive markets, restraining overall market growth.

Environmental regulations on metal mining add to supply chain disruptions, while the shift toward eco-friendly alternatives pressures traditional mud valve designs. Smaller manufacturers struggle with compliance costs, exacerbating market fragmentation and slowing innovation in core segments.

Opportunity: Rising demand in the Renewable Energy and Electric Vehicle Sectors

The increasing focus on renewable energy and electric vehicles (EVs) presents significant opportunities for the mud valves market. Mud valves are essential in renewable energy projects, such as geothermal drilling and offshore wind farms, for fluid circulation and sediment control. The International Energy Agency projects global renewable energy capacity to grow by 2.7 times by 2030, with offshore investments driving demand for abrasion-resistant valves.

In the EV sector, mud valves are used in battery manufacturing processes and wastewater treatment for chemical handling. Companies such as Emerson Electric Co. are innovating with corrosion-resistant mud valves for renewable applications, aligning with sustainability trends.

Government incentives, such as the EU’s Green Deal, further encourage investments in green technologies, creating opportunities for manufacturers to develop advanced, eco-friendly mud valves to meet evolving industry needs through 2032. The push for zero-liquid discharge systems in EV plants amplifies this, as mud valves ensure precise sludge management, reducing environmental impact.

Emerging markets in the Asia Pacific offer untapped potential, where rapid EV adoption intersects with water scarcity challenges, fostering hybrid valve solutions that blend durability with energy efficiency.

Category-wise Insights

By Product Type

- Gate Valves hold the largest market share of the mud valves market, approximately 38.9% in 2025, due to their high sealing efficiency and cost-effectiveness. Widely used in oil & gas and mining applications, gate valves are favored for their ability to provide full flow with minimal pressure drop, making them ideal for handling abrasive slurries and high-pressure environments. Companies such as Emerson Electric Co. and Flowserve Corporation lead with extensive portfolios, catering to demand in infrastructure and drilling sectors across North America and the Asia Pacific. Their robust design ensures bubble-tight shutoff, reducing leakage risks in critical operations, while advancements in resilient seating enhance longevity in corrosive conditions.

- Ball Valves are the fastest-growing product segment, driven by their compact design and quick quarter-turn operation, making them ideal for chemical and water treatment applications. Their adoption is rising in dynamic environments, such as offshore drilling, with brands such as Weir Group PLC expanding offerings in coastal regions of Europe and the Asia Pacific, supported by growing demand for low-maintenance, high-flow valves. Innovations such as trunnion-mounted designs improve stability under extreme pressures, aligning with the shift toward efficient resource management in mining operations.

By Application

- The Oil & Gas sector accounts for over 29.8% of market revenue in 2025, driven by global exploration projects and production demands. Mud valves are critical for controlling drilling fluids and preventing blowouts in upstream operations. Major players such as Schlumberger Limited and Baker Hughes Company supply high-performance valves for projects in the U.S. and China, where government investments in shale gas and offshore rigs fuel demand.

- The Water Treatment sector is the fastest-growing application of the mud valves market, propelled by rising investments in wastewater management and clean water initiatives. Mud valves are used in sludge dewatering and clarifier systems, with companies such as AVK Holding A/S innovating for high-solids handling. Growth in the Asia Pacific and the Middle East, driven by urbanization and scarcity challenges, supports this segment’s rapid expansion.

By Material

- Stainless Steel holds the largest market share, approximately 38.9% in 2025, due to its superior corrosion resistance and durability. Widely used in chemical and oil & gas applications, stainless steel mud valves are favored for their ability to withstand harsh, abrasive environments without degradation. Companies such as KSB SE & Co. KGaA and Crane Co. lead with extensive portfolios, catering to demand in water treatment and mining sectors across North America and the Asia Pacific.

- Cast Iron is the fastest-growing material segment, driven by its cost-effectiveness and robustness, making it ideal for mining and industrial applications. Its adoption is rising in budget-sensitive environments, such as large-scale water treatment plants, with brands such as L&T Valves Limited expanding offerings in emerging markets of Europe and the Asia Pacific, supported by growing demand for affordable, heavy-duty valves. Epoxy coatings improve corrosion protection, extending usability in humid conditions, while ductile variants offer flexibility without sacrificing strength.

Regional Insights

Asia Pacific Mud Valves Market Trends

The Asia Pacific dominates the mud valves market, accounting for 31.8%, fueled by rapid urbanization, infrastructure investments, and high drilling activities in countries such as China and India.

