- Specialty & Fine Chemicals

- Leak Detection Dyes Market

Leak Detection Dyes Market Size, Share, and Growth Forecast 2025 - 2032

Leak Detection Dyes Market Analysis By Product Type (Oil-based, Water-based, Universal Dyes), Dye Type (Fluorescent, Non-fluoroscent), Application (Water Leak Detection, Oil-Lead Detection, Refrigerant Leak Detection), End-use, and Regional Analysis 2025 - 2032

Leak Detection Dyes Market Share and Trends Analysis

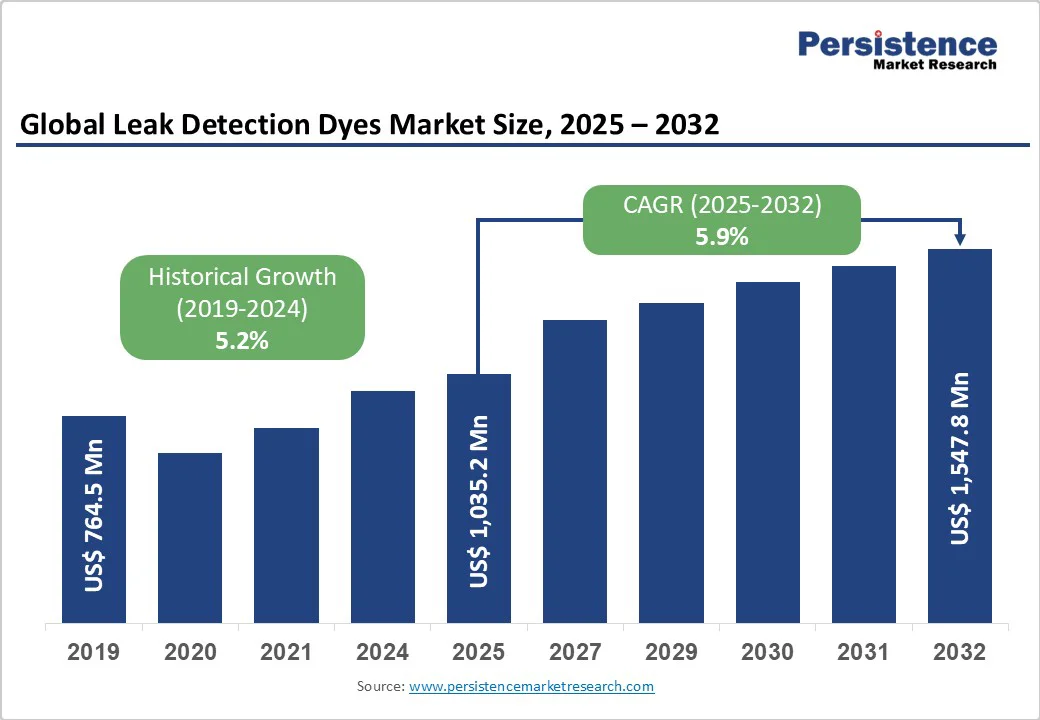

The global leak detection dyes market size is likely to reach US$1,036.2 million in 2025 and is projected to reach US$1,547.8 million by 2032, growing at a CAGR of 5.9% between 2025 and 2032.

The robust growth is driven by stringent environmental regulations that mandate leak monitoring systems across various industrial sectors, particularly in the automotive, HVAC, and oil-gas pipeline infrastructure.

Rising awareness of preventive maintenance strategies and the increasing complexity of fluid-based systems in modern machinery are accelerating market adoption globally.

