- Metals & Minerals

- Shape Memory Alloys Market

Shape Memory Alloys Market Size, Share, and Growth Forecast 2026 - 2033

Shape Memory Alloys Market by Product Type (Nickel Titanium-Based (Nitinol), Copper based, Iron-Manganese-Silicon, Others), Application (Biomedical, Automotive, Aerospace & Defense, Consumer Electronics, Home Appliances), and Regional Analysis, 2026 - 2033

Shape Memory Alloys Market Size and Trend Analysis

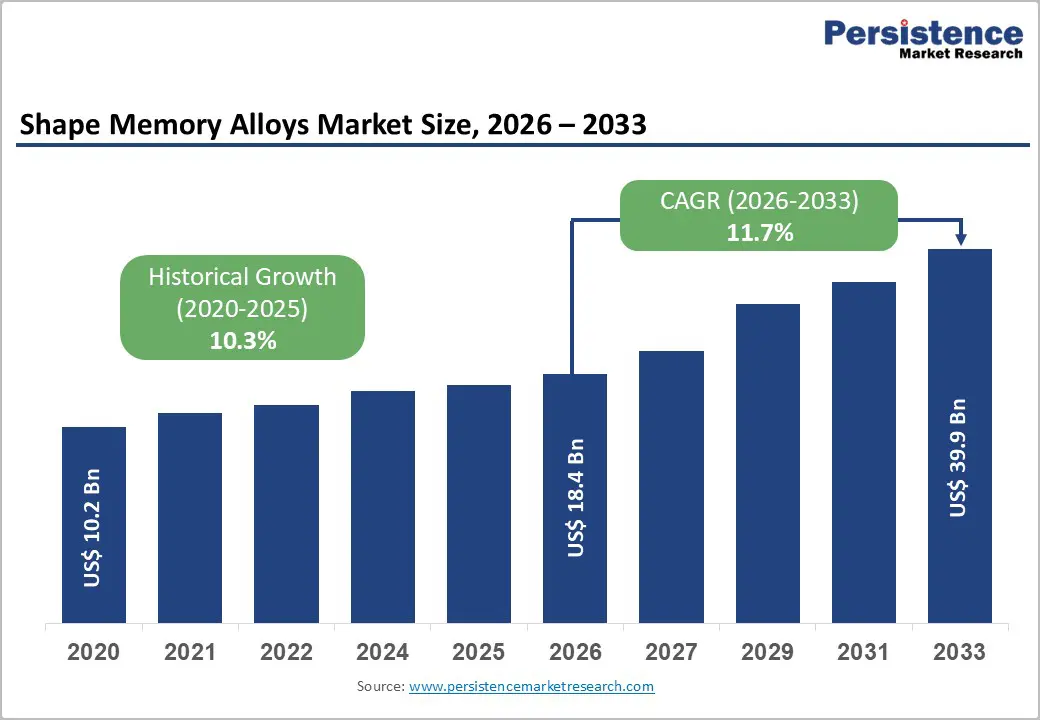

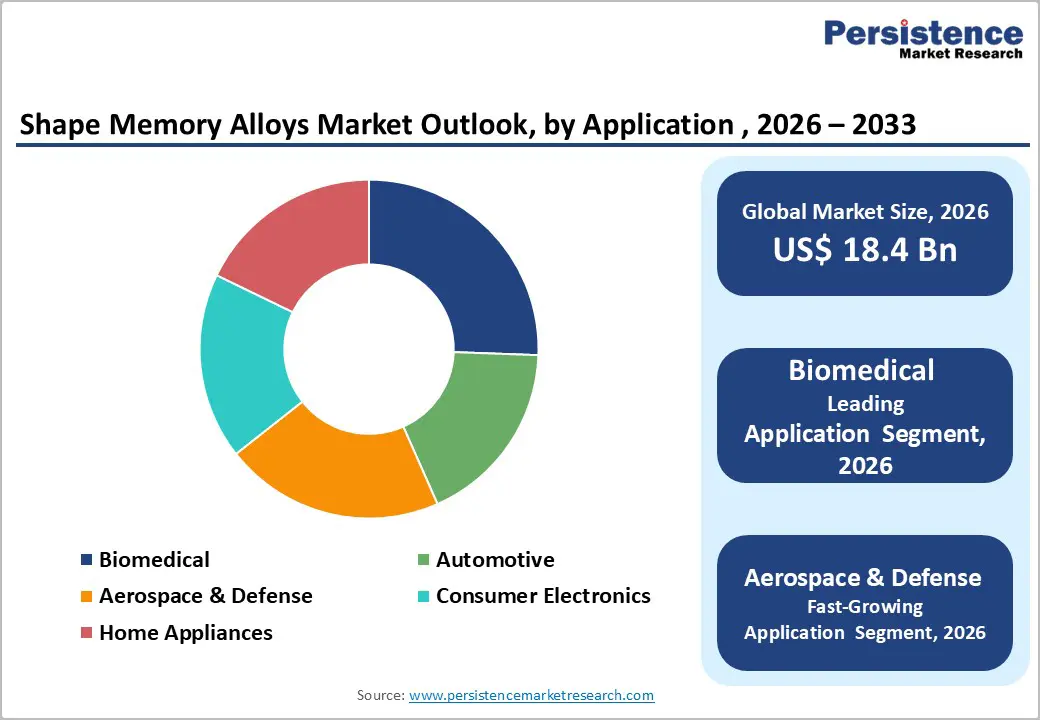

The global shape memory alloys market size is expected to be valued at US$ 18.4 billion in 2026 and projected to reach US$ 39.9 billion by 2033, growing at a CAGR of 11.7% between 2026 and 2033.

Growth is driven by rising demand for high-performance materials across the biomedical, aerospace, and automotive industries. Shape memory alloys, particularly Nitinol, offer superelasticity, corrosion resistance, and biocompatibility, enabling minimally invasive surgical devices and precision actuators. In aerospace, lightweight, adaptive components enhance fuel efficiency and structural optimization, as supported by NASA research.

Key Industry Highlights:

