- Semiconductor Materials & Components

- Non-volatile Memory Market

Non-volatile Memory Market Size, Share, and Growth Forecast 2026 - 2033

Non-volatile Memory Market by Product Type (Traditional Non-volatile Memory, Next-gen Non-volatile Memory, and Others), Wafer Size (200 mm, 300 mm, and 450 mm), End-user (Consumer Electronics, Enterprise Storage, Automotive and Transportation, Military and Aerospace, and Others), and Regional Analysis for 2026 - 2033

Non-volatile Memory Market Size and Share Analysis

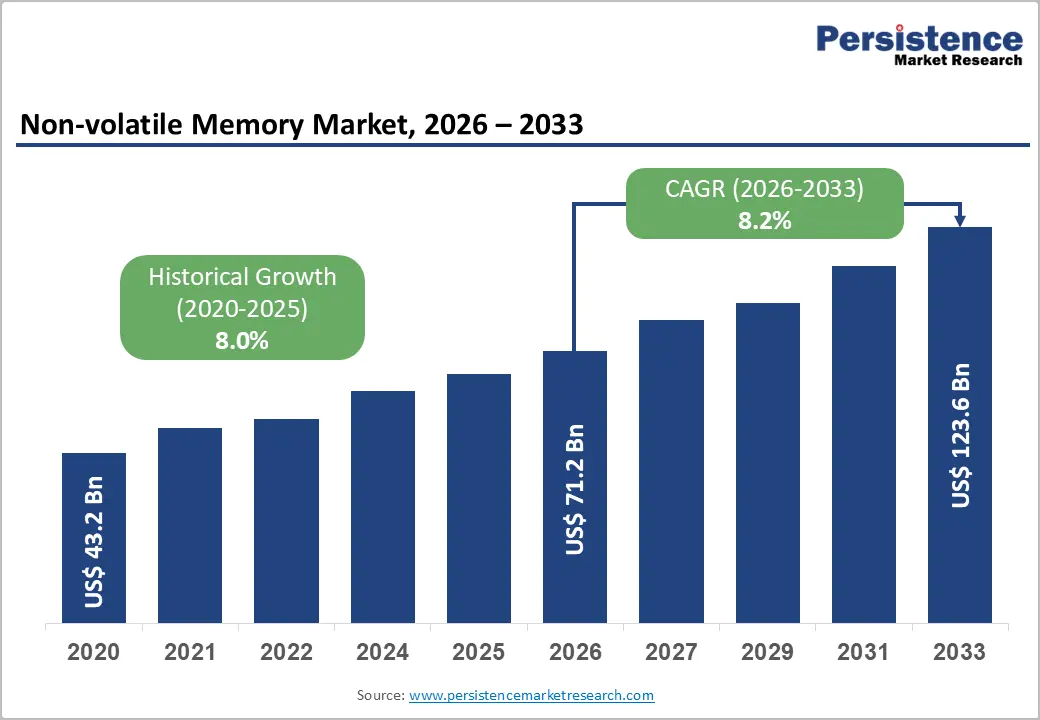

The global non-volatile memory market size is likely to be valued at US$ 71.2 billion in 2026 and is projected to reach US$ 123.6 billion by 2033, growing at a CAGR of 8.2% between 2026 and 2033. The market is experiencing robust expansion driven by the exponential surge in data generation from artificial intelligence (AI) and machine learning (ML) applications, combined with the proliferation of Internet of Things (IoT) devices and expanding cloud computing infrastructure globally.

Key Industry Highlights:

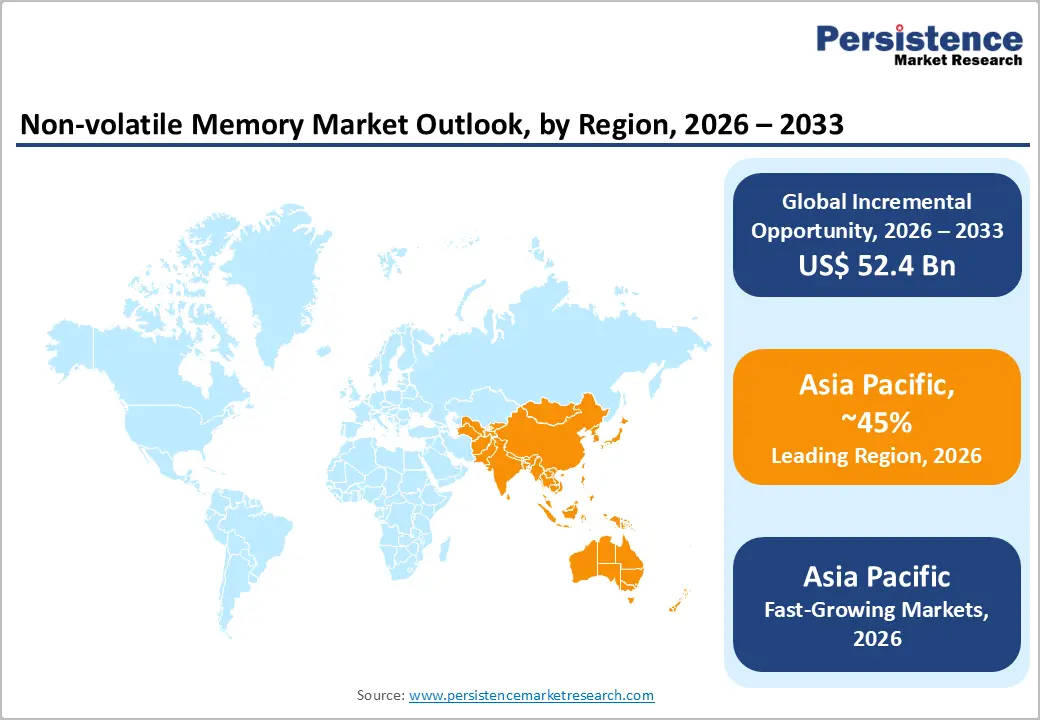

- Leading Region: Asia Pacific with 45% share dominate the global non-volatile memory market driven by manufacturing dominance in South Korea, Japan, China, and Taiwan, where companies including SK Hynix, Samsung, and emerging Chinese manufacturers are rapidly expanding production capacity and advancing next-generation technologies.

- Fastest Growing Region: Asia Pacific demonstrates fastest regional growth trajectory, through substantial artificial intelligence infrastructure investment, advanced data center proliferation, and government support via the U.S. CHIPS and Science Act.

- Dominant Product Type: Traditional flash memory dominates product category, representing approximately 65% market share through mature NAND and NOR technologies, with 3D NAND flash emerging as dominant architecture.

- Fastest Growing Product Type: Next-generation memory technologies experience accelerating commercialization, with MRAM, ReRAM, and PCM advancing toward volume production through strategic investments by major manufacturers and semiconductor foundries.

- Key Market Opportunity: Artificial intelligence and autonomous vehicle adoption represent key market opportunities, generating unprecedented demand growth through hyperscale data center expansion, automotive electronics proliferation, and edge computing deployment.

| Key Insights | Details |

|---|---|

|

Global Non-volatile Memory Market Size (2026E) |

US$ 71.2 Bn |

|

Market Value Forecast (2033F) |

US$ 123.6 Bn |

|

Projected Growth CAGR(2026-2033) |

8.2% |

|

Historical Market Growth (2020-2025) |

7.2% |

Market Dynamics

Drivers - Accelerating Demand from Artificial Intelligence and Data Centers

The robust growth of AI and large language models (LLMs) has fundamentally transformed memory market dynamics, with data centers representing the single largest consumption driver. According to industry analysis, demand for high-bandwidth memory (HBM) experienced growth exceeding 200% in 2024, with projections indicating an additional 70% expansion in 2026, as hyperscale cloud providers deploy thousands of GPU nodes requiring substantial memory resources.

Companies such as SK Hynix, Samsung Electronics, and Micron Technology are prioritizing HBM production to address critical demand from AI accelerators and data center operators, with SK Hynix alone reporting that HBM constituted 77% of its operating revenues in recent quarters. This trend demonstrates how emerging computational paradigms are reshaping memory allocation patterns, with organizations investing tens of billions in memory infrastructure to support machine learning training and inference operations that consume hundreds of gigabytes of DRAM and terabytes of flash storage per GPU node.