Key Market Highlights:

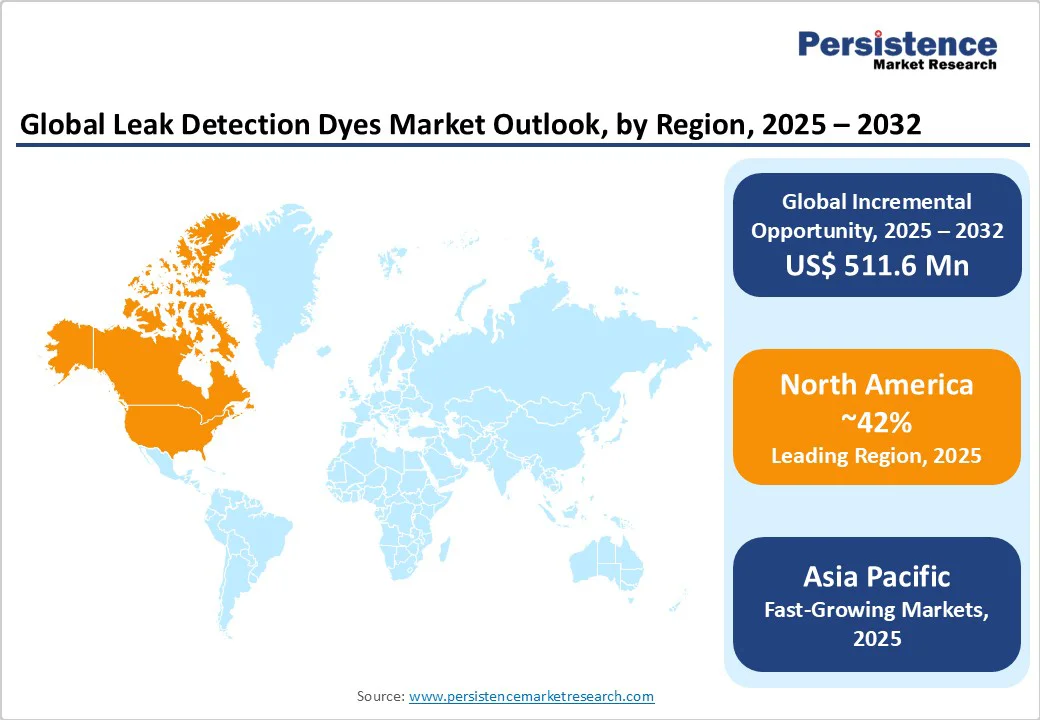

- Leading Region: North America dominates global leak detection dye consumption, with approximately a 42% market share, supported by comprehensive regulatory frameworks and advanced automotive aftermarket infrastructure.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing regional market with a projected CAGR of 6.8% through 2032, driven by industrial expansion in China and India.

- Leading Dye Type: Fluorescent dyes maintain dominance with a 72% segment share, owing to their superior detection sensitivity and compatibility with automated monitoring systems.

- Fastest-Growing Product Type: Water-based dyes emerge as the fastest-growing product segment with a CAGR of 6.2%, supported by environmental sustainability requirements and regulatory preferences.

- Key Market Opportunity: Automotive HVAC integration represents the primary market opportunity, with the potential to reach $450 million by 2030 as global electric vehicle adoption accelerates.

| Key Insights | Details |

|---|---|

| Leak Detection Dyes Market Size (2025E) | US$ 1,036.2 million |

| Market Value Forecast (2032F) | US$ 1,547.8 million |

| Projected Growth CAGR (2025-2032) | 5.9% |

| Historical Market Growth (2019-2024) | 5.2% |

Market Dynamics

Drivers - Stringent Environmental Regulations and Compliance Requirements

The implementation of stringent environmental regulations has emerged as a major growth driver for the leak detection dyes market. Policies such as the European Union’s F-Gas Regulation (EU 517/2014) and the EPA’s SNAP program in North America require the systematic monitoring of equipment containing refrigerants with a CO2 equivalent above 5 tonnes.

Installations with 100 kilograms or more of fluorinated greenhouse gases must utilize leak detection systems. The F-Gas Regulation mandates leak checks every 12 months without detection systems and every 24 months with automated systems, creating consistent demand for reliable fluorescent dyes. Companies failing to comply face heavy fines, reaching up to €100,000 in Europe, compelling industrial operators to invest in effective leak detection technologies to avoid penalties.

