- Off-Road Equipment & Machinery

- Motor Graders Market

Motor Graders Market Size, Share, and Growth Forecast, 2026 - 2033

Motor Graders Market by Product Type (Rigid Frame, Articulated Frame), Capacity (Medium, Heavy, Large), Application (Construction, Mining, Others), and Regional Analysis for 2026 - 2033

Motor Graders Market Share and Trends Analysis

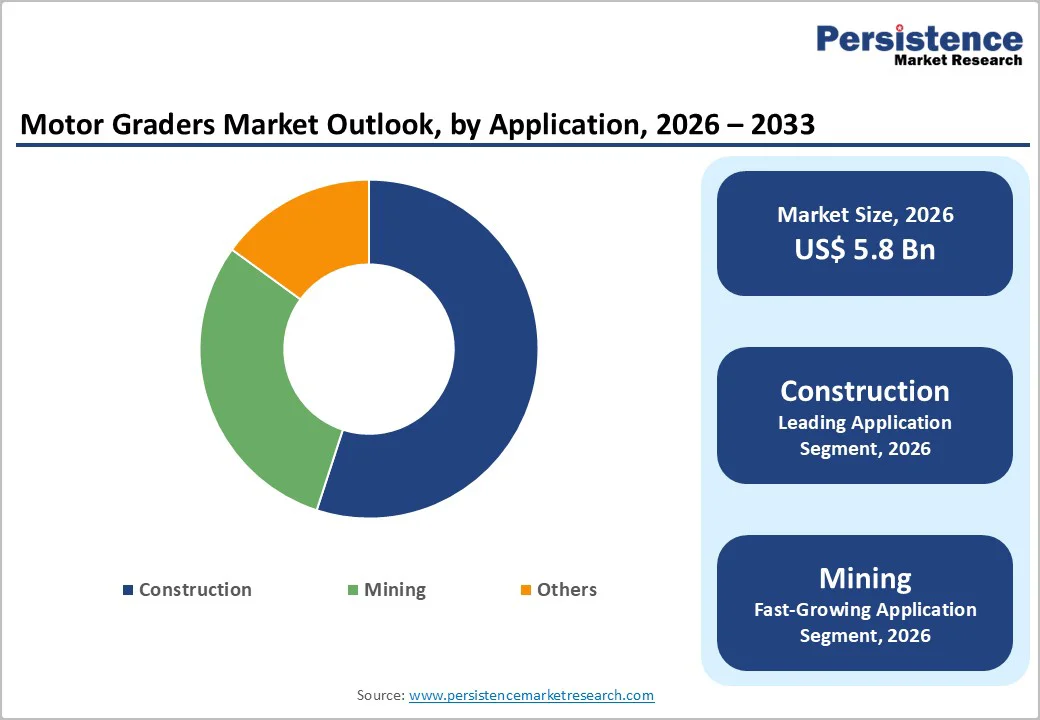

The global motor graders market size is likely to be valued at US$ 5.8 billion in 2026 and is estimated to reach US$ 11.0 billion by 2033, growing at a CAGR of 9.4% during the forecast period 2026 - 2033.

This robust expansion is driven by accelerating infrastructure development initiatives across emerging economies, particularly in road construction and maintenance projects. The market benefits from increasing government investments in transportation infrastructure modernization, with developing nations allocating substantial budgets toward highway network expansion.

Technological advancements in automation and precision grading systems are further enhancing operational efficiency, while replacement demand from aging equipment fleets in developed markets is sustaining growth momentum.

