- Inks, Coatings, Adhesives & Sealants (ICAS)

- Laminating Adhesives Market

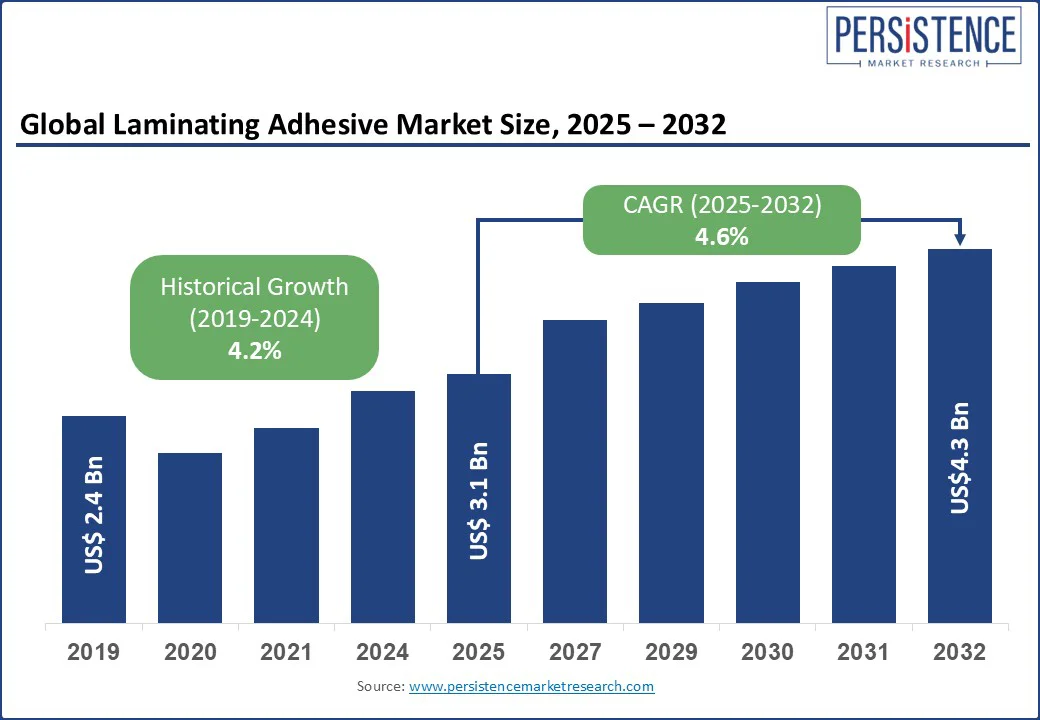

Laminating Adhesives Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Laminating Adhesives Market by Resin Type (Polyurethane (PU), Acrylic), Application Type (Solvent-based, water-based, Solvent-less), End Use (Packaging, Automobile & Transportation, Industrial), and Regional Analysis for 2025 - 2032

Laminating Adhesives Market Size & Forecast

Market Overview

The global laminating adhesives market size is likely to be valued at US$ 3.1 billion in 2025 and is expected to reach US$ 4.3 billion by 2032, growing at a CAGR of 4.6% from 2025 to 2032. Growing demand for flexible packaging in food and pharma drives the laminating adhesives market, with rising preference for lightweight and eco-friendly adhesive solutions.

The global laminating adhesives market is essential to packaging, automotive, and industrial applications, driven by rising demand for high-performance bonding solutions. Key growth factors include the increasing use of flexible packaging adhesives, innovations in solvent-free and bio-based laminating adhesives, and expanding automotive production requiring heat- and chemical-resistant adhesives. Asia Pacific is the fastest-growing laminating adhesives market, supported by industrialization, eco-friendly adhesive demand, and favorable government initiatives. North America and Europe continue to lead due to advanced R&D, strict environmental regulations, and strong infrastructure for packaging and automotive manufacturing.

Market Dynamics

Drivers

Advancements in Adhesive Technologies

Advancements in adhesive formulations, such as low-VOC water-based adhesive for multilayer film lamination, are driving growth in the laminating adhesives market. The increasing shift toward water-based lamination glue, solvent-less, and UV technologies supports global sustainability efforts while enhancing bonding performance in complex packaging and industrial applications.

