- Chipsets & Processors

- Memory Market

Memory Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Memory Market by Technology (DRAM, SRAM, NAND Flash, NOR Flash, Emerging NVM, ROM & EPROM, Others), End-user (PC/Laptop, Data Center, Mobile, Consumer Products, Automotive, Others), by Regional Analysis, 2026 - 2033

Memory Market Size and Trend Analysis

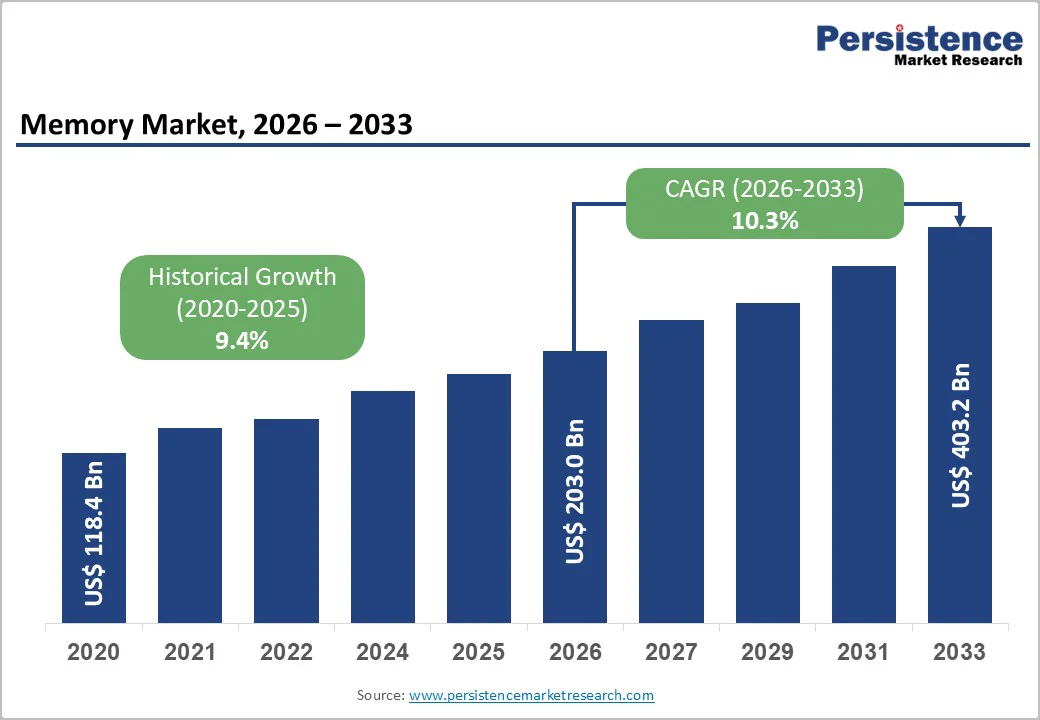

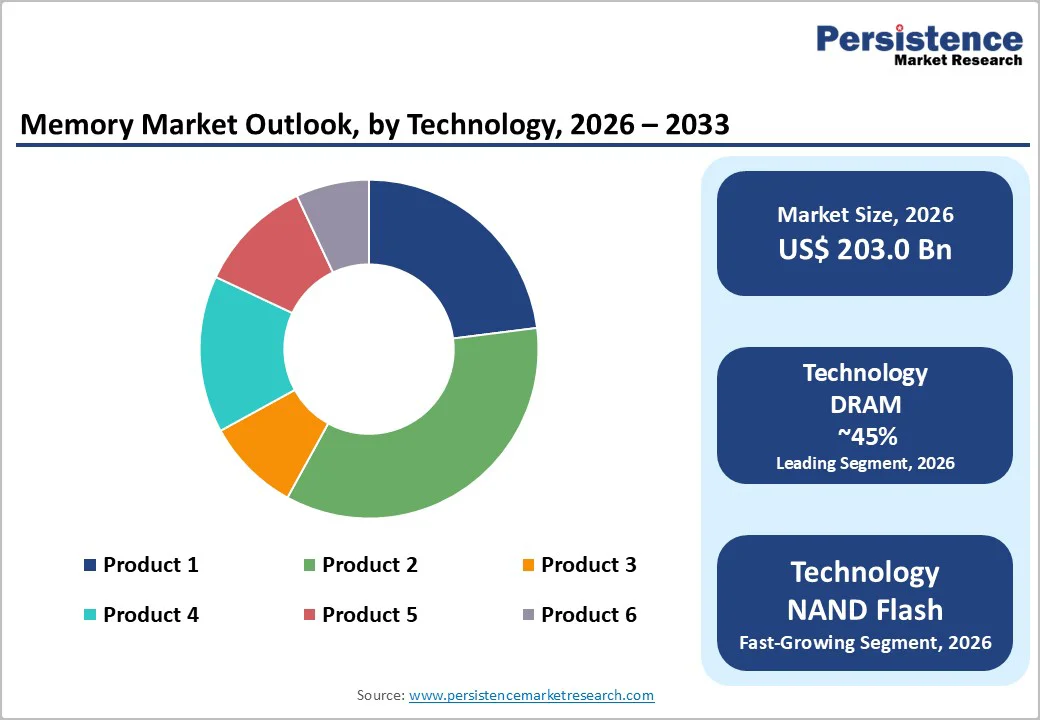

The global memory market size is likely to be valued at US$ 203.0 billion in 2026 and projected to reach US$ 403.2 billion by 2033, expanding at a CAGR of 10.3% between the forecast period 2026 and 2033.

Growth is fueled by accelerating AI adoption across data centers, cloud, and edge environments, alongside rising demand for advanced memory architectures such as High Bandwidth Memory (HBM) and 3D NAND. Supply constraints and manufacturers’ focus on