- Specialty & Fine Chemicals

- Hydrofluoroolefins (HFO) Market

Hydrofluoroolefins (HFO) Market Size, Share, and Growth Forecast 2026 - 2033

Hydrofluoroolefins (HFO) Market by Product Type (HFO-1234ze, HFO-1233zd, HFO-1234yf, HFO-1336mzz, Others), by Application (Refrigerant, Foam Blowing Agent, Aerosol Propellant, Solvent and Cleaning Agents, Others), by End Use (HVAC and Refrigeration, Automotive Air Conditioners, Building and Construction, Personal Care and Consumer Products, Electronics and Precision Cleaning, Others), by Regional Analysis, 2026 - 2033

Hydrofluoroolefins (HFO) Market Size and Trend Analysis

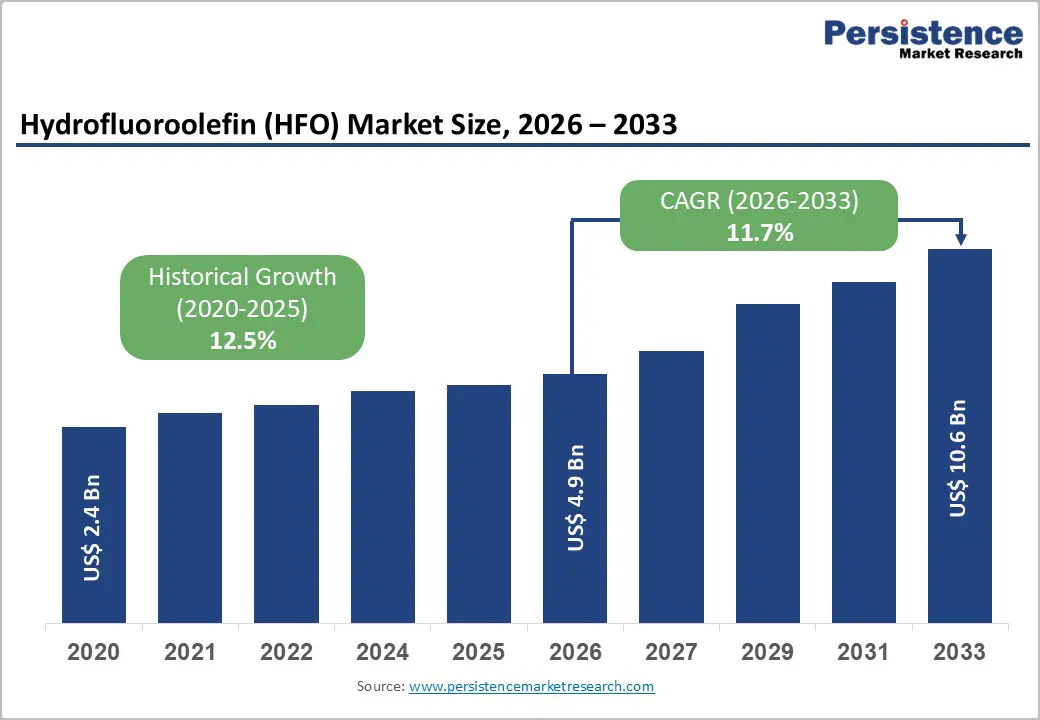

The global hydrofluoroolefins (HFO) market size is expected to be valued at US$ 4.9 billion in 2026 and projected to reach US$ 10.6 billion by 2033, growing at a CAGR of 11.7% between 2026 and 2033.

This exceptional growth trajectory is fundamentally anchored in the global regulatory phase-down of high global warming potential (GWP) hydrofluorocarbons (HFCs) under the Kigali Amendment to the Montreal Protocol, which is compelling governments, industries, and OEMs worldwide to transition to ultra-low GWP HFO refrigerants and blowing agents. HFOs, characterized by a GWP of less than 1 compared to several thousand for incumbent HFCs, offer a chemically compatible, high-performance, and environmentally sustainable transition pathway. The mandated adoption of HFO-1234yf as the standard automotive air conditioning refrigerant across major vehicle markets, combined with expanding applications in stationary HVAC systems, polyurethane foam manufacturing, and precision electronics cleaning, is reinforcing broad-based and structurally durable demand growth through the forecast period.