These regulations have expanded beyond traditional HVAC applications to cover emerging refrigerants such as hydrofluoroolefins (HFOs). This shift has increased demand for specialized dye formulations capable of detecting leaks in newer systems.

As environmental compliance becomes increasingly stringent globally, manufacturers are adopting fluorescent detection solutions across various industrial verticals, thereby strengthening market growth and driving innovation in advanced dye technologies.

Expanding Automotive HVAC and Industrial Pipeline Infrastructure

The growing complexity of automotive HVAC systems and industrial pipelines is driving the adoption of leak detection dyes. Modern vehicles, particularly those utilizing R-1234yf refrigerants or hybrid technologies, require highly sensitive detection solutions capable of identifying leaks as small as 0.65 ounces per year.

Rising vehicle production in emerging markets is further fueling the demand for reliable leak detection dyes. Automotive OEMs and service providers are prioritizing precision in HVAC maintenance, which creates a steady market for advanced fluorescent detection solutions.

Similarly, the global expansion of oil, gas, and water pipeline infrastructure has intensified the need for continuous monitoring systems. With pipeline networks exceeding 3.5 million kilometers worldwide, industrial operators are increasingly implementing fluorescent dyes to detect leaks early and prevent fluid losses, which can reach up to 30% annually in complex circulation systems. The adoption of leak detection solutions in water and wastewater management, particularly in conjunction with industrial pipelines, underscores the crucial role of fluorescent dyes in mitigating operational risks and minimizing environmental contamination.

Market Restraint - High Initial Investment and System Integration Costs

The high upfront cost of implementing comprehensive leak detection dye systems remains a key market restraint. Medium-scale industrial facilities often incur initial expenses exceeding $50,000, which cover specialized UV detection equipment, personnel training, and integration with existing infrastructure. For small and medium enterprises, these substantial investments can strain budgets, particularly in price-sensitive markets where immediate returns on investment are unclear.

Retrofitting older systems with modern leak detection capabilities can be a complex and time-consuming process. Facilities may experience extended downtime during installation, and the process often requires specialized technical expertise. These factors collectively increase the total cost of ownership and can delay adoption, limiting market penetration among cost-conscious operators.

Technical Limitations and False Positive Concerns

Leak detection dye technologies face technical challenges that can restrict their effectiveness. Sensitivity calibration may be affected by environmental factors, such as high humidity or contaminated surroundings. Fluorescent dyes can degrade under extreme temperatures or when exposed to certain chemical compounds, reducing detection reliability.

Electronic detection systems may generate false positives due to background environmental interference, requiring careful interpretation by trained personnel. The dependence on specialized UV lighting equipment and skilled technicians creates operational complexity, making consistent monitoring difficult for some facilities. These technical limitations and potential inaccuracies act as a barrier to widespread adoption in industrial applications.

Market Opportunities

Emerging Smart IoT-Based Monitoring Systems Integration

The integration of leak detection dyes with Internet of Things (IoT) technologies is creating significant growth opportunities in the market. Advanced monitoring systems now leverage real-time data analytics and automated alert mechanisms to enhance traditional leak detection methods.

Smart sensors utilizing fluorescent dye technology can detect leak signatures up to 60 days earlier than conventional approaches, resulting in a reduction of refrigerant losses by as much as 80%. This early detection capability improves operational efficiency and minimizes downtime in industrial and automotive applications.

Combining artificial intelligence algorithms with fluorescent detection systems enables predictive maintenance strategies, allowing facilities to address potential issues before they result in costly repairs.

Cloud-based monitoring platforms facilitate centralized management across multiple sites, creating new revenue opportunities for dye manufacturers through software-as-a-service models. As digital infrastructure adoption grows across industries, integrating IoT with leak detection dyes presents a lucrative avenue for innovation and market expansion.

Biodegradable and Environmentally Sustainable Dye Formulations

Environmental sustainability is driving demand for eco-friendly leak detection solutions, creating opportunities for manufacturers to develop biodegradable dye formulations that meet these needs. UV fluorescent dyes that comply with OECD 301B standards are increasingly used in sensitive ecological zones, including offshore, forestry, and agricultural applications. Products like ECO-GLO Green are designed to meet Environmentally Acceptable Lubricant (EAL) requirements, enabling safe leak detection without harming ecosystems.

