- Rail

- Railway Traction Motors Market

Railway Traction Motors Market Size, Share, and Growth Forecast, 2025 - 2032

Railway Traction Motors Market By Technology Type (AC Traction Motors, Others), Application (Electric Locomotives, Diesel-Electric Locomotives, Others), Drive, End-user (Passenger Transit, Others), Sales Channel (OEM, Aftermarket), and Regional Analysis for 2025 - 2032

Railway Traction Motors Market Share and Trends Analysis

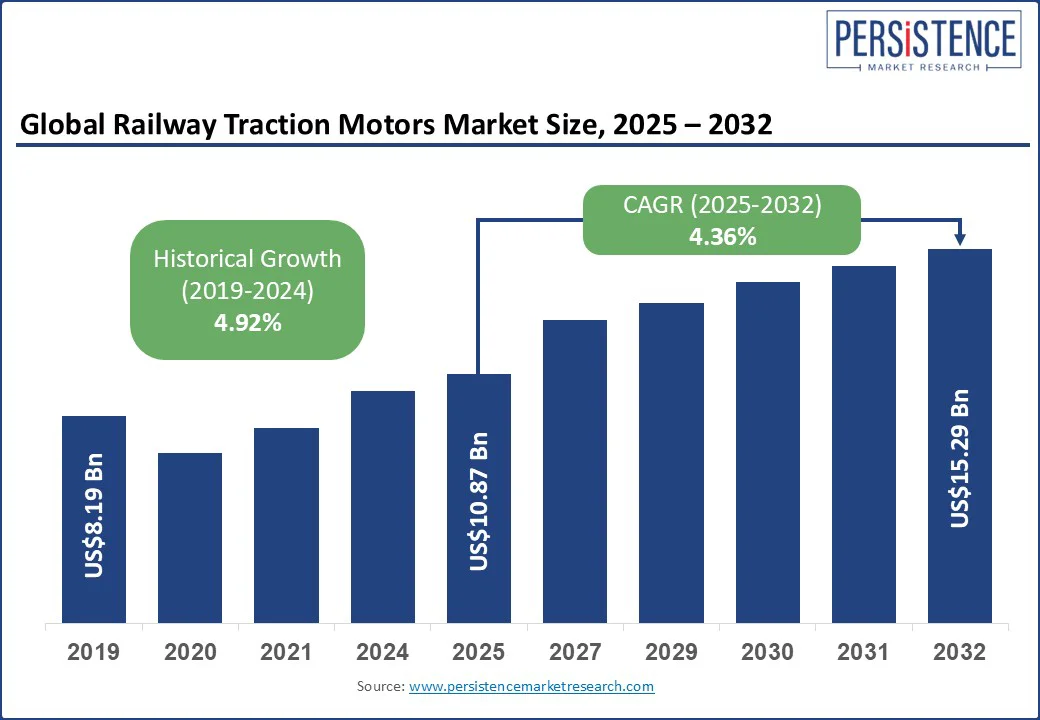

The global railway traction motors market size is projected to rise from US$10.87 Bn in 2025 to US$15.29 Bn by 2032. It is anticipated to witness a CAGR of 4.36% during the forecast period from 2025 to 2032.

As rail electrification and modernization accelerate globally, traction motors are increasingly positioned as technological and strategic enablers in the shift toward low-carbon mobility.

Railway traction motors power modern trains by converting electricity into motion. Advances in motor technology are improving energy efficiency and helping reduce costs and emissions. The market is growing thanks to expanding electrified networks, urban transit projects, and upgrades to older trains.

For example, Japan’s use of a new motor type has cut energy use by 20%, and Alstom is supplying traction systems for India’s Vande Bharat sleeper trains. There are strong opportunities in efficient motor designs, combined motor and inverter units, and smart maintenance systems.

Key Industry Highlights:

- Investment Focus: Growing investments in predictive maintenance and digital twin technologies are enabling operators to extend the asset life, optimize performance, and reduce downtime in traction motor systems.