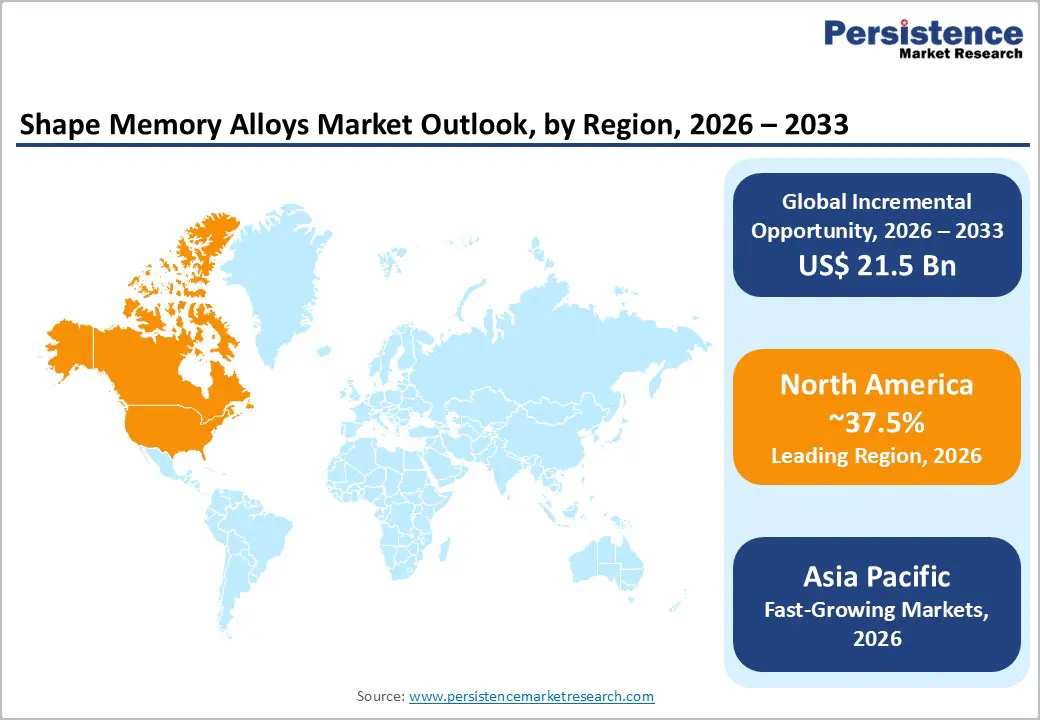

- Leading Region: North America leads the Shape Memory Alloys market with a 37.5% share, supported by strong U.S. R&D capabilities, regulatory backing from the FDA, and advanced aerospace and biomedical innovation.

- Fastest Growing Region: Asia Pacific holds a 30.3% market share and remains the fastest-growing region, driven by expanding manufacturing capacity in China and advanced aerospace research initiatives in Japan.

- Leading Product: Nitinol dominates the product segment with a 65% share in 2025, owing to its superior biocompatibility, corrosion resistance, and widespread use in precision medical devices.

- Leading Application: Biomedical applications account for 45% of the total market share, driven by strong demand for minimally invasive devices, including cardiovascular stents and orthopedic implants.

- Key Opportunity: Aerospace morphing and adaptive structure technologies present a major opportunity, supported by ongoing research programs and increasing adoption of lightweight, high-performance smart materials.

| Key Insights | Details |

|---|---|

| Shape Memory Alloys Size (2026E) | US$ 18.4 billion |

| Market Value Forecast (2033F) | US$ 39.9 billion |

| Projected Growth CAGR (2026 - 2033) | 11.7% |

| Historical Market Growth (2020 - 2025) | 10.3% |

Market Dynamics

Drivers - Expanding Adoption of Shape Memory Alloys in Advanced Biomedical Devices

The expanding integration of shape memory alloys (SMAs) in biomedical devices is a major market driver, particularly in minimally invasive procedures. Their superelasticity, corrosion resistance, and biocompatibility make them ideal for vascular stents, guidewires, and orthodontic archwires. Nitinol is widely preferred for its fatigue resistance and reliable shape recovery at body temperature.

Rising cardiovascular disease prevalence, highlighted by data from the World Health Organization, continues to increase demand for interventional treatments. Regulatory approvals from agencies such as the U.S. Food and Drug Administration for self-expanding stents further support commercialization. These factors collectively strengthen investments in SMA-based medical innovation and sustained industry expansion.