The demand for non-toxic, biodegradable dyes is especially strong in water treatment facilities, food processing plants, and offshore drilling operations, where environmental impact is a critical concern. Regulatory support for sustainable chemical solutions further encourages innovation in green chemistry research. Manufacturers investing in eco-friendly formulations can differentiate themselves, tap into new market segments, and capitalize on growing environmental awareness while complying with evolving global regulations.

Category-wise Analysis

Product Type Insights

Water-based dyes dominate the leak detection market, holding a roughly 46% share due to their cost-effectiveness and environmental safety. These formulations are highly compatible with aquatic systems and HVAC applications, providing superior fluorescent visibility under UV illumination.

They excel in detecting leaks in cooling systems, plumbing networks, and industrial water circulation systems, making them ideal for applications in food processing facilities, pharmaceutical manufacturing, and residential buildings where safety is paramount.

Water-based dyes are biodegradable and comply with stringent environmental regulations, enhancing their appeal among eco-conscious operators. Universal dyes, on the other hand, represent the fastest-growing segment, offering versatility across different fluid types. Their use reduces the need for multiple dye inventories, simplifies operational management, and allows service technicians to implement more efficient leak detection programs.

Dye Type Insights

Fluorescent dyes lead the market with approximately 73% share due to their high sensitivity and reliability across varied environmental conditions. These formulations can detect leaks as small as 1 part per million, providing early warnings that prevent minor leaks from escalating into major failures. Their bright yellow-green fluorescence under UV light ensures clear visual identification, reducing diagnostic time and improving maintenance efficiency.

Fluorescent dyes also offer photostability and consistent performance across temperature ranges of -20°C to +65°C, making them suitable for long-term monitoring applications. Integration with automated detection systems enables continuous surveillance and predictive maintenance, particularly in critical industrial and commercial settings. Modern formulations resist background interference, further enhancing their operational reliability and adoption in complex environments.

