- Pharmaceuticals

- Male Infertility Market

Male Infertility Market Size, Share, and Growth Forecast, 2026 – 2033

Male Infertility Market by Test Type (Conventional Semen Analysis, Computer-Assisted Semen Analysis (CASA), Others), Treatment Type (Medication Therapy, Assisted Reproductive Technology (ART), Others), End-User (Hospitals, Fertility Clinics, Others), and Regional Analysis for 2026 - 2033

Male Infertility Market Share and Trends Analysis

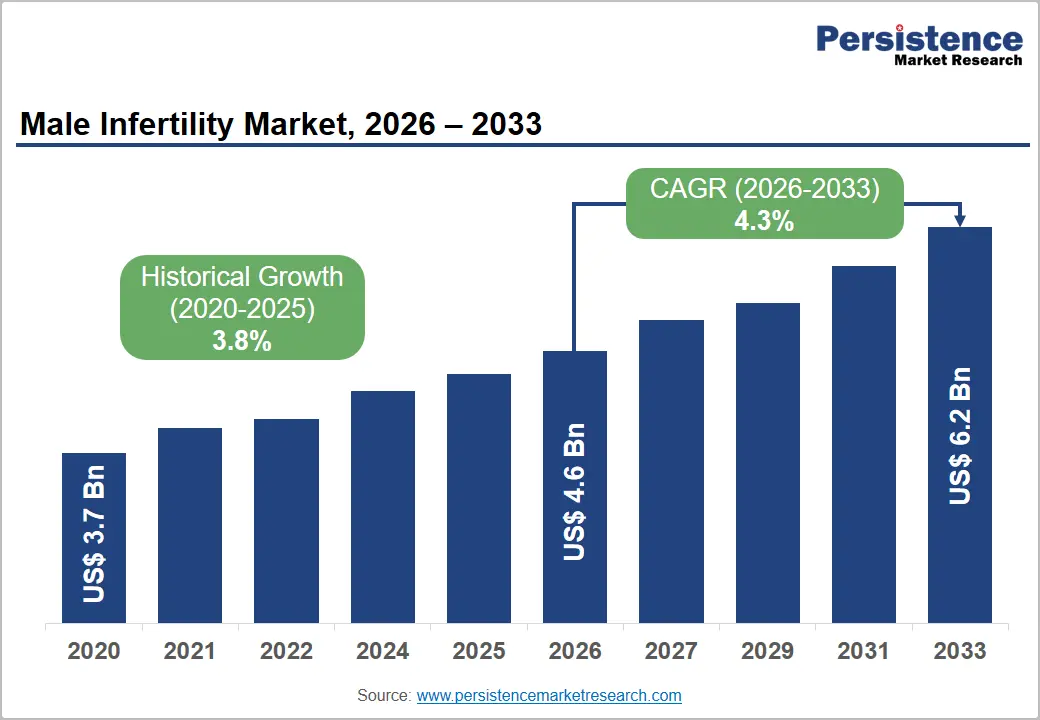

The global male infertility market size is likely to be valued at US$4.6 billion in 2026 and is estimated to reach US$6.2 billion by 2033, growing at a CAGR of 4.3% during the forecast period from 2026 to 2033, driven by demographic shifts toward delayed parenthood, which extends exposure to lifestyle factors that impair reproductive health.

Regulatory frameworks promote standardized diagnostic protocols and expand access to assisted reproductive services in key regions. Technology adoption in semen analysis and genetic testing improves detection accuracy and treatment selection.

