- Biotechnology

- Life Science Products Market

Life Science Products Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Life Science Products Market by Product (Instruments & Equipment, Kits & Reagents, Consumables, Software & Informatics, and Others), by Application (Molecular Biology, Protein & Immunoassays, Cell & Gene Technologies, Chromatography, and Others) by End-user (Pharmaceutical Companies, Biotechnology Companies, Academic and Research Institutions, Contract Research Organizations, and Others), and Regional Analysis from 2026 to 2033

Life Sciences Products Market Share and Trends Analysis

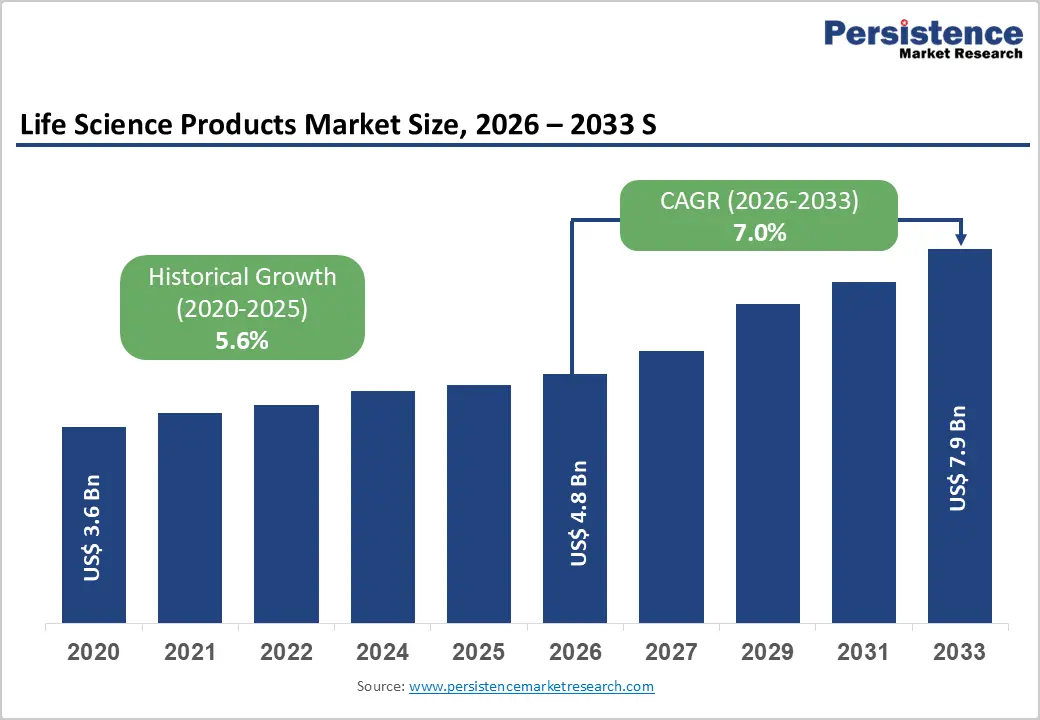

The global life sciences products market is projected to grow from US$4.8 billion in 2026 to US$ 1.7 billion by 2033, at a CAGR of 7.0% over the forecast period.

Global demand for life sciences products is increasing steadily, driven by rising investments in pharmaceutical and biotechnology R&D, the growing adoption of advanced molecular and cellular technologies, and the expanding use of high-precision instruments and consumables across research, diagnostics, and biomanufacturing workflows. Higher volumes of routine and advanced laboratory testing, coupled with increasing healthcare and life sciences spending, are supporting sustained market growth.

The expansion of pharmaceutical companies, biotechnology firms, CROs/CDMOs, and academic research institutions is further accelerating demand for high-performance kits, reagents, and consumables. Continuous innovation in assay chemistry, reagent formulations, automation compatibility, and data-driven laboratory workflows is improving accuracy, reducing turnaround time, and enhancing reproducibility across molecular biology, immunoassays, and cell-based applications. Additionally, the growing focus on precision medicine, digital laboratories, and broader acceptance of automated and informatics-enabled workflows is further propelling the global life science products market.