Key Industry Highlights

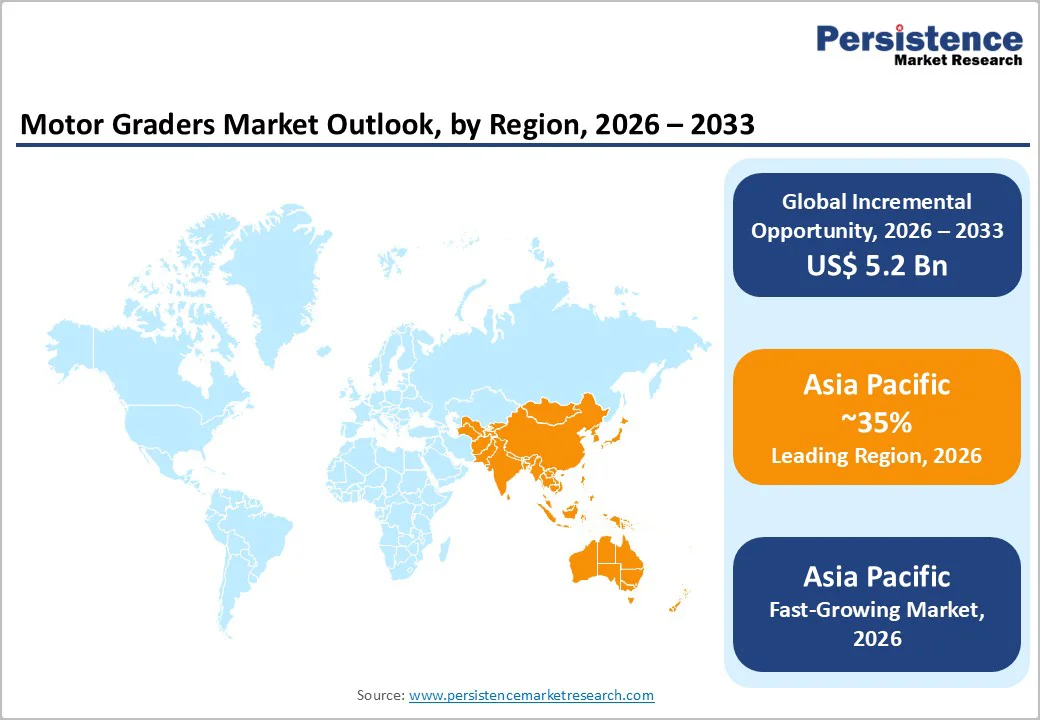

- Dominant Region: Asia Pacific is expected to command about 35% market share in 2026, supported by rapid urbanization and accelerating industrialization.

- Fastest-growing Market: Asia Pacific is poised to be the fastest-growing market through 2033, due to the ongoing expansion of national and cross-border transport networks.

- Leading & Fastest-growing Product Types: Rigid frame is slated to lead with an approximate 65% revenue share in 2026, while articulated frame is likely to be the fastest-growing during the 2026 - 2033 forecast period.

- Dominant & Fastest-growing Applications: Construction is set to dominate with an approximate share of 55% in 2026, whereas mining is anticipated to be the fastest-growing through 2033.

- August 2025: Mahindra launched the CEV-V range of EarthMaster Backhoe Loaders and RoadMaster Motor Graders, featuring improved fuel efficiency, enhanced productivity, and robust designs.

| Key Insights | Details |

|---|---|

| Motor Graders Market Size (2026E) | US$ 5.8 Bn |

| Market Value Forecast (2033F) | US$ 11.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Infrastructure Development and Urbanization Initiatives

Global infrastructure investment has witnessed unprecedented growth, with the Asian Development Bank (ADB) reporting that developing Asia alone requires US$ 1.7 trillion annually in infrastructure spending through 2030. Motor graders play a critical role in road construction, maintenance, and grading operations essential for highway development projects.

Motor graders occupy a central position in this ecosystem because they enable high-precision surface preparation, alignment, and finishing of roadways. As governments prioritize upgrades to highways, regional link roads, and logistics corridors, contractors increasingly rely on reliable grading equipment to meet tighter timelines, quality standards, and lifecycle performance requirements.

This growing emphasis on durable, well-designed transport networks reinforces the importance of motor graders in both new construction and periodic maintenance cycles. At the same time, accelerating urbanization in emerging economies is reshaping land-use patterns and driving the ongoing expansion of transportation networks.

New urban centers, industrial corridors, and peri-urban developments all require access roads, arterial routes, and supporting infrastructure, with each stage demanding consistent and reliable grading performance. National programs focused on improving connectivity between cities, ports, and economic zones generate multi-year project pipelines that sustain recurring demand for motor graders across planning, construction, and maintenance phases.

