- Automotive

- Interior Car Accessories Market

Interior Car Accessories Market Size, Share, and Growth Forecast 2026 - 2033

Interior Car Accessories Market by Product Type (Comfort & Convenience Accessories, Interior Styling & Aesthetic Accessories, Electronic & Smart Accessories, Others), by Vehicle Type (Passenger Cars, SUVs & Crossovers, Commercial Vehicles), by Distribution Channel (OEM, Aftermarket), by Regional Analysis, 2026 - 2033

Interior Car Accessories Market Size and Trend Analysis

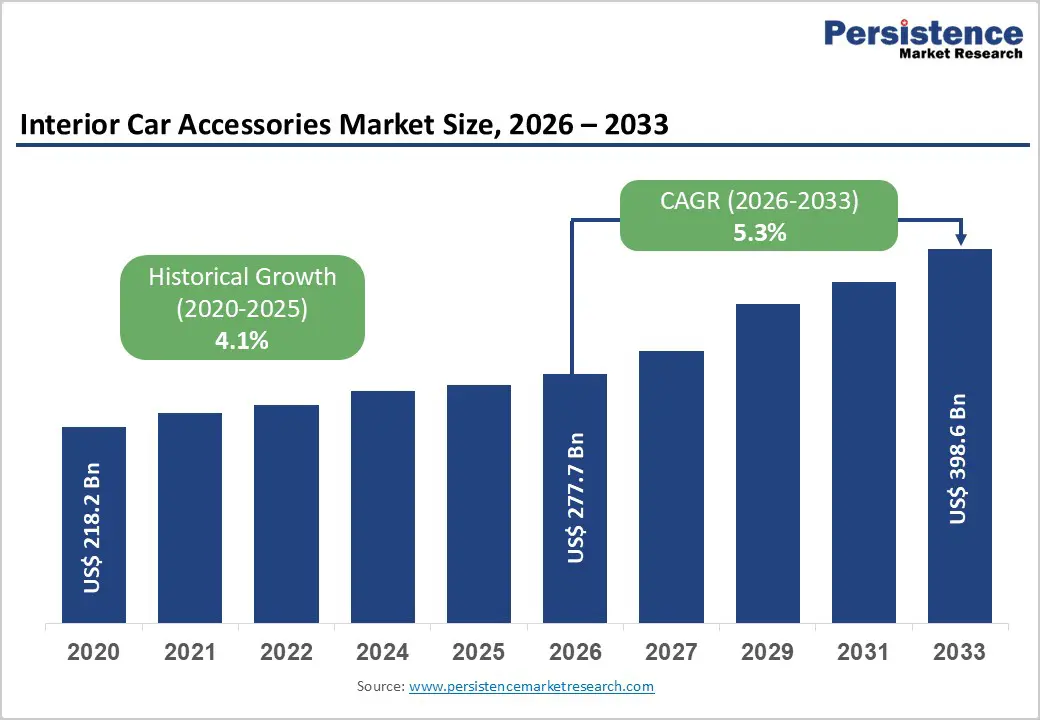

The global interior car accessories market size is expected to be valued at US$ 277.7 billion in 2026 and projected to reach US$ 398.6 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

This growth is driven by rising consumer preference for enhanced in-cabin comfort, aesthetics, and personalization. Increasing global vehicle ownership, coupled with longer vehicle usage cycles, continues to support steady aftermarket demand. Technological advancements, particularly in smart and connected accessories, are reshaping interior designs. The growing adoption of electric vehicles has further accelerated demand for advanced infotainment systems, ambient lighting, and integrated digital features, while improving disposable incomes in emerging economies fuel customization trends.