Growing Demand for Lightweight and High-Performance Materials in Aerospace and Automotive Sectors

Shape memory alloys are increasingly adopted in aerospace and automotive applications due to their lightweight properties and high work density. In aircraft systems, SMAs enable compact actuators and adaptive components that enhance aerodynamic efficiency. NASA-led research initiatives have explored SMA-based morphing structures for performance optimization.

In the automotive sector, SMAs are used as smart actuators in emission control systems and thermal management components. Regulatory frameworks, including CO2 emission standards set by the European Commission, encourage the integration of lightweight materials. Certification processes overseen by the Federal Aviation Administration further validate SMA reliability in high-performance environments.

Restraints - High Manufacturing Complexity and Raw Material Price Volatility Increasing Overall Production Costs

The production of shape memory alloys involves complex vacuum melting, precision thermo-mechanical processing, and stringent quality control, significantly increasing manufacturing costs compared to conventional alloys. Alloys such as Nitinol require tight compositional control to maintain transformation temperatures and superelastic performance. This complexity restricts large-scale cost efficiency, particularly for price-sensitive consumer electronics applications.

In addition, raw material price volatility, especially nickel traded on the London Metal Exchange, creates cost uncertainty for manufacturers. Fluctuations in nickel supply directly impact alloy pricing structures. These elevated and unstable input costs limit broader scalability and constrain adoption in mass-market industrial segments.

Limited Fatigue Life Under Cyclic Loading Restricting Use in High-Durability Applications

Despite their functional advantages, shape memory alloys exhibit limited fatigue life under repeated cyclic loading compared to traditional engineering metals. Industry evaluations from the SAE International indicate that high-cycle automotive systems often require durability beyond typical SMA cycle thresholds. This performance limitation restricts use in continuously dynamic mechanical environments.