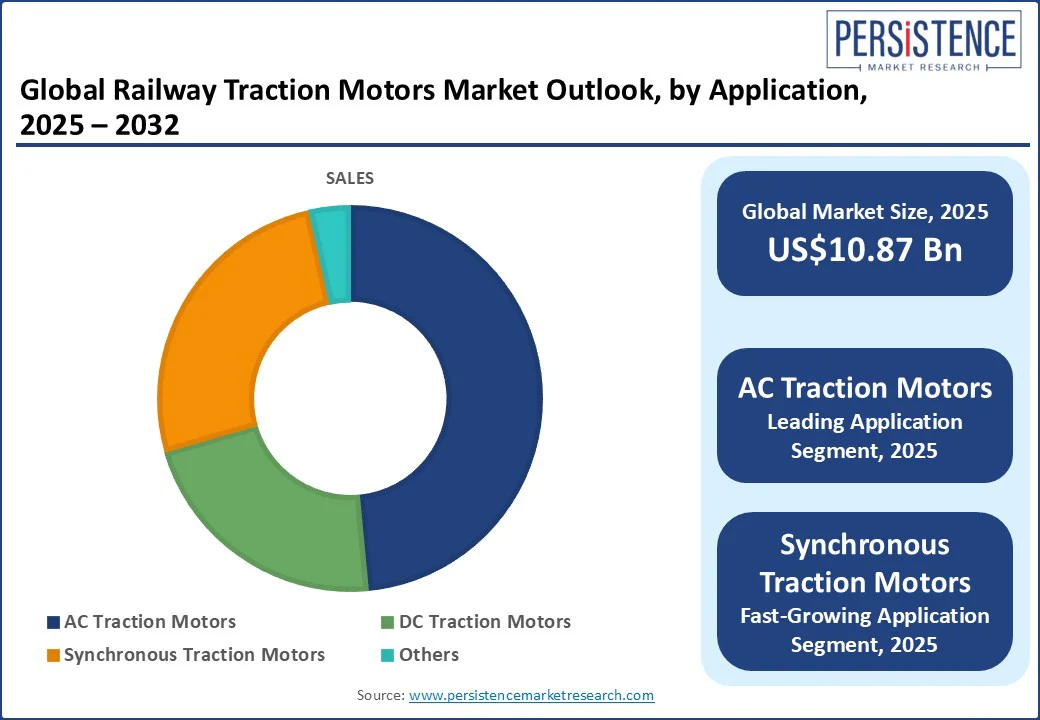

- Dominant Technology Segment: AC traction motors are expected to lead the market with a share of about 48.5% in 2025, on account of the industry-wide shift from legacy mechanical systems to inverter-fed AC drives, mainly SiC-enabled power electronics and sometimes insulated gate bipolar transistor (IGBT) systems.

- Fastest-growing Application Segment: The electric locomotives segment is projected to display the highest CAGR through 2032, fueled by large-scale electrification programs across emerging and developed economies.