Key Industry Highlights:

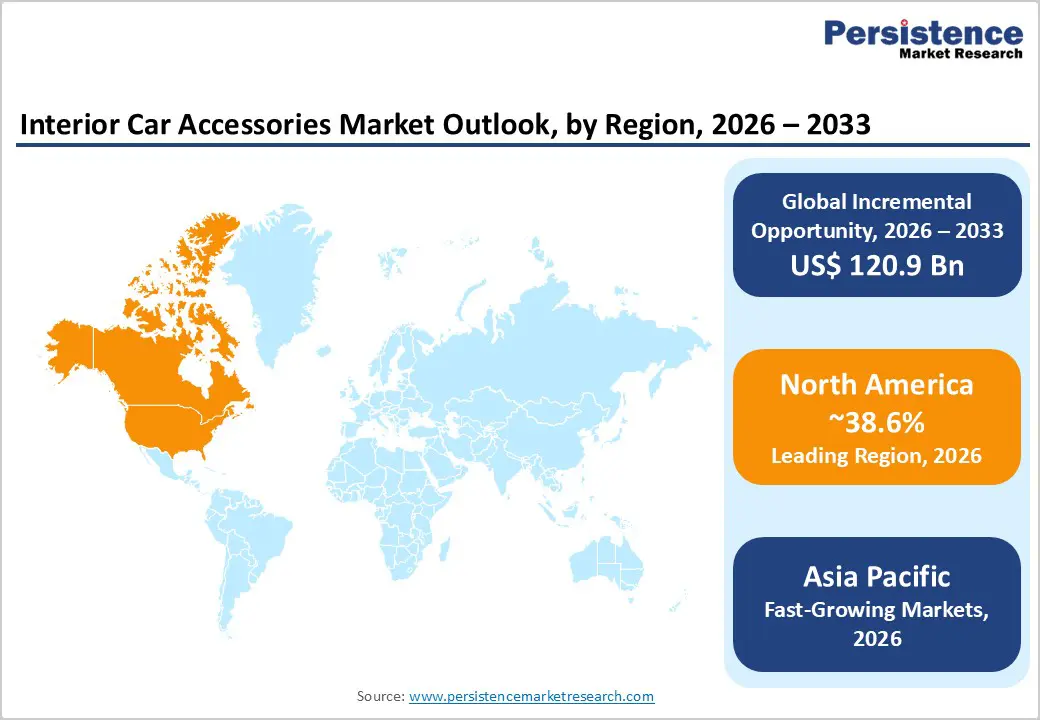

- Leading Region: North America leads the interior car accessories market with 38.6% share in 2025, driven by high vehicle ownership, strong personalization culture, and a mature aftermarket ecosystem.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, with a 35.8% share in 2025, driven by rising vehicle production in China and India, expanding middle-class incomes, and strategic manufacturing hubs such as Thailand.