High Capital Investment and Ownership Costs

Motor graders entail substantial capital investments, which can create significant barriers for small and medium-sized contractors. The financial burden extends well beyond the initial purchase, as owners must also account for ongoing maintenance, operator training, insurance, and financing obligations.

These recurring costs become particularly challenging in markets where access to credit is limited and lending conditions are relatively stringent. In such environments, contractors must make difficult trade-offs between upgrading their fleets, preserving cash flow, and remaining competitive when bidding for large-scale projects.

Economic volatility and project delays further intensify these pressures by disrupting revenue visibility and extending equipment payback periods. When workloads become unpredictable, the risks associated with owning high-value machinery increase, prompting many smaller operators to reconsider outright acquisition.

High utilization thresholds are often necessary to make ownership economically viable, but achieving them is difficult for contractors with irregular or seasonal project pipelines.

Expansion of Infrastructure Projects in Emerging Markets

Developing economies across the Asia Pacific, Africa, and Latin America offer a clear expansion pathway for motor grader manufacturers because governments continue to prioritize transport links, trade logistics, and rural access within national development programs.

Multilateral development banks (MDBs) can strengthen these buildouts by mobilizing additional funding from other public and private sources, thereby helping convert road plans into financed projects and sustaining equipment demand.

In parallel, structured project-pipeline initiatives help countries shape investable infrastructure portfolios, which gives contractors and original equipment manufacturers (OEMs) better multi-year visibility. This dynamic typically lifts grader requirements alongside corridor programs that include highways, secondary routes, and industrial logistics nodes.

These regions also offer meaningful headroom because many fleets remain underpenetrated and older, setting up both first-time purchases and predictable replacement cycles as utilization rises. One industry benchmark estimates that motor graders often run for roughly 10 to 15 years, underscoring why today’s low installed base can translate into recurring upgrades once spending stabilizes.

Public-private partnerships (PPPs) can further broaden the buyer pool by bringing in private capital, technical capability, and operational discipline when public budgets remain constrained. To convert this opportunity into orders, suppliers can pair right-sized machine configurations with localized parts availability, operator training, and financing structures that match project cash-flow timing.

Category-wise Analysis

Product Type Insights

The rigid frame segment is projected to command approximately 65% of the motor graders market revenue share in 2026, as these frames are the established benchmark for heavy-duty performance. Contractors favor these fixed-frame configurations for their unmatched stability during highway construction, mining operations, and extensive earthmoving tasks.

Precise blade positioning and operational reliability make them indispensable in high-intensity environments where downtime proves costly. Simplified maintenance routines further enhance their appeal to major firms that prioritize equipment longevity over frequent interventions. This segment's dominance reflects a proven return on investment for stakeholders managing large-scale, continuous workloads.

Articulated frame models are forecast to grow the fastest from 2026 to 2033, driven by their exceptional maneuverability in confined spaces. The flexible joint connecting the front and rear sections enables tight turns and superior navigation, making these units optimal choices for urban roadwork, municipal upkeep, and space-limited projects.

Recent engineering improvements have bolstered their durability without sacrificing agility advantages. Accelerating urbanization across Asia is compelling municipalities to specify these versatile machines for infrastructure maintenance. Contractors can gain a competitive edge by deploying articulated graders that accelerate project timelines in densely populated areas.

Capacity Insights

Medium-capacity motor graders are well positioned to dominate, accounting for approximately 65% of market revenue in 2026. This segment strikes an ideal equilibrium among power output, fuel consumption, and upfront investment, positioning it perfectly for highway builds, routine road upkeep, airport expansions, and standard earthmoving tasks.

Operators value the adaptable blade setups and interchangeable attachments that deliver the flexibility essential for diverse project scopes. Extensive manufacturer involvement in this category fosters intense price competition and expands equipment options for general contractors. Procurement teams recognize this range as a pragmatic choice that maximizes utilization across variable workloads while controlling total ownership expenses.