Rapid Expansion of Electric Vehicles and Automotive Electronics

The rapid global expansion of electric vehicles (EVs) and the increasing electronic content per vehicle are emerging as a powerful demand driver for the global non-volatile memory (NVM) market. Modern vehicles are evolving into software-defined platforms, integrating a wide array of electronic control units (ECUs), sensors, and data-processing systems that rely heavily on reliable, high-density non-volatile memory for data storage, logging, and real-time decision-making. EVs, in particular, require sophisticated battery management systems (BMS) to monitor cell health, thermal conditions, and charging cycles, all of which generate and store large volumes of data.

The adoption of advanced driver-assistance systems (ADAS), in-vehicle infotainment, digital instrument clusters, and over-the-air (OTA) software update capabilities is significantly increasing onboard data storage requirements. As a result, average vehicle storage demand has crossed 28 GB in 2025, reflecting a year-over-year growth of more than 20%, and this figure is expected to rise further as autonomous driving features advance. Non-volatile memory technologies, such as NAND flash, NOR flash, and emerging automotive-grade EEPROM solutions, are becoming indispensable in this environment due to their ability to retain critical data without power, ensure fast boot times, and support frequent read/write cycles.

Automotive applications also impose stringent reliability and safety requirements, including extended operating temperature ranges, long product lifecycles, functional safety compliance (ASIL), and resistance to vibration and electromagnetic interference. To address these needs, memory manufacturers are investing in automotive-qualified NVM solutions that meet AEC-Q100 standards and support higher endurance and data integrity. The global push toward electrification, stricter emission regulations, and government incentives for EV adoption are further accelerating vehicle production volumes and electronic content per vehicle, directly translating into sustained demand growth for non-volatile memory.

Restraints - Supply Chain Disruptions and Manufacturing Capacity Constraints

The semiconductor industry faces persistent supply chain vulnerabilities that limit non-volatile memory growth, with critical inputs including borates and silicon wafers concentrated in a handful of geographically vulnerable regions. The United States has insufficient domestic capacity for 60% of materials and chemicals essential for front-end wafer manufacturing, requiring an estimated $9 billion in capital investments to achieve supply chain independence. Multiple fab projects initiated between 2021 and 2022 have experienced delays, with TSMC's $40 billion Arizona facility now delayed until 2028, creating short-to-medium-term capacity constraints that restrict market growth and drive component pricing escalation across industries dependent on memory solutions.

Intense Price Competition and Margin Compression

Memory manufacturers face severe pricing pressure as commodity NAND flash and DRAM markets experience cyclical oversupply conditions, with prices expected to experience volatility due to divergent supply-demand dynamics across product categories. The transition from DDR4 to DDR5 memory and PCIe 4.0 to PCIe 5.0 storage solutions creates temporary production slowdowns that increase per-unit manufacturing costs while simultaneously limiting pricing power. Companies must invest substantially in research and development to advance next-generation technologies while managing profitability amid fierce competition from consolidated global manufacturers, creating margin compression challenges that inhibit investment in emerging memory technologies and limit expansion by smaller specialized players.

Opportunity - Rapid Commercialization of Next-Generation Non-Volatile Memory Technologies

Emerging memory technologies including MRAM (magnetoresistive RAM), ReRAM (resistive RAM), PCM (phase-change memory), and FeRAM (ferroelectric RAM) are advancing toward volume production with significant commercial potential. GlobalFoundries launched its 22FDX+ RRAM technology in August 2025, specifically targeting wireless connectivity and AI applications with enhanced energy efficiency. Samsung Electronics demonstrated MRAM-based in-memory computing capabilities achieving 98% accuracy in handwritten digit classification, while actively developing 14 nm, 8 nm, and 5 nm embedded MRAM technologies scheduled for production between 2024 and 2027.

These advanced memory solutions offer superior speed, endurance, and energy efficiency compared to traditional flash memory, presenting substantial opportunities for companies pioneering commercial deployment in edge computing, autonomous vehicles, and next-generation data center architectures where traditional memory technologies reach fundamental scaling limitations. Growing foundry support and ecosystem maturity, spanning IP vendors, EDA tools, and automotive/industrial qualification standards, are accelerating design adoption and reducing time-to-market risks for OEMs. As manufacturing yields improve and costs decline, these memories are expected to transition from niche deployments to mainstream system architectures, enabling new revenue pools and higher-margin opportunities for early movers in advanced non-volatile memory commercialization.