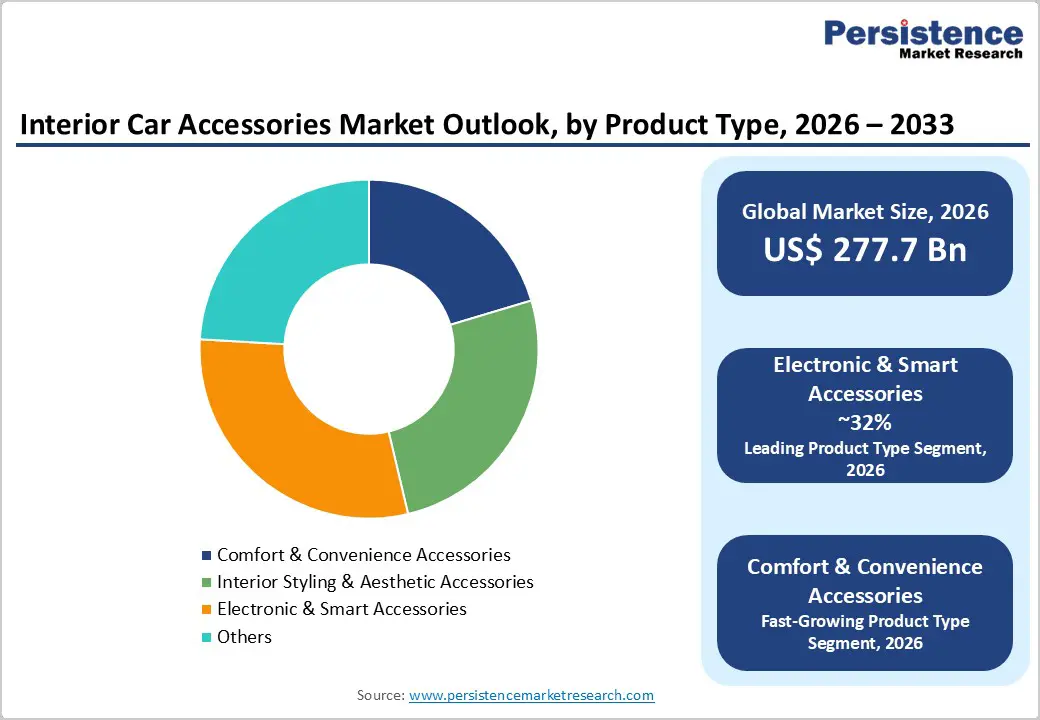

- Leading Product Category: Electronic & Smart Accessories dominate with approximately 32% market share in 2025, driven by consumer demand for infotainment, dash cams, and connectivity integration.

- Fastest-Growing Product Segment: Interior comfort and wellness-focused accessories are gaining traction, driven by ergonomic seating, ambient lighting, and in-cabin air quality solutions.

- Leading Vehicle Segment: SUVs & Crossovers lead with around 31% of the market in 2025, reflecting global preference for versatile, spacious, and safety-focused vehicles.

- Key Opportunity: Smart accessories tailored for electric vehicles present significant growth potential, including digital displays, infotainment, and integrated connectivity solutions.

| Key Insights | Details |

|---|---|

| Interior Car Accessories Size (2026E) | US$ 277.7 billion |

| Market Value Forecast (2033F) | US$ 398.6 billion |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Drivers - Growing Consumer Preference for Personalized and Comfort-Focused Vehicle Interiors

Consumers increasingly view vehicles as extensions of personal identity, driving strong demand for interior car accessories such as seat covers, ambient lighting, customized trims, and comfort-enhancing add-ons. Rising disposable incomes and a cultural shift toward personalization, especially among younger buyers, are accelerating this trend. Interior upgrades enable vehicle owners to enhance aesthetics and comfort without purchasing new vehicles, thereby supporting sustained aftermarket demand.

According to the Specialty Equipment Market Association (SEMA), sales of accessories for alternative-power vehicles reached US$2.5 billion in 2023, highlighting the growing role of personalization across evolving vehicle platforms. In regions with high vehicle ownership, such as North America, consumers increasingly prioritize interior upgrades that enhance comfort and visual appeal while maintaining manufacturer warranties, thereby further strengthening aftermarket adoption.

Increasing Integration of Smart Technologies within Vehicle Interiors

Technological advancements in automotive interiors are a key driver of the interior car accessories market, as consumers demand enhanced connectivity, convenience, and safety features. Smart accessories such as infotainment systems, dash cams, heads-up displays, and wireless charging solutions are gaining traction due to rising smartphone dependency and growing awareness of road safety and navigation efficiency

This trend is reinforced by the rapid adoption of advanced interior electronics by OEMs and aftermarket suppliers. For instance, Gentex Corporation reported shipments of 2.96 million Full Display Mirrors in 2024, reflecting a 21% year-over-year increase. Such technologies significantly improve driver experience and align closely with electric vehicle interiors, where digital cockpits and integrated electronics are increasingly standard.

Restraints - Elevated Pricing of Premium and Technology-Driven Interior Accessories

Premium interior car accessories, particularly smart and electronic products such as advanced infotainment systems, digital displays, and connected safety devices, often carry high price points that limit adoption among cost-sensitive consumers. This challenge is more pronounced in emerging markets, where affordability remains a key determinant of purchasing decisions. Volatility in raw material prices, including plastics, resins, and electronic components, further elevates production costs and retail pricing.

In addition, trade policies and import duties continue to influence accessory costs. U.S. tariffs on Chinese-sourced automotive components, which rose to 25% in 2019, still affect global supply chains and pricing structures. These cost pressures slow the adoption of premium innovations and restrict market penetration across budget-constrained consumer segments.

Supply Chain Constraints Affecting Production and Product Availability

Ongoing global supply chain disruptions pose a significant constraint on the interior automotive accessories market by disrupting manufacturing continuity and product availability. Shortages of key raw materials, including foams, textiles, plastics, and interior trims, have led to inconsistent production schedules and longer lead times. Post-pandemic logistics challenges, such as port congestion and transportation delays, continue to strain global sourcing networks.