Key Industry Highlights:

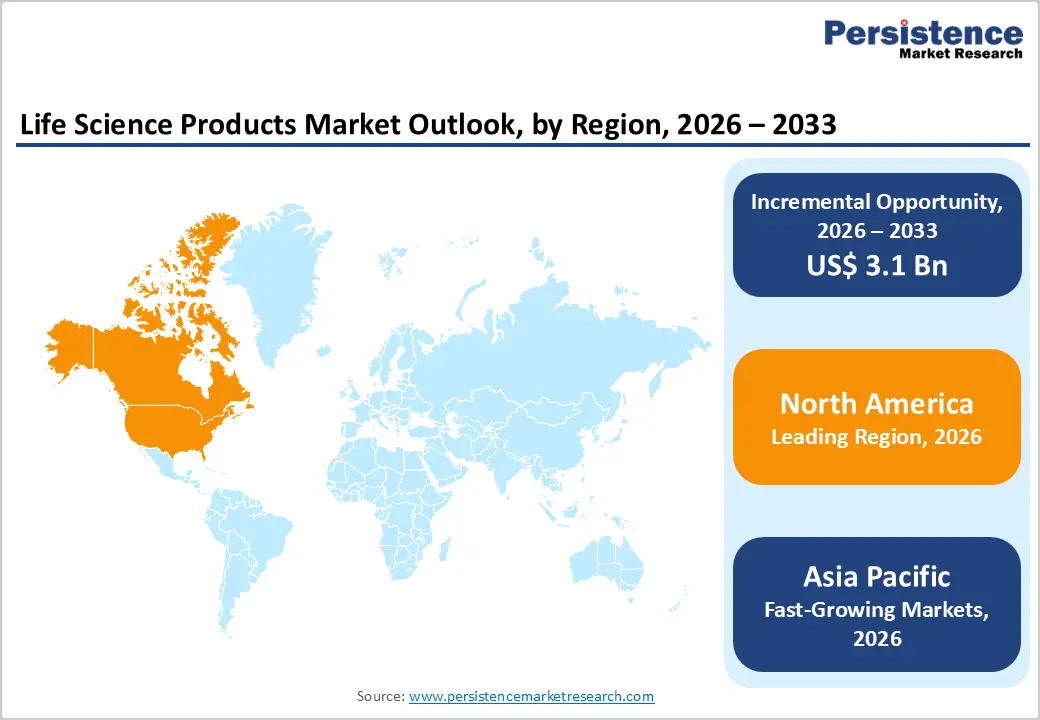

- Leading Region: North America holds the largest share at 46.7%, supported by strong life sciences infrastructure, high R&D expenditure, early adoption of advanced laboratory technologies, and the presence of leading global manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large patient and research base, rapid growth in pharmaceutical and biotechnology activities, increasing penetration of modern laboratories, and rising investments in molecular diagnostics and biomanufacturing.

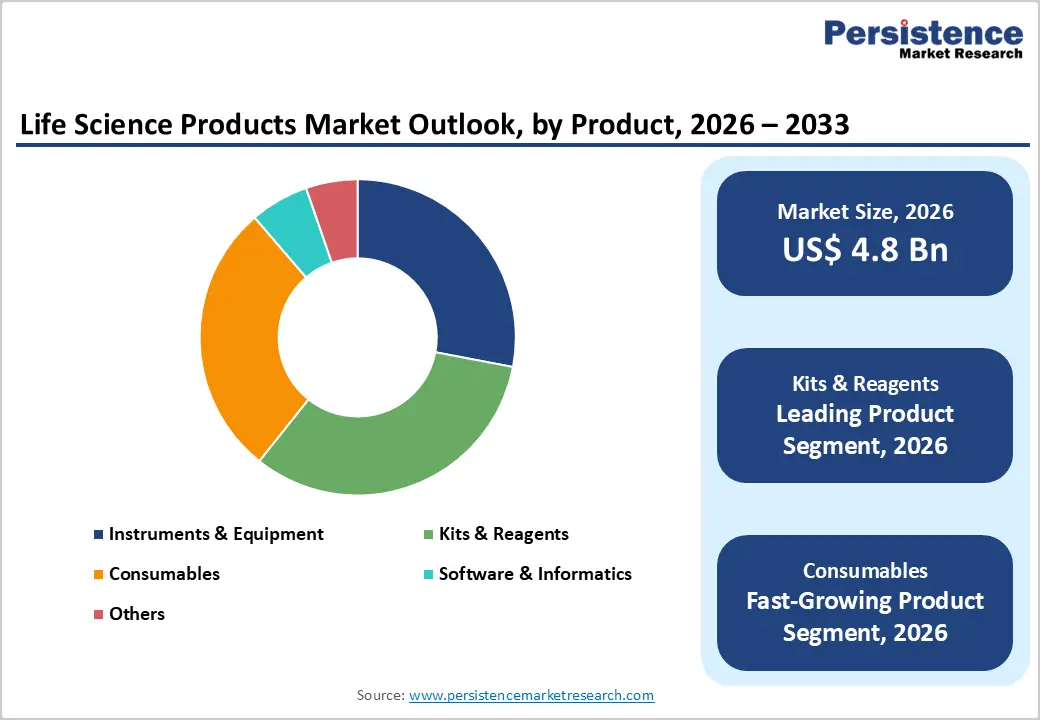

- Leading Product Segment: Kits & reagents dominate the market due to their broad applicability across molecular biology, diagnostics, bioprocessing, and regulated laboratory workflows.