Key Industry Highlights

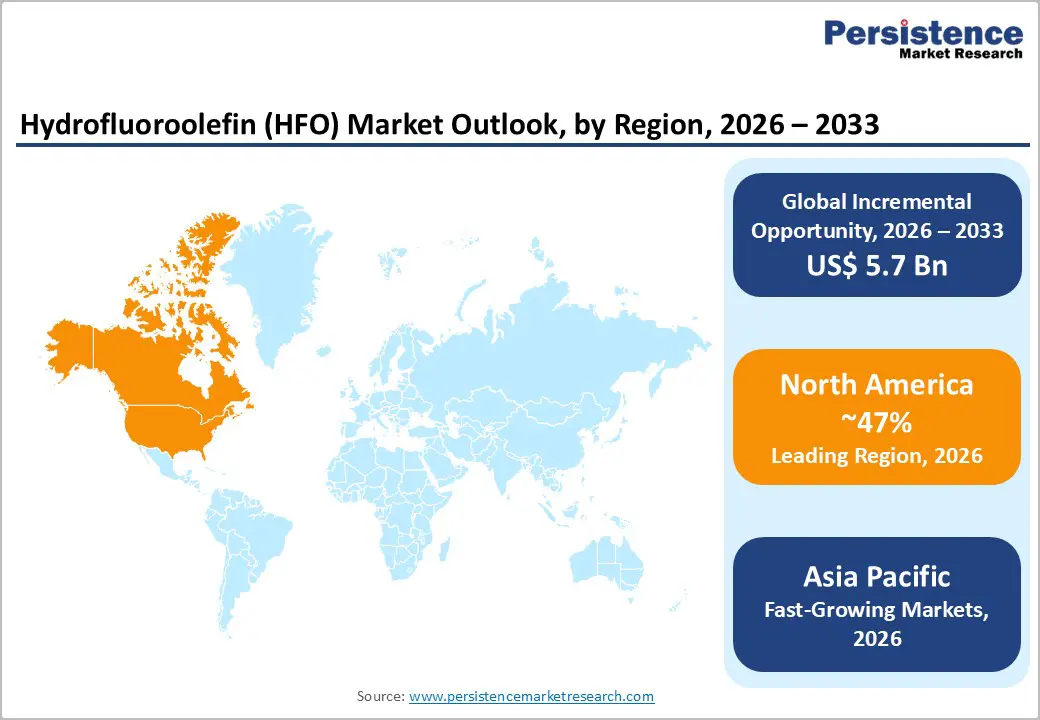

- Leading Region: North America leads the global HFO Market, holding approximately 47% of market share in 2025, anchored by the AIM Act’s comprehensive HFC phase-down framework and the dominant global production presence of Honeywell International and The Chemours Company in HFO-1234yf supply.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of approximately 15% through 2033, propelled by China’s massive automotive production volumes, Japan’s HVAC industry leadership, India’s Kigali Amendment commitments, and rapidly expanding ASEAN electronics manufacturing.

- Dominant Segment: HFO-1234yf dominates the product type segment with an extraordinary 87% market share in 2025, underpinned by multinational regulatory mandates replacing HFC-134a in automotive mobile air conditioning across the EU, US, Japan, and an expanding number of global jurisdictions covering approximately 90 million vehicles produced annually.

- Fastest Growing Segment: Electronics and Precision Cleaning is the fastest-growing end-use segment, projected to expand at a CAGR of 29% through 2033, driven by soaring demand for ultra-pure, residue-free HFO-based cleaning solvents in advanced semiconductor packaging, 5G electronics manufacturing, and high-reliability PCB cleaning applications globally.