Automotive manufacturers and accessory suppliers report persistent difficulties in securing timely component deliveries, directly affecting aftermarket supply. These disruptions limit consumers’ access to interior upgrades, delay product launches, and constrain inventory levels, ultimately slowing market momentum despite steady underlying demand.

Opportunity - Rising Opportunities from Electric Vehicle-Specific Interior Accessories

The accelerating shift toward electric vehicles is creating strong opportunities for interior car accessory manufacturers to develop EV-specific solutions tailored to new vehicle architectures. EV interiors increasingly emphasize digital displays, integrated infotainment systems, ambient lighting, and smart charging management interfaces. As global EV fleets expand, demand for compatible, lightweight, and energy-efficient interior accessories continues to rise, particularly in Asia Pacific, which leads EV production and adoption.

Industry data from SEMA indicate increasing momentum in EV-related accessory sales, suggesting sustained long-term growth potential. Manufacturers can capitalize on this trend by designing multifunctional and modular interior products optimized for EV platforms, enhancing user experience while aligning with evolving digital cockpit and connectivity requirements.

Expanding Potential within the Aftermarket Customization Ecosystem

The aftermarket segment offers significant growth opportunities by enabling cost-effective and flexible interior customization for a broad consumer base. DIY vehicle owners increasingly prefer aftermarket accessories that enable personalization without dependence on dealers, supporting strong demand across online and offline channels. E-commerce platforms, in particular, are expanding global reach and product visibility, strengthening aftermarket penetration.

Opportunities are further emerging in the development of sustainable and eco-friendly interior accessories, as consumers become more environmentally conscious. Companies such as Essentra plc are advancing the use of recycled plastics in automotive components, setting benchmarks for sustainable innovation. This focus on affordability, accessibility, and sustainability positions aftermarket customization as a key avenue for growth.

Category-wise Analysis

Product Type Insights

Electronic & Smart Accessories constitute the leading product category, accounting for approximately 32% of the market in 2025, driven by growing consumer dependence on in-vehicle connectivity and safety features. Products such as infotainment systems, dash cams, wireless chargers, and heads-up displays are increasingly prioritized, supported by smartphone integration trends and regulatory emphasis on driver assistance technologies from authorities such as the National Highway Traffic Safety Administration.

Looking ahead, interior comfort and wellness-focused accessories are emerging as the fastest-growing product segment. Rising awareness of driver fatigue, in-cabin air quality, and ergonomic comfort is accelerating demand for air purifiers, seat comfort solutions, and ambient lighting. These products appeal to daily commuters and long-distance drivers seeking enhanced driving experiences.

Vehicle Type Insights

SUVs & Crossovers dominate the market, with an estimated 31% share in 2025, reflecting global consumer preference for spacious, versatile vehicles that offer higher safety and comfort. Owners of these vehicles tend to invest heavily in premium interior accessories such as customized seat covers, advanced infotainment systems, and cargo management solutions, reinforcing higher accessory attachment rates.

Passenger cars are expected to emerge as the fastest-growing vehicle category for interior accessories. Growth in compact and mid-size car production, particularly in North America and the Asia Pacific, combined with rising personalization among urban consumers, is driving increased adoption of affordable interior upgrades and smart accessories across this segment.

Distribution Channel Insights

The aftermarket channel accounts for roughly 59% of the market in 2025, supported by its flexibility, broad product availability, and cost advantages over OEM-fitted accessories. Consumers favor aftermarket options for interior upgrades, particularly for aging vehicles, as they allow customization without high dealership costs. The expanding presence of generic and compatible parts further strengthens aftermarket penetration.

Online retail platforms are emerging as the fastest-growing distribution channel within the aftermarket ecosystem. Increasing consumer confidence in e-commerce, coupled with DIY installation trends and wider digital product availability, is accelerating online sales. Enhanced logistics networks and competitive pricing further support rapid channel expansion.