Growing Integration into Edge Computing and IoT Ecosystems

Edge computing and IoT applications represent the fastest-growing deployment vectors for non-volatile memory, with embedded systems requiring compact, energy-efficient, and high-endurance memory solutions. Industrial IoT devices, smart home appliances, and connected automotive systems increasingly integrate sophisticated memory architectures to enable local data processing, reduce cloud dependency, and support real-time decision-making at network edges. Microchip Technology, Adesto Technologies, and emerging startups are developing specialized non-volatile memory products optimized for power-constrained embedded environments, capturing substantial market share from traditional microcontroller applications.

Government initiatives including the European Chips Act (mobilizing over €80 billion in investments) and the U.S. CHIPS and Science Act are accelerating development of resilient memory manufacturing ecosystems specifically targeting edge computing and IoT applications, creating significant commercial opportunities for memory suppliers capable of delivering innovative solutions addressing emerging computational paradigms.

Category-wise Analysis

Product Type Insights

Traditional non-volatile memory, particularly flash memory (encompassing NAND and NOR variants), maintains dominant market position with approximately 65% market share, driven by mature manufacturing processes, established supply chains, and widespread application across consumer electronics, enterprise storage, and data centers. 3D NAND flash memory technology has emerged as the dominant flash architecture, with over 72% of production featuring 128+ layers in 2023, increasing from 46% in 2021.

Samsung Electronics introduced its 8th-generation V-NAND with 236 layers in early 2024, delivering 2TB storage capacity in single-chip configurations with 15% improved write speed and 22% enhanced energy efficiency compared to previous-generation designs. The sustained dominance of traditional flash memory reflects its cost-effectiveness, manufacturing maturity, and suitability for high-volume consumer applications, although next-generation technologies are capturing increasing share in specialized high-performance segments requiring superior speed or endurance characteristics.

Wafer Size Insights

The 300mm wafer segment dominates manufacturing capacity with approximately 64% market share, representing the preferred manufacturing platform for high-volume memory production due to its capacity to yield 2.3 times more chips per wafer compared to 200mm wafers, significantly reducing per-unit manufacturing costs. Leading semiconductor foundries including TSMC, GlobalFoundries, and Samsung Electronics have standardized 300mm wafer processing for advanced memory architectures including MRAM and 3D XPoint, with industry projections indicating that 300mm wafer capacity will reach 70.4% of total fabrication infrastructure by 2026.

The 200mm wafer segment is experiencing resurgence growth at 9.7% CAGR due to widespread industry adoption for cost-effective memory solutions in embedded systems, consumer electronics, and IoT devices, where foundries are repurposing legacy 200mm fabrication facilities to capture demand for power chips and microprocessors requiring specialized manufacturing processes. This bifurcated market structure reflects the distinct requirements of high-volume commodity memory production versus specialized embedded memory applications, with both segments contributing substantially to total market value and demonstrating complementary growth trajectories through 2032.