- Key Opportunity: HFO-1336mzz presents the most compelling emerging opportunity, as its unique high-temperature thermodynamic properties position it as the preferred low-GWP refrigerant for industrial high-temperature heat pumps and organic Rankine cycle systems, critical decarbonization technologies for energy-intensive industries under tightening global climate mandates.

| Key Insights | Details |

|---|---|

| Hydrofluoroolefins (HFO) Market Size (2026E) | US$ 4.9 Billion |

| Market Value Forecast (2033F) | US$ 10.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 11.7% |

| Historical Market Growth (2020 - 2025) | 12.5% |

Market Dynamics

Drivers - Kigali Amendment and Global HFC Phase-Down Creating Structural Demand for HFO Refrigerants

The Kigali Amendment to the Montreal Protocol, which entered into force in January 2019 and has since been ratified by over 150 countries, represents the single most consequential regulatory driver for the global HFO market. The amendment mandates a staged reduction in the production and consumption of hydrofluorocarbons (HFCs), which have GWPs ranging from 1,000 to 14,800, by 80-85% over the next three decades. Under this framework, developed nations including the United States, the European Union member states, and Japan are required to achieve an 85% reduction in HFC consumption by 2036 relative to their baseline levels, while developing nations follow a delayed but mandatory reduction schedule. HFOs, with their near-zero GWP profiles and performance characteristics comparable to incumbent HFC refrigerants, are the preferred transition solution for stationary refrigeration, commercial air conditioning, and heat pump applications. The U.S. Environmental Protection Agency’s (EPA) AIM Act regulations and the EU F-Gas Regulation (EU) 2024/573, which significantly tighten HFC phase-down timelines, are accelerating domestic and European HFO adoption, generating consistent volume and revenue growth for HFO producers across the forecast period.

Mandatory Adoption of HFO-1234yf in Automotive Air Conditioning Systems Globally

Regulatory mandates requiring the replacement of HFC-134a (GWP: 1,430) with HFO-1234yf (GWP: 4) in mobile air conditioning (MAC) systems have established automotive air conditioning as the dominant and most structurally secure application for the HFO market. The European Union’s MAC Directive (2006/40/EC) has required all new vehicle platforms to use refrigerants with a GWP below 150 since January 2017, effectively mandating HFO-1234yf adoption across all EU-sold vehicles. The United States followed with EPA SNAP Program approvals and California Air Resources Board (CARB) regulations that have progressively encouraged OEM transition, while Japan and South Korea have adopted comparable standards under their respective environmental frameworks. According to Honeywell International, which co-developed HFO-1234yf alongside Chemours, the global automotive sector processes hundreds of millions of vehicles requiring MAC refrigerant service and replacement annually, ensuring a substantial and recurring demand base. As automotive production recovers and EV adoption introduces new thermal management requirements, HFO-1234yf demand in the automotive segment is expected to remain robust through 2033.

Restraints - High Production Costs and Premium Pricing Relative to Legacy HFC Refrigerants

Despite their compelling environmental profile, HFO refrigerants command a significant price premium over the HFC refrigerants they are designed to replace. HFO-1234yf, for instance, is priced approximately 5-10 times higher per kilogram than HFC-134a in commodity markets, a differential primarily attributable to the complexity of its multi-step fluorochemical synthesis process and the limited number of global producers currently holding the proprietary manufacturing technology. This pricing gap creates adoption resistance in cost-sensitive markets, particularly in developing economies across Asia, Latin America, and Africa, where the financial burden of retrofitting existing refrigeration equipment and sourcing more expensive HFO refrigerants is significant. For small and medium-sized HVAC operators and food retail businesses in emerging markets, the total cost of ownership implications of transitioning to HFO-based systems can delay adoption timelines, constraining the pace of global market expansion.

Flammability Characteristics of Select HFO Products Restricting Certain Applications

A number of commercially significant HFO compounds, including HFO-1234yf and HFO-1234ze(E), are classified as mildly flammable refrigerants under ASHRAE Standard 34, receiving an A2L flammability classification. While their flammability is significantly lower than hydrocarbon refrigerants such as propane (R-290), this classification necessitates the use of safety-certified equipment, modified system designs, and installation protocols that comply with updated building codes and safety standards. The requirement for A2L-compliant components, including updated compressors, leak detection systems, and charge-limiting system designs, adds engineering complexity and incremental cost to HVAC system manufacturers and installers, particularly in residential and light commercial segments. Regulatory harmonization of A2L safety standards across jurisdictions remains incomplete, creating compliance uncertainty that slows market penetration in certain geographies.