Key Industry Highlights:

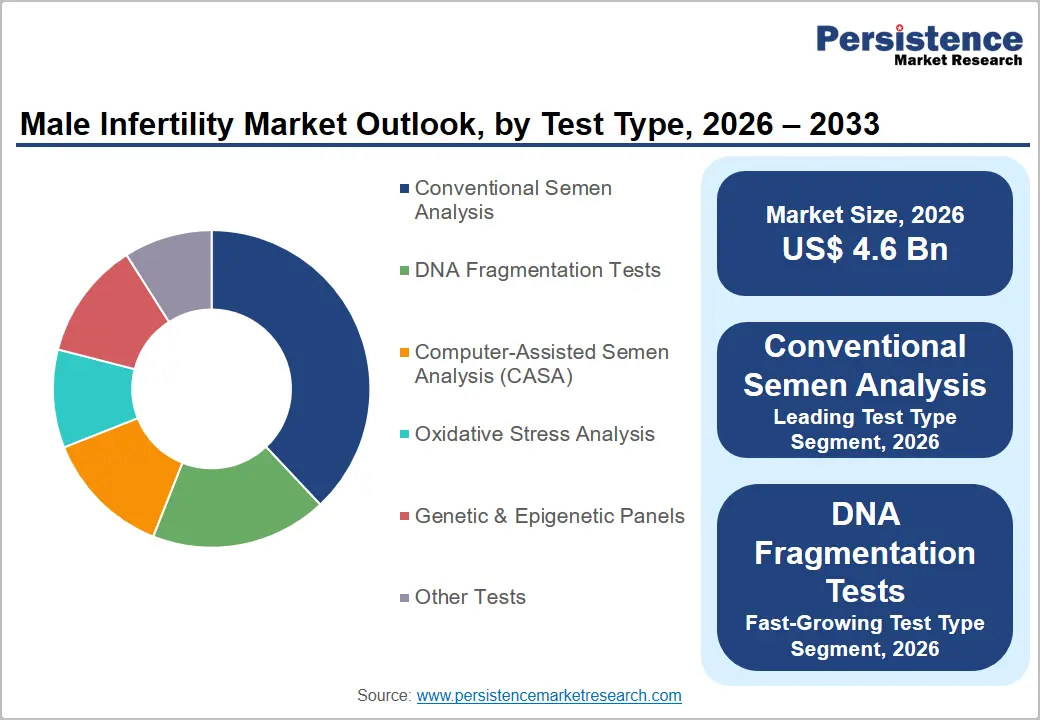

- Leading Test Type: Conventional semen analysis is set to hold approximately 38% revenue share in 2026, driven by broad clinical accessibility and established reimbursement coverage across major markets.

- Fastest-Growing Test Type: DNA fragmentation tests are projected as the fastest-growing segment, supported by rising integration into routine male infertility workup protocols at specialized fertility centers.

- Leading Treatment Type: Assisted reproductive technology (ART) is estimated to hold roughly a 42% revenue share in 2026, driven by high procedural volume in ICSI and IVF cycles addressing severe male factor infertility.

- Fastest-Growing Treatment Type: Hormone therapy is forecast to record the fastest growth, driven by expanding clinical identification of hypogonadism as a primary treatable cause of male infertility.