Heavy-capacity models are set to register the strongest expansion from 2026 through 2033, propelled by escalating requirements in mining activities and mega-infrastructure initiatives. High-horsepower configurations excel in demanding earthmoving applications, proving indispensable for haul road construction, pit preparation, and material logistics in large-scale mining operations.

Site managers depend on these robust units to navigate rugged landscapes and sustain productivity under extreme conditions. As global commodity extraction intensifies alongside ambitious public works programs, forward-looking suppliers should prioritize scalable designs that integrate telematics to optimize real-time performance.

Application Insights

Construction is expected to remain the largest application segment, capturing approximately 55% of the revenue share in 2026 as countries continue to modernize infrastructure and expand highway networks. Motor graders play a central role in road projects by handling subgrade preparation, surface shaping, material distribution, and final finishing to meet design specifications, making them indispensable in both new-build and rehabilitation programs.

Developing economies that view transport connectivity as a lever for economic growth sustain baseline demand, while mature markets allocate ongoing budgets to highway maintenance, lane additions, and reconstruction. For contractors and fleet owners, this translates into steady utilization rates and a strong business case for investment in versatile, construction-focused grader fleets that can move efficiently across multiple project types.

Mining is projected to be the fastest-growing application from 2026 to 2033 as global extraction activity and associated infrastructure requirements intensify. Operators rely on motor graders to build and maintain access routes, keep haul roads in optimal condition, support pit development, and manage tailings areas, all of which directly influence fuel efficiency, cycle times, and equipment wear across the mine fleet.

Large mining companies often deploy 10 to more than 20 graders per site, which creates recurring opportunities for replacement and incremental units as production scales or new pits open. From a strategic standpoint, suppliers that tailor offerings to mining needs, such as enhanced durability packages, high-visibility cabs, and telematics for road-condition monitoring, can capture outsized growth and deepen relationships with high-value industrial customers.

Regional Insights

Asia Pacific Motor Graders Market Trends

Asia Pacific is likely to be the leading and fastest-growing market for motor graders, forecasted to secure around 35% of the market share in 2026. The growth is underpinned by rapid urbanization, accelerating industrialization, and the ongoing expansion of national and cross-border transport networks.

Large economies such as China and India anchor regional demand through extensive highway, railway, airport, and logistics corridor programs, while Japan, Australia, and the major ASEAN countries add further depth through continuous upgrades of mature infrastructure and new green field projects in fast-growing urban clusters.

This combination of scale, diversified project pipelines, and strong government focus on connectivity creates a broad and resilient demand base for both new motor graders and fleet replacement across the region.

Investment trends emphasize localization strategies, with international manufacturers establishing regional production facilities, research centers, and after-sales support infrastructure.

Technology adoption accelerates in developed markets, including Japan, South Korea, and Australia, while price-competitive models address the requirements of emerging market. Government initiatives promoting domestic manufacturing through Make in India, Made in China 2025, and similar programs influence market dynamics and competitive positioning.

Europe Motor Graders Market Trends

Europe is expected to command a substantial portion of motor graders market share in 2026, fueled by consistent investments in transport infrastructure, road rehabilitation, and cross-border connectivity. Germany serves as the central demand hub, with the United Kingdom, France, and Spain contributing as established markets.

Central and Eastern European nations such as Poland, the Czech Republic, and Romania are accelerating growth through European Union (EU) funding and domestic development plans. This blend of mature and emerging economies creates a balanced foundation for suppliers seeking diversified revenue exposure.

Procurement managers benefit from this structure, as it supports both high-volume contracts in core countries and expansion opportunities in transitional markets.

Extensive project pipelines targeting highways, freight corridors, and urban networks sustain ongoing needs for grading equipment throughout construction, renovation, and upkeep stages. Contractors and rental firms achieve reliable utilization rates by deploying graders across diverse soil types and project magnitudes.

Multi-year funding horizons offer clear visibility for fleet strategists, facilitating proactive decisions on acquisitions, replacements, and technological enhancements. Organizations that align equipment specifications with regional soil challenges and emission standards can optimize performance while meeting regulatory expectations.