Opportunity - HFO-1336mzz Emerging as a High-Growth Opportunity in High-Temperature Heat Pump and ORC Applications

HFO-1336mzz, available in two isomers, (Z) and (E), is emerging as one of the highest-potential growth compounds within the HFO family, driven by its unique thermodynamic properties that make it ideal for high-temperature heat pump (HTHP) systems, organic Rankine cycle (ORC) power generation, and centrifugal chiller applications. The (Z) isomer, commercialized by Honeywell under the trade name Solstice® MZ and by Chemours as Opteon™ MZ, has a GWP below 2 and an atmospheric boiling point of approximately 33.4°C, enabling efficient operation in high-temperature industrial heat recovery applications up to 180°C. The International Energy Agency (IEA) has identified industrial heat pumps as a critical decarbonization technology for energy-intensive industries, projecting that HTHP could meet up to 20% of global industrial low-temperature heat demand by 2030. As European industrial decarbonization policies under the EU Industrial Emissions Directive and national energy efficiency programs drive investment in HTHP systems, HFO-1336mzz demand is expected to grow at a significantly above-average CAGR through 2033, representing a compelling revenue expansion opportunity for HFO producers.

Rapidly Expanding Electronics and Precision Cleaning Segment Offering a High-Margin Growth Avenue

The electronics and precision cleaning segment is the fastest-growing end-use application for HFOs, projected to expand at an extraordinary CAGR of approximately 29% between 2026 and 2033. This growth is driven by the escalating complexity of printed circuit board (PCB) assemblies, advanced semiconductor packaging, and miniaturized electronic components, all of which require ultra-pure, residue-free cleaning processes that conventional aqueous or solvent cleaning systems cannot reliably deliver. HFO-1233zd(E) and HFO-1336mzz(Z) are emerging as leading precision cleaning agents due to their zero ozone depletion potential (ODP), near-zero GWP, non-flammability, and excellent solvency for flux residues and contamination in high-reliability electronics manufacturing. The global semiconductor industry, which surpassed US$ 500 billion in revenue in 2023 according to the Semiconductor Industry Association (SIA), requires stringent cleaning standards for advanced node chip packaging, driving accelerating adoption of HFO-based cleaning solvents. As 5G infrastructure rollout, electric vehicle power electronics, and advanced AI chip packaging demand continues to grow, the electronics precision cleaning opportunity represents a structurally durable and high-margin growth avenue for HFO manufacturers through the forecast period.