End-user Insights

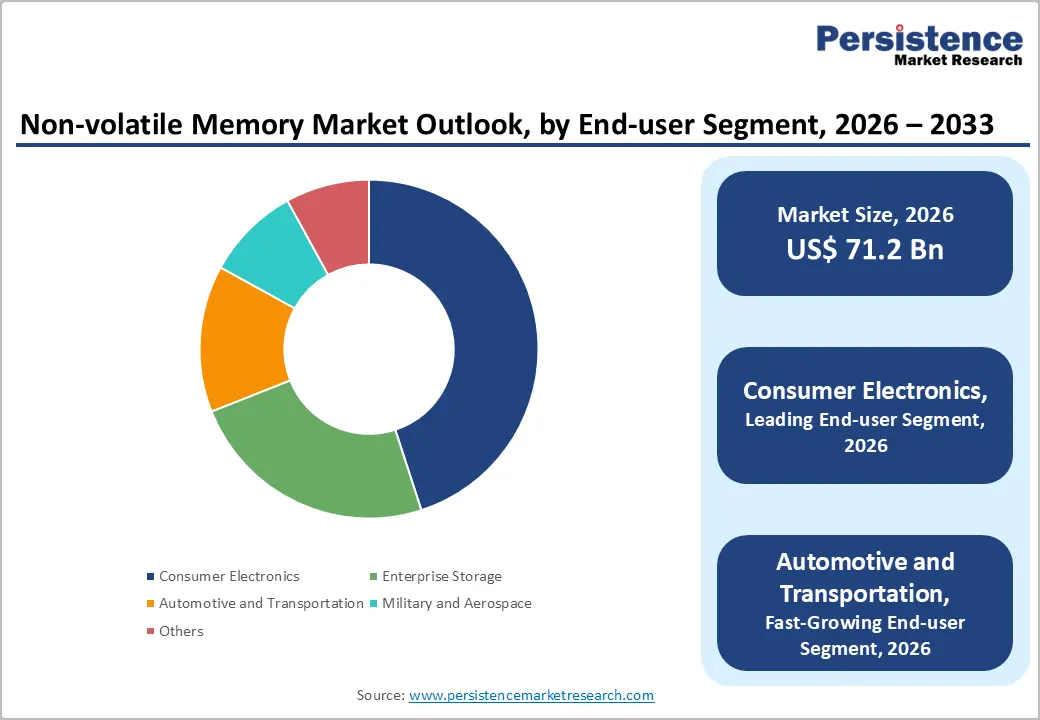

Consumer electronics continues to dominate the global non-volatile memory market, accounting for approximately 45% of total demand. This segment is driven by the sustained proliferation of smartphones, laptops, tablets, wearable devices, and portable gaming consoles, all of which increasingly rely on high-density non-volatile memory to support advanced operating systems, high-resolution content, AI-enabled features, and always-on connectivity. Rising consumer expectations for faster boot times, seamless multitasking, high-definition video storage, and extended device lifecycles are pushing OEMs to integrate higher-capacity NAND and NOR flash solutions, reinforcing the segment’s leadership position in overall market share.

Automotive and transportation applications represent the fastest-growing end-user segment, with a projected CAGR of 10.7% through 2033. Growth is being fueled by rapid electric vehicle adoption, expanding deployment of advanced driver-assistance systems (ADAS), and progress toward autonomous driving. Modern vehicles incorporate dozens of electronic control units and software-driven platforms that require reliable, high-endurance embedded non-volatile memory for real-time data processing, secure firmware storage, and over-the-air updates.

Regional Insights

North America Non-volatile Memory Market Trends

North America is emerging as the fastest-growing regional market with projected 9.1% CAGR through 2033, driven by substantial investments in artificial intelligence infrastructure, advanced semiconductor manufacturing, and government support through the U.S. CHIPS and Science Act. The region houses leading memory manufacturers including Intel, Micron Technology, and Western Digital, supported by world-class research institutions and a robust innovation ecosystem developing next-generation memory technologies.

U.S. government initiatives are actively incentivizing domestic semiconductor production and R&D funding, attracting significant capital investment toward localized fab construction and advanced technology development, with CHIPS Act funding allocating billions toward strengthening regional semiconductor competitiveness and supply chain resilience. The region's dominance in AI and cloud computing, concentrated demand from major hyperscale tech companies, and substantial government support position North America as the primary driver of next-generation memory technology adoption.

Europe Non-volatile Memory Market Trends

Europe is undertaking comprehensive semiconductor ecosystem strengthening through the European Chips Act, which has mobilized over €80 billion in public and private investments targeting semiconductor manufacturing and research infrastructure development. Germany has become a focal point for semiconductor investment, with the European Commission approving €623 million in state aid supporting GlobalFoundries and X-FAB semiconductor manufacturing facilities, representing strategic efforts to reduce regional dependence on imported memory chips and strengthen supply chain resilience.

France, the United Kingdom, and Spain are actively supporting semiconductor research initiatives, with emphasis on advanced packaging technologies, 300mm wafer processing, and specialized memory solutions for automotive and industrial applications. European governments are implementing regulatory harmonization mechanisms and coordinating crisis response systems to monitor semiconductor supply chains, ensuring continued access to critical memory components for automotive manufacturers, industrial electronics producers, and healthcare technology providers across the region, positioning Europe as increasingly self-sufficient in memory production capabilities.

Asia Pacific Non-volatile Memory Market Trends

Asia Pacific maintains commanding global market dominance accounting nearly 45% of the share, with manufacturing capacity concentrated in China, Japan, South Korea, and Taiwan, representing over 80% of worldwide NAND flash production. South Korea's Samsung Electronics and SK Hynix maintain industry-leading positions in memory technology development, with SK Hynix announcing completion of HBM4 development and preparing for mass production, delivering double the bandwidth and 40% improved power efficiency compared to previous-generation specifications.