AI-optimized memory solutions are further reshaping the industry, pushing leaders like SK Hynix, Samsung Electronics, and Micron Technology to scale production to meet hyperscale and enterprise demand.

Key Industry Highlights:

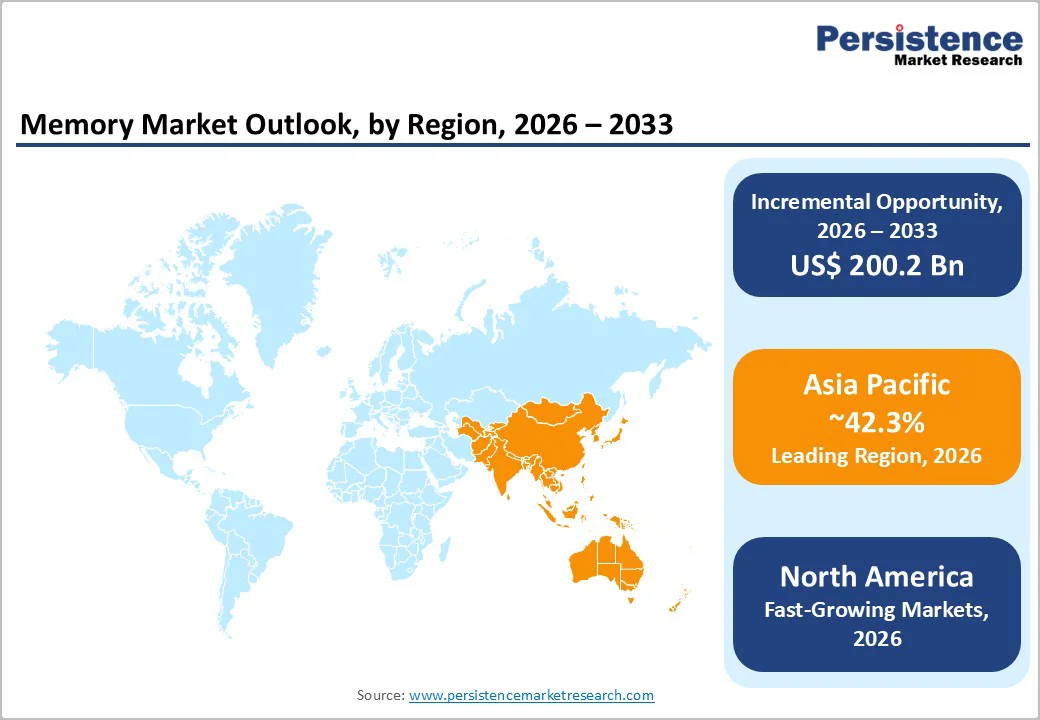

- Leading Region: Asia Pacific remains the dominant region, accounting for 42.3% of global memory market value, supported by concentrated manufacturing capacity and strong demand from consumer electronics and data center ecosystems.

- Fastest-Growing Region: North America records the highest growth momentum with a CAGR of 11.2%, driven by accelerating AI infrastructure investments and expanding domestic semiconductor programs.

- Dominant Technology Segment: DRAM leads the technology category with 45% market share, reinforced by growing adoption of DDR5 and HBM architectures across AI and high-performance computing workloads.