Regional Insights

North America Interior Car Accessories Market Trends

North America leads the global interior car accessories market, accounting for over 38.6% share in 2025. Growth is anchored by high vehicle ownership rates, a strong culture of personalization, and mature aftermarket infrastructure. Premium accessories, including dash kits, infotainment systems, and smart interior solutions, are in high demand. Regulatory initiatives by the EPA also encourage sustainable material usage, while R&D in connected technologies fosters innovation. The rising adoption of electric vehicles further boosts demand for integrated digital interiors and advanced infotainment solutions.

In addition, the U.S. aftermarket ecosystem supports widespread availability of cost-effective and premium interior upgrades. Consumers increasingly prioritize comfort, aesthetics, and technology, while aftermarket customization continues to expand across online and offline channels, reinforcing North America’s dominance in the global market.

Europe Interior Car Accessories Market Trends

Europe emphasizes luxury, safety, and regulatory compliance in its interior car accessories market. Germany leads in high-quality components for premium vehicles, while EU-wide emission regulations and safety standards drive the adoption of environmentally friendly materials and advanced interior solutions. Interior lighting and smart infotainment accessories are emerging as key growth segments, with a projected CAGR of 4.8% through 2028, reflecting rising consumer preference for premium and connected interiors.

The UK and France place significant emphasis on bespoke interior upgrades, particularly amid the EV transition. Harmonized European standards facilitate cross-border trade in components and accessories, thereby supporting growth in both the OEM and aftermarket sectors. Increasing adoption of digital and connected features further strengthens Europe’s strategic position in the global market.

Asia Pacific Interior Car Accessories Market Trends

Asia-Pacific is the fastest-growing interior car accessories market, accounting for approximately 35.8% of the market in 2025, driven by rapid vehicle production in China and India. Rising middle-class incomes fuel aftermarket demand for seat covers, floor mats, and technology-enabled accessories. Thailand emerges as a key manufacturing hub, while OEMs like Toyota enhance supply chain efficiency and local production capabilities.

Japan and ASEAN countries focus on integrating advanced technologies and cost-effective solutions to meet growing domestic and export demand. The expanding vehicle base, coupled with increasing urbanization and consumer awareness, accelerates the adoption of both premium and affordable interior accessories, positioning the Asia Pacific as a major growth engine globally.

Competitive Landscape

The global interior car accessories market is highly fragmented, characterized by a strong presence of aftermarket players alongside consolidated OEM suppliers. Market participants compete by offering a wide range of products, focusing on personalization, quality, and functionality to attract diverse consumer segments. Differentiation often stems from innovative designs, material selection, and alignment with evolving vehicle trends, including electric and connected vehicles.

Sustainability and technology integration are key strategies driving competition, with firms increasingly adopting eco-friendly materials and smart, connected accessories. Additionally, e-commerce and direct-to-consumer models are gaining prominence, allowing companies to expand reach, enhance customer engagement, and improve aftermarket penetration globally.

Key Developments:

- In April 2024, Essentra plc advanced sustainable interior solutions by acquiring BMP TAPPI, focusing on developing and testing recycled plastic content for automotive caps, enhancing eco-friendly product offerings, and supporting the growing demand for environmentally responsible interior accessories.

- In January 2025, Gentex Corporation shipped 2.96 million Full Display Mirrors, marking a 21% year-over-year increase, highlighting strong adoption of smart interior technologies and reinforcing its leadership in connected and digital automotive interior solutions globally.

Companies Covered in Interior Car Accessories Market

- Continental AG

- Grupo Antolin

- Hyundai Mobis

- IAC Group

- Visteon Corporation

- Toyota Boshoku Corporation

- Lear Corporation

- Magna International

- Harman International

- Pioneer Corporation

- Garmin Ltd.

- 3M Company

- WeatherTech Direct

- Covercraft Industries

- Car Mate Manufacturing Co., Ltd.

Frequently Asked Questions

The interior car accessories market is expected to reach US$ 277.7 billion in 2026.

Rising vehicle personalization and Electronic & Smart Accessories (32% share in 2025) drive market growth.

North America leads with 38.6% share in 2025, supported by high vehicle ownership and a mature aftermarket.

Smart accessories tailored for EVs present growth potential amid the electrification trends.

Leading players include Essentra plc, FORVIA Faurecia, Adient plc, Yanfeng, and Lear Corporation.