In automotive and industrial automation systems requiring long service life, premature fatigue may increase maintenance frequency and lifecycle costs. As a result, manufacturers must incorporate design redundancies or alternative materials for high-load components, slowing adoption in applications demanding extreme durability and long-term structural reliability.

Opportunity - Expanding Biomedical Innovation and Aging Demographics Creating Strong Long-Term Demand Potential

Ongoing biomedical innovation presents significant growth opportunities for shape memory alloys, particularly in next-generation implants, prosthetics, and minimally invasive surgical tools. Nitinol continues to gain traction due to its biocompatibility, corrosion resistance, and superelastic behavior. Increasing regulatory clearances from the U.S. Food and Drug Administration are supporting the commercialization of advanced SMA-based medical devices.

Demographic trends further strengthen this opportunity. According to projections from the United Nations, the global population aged 60 and above is expected to expand substantially by 2050, increasing demand for orthopedic implants and assistive devices. In parallel, research funding from the National Institutes of Health continues to accelerate innovation in advanced biomaterials.

Rising Adoption of Morphing Structures and Adaptive Systems in Aerospace and Defense

The development of morphing and adaptive aerospace structures presents a promising avenue for the deployment of shape memory alloys. NASA research programs are evaluating SMA-enabled components that enhance aerodynamic performance and reduce structural weight. These smart materials support drag reduction, noise control, and improved fuel efficiency in next-generation aircraft platforms.

Defense modernization initiatives further expand opportunities. Global military expenditure tracked by the Stockholm International Peace Research Institute highlights sustained investment in advanced materials and smart systems. As aerospace and defense manufacturers prioritize efficiency and performance, SMAs are increasingly positioned as enabling materials for adaptive flight and high-performance actuation technologies.

Category-wise Analysis

Product Type Insights

Nickel-titanium-based alloys, particularly Nitinol, dominate the product landscape, accounting for an estimated 65% market share in 2025. Their leadership stems from superior corrosion resistance, biocompatibility, and stable superelastic response under physiological conditions. Regulatory clearances from the U.S. Food and Drug Administration continue to support widespread adoption in medical-grade components.

Iron-based shape memory alloys are emerging as the fastest-growing product category, especially in civil engineering and infrastructure reinforcement. Their cost efficiency and high load-bearing capability make them suitable for seismic damping and structural retrofitting applications. Increasing infrastructure modernization initiatives globally are accelerating research and pilot deployments of iron-based SMAs in large-scale construction projects.

Application Insights

Biomedical applications lead the market with an estimated 45% share, driven by extensive use of SMAs in cardiovascular, orthopedic, and dental devices. According to the American Heart Association, millions of minimally invasive cardiovascular procedures are performed annually, supporting strong demand for Nitinol-based stents and guidewires that enhance recovery outcomes and procedural precision.

Aerospace and defense represent the fastest-growing application segment, supported by the increasing integration of smart materials in adaptive flight systems. NASA research initiatives are exploring SMA-enabled morphing structures and compact actuators. As aircraft manufacturers focus on efficiency and weight optimization, demand for high-performance SMA components continues to expand across advanced aerospace platforms.

Regional Insights

North America Shape Memory Alloys Market Trends

North America leads the global shape memory alloys market, accounting for approximately 37.5% of the total share. The United States drives regional dominance through strong innovation in aerospace, defense, and medical devices. Research initiatives led by NASA and advanced manufacturing capabilities of companies such as Fort Wayne Metals strengthen technological leadership in Nitinol processing.

A well-established regulatory ecosystem further accelerates commercialization. Approvals and quality standards overseen by the U.S. Food and Drug Administration support rapid integration of SMA-based medical devices. In parallel, research funding from the National Institutes of Health continues to encourage biomaterial innovation, reinforcing North America’s leadership position.