- Fastest-Growing End-User Segment: Data Centers represent the fastest-growing end-use segment, supported by AI workload expansion, server modernization cycles, and strong pricing dynamics extending through 2027.

- Key Market Opportunity: Automotive and edge computing applications offer major opportunities as vehicle memory content surges and IoT edge devices exceed 21.1 billion units, driving demand for specialized embedded memory solutions.

| Key Insights | Details |

|---|---|

| Memory Market Size (2026E) | US$ 203.0 Billion |

| Market Value Forecast (2033F) | US$ 403.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 10.3% |

| Historical Market Growth (2020 - 2025) | 9.4% |

Market Dynamics

Drivers - Explosive Demand for Artificial Intelligence Infrastructure

The global acceleration of artificial intelligence adoption is fundamentally reshaping memory market dynamics, with data-center memory demand expected to grow at an average annual rate of 33% through 2030. AI workloads demand extremely high bandwidth and low-latency performance, driving exceptional growth in High Bandwidth Memory (HBM). HBM shipments increased more than 200% in 2024 and are projected to rise another 70% in 2025 as training and inference models scale in complexity and size.

Major technology firms, including Microsoft, Google, ByteDance, and OpenAI, are aggressively securing long-term HBM supply to support expanding AI infrastructure. OpenAI’s letters of intent with Samsung Electronics and SK Hynix aim to lift production to nearly 900,000 HBM chips per month by 2029, more than doubling current global capacity. This structural demand-supply imbalance is expected to persist until at least 2027, supporting elevated pricing, utilization rates, and long-term revenue visibility for memory manufacturers.

Proliferation of Data-Intensive Computing Across Multiple Verticals

Memory requirements are rising sharply across consumer electronics, automotive platforms, and intelligent edge systems as industries accelerate digital transformation. Automotive memory consumption alone is increasing from about 90 GB per vehicle in 2025 to nearly 278 GB by 2026, with next-generation EVs and autonomous-ready systems potentially reaching 2 TB per vehicle. Meanwhile, smartphones now integrate up to 1 TB of onboard storage in flagship models to support high-resolution imaging, gaming, and AI-driven applications.

Beyond consumer and automotive, the expansion of 5G networks and IoT ecosystems continues to fuel incremental memory usage across billions of connected devices. Over 18.5 billion IoT devices were deployed globally in 2024, spanning smart manufacturing, home automation, healthcare monitoring, and industrial robotics. This broad-based, multi-sector growth provides diverse and resilient demand avenues for memory manufacturers, reducing reliance on traditional PC and server markets.

Restraint - Cyclical Supply Chain Disruptions and Production Capacity Constraints

The memory semiconductor industry remains highly cyclical, with production tightly limited by long facility construction timelines and high capital expenditure requirements. Building an advanced memory fabrication plant typically requires 24 to 36 months and an investment of US$ 5-10 billion, making rapid supply expansion nearly impossible during demand spikes. As AI-driven workloads surge, manufacturers are shifting production toward premium HBM and advanced DRAM, reducing the availability of conventional memory products essential for consumer electronics and legacy server applications.

Major players such as SK Hynix and Samsung Electronics are adopting cautious capacity expansion strategies due to concerns over a potential correction if AI infrastructure investments slow. This selective investment approach, combined with resource prioritization toward high-value memory types, has created a multi-year supply imbalance. While overall market growth remains strong, several downstream sectors face constrained supply conditions that limit their expansion potential despite robust demand.

Geopolitical Tensions and Trade Restrictions Impacting Manufacturing Diversification

Global memory manufacturing remains heavily concentrated in the Asia Pacific region, with South Korea alone representing roughly 70.5% of DRAM production and over 52.6% of NAND flash output. Rising geopolitical tensions, particularly U.S. export restrictions on advanced High Bandwidth Memory to China have intensified supply chain fragmentation. In response, Chinese manufacturers such as Yangtze Memory Technologies Co. (YMTC) are accelerating domestic development efforts, though they remain limited by restricted access to advanced lithography and fabrication equipment.

To mitigate supply-chain dependency risks, governments in the U.S. and Europe are advancing major semiconductor initiatives, including the CHIPS and Science Act and the European Chips Act, to stimulate local fabrication capacity. However, these new facilities require several years to achieve operational maturity. The resulting regional diversification, while necessary, increases duplication of investments, operational inefficiencies, and higher production costs, ultimately constraining overall industry profitability and competitiveness during the forecast period.