Category-wise Analysis

Product Type Insights

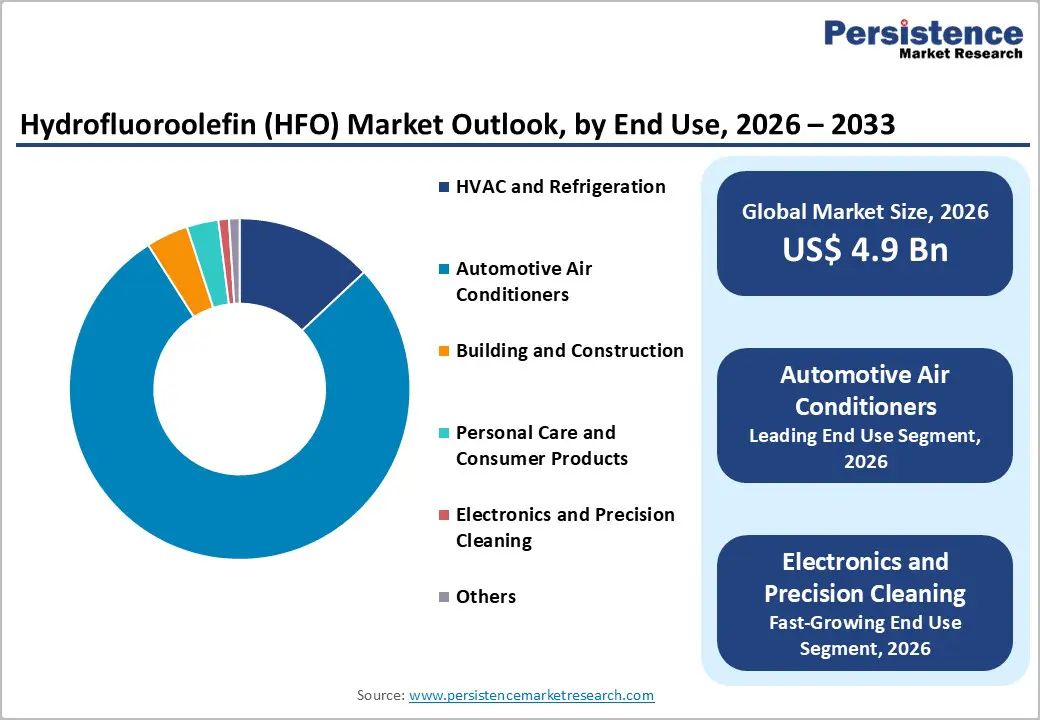

HFO-1234yf dominated the global Hydrofluoroolefins (HFO) Market by product type, commanding an overwhelming 87% share of total market revenue in 2025. This extraordinary concentration reflects the compound’s near-universal regulatory mandate as the replacement refrigerant for HFC-134a in automotive mobile air conditioning systems across the European Union, United States, Japan, South Korea, and an expanding list of jurisdictions globally. HFO-1234yf possesses a GWP of just 4, 99.7% lower than HFC-134a, and offers comparable thermodynamic performance, enabling seamless system integration with modified component specifications. The compound is produced primarily by Honeywell International (under the Solstice® YF brand) and The Chemours Company (under the Opteon™ YF brand), giving these two producers considerable market influence over global supply and pricing. The global vehicle parc of over 1.4 billion cars requiring periodic MAC service ensures a recurring, high-volume demand base. HFO-1336mzz is the fastest-growing product type segment, supported by its expanding role in high-temperature heat pumps, centrifugal chillers, and precision electronics cleaning.

Application Insights

Refrigerants dominated the Hydrofluoroolefins (HFO) Market by application, accounting for approximately 95% of total market share in 2025. The overwhelming dominance of the refrigerant application is a direct consequence of the global regulatory phasedown of HFC refrigerants and the concurrent mandated transition to low-GWP alternatives across mobile air conditioning, stationary HVAC, commercial refrigeration, and industrial cooling applications. HFO refrigerants, including HFO-1234yf for automotive MAC systems, HFO-1234ze(E) for stationary air conditioning and heat pumps, and HFO-blend products such as R-454B and R-32/HFO mixtures, offer a regulatory-compliant, high-performance solution for a broad spectrum of refrigeration applications. The European F-Gas Regulation (EU) 2024/573, which introduces further tightened HFC quotas, is compelling HVAC equipment manufacturers and refrigerant distributors to accelerate HFO refrigerant integration across new equipment installations and retrofit programs. Solvent and Cleaning Agents represent the fastest-growing application segment, driven by precision electronics cleaning demand in the semiconductor and advanced electronics manufacturing industries.

End-user Insights

Automotive Air Conditioners dominated the Hydrofluoroolefins (HFO) Market by end use, representing 78% of total market share in 2025. The segment’s leadership is a direct and structurally permanent consequence of multinational regulatory mandates requiring the replacement of HFC-134a with HFO-1234yf in all newly manufactured passenger cars and light commercial vehicles. Since the EU MAC Directive took full effect in 2017, virtually all new vehicles sold across the European Union, and increasingly across the United States, Japan, Canada, and Australia, are factory-filled with HFO-1234yf, creating an enormous and recurring annual demand base driven by both new vehicle production and aftermarket service needs. Global automotive production of approximately 90 million vehicles annually according to the International Organization of Motor Vehicle Manufacturers (OICA) underpins the scale of this demand. The Electronics and Precision Cleaning end-use segment is the fastest-growing, projected to expand at an exceptional CAGR of 29% through 2033 as advanced semiconductor packaging and high-reliability electronics manufacturing ramp globally.