North America Motor Graders Market Trends

North America sustains a mature yet expanding motor grader market through extensive infrastructure renewal initiatives and the steady replacement of established fleets. The United States drives primary consumption through federal and state funding for highways, bridges, and logistics pathways.

Canada adds meaningful volume via provincial road maintenance programs and robust mining activities. Contractors and rental operators prioritize machines that boost productivity, optimize fuel use, and improve operator ergonomics. This preference strengthens demand for mid-to-large-capacity units featuring sophisticated control interfaces that streamline fieldwork across diverse project demands.

Regulatory pressures on emissions and workplace safety are compelling fleet upgrades to cleaner, more advanced configurations. Organizations must integrate models with enhanced engine efficiency, superior visibility features, and operator-assistance technologies to meet tender specifications. High rental market penetration allows small and medium-sized enterprises to deploy cutting-edge graders without substantial capital outlays.

Procurement leaders can leverage this dynamic to access modern capabilities that enhance operational metrics while aligning with compliance mandates. Consequently, North America emerges as a stable platform for suppliers offering reliable, technology-integrated solutions that support long-term fleet evolution.

Competitive Landscape

The global motor graders market maintains a moderately concentrated structure, where leading manufacturers such as Caterpillar, Komatsu, John Deere, Xuzhou Construction Machinery Group (XCMG Group), and Sany Heavy Industry command 60% to 65% of total revenue. These organizations differentiate through superior product quality, cutting-edge technological integrations, competitive pricing models, and comprehensive after-sales support networks.

Procurement specialists recognize that sustained innovation remains essential for market leaders to deliver graders equipped with precision controls and telematics capabilities. Forward-thinking suppliers prioritize these elements to secure long-term contracts with infrastructure developers and mining operators who demand measurable productivity gains.

Manufacturers actively compete by embedding advanced features such as automated blade adjustments and enhanced operator interfaces into their equipment lines. Environmental regulations are compelling the industry to accelerate development of fuel-efficient engines and low-emission powertrains that reduce operational costs over equipment lifecycles.

Contractors benefit from this rivalry as it expands access to machines that align with sustainability mandates while maintaining rugged performance in demanding applications. Strategic buyers should evaluate suppliers based on total cost of ownership metrics, including parts availability and service response times, to maximize return on fleet investments.

Key Industry Developments

- In August 2025, Caterpillar launched the next-generation 140 LVR motor grader with customizable controls (levers/joysticks), all-wheel drive options, enhanced cab visibility, and advanced tech such as Cat Grade 3D and Stable Blade for superior grading precision.

- In August 2025, Hitachi Construction Machinery Australia expanded its partnership with Bell Equipment to bring the full Bell motor grader range to the Australian market, complementing its existing distribution of Bell articulated dump trucks.

- In April 2025, BEML introduced the indigenously designed BG 1205 motor grader at its Mysuru complex, positioned as a key contribution to India’s Atmanirbhar Bharat (self-reliance) initiative in mining and construction equipment.

Companies Covered in Motor Graders Market

- Caterpillar Inc.

- Komatsu Ltd.

- John Deere

- XCMG Group

- Sany Heavy Industry

- Volvo Construction Equipment

- LiuGong Machinery

- BEML Limited

- CNH Industrial N.V.

- Mahindra Construction Equipment

- Veekmas

- Shantui Construction Machinery

- Dingsheng Tiangong Construction Machinery

- Mitsubishi Heavy Industries

- Terex Corporation

Frequently Asked Questions

The global motor graders market is projected to reach US$ 5.8 billion in 2026.

Ongoing infrastructure development, road construction and maintenance needs, and the replacement of aging fleets with more efficient, regulation-compliant machines are driving the market.

The market is poised to witness a CAGR of 9.4% from 2026 to 2033.

Key market opportunities arise from large-scale infrastructure projects in emerging economies, widening technology adoption, and growing demand for advanced, fuel-efficient graders in construction and mining.

Caterpillar Inc., Komatsu Ltd., John Deere, XCMG Group, and Sany Heavy Industry are some of the key players in the market.