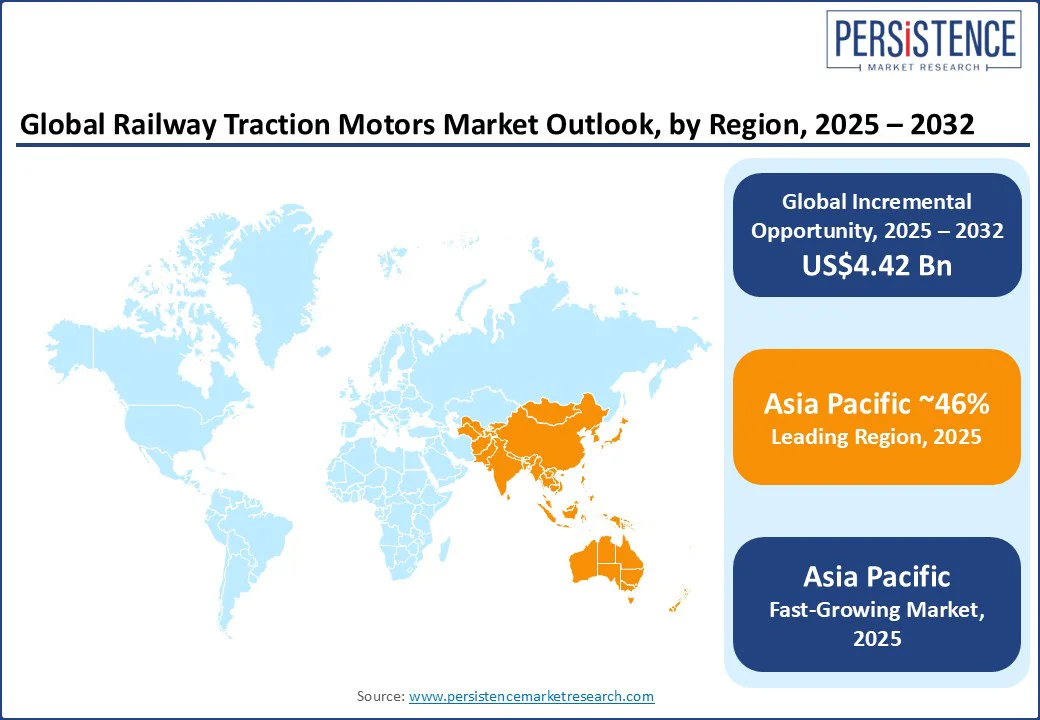

- Leading Regional Market: Asia Pacific is anticipated to be the dominant regional market, holding an approximate share of 46% in 2025 and exhibiting the highest CAGR through 2032, supported by China’s high-speed rail network expansion, India’s massive railway electrification drives, and Japan’s Shinkansen upgrades.

|

Global Market Attribute |

Key Insights |

|

Railway Traction Motors Market Size (2025E) |

US$10.87 Bn |

|

Market Value Forecast (2032F) |

US$15.29 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.36% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.92% |

Market Dynamics

Driver - Accelerating Rail Electrification Mandates to Stoke the Adoption of Advanced Traction Motors

The rising wave of rail electrification mandates and fleet modernization programs aimed at achieving net-zero transport emission targets. Governments from India to the European Union (EU) are aggressively prioritizing full or partial electrification of key corridors.

India aims to achieve 100% electrification of broad-gauge routes by 2030, a move projected to save over 10 billion liters of diesel annually. This policy momentum is directly catalyzing the demand for high-efficiency AC traction motors, permanent magnet synchronous motors, and integrated motor-inverter systems, as operators seek to improve energy efficiency by up to 20%.

This has already been demonstrated by Japan’s synchronous reluctance motor adoption in the Fukuoka Subway 4000-series. As is evident, electrification mandates have created immediate procurement needs for modern traction systems, which can unlock new possibilities in regional markets for railway traction technologies.

Restraint - Rise in Rare-Earth Costs and Logistical Challenges

The sharp rise in the cost and the constrained availability of rare-earth materials, especially neodymium and praseodymium, critical to the performance of PMSM systems, is proving to be a crippling impediment for the railway traction motors market.

Following China’s April 2025 export restrictions, industries globally are paying a staggering US$10-US$30 per kg premium, and in some cases up to 30% above Chinese pricing, to source magnets from suppliers such as Neo Performance Materials in Estonia.

The cost inflation entailing these supply chain bottlenecks has eroded the value proposition of advanced traction-motor technologies, forcing original equipment manufacturers (OEMs) and rail agencies to delay or scale down procurement of high-efficiency, low-maintenance permanent-magnet railway traction motors.

In extreme cases, reconsideration of rail electrification projects is also likely. As rare-earth prices soar and supply chains show fragility, the operational and environmental advantages of state-of-the-art traction systems are set to be compromised, injecting uncertainty into traction system procurement processes, inhibiting PMSM adoption, and complicating long-term service contracts.

Opportunity - Integration of SiC Power & IIoT to Produce New Revenue Streams for Market Players

The integration of silicon carbide (SiC)-based power electronics with motor-inverter modules and IIoT-enabled predictive maintenance services enhances system efficiency, reduces OEM and lifecycle costs, and unlocks recurring service revenues. SiC-based traction inverters significantly reduce switching losses and allow higher switching frequencies and compact cooling architectures, resulting in lighter, smaller traction units and measurable system-level energy savings.

According to a July 2024 article by Europe’s Rail, an EU body, European rail networks and semiconductor vendors are already validating traction SiC demonstrators and product roadmaps. The advantage this technological convergence offers is that when the inverter is tightly integrated with high-efficiency motor topologies into a packaged traction module, operators gain not only lower installed power losses but also simplified maintenance envelopes.

For instance, this packaging helped Alstom secure recent large traction-component and services contracts for Vande Bharat sleeper trainsets. Layering IIoT condition monitoring and AI-driven predictive maintenance on these modules converts one-time capital sales into high-margin, long-term service streams.

For market players, investing in supplier partnerships and product roadmaps that combine SiC-optimized inverters, compact PMSM/synchronous motor designs, and IIoT service platforms will deliver attractive returns during the forecast period 2025 - 2032.

