- Beauty & Personal Care

- Dead Sea Mud Cosmetics Market

Dead Sea Mud Cosmetics Market Size, Share, and Growth Forecast, 2026 - 2033

Dead Sea Mud Cosmetics Market by Product (Bathing Products, Body Care Products, Facial Care Products, Hair Care Products), End-User (Women, Men), Distribution Channel (Online, Offline), and Regional Forecast for 2026 - 2033

Dead Sea Mud Cosmetics Market Share and Trends Analysis

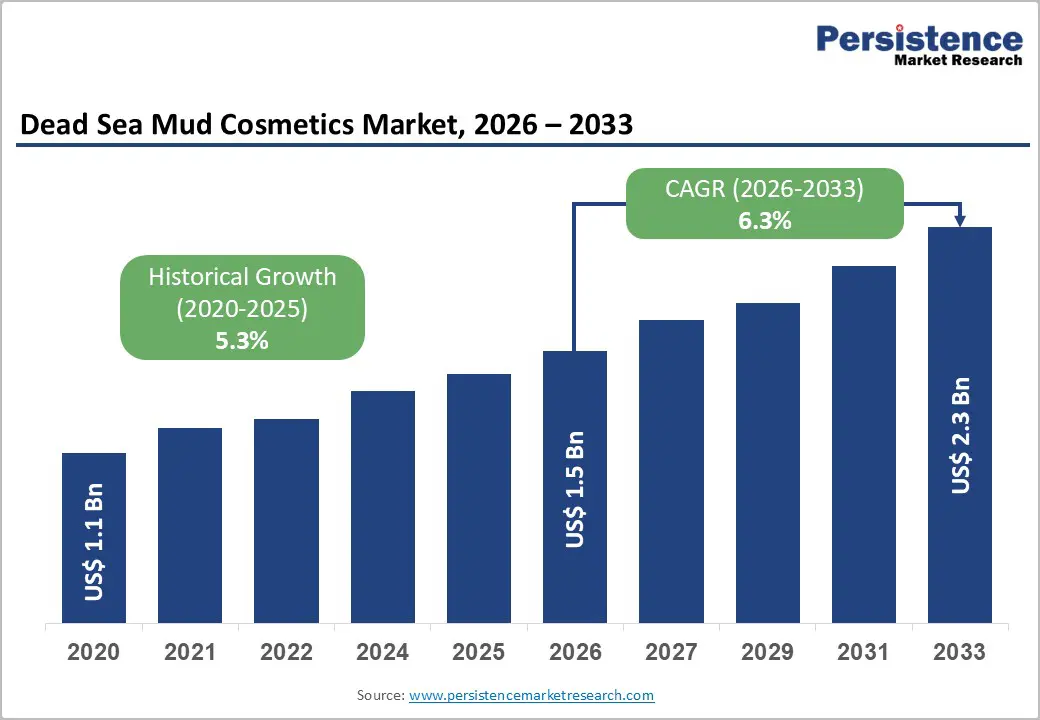

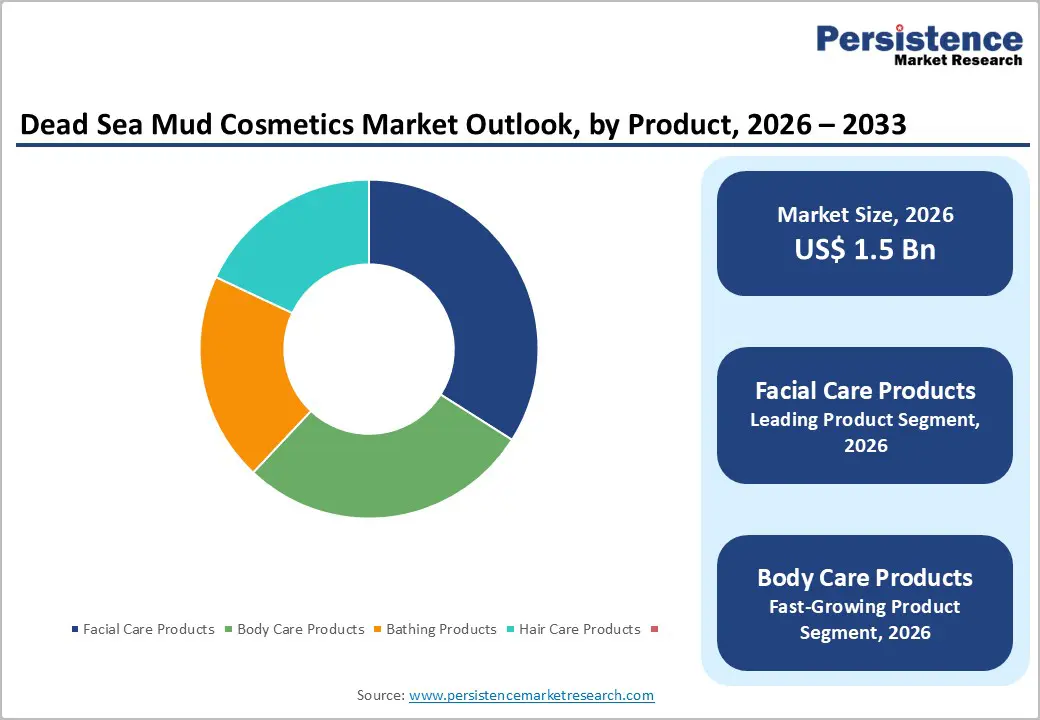

The global dead sea mud cosmetics market size is likely to be valued at US$1.5 billion in 2026, and is projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 6.3% during the forecast period 2026 - 2033.

This forecast reflects sustainable growth driven by rising consumer demand for natural & mineral-based skincare, increased awareness of wellness and therapeutic benefits, and expanding global distribution networks. Ongoing product innovation in natural cosmetics and rising uptake in emerging regions substantiate growth momentum. Digital marketing and e-commerce adoption further bolster the market’s expansion by enhancing accessibility and brand reach.

Key Industry Highlights

- Dominant Products: Facial care products are expected to lead with approximately 34% market share in 2026, while body care products are likely to be the fastest-growing, with a 7.1% CAGR through 2033, driven by rising full-body wellness and spa routines.

- Leading Distribution Channels: Offline channels are anticipated to command about 60% of revenue share in 2026, whereas online channels are projected to grow the fastest at a 9.2% CAGR during 2026-2033, owing to the deployment of a direct-to-consumer (D2C) marketing strategy.

- Dominant End-Users: Women are expected to account for a 70% share in 2026, while men are likely to register the fastest growth at 8.5% CAGR through 2033, driven by increasing adoption of skincare and grooming solutions.