Opportunity - High-Capacity Storage Solutions for Cloud Infrastructure and Data Center Modernization

Data center storage architectures are undergoing major structural upgrades as hyperscalers migrate from legacy Hard Disk Drives (HDDs) to next-generation Solid State Drives (SSDs). Organizations are transitioning to high-density NAND-based SSDs such as 30TB and 60TB capacities to improve energy efficiency, reduce latency, and support rapidly expanding AI and machine-learning workloads. Advancements in Quad Level Cell (QLC) NAND and 1-terabyte die technologies are enabling higher storage density, lower power consumption, and optimized performance for large-scale cloud environments.

Rapid cloud expansion across emerging technology hubs globally is increasing demand for high-capacity memory modules for compute, storage, and AI inference workloads. These modernization initiatives represent long-term growth opportunities for memory manufacturers as enterprises implement cloud-first strategies, consolidate data centers, and deploy analytics platforms requiring sophisticated storage architectures.

Emerging Automotive and Edge Computing Applications Demanding Specialized Memory Solutions

The automotive semiconductor memory segment is evolving into one of the most dynamic application areas, driven by the rapid adoption of Advanced Driver Assistance Systems (ADAS), autonomous driving features, and software-defined vehicle architectures. Modern vehicles are integrating multicore processors and advanced compute platforms that require specialized memory solutions offering functional safety certifications, real-time responsiveness, and resilience under extreme environmental conditions.

Vehicle memory requirements continue to rise sharply as automotive software complexity escalates, with next-generation vehicles incorporating hundreds of millions of lines of code to support autonomous navigation, sensor fusion, and intelligent cockpit systems. In parallel, the expansion of IoT and edge computing ecosystems with billions of connected devices deployed globally is creating sustained demand for embedded memory optimized for low power consumption, compact form factors, and real-time data processing at the network edge. Combined, these trends are establishing significant multi-year opportunities for memory manufacturers developing automotive-grade and edge-optimized memory technologies.

Category-wise Analysis

Technology Insights

DRAM remains the leading technology category, accounting for about 45% of the global memory market in 2024. Its dominance stems from its essential role as the primary volatile memory across mobile, PC, and data-center computing ecosystems. Shipments continue to rise, supported by widespread DDR5 adoption and rapid scaling of High Bandwidth Memory. HBM’s share of overall DRAM bit capacity is rising steadily as AI workloads reshape memory architecture priorities.

High Bandwidth Memory represents the fastest-growing memory technology, driven by soaring AI, HPC, and accelerator-based computing requirements. Its exceptional bandwidth, energy efficiency, and close coupling with GPU and ASIC architectures make it the preferred choice for next-generation AI infrastructure. Leading suppliers are aggressively expanding HBM production footprints, with new HBM4 and HBM4E roadmaps accelerating multi-year growth. Increasing AI model complexity and inference scaling further strengthen the segment’s long-term trajectory.

End-user Insights

Data Centers represent the leading and most influential end-user category, expected to contribute around 35% of the total memory market value by 2033. The segment’s dominance is driven by hyperscaler adoption of HBM and DDR5 modules for AI clusters, cloud servers, and accelerated computing infrastructure. Replacement of legacy server fleets and rising deployment of GPU-dense architectures continue to elevate memory intensity per rack across global cloud regions.

AI and Machine Learning infrastructure emerges as the fastest-expanding end-user segment, characterized by unprecedented growth in memory bandwidth requirements and parallel compute workloads. Next-generation AI models require increasingly dense, energy-efficient memory pools to support large-scale training and inference. This segment’s momentum is reinforced by expanding AI data centers, rising model-as-a-service adoption, and continuous scaling of accelerator-based compute architectures across global technology ecosystems.

Regional Insights

North America Memory Market Trends

North America accounts for 31.5% of global memory demand, driven primarily by large-scale AI and cloud infrastructure investments concentrated in the United States. Hyperscalers such as Microsoft, Google, Meta, Amazon, and OpenAI continue expanding GPU and accelerator clusters that require high-density DRAM and HBM architectures. Government-backed initiatives under the CHIPS and Science Act are pushing major manufacturers to establish domestic fabrication capacity, reinforcing supply resilience and reducing dependence on Asia Pacific production hubs. These efforts have accelerated multi-billion-dollar investments across Arizona, New York, and Texas.