Category-wise Analysis

Technology Type Insights

AC traction motors are expected to lead the market in terms of technology with a share of about 48.5% in 2025. These motors combine reliability, lower lifecycle maintenance, and compatibility with modern inverter-based propulsion systems, making them the default choice for new EMUs, metros, and mainline locomotives.

The prime driver for these railway traction motors is the industry-wide shift from legacy mechanical systems to inverter-fed AC drives, mainly SiC-enabled power electronics and sometimes insulated gate bipolar transistor (IGBT) systems, which improve mean time between failures and reduce total cost of ownership for operators.

The engineering of motor-inverter thermal co-design, strong growth in air- and liquid-cooled AC traction modules for high-power locomotives, and an aftermarket boom in AC retrofits for diesel-electric fleets are emerging as exciting trends for this segment.

Synchronous motors, especially PMSM and synchronous-reluctance types, deliver between 10% and 20% system energy gains compared to conventional induction machines, a fact recently substantiated by Japan’s Fukuoka Subway 4000-series.

The core growth determinant for synchronous motors is the combined effect of rail electrification drives across major economies and decarbonization imperatives declared by several governments that focus on making public transit networks cleaner, greener, and more sustainable.

Unique monetization opportunities in the form of developing technologies and models for rare-earth risk mitigation, integrating motor-inverter modules optimized for SiC switching, and securing premium service contracts for magnet lifecycle management await market players.

Application Insights

In the application category, electric multiple units (EMUs) are set to dominate with an approximate revenue share of 34% in 2025. Representing the central element of traction-motor demand because urbanization and sustainable mobility programs translate directly into high-volume fleet procurements, EMUs have rapidly emerged as the largest single application area in the railway traction motors market.

Alstom’s large Mitrac traction component supply for India’s Vande Bharat EMUs, along with the continued roll-out of new metro and suburban EMUs across Asia Pacific and Europe, demonstrate how rolling-stock programs are stimulating the demand for compact, high-torque motors and integrated motor-inverter modules.

The advent of EMUs has enabled operators to buy at scale while also pushing for the procurement of higher efficiency motor systems, such as PMSM and synchronous-reluctance.

Electric locomotives are anticipated to be the fastest-growing segment, exhibiting a high CAGR during the forecast period 2025-2032. The promising growth of this segment is powered by freight and heavy-haul electrification, that are accelerating procurement of high-power traction packages.

In regions where governments and large freight operators are committing to electrifying mainlines, such as the expansion of dedicated freight corridors (DFCs) in India, any improvement in the per-kilometer cost and consumption triggers a demand for high-end traction motors, advanced cooling systems, and inverter co-engineering.

The shift toward SiC-optimized motor-inverter systems for better system efficiency and a strong aftermarket for heavy-duty overhaul and condition-based spare parts are further enhancing the prospects of electric-powered locomotives.

Regional Insights

Asia Pacific Railway Traction Motors Market Trends

Asia Pacific is slated to command a dominant 46% of the railway traction motors market share in 2025, driven by rapid electrification of rail networks across India and China, heavy public and private investments in the modernization of existing rail technologies, and a surging demand for high-capacity, energy-efficient rolling stock.

For example, China’s Medium- and Long-Term Railway Network Plan and India’s Mission 100% Electrification by 2030 are boosting the implementation of high-performance AC traction motors and synchronous drive systems. Going further east, Japan’s consistent innovation in high-speed rail, including the Chuo Shinkansen Maglev, has further brightened the market outlook in the region.

Regional supply chains led by CRRC, Toshiba, and Hitachi Rail are fostering domestic manufacturing competitiveness, lowering procurement costs, and encouraging localization. The expanding adoption of railway traction motors is also getting amplified by the undertaking of urban transit projects across Indonesia, Thailand, and Australia, which are stoking the demand for compact, high-torque, and regenerative braking-enabled motor systems. Asia Pacific is also forecasted to showcase the highest CAGR of nearly 6% through 2032.

Europe Railway Traction Motors Market Trends

Expected to hold an approximate share of 31% in 2025, the Europe market for railway traction motors is driven by stringent EU decarbonization goals in public transit systems, aggressive electrification mandates, and rising investments in cross-border, high-speed rail corridors.