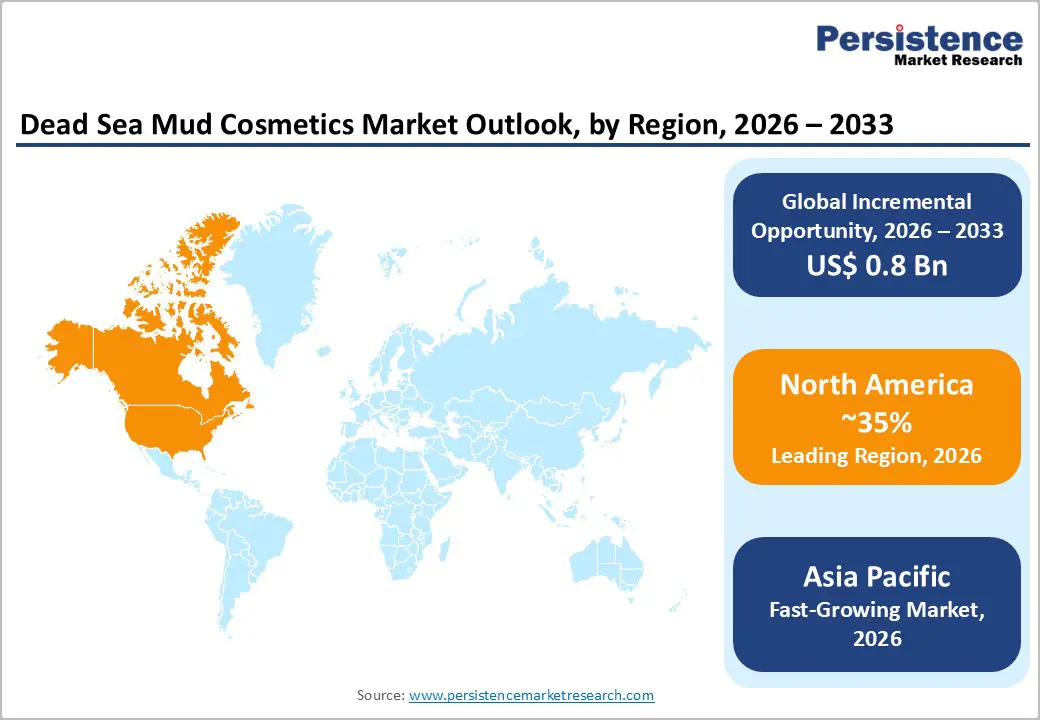

- Regional Leadership: North America is poised to dominate with an estimated 35% share in 2026, supported by strong consumer demand for natural skincare

- Fastest-growing Market: Asia Pacific is expected to register the highest 2026 - 2033 CAGR of about 10.3%, fueled by massive urbanization and improving beauty-wellness awareness.

- Competitive Environment: The market is moderately concentrated, with specialist players controlling authentic Dead Sea sourcing, leveraging brand heritage, supply chain exclusivity, and innovation-focused differentiation.

| Key Insights | Details |

|---|---|

| Dead Sea Mud Cosmetics Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 2.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Natural and Digitally Accessible Skincare Solutions

The global shift toward clean beauty and mineral-rich formulations is fueling growth in the Dead Sea mud osmetics market. Consumers increasingly prefer products with natural ingredients and proven therapeutic benefits, with Dead Sea mud valued for its high mineral content, including magnesium, calcium, and potassium, supporting skin detoxification and hydration. This trend drives innovation across facial cleansers, body masks, and full-body therapeutic skincare, catering to both premium and mass-market segments. Regulatory focus on ingredient authenticity and traceability enhances consumer confidence, reinforcing preference for mineral-based products. A related development is Jericho Cosmetics receiving ECOCERT organic certification for its Dead Sea mud product line, reflecting the growing importance of eco-labeled and certified organic skincare in the industry.

The expansion of digital channels and e-commerce platforms is accelerating market adoption. Online sales benefit from direct-to-consumer strategies, social media engagement, and interactive digital marketing, allowing consumers to explore products, read reviews, and compare formulations globally. This digital presence boosts visibility for established and emerging brands while enabling market penetration in both developed and developing regions, particularly among digitally native consumers. Supporting this trend, leading beauty brands are integrating augmented reality (AR) tools and virtual skincare consultations, allowing consumers to trial products online and make more informed purchasing decisions, further enhancing engagement and sales.

Supply Chain and Regulatory Challenges

The Dead Sea mud cosmetics market growth faces significant supply chain complexities due to the geographic specificity of Dead Sea mud, which elevates sourcing costs and operational challenges. For example, AHAVA, a leading Dead Sea mud brand, reports higher procurement costs for authentic mud, while smaller firms face notably higher unit costs compared to conventional cosmetic formulations. These factors constrain price competitiveness, making it difficult for emerging brands to penetrate mainstream markets. Additionally, the limited availability of authentic mud can lead to supply delays, affecting production schedules and inventory management. Such operational pressures require strategic sourcing and robust logistics planning to ensure consistent product delivery.

The regulatory challenges associated with therapeutic and health-benefit claims introduce additional risk. Compliance requirements vary by region, and approximately 15-20% of new products experience delays due to audits or claims verification. Local authorities often scrutinize health, wellness, or “spa-quality” statements, which can increase time to market and elevate compliance costs. Brands must implement stringent documentation and testing protocols to meet regulatory standards while maintaining consumer trust. These combined supply chain and regulatory pressures remain key barriers to faster market growth.