The region benefits from strong pricing leverage due to persistent HBM shortages and technology alignment between U.S. AI chip designers and memory suppliers. North America is positioned among the fastest-growing regional markets through 2033 as AI-related workloads scale and domestic fabs mature. Strategic autonomy measures, combined with elevated AI infrastructure spending, ensure sustained long-term demand for advanced memory technologies.

Europe Memory Market Trends

Europe’s memory market is expanding steadily, supported by a CAGR of 11.2% driven by increasing semiconductor demand across automotive, industrial automation, and cloud data center segments. The European Chips Act continues to fuel regional investment through large-scale funding programs, pilot lines, and localized semiconductor ecosystem development. While Europe remains heavily import-dependent for DRAM and NAND, local manufacturers such as Infineon Technologies and STMicroelectronics continue strengthening regional capabilities with new process technologies and capacity upgrades.

Growth is further supported by rising memory needs in next-generation vehicles and expanding cloud deployments. Although fabrication timelines remain long, Europe is steadily improving supply stability and reducing dependency on external suppliers for mid-range memory technologies.

Asia Pacific Memory Market Trends

Asia Pacific leads the global memory industry with 42.3% market share, driven by large-scale production in South Korea, China, Taiwan, and Japan. SK Hynix and Samsung Electronics dominate global DRAM and NAND output, while Chinese manufacturers like YMTC continue expanding despite export controls. The region also benefits from strong smartphone manufacturing, data center growth, and a highly integrated semiconductor supply chain that supports rapid scaling of advanced memory nodes.

Continued investment across emerging hubs such as India and Southeast Asia strengthens diversification and capacity expansion. Asia Pacific is expected to retain its leadership position as both manufacturing and consumption accelerate, supported by strong electronics demand and deep industry ecosystem advantages.

Competitive Landscape

The global memory semiconductor market is highly consolidated, with a small group of leading producers controlling nearly 85-90% of global output. These players dominate advanced segments such as high-performance DRAM, next-generation interfaces, and premium high-bandwidth solutions, benefiting from strong pricing power created by structural supply shortages and rapid AI-driven demand growth.

Smaller manufacturers operate in specialized or legacy product categories with limited participation in cutting-edge AI-optimized memory. Across the industry, companies are pursuing strategies such as capacity expansion, AI-tailored memory development, and investments in emerging non-volatile technologies to strengthen long-term competitiveness and address evolving computing architectures.

Key Market Developments

- In December 2025, SK Hynix declared that its entire High Bandwidth Memory (HBM) and conventional memory production for 2026 has been fully allocated to existing customers, signaling unprecedented supply constraints and elevated pricing power throughout the forecast period. The company indicated that memory shortages could persist until late 2027 as manufacturers struggle to expand production capacity sufficiently to meet escalating AI infrastructure demand from global hyperscalers and enterprise data centers.

- In October 2025, Samsung Electronics and SK Hynix signed preliminary letters of intent with OpenAI to supply approximately 900,000 High Bandwidth Memory chips monthly by 2029, representing more than double the current industry production capacity and validating long-term demand visibility for premium memory technologies supporting advanced AI applications across global infrastructure.

- In September 2025, SK Hynix announced the completion of validation and quality assurance for HBM4 high-bandwidth memory chips, positioning the company to commence mass production and reinforce its technological leadership in next-generation memory solutions with doubled bandwidth and 40% power efficiency improvements versus HBM3E predecessors.

Companies Covered in Memory Market

- Samsung Electronics

- SK Hynix

- Micron Technology

- Kioxia

- Western Digital

- Nanya Technology

- Winbond Electronics

- Macronix International

- GigaDevice Semiconductor

- YMTC

- Intel

- Toshiba

- Infineon Technologies

- MediaTek

- Texas Instruments

Frequently Asked Questions

The memory market is projected to reach US$ 403.2 billion by 2033, supported by strong AI, cloud, and automotive-edge computing demand.

AI hyperscale workloads especially soaring HBM demand are the primary growth drivers, supported by smartphones, automotive electrification, and expanding IoT devices.

DRAM leads with ~45% share, driven by its essential role across devices and rapid transition to DDR5 and HBM architectures.

Asia Pacific leads with over 45% market value, anchored by high production capacity across South Korea, China, and Japan.

Data-center upgrades to ultra-high-capacity SSDs and the sharp rise in automotive memory needs driven by ADAS and autonomous systems represent the strongest growth opportunities in the market.

Samsung Electronics, SK Hynix, Micron Technology, Kioxia, and Western Digital represent the dominant global competitors in the memory market.