In 2022, China produced approximately 1.018 billion metric tons of crude steel, accounting for 54.0% of the global output, which was 1.885 billion metric tons in total, driving the availability of raw materials for mud valves. India’s infrastructure sector, supported by initiatives such as the Smart Cities Mission, boosts demand for water treatment-grade valves.

The region’s mining and chemical industries also contribute, with companies such as L&T Valves Limited and KSB SE & Co. KGaA expanding their presence. Rising industrial manufacturing and government-led projects ensure the Asia Pacific’s rapid market growth through 2032.

Key drivers include China's Belt and Road Initiative, necessitating robust mud valves for fluid control in pipelines and refineries. India's mining output, further amplifies need for abrasion-resistant solutions. Technological adoption, such as automated valves in smart grids, enhances efficiency, positioning the region as a hub for innovation amid escalating resource demands.

North America Mud Valves Market Trends

North America is the fastest-growing region of the mud valves market due to strong demand from the U.S. oil & gas and Canadian mining sectors. The U.S. oil & gas industry extensively uses mud valves for drilling and flow control, ensuring operational safety and efficiency.

Meanwhile, Canada’s mining sector relies on durable valves to handle harsh environments and abrasive materials, as highlighted by the Mining Association of Canada. Advanced industrial infrastructure supports this robust growth and technological adoption.

Major players such as Emerson Electric Co. and Flowserve Corporation dominate with extensive distribution networks, catering to exploration projects such as shale fracking and bridge infrastructure.

Consumer preference for high-quality, corrosion-resistant valves further strengthens North America’s market position. As of 2023, the United States had approximately 700,000 active oil and gas wells, underscores the need for high-pressure mud valves, while Canada's geothermal initiatives align with green transitions.

Europe Mud Valves Market Trends

Europe is the second fastest-growing region for the mud valves market, driven by stringent safety regulations, rising demand in the chemical and water treatment sectors, and infrastructure development in countries such as Germany and France.

The European water treatment industry, supports demand for mud valves in sludge handling and purification. Germany’s chemical sector, a key consumer of alloy steel valves, benefits from players such as AVK Holding A/S and Weir Group PLC. The EU’s Green Deal promotes renewable projects, increasing demand for corrosion-resistant valves in wastewater facilities.

Europe’s focus on sustainability and high-quality standards drives market growth, with companies innovating to meet regulatory and consumer demands. The directive on urban wastewater treatment, propels adoption in municipal systems, while France's nuclear decommissioning projects require precise fluid control.

Germany's Industry 4.0 framework integrates smart mud valves, enhancing predictive maintenance and reducing emissions, ensuring Europe's competitive edge in eco-driven markets.

Competitive Landscape

The global mud valves market is highly competitive, dominating through extensive product portfolios and global distribution networks. The mud valves market is characterized as a fragmented market based on competitors. This is due to the presence of numerous domestic and international players, ranging from large, established companies to smaller, regional manufacturers.

Regional players such as L&T Valves Limited focus on localized offerings in the Asia Pacific. Companies are investing in advanced manufacturing technologies and abrasion-resistant coatings to enhance market share, driven by demand for high-performance valves in the oil & gas and water treatment sectors.

Key Industry Developments

- November 2024: At ADIPEC 2024, American Mud Pumps (AMP) unveiled its next-generation mud pump solutions, featuring high-performance pistons, valve assemblies, and liners. These innovations were designed to enhance efficiency, reliability, and performance in extreme drilling conditions, reflecting AMP’s commitment to advancing technology for the oil and gas industry.

- December 2023: JSC Valve launched its latest Mud Gate Valve, designed according to API Spec 6A standards. The new valve featured a compact design with about one-third reduction in height, faster opening and closing times, and lower production costs compared to traditional valves. This development aimed to improve efficiency and reliability in oil and gas drilling operations globally.

Companies Covered in Mud Valves Market

- Emerson Electric Co.

- Flowserve Corporation

- Weir Group PLC

- Schlumberger Limited

- Baker Hughes Company

- National Oilwell Varco, Inc.

- Cameron International Corporation

- Curtiss-Wright Corporation

- Velan Inc.

- L&T Valves Limited

- AVK Holding A/S

- KSB SE & Co. KGaA

- Crane Co.

- Others

Frequently Asked Questions

The Mud Valves market is projected to reach US$1.78 Bn in 2025.

Growing infrastructure and construction activities, and expanding applications in renewable energy are the key market drivers.

The Mud Valves market is poised to witness a CAGR of 5.24% from 2025 to 2032.

The rising demand in the renewable energy and electric vehicle sectors is the key market opportunity.

Emerson Electric Co., Flowserve Corporation, Weir Group PLC, and Schlumberger Limited are key market players.