Expansion and Multi-Functional Product Innovation

Emerging markets in the Asia Pacific, the Middle East, and Latin America represent a significant growth frontier for Dead Sea mud cosmetics. Asia Pacific alone is recording huge annual volume increases, driven by rising urban middle-class spending and beauty-wellness adoption, especially in China and India. Brands that pursue targeted regional expansion and localized product assortments, such as Freeman Beauty entering India with Dead Sea mineral face masks and body scrubs via major e-commerce platforms, can tap under-penetrated consumer segments and diversify revenue streams. Tailoring products to regional skincare preferences and cultural beauty routines strengthens brand relevance and enhances market penetration. Strategic investment in these regions allows companies to capture both premium and mass-market opportunities, aligning offerings with evolving consumer needs and preferences.

Multi-functional product innovation continues to drive market growth. Products that combine facial and body masks or integrate hair care benefits with Dead Sea mud formulations have become increasingly common in recent cosmetic launches, reflecting strong consumer demand for efficacy-driven, value-added solutions. Focusing on cross-segment applicability, enhanced performance, and convenience enables brands to expand into the skincare, body care, and hair care categories, thereby maximizing shelf appeal and consumer engagement. This innovative approach strengthens brand differentiation and competitive positioning, increases revenue potential, and drives long-term growth in a competitive landscape.

Category-wise Insights

Product Insights

The facial care segment is expected to hold an estimated 34% of the Dead Sea mud cosmetics market revenue share in 2026, driven by deep-cleansing, detoxifying, and anti-aging benefits in masks, scrubs, and serums. Consumers seek visible results in hydration, pore refinement, and skin rejuvenation, making facial care a staple in daily beauty routines. Premium pricing of specialized facial masks further enhances its contribution to market value. For instance, L’Occitane’s launch of sea mineral anti-aging facial mask illustrates innovation targeting facial detoxification and rejuvenation. Distribution through specialty retailers and e-commerce ensures broad reach, consolidating facial care’s leadership in the market.

The body care segment, including mud-infused scrubs, wraps, and lotions, is projected to be the fastest-growing product category with an estimated CAGR of 7.1% through 2033, reflecting consumer interest in full-body wellness and spa-inspired self-care at home. Its growth is fueled by rising demand for therapeutic treatments that improve skin texture, circulation, and overall wellness. Brands are innovating to capture this trend, such as Freeman Beauty’s introduction of Dead Sea Mud Body Scrubs for at-home spa experiences, appealing to wellness-conscious consumers. Expanding the product portfolio beyond facial applications allows brands to increase market penetration and revenue. The segment’s adoption in both professional spa settings and retail channels supports its strong CAGR relative to other categories.

End-User Insights

Women are likely to remain the dominant consumer group of Dead Sea mud cosmetics, accounting for nearly 70% of the total market consumption in 2026, driven by comprehensive skincare routines emphasizing hydration, detoxification, and anti-aging benefits. Female consumers are more likely to incorporate facial masks, serums, and body exfoliators into their daily regimens. Seacret’s Sea Mud Mineral Mask targeted at women strengthened engagement in this segment, highlighting the effectiveness of products designed for female skincare routines. Distribution through offline premium stores and online platforms further consolidates women’s leadership in market share. This segment continues to anchor the market, guiding product innovation and marketing strategies.

Although smaller, the men's segment is expected to be the fastest-growing, with a 8.5% CAGR through 2033, supported by changing societal norms and rising male interest in skincare. Products targeting men, including oil-control face masks, sensitivity-reducing cleansers, and scalp treatments, are increasingly accepted. For example, Bulldog Skincare’s launch of Dead Sea mud face scrub for men tapped into this emerging demand, reflecting a shift toward functional male grooming solutions. Digital campaigns and social media strategies aimed at male consumers enhance visibility and adoption. This growth trajectory indicates strong potential for brands to expand offerings and increase penetration within the male demographic.