These developments also align with regulatory mandates and consumer demand for eco-friendly solutions. Flexible packaging adhesives and PU laminating adhesives now deliver stronger bonds with reduced emissions. For example, Henkel AG increased its R&D spending by 20% on VOC-compliant laminating adhesives in 2023. For instance, The U.S. District of Columbia’s 20 DCMR § 744 regulation mandates VOC limits, encouraging adoption of sustainable formulations.

Growth in Automotive and Transportation Sector

The global automotive industry, valued at US$ 2.8 trillion in 2023, is increasingly using laminating adhesives to reduce vehicle weight and improve fuel efficiency. These adhesives are replacing traditional mechanical fasteners in lightweight components, supporting the industry's shift toward more efficient manufacturing methods. Laminating adhesives play a vital role in achieving durability, flexibility, and resistance under high temperatures in vehicle interiors and structures.

With the rapid adoption of electric vehicles, particularly in China, demand for advanced bonding solutions has surged. For instance, according to the International Energy Agency (IEA), China accounted for nearly 60% of global EV sales in 2023, significantly boosting the need for battery bonding and flexible electronics lamination adhesives.

Restraints

High Production and R&D Costs

High production and R&D costs present a key challenge in the laminating adhesives market. Developing advanced laminating adhesives-especially bio-based and solvent-less adhesive solutions-requires significant investment. For example, 3M Company invested US$ 1.1 billion in adhesive R&D in 2023. These high costs create barriers for new entrants and contribute to higher laminating adhesive prices, limiting adoption in cost-sensitive markets. This is particularly impactful in emerging regions, where demand for flexible packaging adhesives and automotive laminating adhesives is growing but remains price-driven.

Volatility in Raw Material Prices

Volatility in raw material prices, particularly petrochemical-based inputs such as polyurethane precursors, poses a major challenge for the laminating adhesives market. Fluctuating crude oil prices directly impact the cost of manufacturing adhesives. According to the U.S. Energy Information Administration, an 18% fluctuation in crude oil prices in 2024 significantly affected adhesive pricing. This volatility puts pressure on production margins and complicates cost management for manufacturers such as Bostik SA, especially amid rising demand for flexible packaging adhesives and high-performance laminating adhesive solutions across key end-use industries.

Opportunities

Growth in Emerging Markets

Emerging markets such as Asia-Pacific and Latin America are fueling growth in the laminating adhesives market. Rapid industrialization and expanding packaging sectors are creating strong demand for high-performance laminating adhesive solutions. In India, the packaging industry was valued at US$ 75 billion in 2024 and is projected to grow steadily, according to the Indian Brand Equity Foundation. This expansion is driving increased use of laminating adhesives in food packaging pouches and flexible packaging applications, offering significant opportunities for manufacturers targeting cost-effective and durable adhesive technologies in high-growth regions.

Expansion in Industrial Applications

The laminating adhesives market is experiencing strong growth across industrial applications, particularly in the electronics and construction sectors. The global electronics market, valued at US$ 1.5 trillion in 2023, relies heavily on laminating adhesives for electronic component bonding, thermal insulation, and circuit board assembly. Rising demand for smartphones, electric vehicles, and IoT devices is fueling adhesive usage in high-precision electronics manufacturing. In the construction industry-valued at over US$ 10 trillion-laminating adhesives are increasingly used in insulation panels, flooring, and structural composites, offering strong, durable bonds essential for long-term performance in demanding environments.

Category-wise Analysis

Resin Type Insights

- Polyurethane (PU) adhesives dominate with a 46.34% market share in 2024, due to their flexibility, durability, and applicability across the packaging and automotive sectors.

- Acrylic adhesives are projected to witness steady growth from 2025 to 2032, driven by their eco-friendly properties and the rising adoption of water-based formulations across various industries.

Application Type Insights

- Solvent-based adhesives currently dominate the laminating adhesives market because of their strong performance and wide use in packaging. However, solvent-less adhesives are gaining rapid traction, supported by global regulations promoting VOC-compliant solutions that offer environmental benefits and improved safety during application.