The European Green Deal and TEN-T Core Network projects, for example, are accelerating the deployment of next-generation traction systems, with Siemens Mobility and Alstom pushing advanced PMSM designs to enhance efficiency and reduce lifecycle costs.

Retrofitting of existing diesel-electric fleets with hybrid traction solutions in countries such as Germany, France, and the U.K. is gathering heat, helping operators meet emission targets while extending asset life. In addition, Europe’s focus on interoperable, digitalized rail systems, aided by the adoption of such solutions by the European Rail Traffic Management System (ERTMS), is generating demand for traction motors with smart diagnostics and predictive maintenance capabilities.

North America Railway Traction Motors Market Trends

The railway traction motors market in North America is supported by a well-established freight-centric rail network, increasing investment in urban transit modernization, and emerging high-speed rail initiatives. For instance, the U.S. Federal-State Partnership for Intercity Passenger Rail program and Canada’s High Frequency Rail project are expected to create high demand for advanced traction technologies on the continent.

Freight operators such as Union Pacific and Canadian National are also actively experimenting with battery-electric and hydrogen-powered locomotives, prompting suppliers to develop traction motors compatible with alternative propulsion architectures.

However, compared to Asia Pacific and Europe, the electrification rate in North America is much lower, which limits the large-scale adoption of next-gen traction motors and perpetuates the reliance of the sector on diesel-electric upgrades, hybrid retrofits, and specialized motors for metro and light rail expansion.

Competitive Landscape

The global railway traction motors market is experiencing a structural remodeling owing to supplier consolidation, vertical integration, and rapid technological differentiation. Major OEMs and suppliers are packaging motors, inverters, and long-term service contracts to win large-scale tenders, such as Alstom’s 2025 deal for India’s Vande Bharat train line.

Advancements in SiC power electronics are enabling lighter, more efficient traction systems, delivering operational savings, as validated by rail operators in Europe, while geopolitical risks around rare-earth minerals, heightened by China’s export controls, are pushing manufacturers toward low-rare-earth designs and diversified supply chains.

Market leaders such as Siemens Mobility and CRRC are integrating predictive maintenance, digital twins, and guaranteed availability agreements, converting one-off equipment sales into recurring, high-margin business streams emphasizing services.

Key Industry Developments

- In August 2025, Alstom unveiled the Traxx Universal electric locomotive for Romania’s Railway Reform Authority (ARF), with the first unit undergoing dynamic testing at the Faurei Centre. Designed for speeds up to 200 km/h and towing 16 passenger cars, it features Alstom’s advanced ERTMS for safe, efficient, and interoperable operation. The locomotive aims to enhance urban mobility and support Romania’s sustainable rail goals.

- In June 2025, CRRC, in partnership with Kazakhstan Temir Zholy, rolled out the CKD6H hybrid locomotive from its Ziyang facility for delivery to Kazakhstan. Built for Central Asia’s harsh climate, it features a "diesel engine + power battery" system with advanced digital and eco-friendly technologies, cutting CO2 emissions by about 240 tons annually. The locomotive is part of China’s new energy platform, with CRRC offering hybrid, electric, and hydrogen-powered options to suit diverse needs.

- In May 2025, Indian Railways unveiled the 9,000 HP WAG D-9 electric locomotive, built at the new Dahod workshop in Gujarat. Capable of hauling 4,600-5,800 tonnes at 120 km/h, it ranks among India’s most powerful freight engines. It features regenerative braking, IGBT-based propulsion, and the indigenous Kavach safety system. With 89% local components and renewable energy use, it supports India’s self-reliance and green manufacturing goals.

Companies Covered in Railway Traction Motors Market

- Alstom SA

- Siemens Mobility GmbH

- CRRC Corporation Limited

- Nidec Corporation

- Wabtec Corporation

- Hitachi Rail Limited

- Toshiba Corporation

- Mitsubishi Electric Corporation

- ABB Ltd.

Frequently Asked Questions

The railway traction motors market is projected to reach US$ 10.87 Bn in 2025.

The rising wave of rail electrification mandates and fleet modernization programs aimed at achieving net-zero transport emission targets is driving the market.

The market is poised to witness a CAGR of 4.36% from 2025 to 2032.

The pairing of SiC-based power electronics with integrated motor-inverter modules and the adoption of IIoT-enabled predictive maintenance services are key market opportunities.

Alstom SA, Siemens Mobility GmbH, and CRRC Corporation Limited are some of the leading players in this market.