- Fastest-Growing Product Segment: Consumables are expanding rapidly as laboratories increase test volumes and adopt cost-effective, scalable solutions for routine and high-throughput applications.

- Leading Application Segment: Molecular biology remains the top application, driven by high testing volumes in genomics, infectious disease diagnostics, oncology research, and biomarker analysis.

- Fastest-Growing Application Segment: Cell & gene technologies are scaling quickly as demand rises for advanced therapeutics, regenerative medicine, and next-generation research platforms.

| Key Insights | Details |

|---|---|

| Life Science Products Market Size (2026E) | US$ 4.8 Bn |

| Market Value Forecast (2033F) | US$ 7.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.0% |

Market Dynamics

Driver - Rising R&D Investment and Expansion of Molecular Diagnostics

Increasing pharmaceutical and biotechnology R&D expenditure is a fundamental driver of sustained growth in the global life science products market. Drug discovery, preclinical research, clinical development, and quality control activities rely heavily on advanced analytical instruments, high-performance reagents, and recurring consumables to support complex experimental workflows. Growing focus on biologics, biosimilars, and cell and gene therapies has further intensified demand for precision tools, validated assay kits, and scalable laboratory solutions. In addition, pharmaceutical and biotech companies are expanding internal R&D capabilities and strengthening collaborations with CROs and academic institutions, resulting in higher test volumes and consistent use of life sciences products across research and manufacturing environments.

Additionally, the rapid adoption of molecular diagnostics and genomics is significantly accelerating market expansion across clinical, research, and public health laboratories. Techniques such as PCR, qPCR, next-generation sequencing, and molecular immunoassays are increasingly used for infectious disease detection, oncology diagnostics, genetic screening, and population health monitoring. The shift toward early disease detection, precision medicine, and data-driven healthcare is driving routine, high-throughput testing, thereby increasing recurring demand for molecular biology reagents and consumables. Continued investments in laboratory automation, standardization, and digital data integration further enhance testing efficiency and scalability, reinforcing long-term demand for life sciences products.

Restraints - High Cost Pressures and Regulatory Complexity Constraining Market Adoption

The high capital costs associated with advanced life sciences instruments and integrated analytical platforms remain a significant restraint on market growth, particularly for small laboratories, start-ups, and institutions in emerging markets. Sophisticated systems used for genomics, high-throughput screening, and bioprocessing require substantial upfront investment, along with ongoing expenses related to maintenance, calibration, and skilled personnel. Budget constraints often delay technology upgrades or limit adoption to basic platforms, slowing the penetration of advanced solutions beyond large pharmaceutical companies and well-funded research centers. This cost sensitivity is further amplified in price-constrained geographies, where laboratories prioritize essential consumables over capital-intensive instrumentation.

Moreover, stringent regulatory and validation requirements add complexity and cost across the product lifecycle, from development to commercialization. Compliance with regulatory standards such as GMP, ISO, and regional diagnostic approval frameworks increases development timelines, documentation burden, and testing expenses for manufacturers. Additionally, pricing pressure driven by procurement consolidation among large pharmaceutical companies, hospital networks, and group purchasing organizations is compressing supplier margins. Bulk purchasing agreements and aggressive price negotiations limit pricing flexibility, particularly for commoditized consumables and reagents. Together, regulatory complexity and margin pressure challenge profitability and can impede innovation, particularly for smaller and mid-sized life sciences product manufacturers.

Opportunity - Expansion of Advanced Therapeutics and Outsourced Research Creating Long-Term Market Opportunities

The rapid expansion of biologics, cell, and gene therapy pipelines is creating significant growth opportunities for the global life science products market. These advanced therapeutic modalities require highly specialized reagents, cell culture media, viral vectors, single-use bioprocessing systems, and high-sensitivity analytical tools to support development, manufacturing, and quality control. As pipelines progress from early research to clinical and commercial stages, demand for scalable, validated, and regulatory-compliant life science products continues to rise. In parallel, pharmaceutical and biotechnology companies are increasingly outsourcing research, development, and manufacturing activities to CROs and CDMOs. This trend is driving consistent, high-volume consumption of standardized reagents, consumables, and testing platforms across multiple projects and clients, strengthening recurring revenue streams for suppliers.