- The rising demand for sustainable packaging is fueling the growth of water-based lamination glue, known for its low-VOC emissions, eco-friendly adhesive properties, and regulatory compliance. This makes it a preferred green laminating adhesive in industries such as food packaging, consumer goods, and flexible packaging solutions.

End-Use Insights

- Packaging dominates with a 70.54% market share in 2024, driven by demand for flexible packaging in the food and e-commerce sectors.

- Automotive adhesives used in interior laminating applications are showing strong growth due to the need for high-temperature resistance and durable bonding. These advanced laminating adhesives enhance vehicle performance, reduce weight, and meet the increasing demand for thermal stability in electric and fuel-efficient vehicles.

Regional Insights

North America Laminating Adhesives Market Trends

North America remains a key player in the adhesives market, driven by industrial demand and sustainability initiatives.

- U.S.: Leads with a 22.4% global market share in 2024, supported by a US$ 190 billion packaging industry (PMMI) and automotive sector. The EPA’s push for low-VOC adhesives boosts water-based adhesive adoption by 15% annually.

- Canada: Contributes to a growing demand for eco-friendly adhesives in the construction and automotive industries.

- Mexico: Rising manufacturing activities and investments in infrastructure further drive adhesive consumption, particularly in packaging and automotive sectors.

Europe Laminating Adhesives Market Trends

Europe’s adhesives market continues to grow, driven by strong industrial demand, regulatory push for sustainability, and sector-specific needs.

- Germany: Leads with a 28% regional market share in 2024, driven by its US$ 40 billion packaging industry (VDMA). EU sustainability regulations, including the Green Deal, have boosted bio-based adhesive sales by 10% annually.

- France: The automotive sector, producing 2.5 million vehicles in 2023, fuels adhesive demand, particularly in lightweight vehicle components.

- UK: Contributes with a 4% annual growth in its packaging sector, supported by increasing demand for eco-friendly and efficient adhesive solutions.

Asia-Pacific Laminating Adhesives Market Trends

Asia-Pacific dominates the global adhesives market, driven by rapid industrialization, growing consumer demand, and a focus on sustainability.

- China: Leads with a major contribution to the region’s 48.2% market share in 2024, driven by a US$ 150 billion packaging industry and a booming electric vehicle (EV) market, which significantly increases adhesive demand.

- India: Industrial growth, fueled by the Make in India initiative, propels adhesive consumption, rising by 9% annually.

- Regional Focus: The region is prioritizing sustainable adhesives, aligning with global environmental trends and increasing demand for eco-friendly solutions.

Competitive Landscape

The global laminating adhesives market is highly competitive, driven by key players such as Henkel AG & Co. KGaA, Dow Inc., Bostik SA, and DuPont. These companies leverage strong product portfolios and global distribution networks. R&D investments in sustainable laminating adhesives—such as bio-based and solvent-less solutions-support regulatory compliance and eco-friendly trends.

Strategic partnerships with packaging and automotive manufacturers boost market presence. Firms such as Bostik focus on cost-efficient production to offset raw material price volatility, while others expand across Asia Pacific and Africa through localized manufacturing.

Key Developments

- 2024: Henkel AG launched a bio-based adhesive for flexible packaging, reducing carbon emissions by 28%.

- 2023: Dow Inc. invested US$ 500 million in solvent-less adhesive R&D, enhancing sustainability.

- 2024: 3M introduced a water-based adhesive for automotive applications, improving bonding efficiency.

Companies Covered in Laminating Adhesives Market

- 3M Company

- Henkel AG & Co. KGaA

- Dow Inc.

- Bostik SA

- DuPont de Nemours, Inc.

- Others

Frequently Asked Questions

Rising demand for flexible packaging, advancements in adhesive technologies, and automotive sector growth are key drivers.

Polyurethane adhesives lead due to their versatility and durability.

Solvent-less adhesives are growing rapidly due to sustainability trends.

Asia-Pacific dominates with a 48.2% share in 2024, led by China and India.

They drive demand for bio-based and water-based adhesives to reduce VOC emissions.

3M, Hen