Application Insights

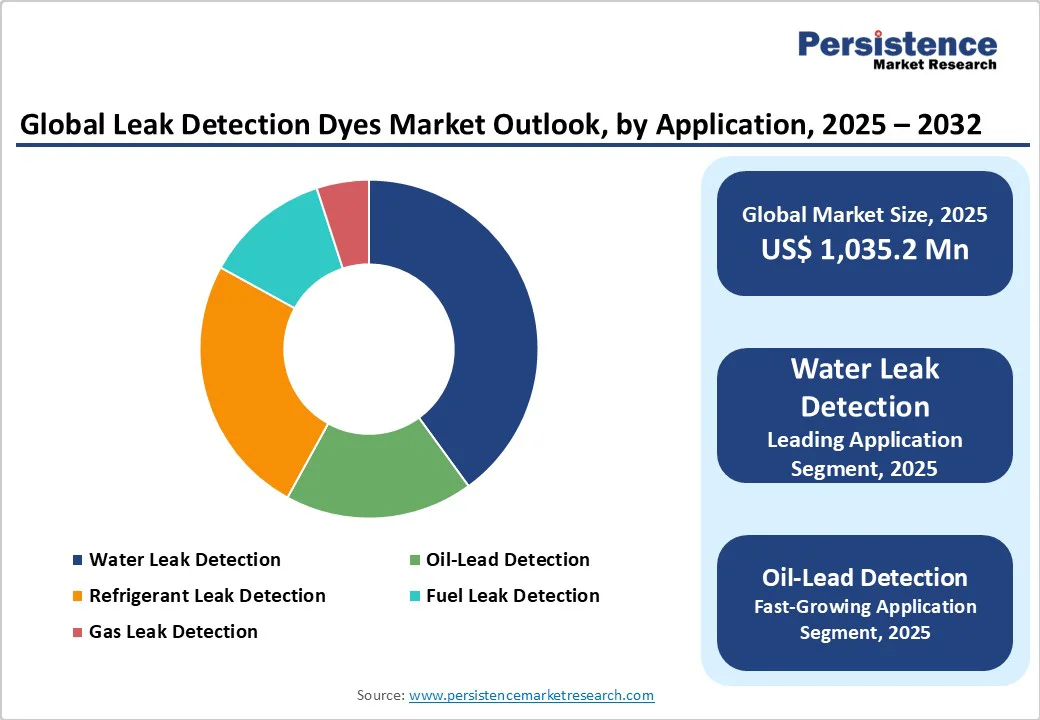

Water leak detection is the largest application segment, holding roughly 40% market share, driven by aging infrastructure and rising water conservation initiatives. Municipal systems that lose over 20% of water annually are increasingly relying on fluorescent dyes for efficient leak monitoring. Strong regulatory support mandates routine leak detection in public water supplies, ensuring resource optimization and operational efficiency.

HVAC and refrigeration applications account for around 28% share, fueled by the expanding commercial building sector and strict refrigerant management regulations. Increasing system complexity and the shift to low-GWP refrigerants are driving demand for precision detection solutions. Automotive oil leak detection continues to grow, with advanced engines and high-pressure hydraulic systems requiring specialized dyes for reliable monitoring.

End-use Analysis

The automotive and transportation sector dominates, with a market share of approximately 35%, driven by the increasing complexity of vehicles and stringent emission control regulations. Modern vehicles integrate multiple fluid systems requiring specialized leak detection, including advanced transmission, brake, and climate control units. Electric and hybrid vehicles present new challenges, particularly in battery thermal management and monitoring the cooling system.

HVAC and refrigeration end-users account for approximately a 32% share, supported by the growth and modernization of commercial construction and existing building systems. Regulatory mandates for periodic leak monitoring and rising emphasis on energy efficiency encourage the adoption of fluorescent dyes. Industrial facilities are increasingly incorporating preventive maintenance strategies, using dye-based leak detection to reduce unexpected failures and optimize operational performance.

Regional Insights

North America Leak Detection Dyes Market Trends

North America maintains market leadership with the United States accounting for approximately 78% of regional demand, driven by comprehensive regulatory frameworks and advanced industrial infrastructure. The EPA's Section 608 regulations require leak detection for commercial refrigeration systems that exceed 50 pounds of refrigerant, creating a consistent demand for fluorescent dye solutions. The region benefits from a mature automotive aftermarket industry, with over 280 million registered vehicles requiring periodic maintenance and leak detection services.

Recent developments include the EPA's updated refrigerant management rules for 2025, which expand leak detection requirements to include HFO refrigerants and reduce permissible leak rates for commercial applications. The implementation of smart building initiatives across major metropolitan areas is driving adoption of automated leak detection systems integrated with IoT monitoring platforms. California's Title 24 energy efficiency standards mandate advanced leak detection for large HVAC systems, driving market growth in commercial applications.

Europe Leak Detection Dyes Market Trends

Germany leads European market with approximately 32% of regional demand, supported by stringent environmental regulations and advanced manufacturing infrastructure. The F-Gas Regulation revision in 2024 has expanded leak detection requirements to include smaller refrigeration systems and introduced automated monitoring mandates for installations exceeding 100 kilograms of fluorinated gases. France and the United Kingdom are demonstrating strong growth in automotive applications, with an increasing adoption of R-1234yf refrigerants requiring specialized leak detection capabilities.

The European market benefits from comprehensive regulatory harmonization across 27 member states, creating consistent demand patterns and standardized technical requirements. Recent initiatives include the Green Deal Industrial Plan, which promotes sustainable leak detection technologies and provides financial incentives for eco-friendly dye formulations.

The region's focus on circular economy principles is driving demand for biodegradable leak detection solutions, particularly in environmentally sensitive applications such as offshore wind installations and marine transportation systems.