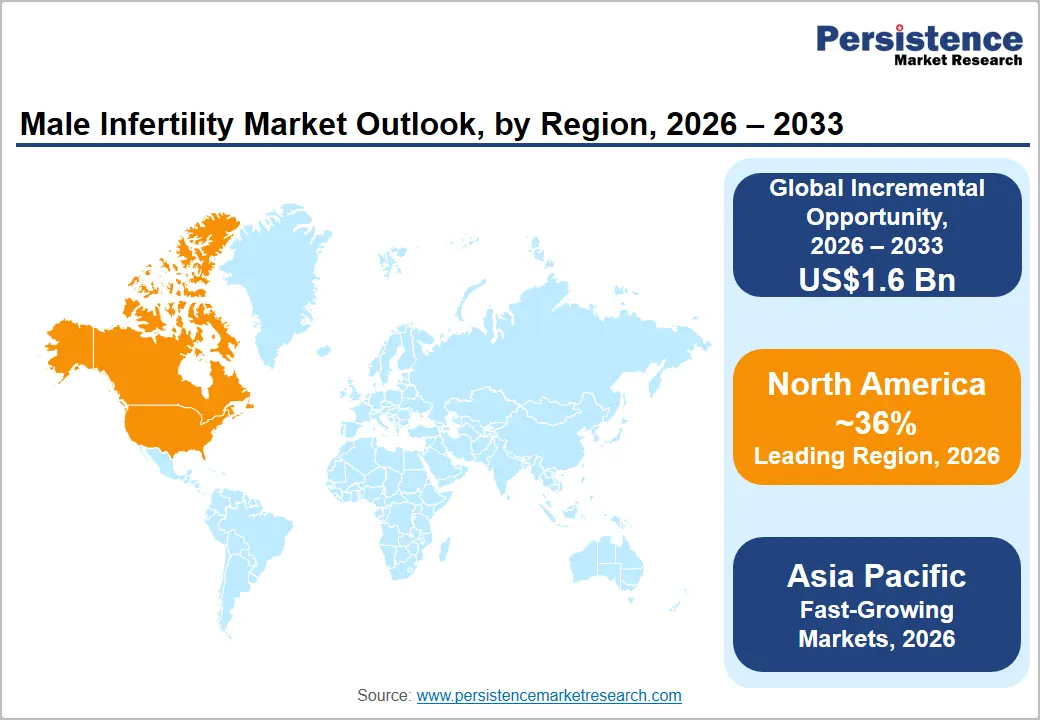

- Regional Leadership: North America is projected to capture approximately 36% of the global market share in 2026, driven by mature fertility infrastructure and progressive FDA regulatory clearances for advanced diagnostic platforms.

DRO Analysis

Driver - Rising Prevalence of Male Reproductive Disorders and Lifestyle-Related Fertility Challenges

The growing incidence of obesity, diabetes, smoking, excessive alcohol consumption, environmental toxin exposure, and delayed parenthood is contributing to declining sperm quality and reproductive health outcomes. Healthcare providers are witnessing increased demand for fertility evaluations among men seeking family planning support. Greater public awareness regarding male reproductive health is encouraging earlier diagnosis and clinical intervention, supporting sustained demand for diagnostic testing and treatment services.

According to the U.S. Centers for Disease Control and Prevention (CDC), adult obesity prevalence exceeded 40.3% during the national assessments conducted from August 2021 to August 2023, highlighting a significant risk factor associated with hormonal imbalance and impaired reproductive function. The rising prevalence of metabolic disorders is increasing the need for fertility assessments, laboratory testing, and specialized therapeutic interventions, creating long-term demand across fertility care networks and reproductive medicine providers.

Restraint - High Cost of Advanced Fertility Testing and Treatment

Advanced diagnostic procedures, genetic testing panels, and assisted reproductive interventions involve significant expenditure, creating affordability challenges for many patients. Limited reimbursement coverage across several healthcare systems restricts access to comprehensive fertility evaluation and treatment services, reducing patient conversion rates and slowing the adoption of premium diagnostic technologies.

Cost-intensive laboratory infrastructure, highly trained specialists, and sophisticated testing equipment increase operational expenditure for healthcare providers. These factors create pressure on profitability and restrict scalability, particularly among smaller fertility centers seeking expansion into underserved markets.

Opportunity - Expansion of Genetic and Precision Fertility Diagnostics

Growing understanding of genetic factors associated with infertility is creating opportunities for broader deployment of molecular diagnostics and personalized treatment pathways. Healthcare providers are increasingly integrating genetic screening into fertility assessments to identify underlying reproductive abnormalities. This approach supports earlier intervention and more targeted therapeutic strategies, improving overall clinical effectiveness.

Investment in genomic technologies, artificial intelligence-enabled interpretation tools, and laboratory automation can create scalable diagnostic ecosystems. Regulatory support for precision medicine programs and ongoing advances in reproductive genetics are expected to strengthen the adoption of personalized fertility management solutions, expanding revenue opportunities for diagnostic developers and fertility service providers.