Regional Insights

North America Hydrofluoroolefins (HFO) Market Trends and Insights

North America is the leading regional market for Hydrofluoroolefins, holding approximately 47% of global market share in 2025. The United States is the dominant national market, underpinned by a comprehensive and accelerating regulatory framework governing HFC phase-down and HFO adoption. The American Innovation and Manufacturing (AIM) Act of 2020 granted the U.S. Environmental Protection Agency (EPA) broad authority to phase down HFC production and consumption, establish HFC allocation programs, and promote the adoption of HFO and other low-GWP alternatives. The EPA’s subsequent rulemaking under the AIM Act has progressively restricted HFC use across refrigeration, HVAC, and foam-blowing applications, creating a clear regulatory pull for HFO substitutes. North America is also home to the two most influential global HFO producers, Honeywell International (headquartered in Charlotte, North Carolina) and The Chemours Company (headquartered in Wilmington, Delaware), giving the region a dominant position in global HFO supply chain governance and pricing dynamics.

Beyond automotive MAC systems, the North American HVAC sector is undergoing a structural transition toward HFO-based refrigerant blends, with R-454B (a blend containing HFO-1234yf) and R-32 increasingly being specified in new residential and commercial air conditioning equipment as the industry prepares for the EPA’s scheduled reduction of R-410A (a high-GWP HFC blend) under the AIM Act framework. Major HVAC OEMs including Carrier Global, Lennox International, and Trane Technologies have begun transitioning product lines to A2L-compatible equipment designed for low-GWP HFO refrigerant blends, generating incremental HFO demand across the region’s large installed base replacement cycle.

Europe Hydrofluoroolefins (HFO) Market Trends and Insights

Europe represents the second-largest regional market for HFOs, driven by the most rigorous and long-established regulatory framework for fluorinated gas (F-gas) management globally. The European Union’s revised F-Gas Regulation (EU) 2024/573, which entered into force in March 2024, significantly strengthens the existing phase-down trajectory for HFCs, setting ambitious quota reduction milestones that are expected to cut total HFC consumption by approximately 95% by 2030 compared to 2015 baselines. This regulatory environment has made Europe a structurally strong and growing market for all HFO product types, with particular demand concentration in refrigerant and foam blowing agent applications. Germany, the United Kingdom, France, and Spain collectively represent the largest national markets within Europe, with their substantial automotive manufacturing sectors, particularly Germany’s OEM ecosystem comprising BMW, Mercedes-Benz, Volkswagen, Audi, and Porsche, generating substantial baseline demand for HFO-1234yf in automotive MAC applications.

The European building and construction sector is also a growing end-use driver, as the EU’s Energy Performance of Buildings Directive (EPBD) mandates increasing energy efficiency standards for new and renovated buildings, stimulating investment in advanced heat pump systems that increasingly incorporate HFO refrigerant blends. France has been particularly proactive, with national incentive programs supporting heat pump installation in residential buildings driving accelerated HFO refrigerant demand. The UK’s F-Gas Regulation GB, maintained post-Brexit with comparable stringency to the EU framework, ensures that the United Kingdom maintains aligned HFC phase-down timelines, preserving the regulatory coherence that supports HFO market development across the broader European region.

Asia Pacific Hydrofluoroolefins (HFO) Market Trends and Insights

Asia Pacific is the fastest-growing regional market for Hydrofluoroolefins, expected to expand at a CAGR of approximately 15% between 2026 and 2033, driven by the combination of the world’s largest automotive and HVAC manufacturing industries, an accelerating regulatory transition toward low-GWP refrigerants, and the rapid growth of advanced electronics manufacturing that is expanding demand for HFO-based precision cleaning solvents. China, the world’s largest automobile producer, manufacturing over 30 million vehicles in 2023 according to the China Association of Automobile Manufacturers (CAAM), represents by far the largest national market for HFO-1234yf in the region. China’s progressive adoption of MAC refrigerant standards aligned with global low-GWP requirements is driving significant volume growth for HFO-1234yf, with domestic producers including Beijing Yuji International Co., Ltd. scaling manufacturing capacity to serve the national automotive supply chain.