Europe Shape Memory Alloys Market Trends

Europe is a technologically advanced market and is projected to grow at a steady CAGR of 12.1%, driven by strong demand in automotive and aerospace. Germany remains a regional innovation hub, with applied research organizations such as the Fraunhofer Society advancing smart materials for mobility and industrial automation. Export competitiveness is reinforced by regulatory alignment under the European Chemicals Agency framework.

Sustainability policies further influence market expansion. Aviation decarbonization initiatives promoted by the European Union Aviation Safety Agency align with broader European climate objectives, encouraging the adoption of lightweight materials. Growing emphasis on emission reduction and green mobility solutions continues to support SMA integration across aerospace and advanced automotive platforms.

Asia Pacific Shape Memory Alloys Market Trends

Asia Pacific holds an estimated 30.3% share of the global market and remains the fastest-growing regional segment. China plays a central role in Nitinol manufacturing capacity and supply chain expansion, supported by industrial modernization initiatives. Japan contributes through aerospace and advanced materials research programs led by the Japan Aerospace Exploration Agency.

Rapid industrialization across China, India, and Southeast Asia is expanding demand for medical devices, consumer electronics, and smart infrastructure. Government-backed manufacturing initiatives and export-driven production strategies are strengthening regional competitiveness. As healthcare access and aerospace investments grow, the Asia Pacific continues to emerge as a critical production and consumption hub for shape memory alloys.

Competitive Landscape

The global shape memory alloys market is moderately consolidated, with leading players focusing on technological differentiation and vertical integration to strengthen their competitive positioning. Companies emphasize high material purity standards, advanced vacuum melting processes, and precision thermo-mechanical treatment to enhance performance reliability. Continuous improvement in transformation temperature control and fatigue resistance remains central to product innovation strategies.

Strategic initiatives include joint ventures, long-term supply agreements, and collaborative research partnerships to expand application capabilities. Many manufacturers allocate a significant portion of revenue toward research and development to support next-generation biomedical and aerospace solutions. Additionally, sustainability initiatives, recycling of alloy scrap, and energy-efficient production models are becoming key competitive differentiators.

Key Developments:

- In January 2025, researchers introduced a new titanium-aluminum-chromium (Ti-Al-Cr) shape memory alloy tailored for space environments, offering enhanced thermal stability and oxidation resistance to support next-generation aerospace structures and deep-space mission components.

- In March 2024, SAES Getters S.p.A. announced a 25% expansion in its Nitinol production capacity to address rising global demand from medical device manufacturers and aerospace component suppliers, strengthening its advanced materials manufacturing footprint.

- In June 2023, Fort Wayne Metals partnered with NASA to advance lunar-grade Nitinol applications, focusing on high-reliability shape memory components designed to withstand extreme temperature variations and structural demands in upcoming space exploration missions.

Companies Covered in Shape Memory Alloys Market

- SAES Getters S.p.A.

- ATI Inc.

- Confluent Medical Technologies

- Fort Wayne Metals

- Nitinol Devices & Components

- Dynalloy Inc.

- Johnson Matthey

- Furukawa Electric Co., Ltd.

- Nippon Steel Corporation

- Nippon Seisen Co., Ltd.

- Memry Corporation

- Ultimate NiTi Technologies, Inc.

- Baoji Seabird Metal Materials Co., Ltd.

- Admedes GmbH

- Euroflex GmbH

Frequently Asked Questions

The shape memory alloys market size is valued at US$ 18.4 billion in 2026, driven by strong biomedical demand and aerospace innovation.

Demand is primarily driven by Nitinol-based medical devices holding 65% product share and increasing aerospace research supported by regulatory and R&D ecosystems.

North America leads the market with a 37.5% share, supported by advanced U.S. innovation, regulatory frameworks, and biomedical research funding.

Asia Pacific, holding a 30.3% share, is the fastest-growing region due to expanding manufacturing capacity and aerospace material advancements.

Aerospace morphing and adaptive structural technologies represent a major growth opportunity supported by ongoing smart material research initiatives.

Key market players include SAES Getters S.p.A., ATI Inc., Confluent Medical Technologies, and Fort Wayne Metals.