Category-wise Analysis

Test Type Insights

Conventional semen analysis is expected to lead the male infertility market, accounting for approximately 38% of revenue share in 2026. Its widespread adoption stems from low procedural cost, established clinical protocols, and broad insurance reimbursement. Quest Diagnostics, for instance, offers standardized semen analysis panels across its U.S. laboratory network. Accessibility in both hospital-based labs and independent diagnostic centers sustains consistent volume generation across diverse healthcare settings.

DNA fragmentation tests are likely to represent the fastest-growing segment, propelled by growing clinical recognition of sperm DNA integrity as a determinant of ART success. Rising rates of unexplained infertility and recurrent pregnancy loss are directly increasing clinical demand, while declining reagent costs are making these tests more viable for routine deployment across mid-tier fertility centers.

Treatment Type Insights

Assisted reproductive technology (ART) is projected to lead the market, capturing around 42% of the revenue share in 2026. ART encompasses In Vitro Fertilization (IVF), Intracytoplasmic Sperm Injection (ICSI), and sperm retrieval procedures that address severe male factor infertility cases where other treatments are insufficient. Clinics such as Boston IVF have deployed ICSI as the primary treatment pathway for azoospermia patients. High procedural revenue per cycle and increasing clinical referral rates from diagnostic centers sustain the dominant revenue position of this segment.

Hormone therapy is likely to be the fastest-growing segment, fueled by increasing identification of hypogonadism and hormonal dysregulation as treatable causes of male infertility. Endocrinology departments at major academic medical centers, including Mayo Clinic, have expanded male reproductive endocrinology programs. Rising awareness among general practitioners of hormonal etiologies and the availability of targeted pharmacological agents are expanding the treatable patient population within this segment at an accelerating rate.

End-user Insights

Fertility clinics are likely to be the leading segment with a projected 45% of the male infertility market share in 2026 due to their specialized infrastructure, dedicated andrology laboratories, and high concentration of reproductive medicine specialists. CARE Fertility in the U.K. and Reproductive Medicine Associates in the U.S. exemplify networks with integrated diagnostic and treatment capabilities. The concentration of both diagnostic equipment and ART procedure volume within these facilities drives disproportionate revenue contribution relative to other care settings.

Diagnostic centers are anticipated to be the fastest-growing segment, fueled by increasing outsourcing of male fertility diagnostics from general hospitals and the proliferation of specialty pathology networks. Companies such as SRL Diagnostics in India are expanding male reproductive health test menus across urban and peri-urban center networks. Cost-efficiency advantages, shorter patient turnaround times, and the absence of procedure-based overhead make these centers an attractive access point for initial male fertility screening and follow-up monitoring.

Regional Insights

North America Male Infertility Market Trends

North America is anticipated to be the leading region, accounting for a market share of 36% in 2026, driven by a mature fertility care infrastructure, high rates of diagnostic adoption, and progressive reimbursement frameworks across major U.S. states. The FDA regulatory environment supports rapid commercialization of novel diagnostic platforms and ART ancillary technologies.

U.S. Male Infertility Market Insights

The U.S. is projected to account for approximately 86% of North America market revenue in 2026, supported by a dense network of accredited fertility clinics and high out-of-pocket healthcare spending capacity. The American Society for Reproductive Medicine (ASRM) guideline updates in 2024 formally expanded male fertility testing recommendations, driving laboratory procurement cycles.

Canada Male Infertility Market Insights

Canada is expected to represent nearly 14% of the North America market in 2026. Demand is supported by increasing public awareness of reproductive health and the expansion of fertility treatment programs. Growth in advanced diagnostic testing capabilities and rising utilization of genetic screening services are strengthening clinical adoption.

Europe Male Infertility Market Trends

Europe is projected to account for 29% of the market in 2026, supported by established reproductive healthcare systems, increasing fertility treatment utilization, and strong regulatory oversight for reproductive medicine. Growth in molecular diagnostics and genetic testing services is enhancing diagnostic precision. Expansion of fertility clinic networks and ongoing investment in reproductive research programs are contributing to market development.