Japan's Kioxia and Tokyo Electron continue advancing 3D NAND technology development, with Kioxia and Western Digital unveiling next-generation 3D flash memory achieving 4.8Gb/s interface speed and 59% improved bit density through 332-layer architecture innovations. China is aggressively pursuing semiconductor self-sufficiency through the "Made in China 2025" initiative allocating $150 billion toward domestic semiconductor capabilities, with companies including SMIC achieving breakthroughs in 7nm production and reducing import dependence.

Competitive Landscape

The non-volatile memory market is characterized as moderately consolidated, dominated by several global manufacturers including Samsung Electronics, SK Hynix, Micron Technology, Toshiba/Kioxia, and Western Digital, collectively controlling approximately 85% of global flash memory and DRAM production capacity. These established manufacturers pursue differentiated strategies emphasizing 3D NAND advancement, next-generation memory technology commercialization, and vertical integration to secure manufacturing capacity and raw material access.

Emerging competitors including Adesto Technologies, Crossbar Inc., Panasonic, and Fujitsu are gaining market share in specialized next-generation memory segments (ReRAM, MRAM, FeRAM) through focused research initiatives and strategic partnerships with semiconductor foundries including TSMC, GlobalFoundries, and UMC. Strategic differentiation focuses on energy efficiency, endurance characteristics, speed performance, and cost optimization, with companies investing substantially in research and development to advance emerging memory architectures addressing specific application requirements in artificial intelligence, edge computing, and automotive sectors.

Key Market Developments

- In September 2025, SK Hynix Completes HBM4 Development SK Hynix announced successful completion and quality assurance validation of its HBM4 high-bandwidth memory chips, positioning the company for mass production and establishing substantial competitive advantage in AI memory solutions with superior bandwidth and power efficiency characteristics.

- In February 2025, Kioxia and Western Digital Unveil Next-Generation 3D Flash Memory Kioxia and Western Digital pioneered advanced 3D flash memory technology featuring 4.8Gb/s NAND interface speed, 10-34% enhanced power efficiency, and 59% improved bit density through revolutionary CMOS directly bonded to array (CBA) technology, setting new performance benchmarks for enterprise and data center applications.

- In August 2025, GlobalFoundries Launches 22FDX+ RRAM Technology GlobalFoundries introduced 22FDX+ RRAM technology specifically engineered for wireless connectivity and AI applications, delivering improved energy efficiency and significantly faster operational speeds compared to traditional memory solutions, addressing accelerating demand for specialized memory in edge computing and wireless infrastructure segments.

Companies Covered in Non-volatile Memory Market

- Samsung Electronics

- Toshiba Corporation

- Micron Technology

- SK Hynix

- Western Digital

- Adesto Technologies

- Intel Corporation

- Microchip Technology

- Nantero

- Crossbar Inc.

- HDD Manufacturers

- Japan Semiconductor Corporation

- Fujitsu Ltd.

- Honeywell International Inc.

- Rohm Co. Ltd.

Frequently Asked Questions

The global non-volatile memory market is projected to expand from US$ 71.2 billion in 2026 to US$ 123.6 billion by 2033, representing substantial growth opportunity across emerging memory technologies and established memory segments.

Artificial intelligence infrastructure proliferation, machine learning workload expansion, electric vehicle adoption, IoT device proliferation, cloud computing infrastructure development, and digital transformation initiatives across industries are the dominant demand drivers.

Traditional flash memory, encompassing NAND and NOR technologies, maintains dominant market position with approximately 65% share, driven by mature manufacturing processes, cost-effectiveness, and widespread application.

North America demonstrates the fastest growth rate with 9.1% CAGR, driven by artificial intelligence infrastructure investment and government support.

Next-generation memory technology commercialization (MRAM, ReRAM, PCM, FeRAM) and edge computing ecosystem integration represent the most substantial growth opportunities, particularly in automotive, aerospace, and industrial IoT segments.

Samsung Electronics, SK Hynix, Micron Technology, Toshiba/Kioxia, Western Digital, Intel Corporation, and emerging specialists, including Adesto Technologies, Crossbar Inc., Panasonic, and Fujitsu, maintain dominant competitive positions.