Distribution Channel Insights

Offline channels, including specialty beauty stores, spas, and salons, are expected to account for the largest revenue share, estimated at 60% in 2026, driven by in-person sampling, professional consultations, and experiential engagement. Consumers prefer tactile evaluation of premium Dead Sea mud products, influencing purchase decisions. Rituals Cosmetics expanded its spa-based retail experiences to feature Dead Sea mud treatments, exemplifying how offline stores drive engagement. Boutique experiences, in-store demos, and personalized consultations enhance brand trust, particularly for premium formulations, ensuring continued leadership of offline channels in total sales.

The online channel is anticipated to be the fastest-growing distribution segment, with an estimated CAGR of 9.2% through 2033, driven by e-commerce adoption, convenience, and direct-to-consumer strategies. Platforms such as brand websites and digital marketplaces allow consumers to research, compare, and purchase products easily. Social media and influencer marketing amplify product discovery and trust. For example, Sephora’s global launch of Dead Sea mud kits on its website demonstrates how brands leverage online channels to reach new audiences. Personalized marketing, subscription models, and global reach contribute to this segment’s rapid growth, making it the most dynamic distribution channel in the market.

Regional Insights

North America Dead Sea Mud Cosmetics Market Trends

North America is anticipated to account for approximately 35% of the Dead Sea mud cosmetics market share in 2026, with the United States accounting for the majority of regional demand. High consumer spending on premium skincare, strong awareness of mineral-based beauty solutions, and a mature beauty retail ecosystem support sustained market leadership. Department stores, specialty beauty retailers, and dermatologist-endorsed brands reinforce consumer confidence. Advanced digital infrastructure further enhances market access through omnichannel engagement. North America’s leadership reflects strong alignment between wellness-driven consumer preferences and premium cosmetic positioning.

The growth momentum is reinforced by regulatory clarity and innovation-led competition. Oversight by the U.S. Food and Drug Administration (FDA) ensures compliance with cosmetic safety and labeling requirements, strengthening product credibility. Estée Lauder Companies expanded mineral-based skincare assortments across select North American retail banners, reflecting growing demand for efficacy-backed natural formulations. Competitive dynamics blend global beauty conglomerates with niche mineral-specialist brands, driving continuous product upgrades. Strategic investments in influencer partnerships and clinical positioning further sustain regional dominance.

Europe Dead Sea Mud Cosmetics Market Trends

Europe represents one of the most influential regional markets for Dead Sea mud cosmetics, supported by strong consumer trust in natural skincare and a deeply rooted spa and wellness culture. Countries such as Germany, the U.K., France, and Spain drive regional demand through high adoption of clean-label and eco-certified beauty products. Well-developed specialty retail networks, pharmacies, and wellness centers strengthen distribution efficiency across the region. European consumers place high importance on mineral authenticity, ethical sourcing, and scientific substantiation. These preferences position Dead Sea mud cosmetics as premium wellness-oriented solutions. Established brand loyalty further supports stable market performance.

Regulatory harmonization under the European Union (EU) Cosmetics Regulation enhances transparency, safety compliance, and consumer confidence. Sustainability mandates and strict controls on misleading claims encourage rigorous formulation and documentation standards. SABON expanded its Dead Sea-inspired body care portfolio across Western Europe, emphasizing responsibly sourced minerals and recyclable packaging. Competitive strategies increasingly prioritize cruelty-free certification, dermatological testing, and sustainability messaging. Investment activity focuses on formulation innovation and environmentally responsible packaging. These factors reinforce Europe’s role as a quality-driven and regulation-led market.

Asia Pacific Dead Sea Mud Cosmetics Market Trends

Asia Pacific is projected to be the fastest-growing regional market for Dead Sea mud cosmetics, expanding at a CAGR of roughly 10.3% through 2033. The growth is driven by rapid urbanization, rising middle-class income, and increasing consumer awareness of mineral-rich skincare benefits. Demand is particularly strong in China, Japan, India, and key ASEAN countries. Consumers increasingly associate Dead Sea mud products with skin detoxification, hydration, and wellness-led beauty routines. The region’s youthful population and evolving beauty standards further accelerate adoption. These factors position the Asia Pacific as the primary growth engine for the market.