Additionally, the expansion of life sciences infrastructure in emerging markets, particularly across the Asia Pacific and Latin America, is broadening the global customer base. Governments and private investors are increasing funding for research institutes, diagnostic laboratories, and biomanufacturing facilities, accelerating the adoption of modern laboratory technologies. At the same time, suppliers are shifting toward recurring revenue models, including reagent rental agreements, consumable subscription programs, and SaaS-based informatics platforms. These models improve customer retention, enhance workflow integration, and provide predictable revenue, positioning vendors for sustained long-term growth.

Category-wise Analysis

By Product, Kits & Reagents Dominate Globally Due to Expanding Use in Molecular and Diagnostic Workflows

The kits & reagents segment is projected to dominate the global life science products market in 2026, accounting for a revenue share of 32.7%. This dominance is primarily driven by their widespread and recurring use across molecular biology, immunoassays, cell analysis, and clinical diagnostics. Kits and reagents are essential to routine laboratory workflows, including PCR, qPCR, NGS library preparation, immunoassays, and biomarker testing, and are indispensable across pharmaceutical research, biotechnology development, and clinical laboratories. The growing adoption of precision medicine, personalized diagnostics, and high-throughput testing platforms has significantly increased reagent consumption per study and per test.

In addition, the expansion of biopharmaceutical R&D pipelines, rising infectious disease testing volumes, and increased focus on reproducibility and standardized workflows are reinforcing demand. Continuous innovation in assay sensitivity, multiplexing capability, and automation-compatible reagent formats is further enhancing performance, reliability, and scalability, supporting sustained segment dominance.

By Application, Molecular Biology Leads the Market Due to High Testing Volumes and Broad Research Adoption

The molecular biology segment is projected to dominate the global life sciences products market in 2026, accounting for 33.8% of revenue. This leadership is driven by the extensive global use of molecular techniques across research, diagnostics, and biomanufacturing. Applications such as gene expression analysis, pathogen detection, genetic screening, and oncology diagnostics rely heavily on molecular biology tools and reagents. The growing emphasis on early disease detection, genomics-based research, and companion diagnostics has accelerated adoption across laboratories worldwide. High test volumes, recurring reagent usage, and expanding access to molecular diagnostics in emerging markets continue to support growth. Furthermore, advances in PCR efficiency, next-generation sequencing workflows, and sample-preparation technologies are improving throughput, accuracy, and cost-effectiveness, thereby strengthening the segment’s market leadership.

By End-user, Pharmaceutical Companies Dominate Globally Due to High R&D Spend and Rapid Technology Adoption

The pharmaceutical companies segment is projected to dominate the global life sciences products market in 2026, accounting for 44.2% of revenue. This dominance is driven by substantial investments in drug discovery, preclinical research, clinical development, and quality control activities. Pharmaceutical companies are major purchasers of advanced instruments, high-value reagents, and validated consumables required for regulated workflows. Strong focus on biologics, cell and gene therapies, and precision medicines has increased demand for specialized assays, molecular platforms, and bioprocessing tools. Pharmaceutical firms also demonstrate faster adoption of automation, digital laboratory solutions, and integrated informatics to improve productivity and data integrity. Long-term supply agreements, bundled procurement models, and extensive internal laboratory networks further reinforce their leading contribution to global market revenues.

Region-wise Insights

North America Life Science Products Market Trends

North America is expected to dominate the global life sciences products market, with a value share of 46.7% in 2026, led by the U.S. Market leadership is supported by high life sciences R&D expenditure, a strong presence of pharmaceutical and biotechnology companies, and early adoption of advanced laboratory technologies. The region benefits from a well-established ecosystem of manufacturers, CROs, academic institutions, and clinical laboratories with high utilization of premium instruments and consumables.

Strong funding for biomedical research, widespread adoption of molecular diagnostics, and rapid integration of automation and informatics platforms continue to drive demand. Supportive regulatory frameworks, frequent product innovation, and robust training and certification programs further accelerate market penetration. In addition, the concentration of large pharmaceutical pipelines and biomanufacturing facilities ensures sustained recurring demand for reagents and consumables.