Germany Male Infertility Market Insights

Germany is forecast to contribute approximately 22% of the Europe market in 2026. Strong healthcare infrastructure and broad availability of fertility specialists are supporting service demand. Expansion of reproductive diagnostic laboratories and increasing use of advanced sperm testing technologies are strengthening clinical capabilities.

U.K. Male Infertility Market Insights

The U.K. is likely to hold around 19% of the Europe market in 2026. Increasing awareness of male reproductive health and growing utilization of fertility assessments are driving demand. The expansion of fertility treatment facilities and the adoption of advanced laboratory technologies are improving access to specialized services.

Asia Pacific Male Infertility Market Trends

Asia Pacific is forecast to be the fastest-growing market for male infertility, stimulated by rising infertility prevalence, expanding healthcare infrastructure, increasing healthcare expenditure, and improving access to fertility treatments. Growth in fertility clinic networks and diagnostic laboratory capacity is enhancing service availability.

China Male Infertility Market Insights

China is expected to account for approximately 31% of the Asia Pacific market in 2026. Expansion of fertility treatment infrastructure and increasing adoption of advanced diagnostic technologies are supporting growth. Rising healthcare investments and greater awareness regarding reproductive health are improving patient access to fertility services.

India Male Infertility Market Insights

India is projected to represent nearly 24% of the Asia Pacific market in 2026. Growth is supported by rapid expansion of fertility clinics, increasing diagnostic testing availability, and growing awareness regarding male infertility. Investments in assisted reproductive technology facilities and laboratory infrastructure are improving treatment accessibility.

Competitive Landscape

The global male infertility market is moderately fragmented, with a combination of large multinational medical device companies and specialized fertility diagnostics firms competing across product categories. Leading participants include CooperSurgical, Hamilton Thorne, Merck KGaA, Vitrolife, and Esco Medical.

Market share distribution is shaped by regional regulatory approvals, distribution agreements with hospital procurement systems, and brand recognition among reproductive medicine specialists. Companies with integrated portfolios spanning semen analysis hardware, consumables, and software analytics hold competitive advantages in multi-year procurement contracts.

Key Industry Developments:

- In January 2026, Spermosens AB signed a memorandum of understanding with Sapyen to advance next-generation male fertility diagnostics and support commercialization of the JUNO-Checked platform for improved assessment of male fertility potential.

- In October 2025, Sapyen launched the United Kingdom's first at-home male fertility testing kit, expanding access to laboratory-grade fertility diagnostics and accelerating early detection of male infertility through home-based sample collection and analysis.

- In July 2025, PGIMER Chandigarh successfully performed India's first robot-assisted vasovasostomy (vasectomy reversal) using the da Vinci Surgical System, advancing microsurgical treatment options for male infertility through enhanced surgical precision and improved fertility restoration outcomes.

Companies Covered in Male Infertility Market

- CooperSurgical Inc.

- Hamilton Thorne Ltd.

- Merck KGaA

- Vitrolife AB

- Esco Medical Group

- IVFtech ApS

- Nidacon International AB

- Microptic SL

- Medical Electronic Systems (MES)

- FertiPro NV

Frequently Asked Questions

The global male infertility market is projected to reach US$4.6 billion in 2026.

Rising prevalence of reproductive disorders, delayed parenthood, lifestyle-related fertility challenges, and increasing adoption of advanced fertility diagnostics and treatments drive the male infertility market.

The male infertility market is poised to witness a CAGR of 4.3% from 2026 to 2033.

Expansion of genetic and at-home fertility testing, precision reproductive diagnostics, and integrated fertility care services creates significant opportunities in the male infertility market.

Some of the key market players include CooperSurgical, Hamilton Thorne, Merck KGaA, Vitrolife, and Esco Medical.