Digital-first retail behavior strongly influences purchasing decisions across the region. Social commerce platforms, influencer-led education, and mobile-driven beauty discovery accelerate product trial and brand visibility. Regulatory environments vary widely, requiring brands to adapt formulations, labeling, and import strategies on a country-by-country basis. Shiseido expanded its mineral-based body and scalp care offerings across select Asia Pacific markets, aligning with regional demand for functional, natural beauty solutions. Global players increasingly pursue localized manufacturing and distribution partnerships to improve cost efficiency and compliance. Meanwhile, regional brands innovate with culturally relevant wellness positioning. These dynamics collectively sustain the Asia Pacific’s high-growth trajectory.

Competitive Landscape

The global Dead Sea mud cosmetics market structure is moderately concentrated, with a group of established specialist and premium skincare brands accounting for a significant portion of overall revenue. These leading players differentiate themselves through exclusive access to authentic Dead Sea mineral sourcing, vertically integrated supply chains, and strong brand positioning around therapeutic and wellness benefits. Broad distribution across specialty beauty retailers, spas, dermatology clinics, and digital platforms supports their market influence. Continuous investment in formulation science, dermatological validation, and sustainable packaging further strengthens competitive positioning and consumer trust.

Regional and niche brands compete by targeting specific consumer needs such as sensitive skin, men’s grooming, or price-accessible wellness products. Barriers to entry remain high due to sourcing constraints, regulatory compliance, and authenticity verification requirements. However, direct-to-consumer and digital-first models lower entry barriers for emerging brands. Competitive intensity is expected to increase as established players pursue geographic expansion, while smaller brands leverage partnerships, private labeling, and sustainability credentials to gain visibility.

Key Industry Developments

- In November 2025, SABON Japan launched its premium holiday collection, “Majestic Gala,” featuring Dead Sea mud body scrubs, scalp scrubs, masks, and curated gift sets. The collection used a “one-night dinner party” theme with festive fragrances such as Osmanthus and White Magnolia to enhance luxury appeal. Gold accents and premium packaging reinforced its high-end positioning.

- In March 2025, Cohere Beauty launched the Luxe Renewal Skincare Collection, featuring nine advanced formulas that blend science and botanicals to support trends such as skinimalism and microbiome balance.

Highlights include the Fresh Start Pore Clearing Clay Mask with Dead Sea mud, salicylic acid, and oat extract for deep detoxification and pore refinement, alongside anti-aging serums and creams targeting brightness, repair, and firmness.

Companies Covered in Dead Sea Mud Cosmetics Market

- AHAVA, Inc.

- Premier Dead Sea

- Seacret Direct LLC

- HB Health & Beauty Ltd.

- Aroma Dead Sea Spa & Cosmetics

- Dr. Sea Cosmetics Inc.

- Sea of Spa Natural Cosmetics Ltd.

- Dead Sea Spa Magik

- Mineral Care

- Kawar Cosmetics

- BCL Spa

- Premier Skin Solutions

- Bio Beauty Labs

- Mayan Earth Cosmetics

Frequently Asked Questions

The global Dead Sea mud cosmetics market is projected to reach US$ 1.5 billion in 2026.

Key market drivers include rising consumer preference for natural and mineral-based cosmetics, increasing awareness of therapeutic skincare benefits, and expanding digital and direct-to-consumer retail channels supporting global accessibility.

The market is poised to witness a CAGR of 6.3% from 2026 to 2033.

Opportunities include growth in multi-functional skincare products, rising male grooming adoption, and increased demand for sustainable and clean-label cosmetic formulations.

AHAVA Dead Sea Laboratories, SABON, Seacret, Premier Dead Sea, L’Occitane Group, are a few among the key players.