Europe Life Science Products Market Trends

The European life science products market is expected to grow steadily, supported by increasing adoption of advanced research technologies, an aging population, and rising demand for diagnostics and biologics development. Key markets such as Germany, the U.K., France, Italy, and the Nordic countries exhibit strong uptake of high-performance laboratory instruments and molecular platforms, attributable to mature healthcare and research infrastructure.

The growing emphasis on genomics, translational research, and personalized medicine is increasing demand for molecular biology reagents and analytical tools. Regulatory support for innovation, expanded public research funding, and the integration of life sciences products into automated and digital laboratory environments are improving efficiency and outcomes. Continuous innovation by regional and global manufacturers, along with strong academic-industry collaboration, supports long-term market expansion across Europe.

Asia Pacific Life Science Products Market Trends

Asia Pacific life science products market is expected to register a relatively higher CAGR of around 8.4% between 2026 and 2033, driven by expanding healthcare infrastructure, rising R&D investments, and growing access to diagnostics and research capabilities. Countries such as China, India, South Korea, and Japan are experiencing robust growth in pharmaceutical manufacturing, biotechnology research, and clinical trial volumes.

Increasing government support for life sciences, cost-competitive manufacturing, and a growing pool of skilled researchers are accelerating adoption across academic and commercial laboratories. Technological advancements that improve the affordability and scalability of instruments and consumables are enhancing penetration in price-sensitive markets. Strategic investments, public-private partnerships, and localization initiatives by global players are further strengthening regional market growth.

Competitive Landscape

The global life science products market is highly competitive, with strong participation from companies such as Thermo Fisher Scientific Inc., Merck KGaA, Agilent Technologies, Inc., Bio-Rad Laboratories, Inc., QIAGEN, and BD. These players leverage extensive global distribution networks, strong brand equity, and continuous innovation across instruments, reagents, consumables, and informatics solutions to address diverse requirements in research, clinical diagnostics, and biopharmaceutical manufacturing.

Rising demand for high-throughput testing, precision molecular analysis, and scalable bioprocessing workflows is accelerating adoption across pharmaceutical and biotechnology companies, clinical laboratories, and academic research institutions. Manufacturers are increasingly focusing on advanced molecular biology platforms, automation and digital laboratory solutions, enhanced assay sensitivity, and workflow integration. Strategic priorities include portfolio expansion, software and informatics integration, customer training and technical support, and geographic expansion to strengthen market positioning and drive sustained growth.

Key Industry Developments:

- In December 2025, Caris Life Sciences® announced that its therapeutic research arm, Caris Discovery, entered into a multi-year collaboration and licensing agreement with Genentech, a member of the Roche Group, to identify and validate novel oncology targets in solid tumor tissues using advanced AI-driven precision medicine approaches.

- In December 2025, In December 2025, Accenture, through Accenture Ventures, invested in Ryght AI, a platform that modernizes clinical research design and execution for the life sciences industry by combining agentic AI with enterprise technology to accelerate the development of new treatments.

- In April 2024, Merck announced an investment of over €300 million to establish a new Advanced Research Center at its global headquarters in Darmstadt, Germany. The facility will support life science research focused on antibody manufacturing, mRNA applications, and other biotechnological production solutions, and is expected to accommodate around 550 employees from 2027. The project forms part of Merck’s broader €1.5 billion investment program at the Darmstadt site through 2025.

Companies Covered in Life Science Products Market

- Thermo Fisher Scientific Inc

- Merck KGaA

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc

- QIAGEN

- BD

- GE HealthCare

- Illumina, Inc.

- Revvity

- Promega Corporation.

- Takara Bio Inc

- Lonza

- Oxford Nanopore Technologies plc.

- Others

Frequently Asked Questions

The global life science products market is projected to be valued at US$ 4.8 Bn in 2026.

Rising pharmaceutical and biotechnology R&D spending, expanding clinical diagnostics volumes, growing adoption of advanced molecular and cell-based technologies, and increasing outsourcing to CROs/CDMOs are driving the global life science products market.

The global life science products market is poised to witness a CAGR of 7.0% between 2026 and 2033.

High-growth opportunities exist in cell and gene therapy tools, single-cell and spatial omics, laboratory automation and informatics, and recurring consumables demand driven by expanding bio-manufacturing and precision medicine are creating opportunities in the market.

Thermo Fisher Scientific Inc., Merck KGaA, Agilent Technologies, Inc., Bio-Rad Laboratories, Inc., QIAGEN, and BD are some of the key players in the life science products market.