Japan is a technically advanced HFO market, with Daikin Industries, Ltd., the world’s largest HVAC manufacturer, and AGC Inc. (formerly Asahi Glass) playing leading roles in HFO product development, manufacturing, and global commercialization. Japan’s progressive Act on Rational Use and Proper Management of Fluorocarbons provides a structured regulatory framework for HFC phase-down that is systematically increasing HFO adoption across both automotive and stationary HVAC applications. India is an emerging high-growth frontier, with the Bureau of Energy Efficiency (BEE) and the country’s commitment under the Kigali Amendment, ratified by India in 2021 with a freeze on HFC consumption by 2028, creating a forward-looking regulatory pull for HFO adoption in the country’s rapidly expanding HVAC and refrigeration sectors. Across ASEAN nations including Thailand, Vietnam, and Indonesia, growing electronics manufacturing investment and expanding automotive production are generating incremental HFO demand that will contribute materially to Asia Pacific’s market leadership through 2033.

Competitive Landscape

The global Hydrofluoroolefins (HFO) market exhibits a highly consolidated structure, characterized by a limited number of vertically integrated fluorochemical producers controlling core intellectual property, feedstock access, and large-scale production assets. Entry barriers remain substantial due to complex synthesis pathways, patent protection, regulatory certification requirements, and high capital intensity. A dominant share of revenue is concentrated in HFO-1234yf, where a small group of manufacturers maintains technological and capacity advantages, reinforcing pricing discipline and long-term supply agreements with automotive OEMs.

Competitive strategies focus on capacity expansion in Asia-Pacific, backward integration into key intermediates, and development of next-generation low-GWP blends for stationary HVAC and commercial refrigeration transitions. Companies are also strengthening application engineering capabilities to support industrial heat pumps and semiconductor cleaning applications. Regulatory advisory services, lifecycle emissions validation, and global distribution partnerships further serve as differentiators, enabling suppliers to secure multi-year contracts and maintain strategic positioning in a compliance-driven market environment.

Key Developments:

- February, 2026: Stallion India Fluorochemicals announced a INR 200 crore investment MoU with the Government of Rajasthan to establish a Hydrofluoroolefin (HFO) manufacturing facility in Bhilwara as part of its capacity expansion strategy.

- August, 2025: Arkema commissioned a new 15 kt Forane 1233zd HFO production unit in Calvert City, Kentucky, expanding domestic sustainable fluorospecialties capacity to support insulation and thermal management markets.

- March, 2024: Thermoseal USA unveiled its 2024 HFO closed-cell spray-foam product line, highlighting new HFO-based formulations with high R-values and improved performance for residential, commercial, and industrial insulation applications.

Companies Covered in Hydrofluoroolefins (HFO) Market

- Honeywell International, Inc.

- Arkema, Inc.

- The Chemours Company

- Central Glass Co., Ltd.

- Danfoss

- Linde PLC

- Climalife (Dehon Group)

- AGC Chemicals Americas, Inc.

- Daikin Industries, Ltd.

- Beijing Yuji International Co., Ltd.

- Mexichem Fluor (Orbia)

- Solvay S.A.

- Zhejiang Juhua Co., Ltd.

- Sinochem Lantian Co., Ltd.

- Navin Fluorine International Ltd.

Frequently Asked Questions

The hydrofluoroolefins market is expected to reach US$ 4.9 billion in 2026, driven by regulatory refrigerant transitions and strong HFO-1234yf adoption.

Demand is driven by the global HFC phase-down under the Kigali Amendment and mandated use of HFO-1234yf in automotive air conditioning.

North America leads with around 47% share, supported by U.S. regulations and strong domestic manufacturing.

Growth opportunities include HFO-1336mzz in industrial heat pumps and HFO-based solvents in semiconductor cleaning.

Major players include Honeywell, Chemours, Arkema, Daikin, AGC Chemicals, Solvay, Orbia, Zhejiang Juhua, and Navin Fluorine.