Asia Pacific Leak Detection Dyes Market Trends

China dominates regional market dynamics with approximately 42% of Asia Pacific demand, driven by massive industrial expansion and increasing environmental compliance requirements. The country's National Environmental Protection Standards for refrigeration systems mandate regular leak monitoring for commercial applications, supporting consistent market growth. Japan's advanced automotive industry and precision manufacturing sector drive demand for high-sensitivity leak detection solutions, particularly in applications for hybrid and electric vehicles.

India's expanding industrial infrastructure and growing automotive market present significant growth opportunities, with increasing adoption of modern HVAC systems in commercial buildings and manufacturing facilities. The region benefits from substantial manufacturing cost advantages and growing local production capabilities for fluorescent dye formulations.

ASEAN countries are experiencing rapid industrialization and urbanization, driving demand for leak detection solutions in both industrial and commercial applications. The region's focus on sustainable development goals and environmental protection is supporting the adoption of eco-friendly dye technologies and automated monitoring systems.

Competitive Landscape

The global leak detection dyes market is moderately concentrated, with the top players controlling around 65% of the global share. Leading companies maintain their position through extensive distribution networks, diverse product portfolios, and strong collaborations with OEMs. Continuous innovation in dye formulations, particularly environmentally sustainable solutions, is a key factor differentiating market leaders from competitors.

Strategic partnerships between dye producers and equipment manufacturers enable integrated offerings that combine fluorescent dyes with specialized detection systems. Emerging players are targeting niche applications and regional markets, especially in developing economies, aiming to capitalize on opportunities where established companies have limited penetration and presence.

Key Market Developments

- In September 2024, Spectronics Corporation launched ECO-GLO Green, the first readily biodegradable UV fluorescent oil dye for industrial maintenance applications. The product targets environmentally regulated installations in marine and agricultural sectors, offering a sustainable solution for facilities seeking compliance with ecological standards while ensuring effective leak detection.

- In June 2024, Tracer Products introduced advanced R-1234yf compatible dye formulations designed for next-generation automotive HVAC systems. These dyes support the industry’s transition toward low-GWP refrigerants, enhancing leak detection efficiency and helping manufacturers and service providers meet evolving environmental regulations for vehicle cooling and climate control systems.

- In March 2024, Errecom S.p.A. expanded its BRILLIANT product line with solvent-free dye formulations compliant with SAE J2297 and SAE J2298 standards. The development targets automotive and industrial refrigeration markets, offering safer, environmentally friendly options while maintaining high-performance leak detection capabilities for modern cooling systems.

Companies Covered in Leak Detection Dyes Market

- FJC Inc.

- Mastercool Inc.

- Refrigeration Technologies

- Spectronics Corporation

- Tracer Products

- Errecom S.p.A.

- Glo-Leak LLC

- UVIEW Technology Inc.

- ChemPoint Inc.

- Fluorescent Solutions Inc.

- AGS Company Automotive Solutions

- Bright Solutions Inc.

Frequently Asked Questions

The global leak detection dyes market is projected to reach US$ 1,547.8 million by 2032, growing from US$ 1,036.2 million in 2025 at a CAGR of 5.9%.

Key growth drivers include stringent environmental regulations such as the EU F-Gas Regulation and EPA SNAP program, expanding automotive HVAC infrastructure, and increasing adoption of preventive maintenance strategies across industrial sectors.

Water-based dyes lead the market with approximately 45% market share due to their environmental safety profile, cost-effectiveness, and compatibility with diverse fluid systems including HVAC and plumbing applications.

North America dominates the global market with approximately 42% market share, supported by comprehensive regulatory frameworks, advanced automotive aftermarket infrastructure, and stringent environmental compliance requirements.

Primary opportunities include IoT-based smart monitoring system integration, development of biodegradable eco-friendly formulations, and expansion into automotive electric vehicle thermal management applications.

Key market players include Spectronics Corporation, Tracer Products, FJC Inc., Mastercool Inc., Errecom S.p.A., and Refrigeration Technologies, with these companies maintaining strong positions through comprehensive product portfolios and extensive distribution networks.