- Semiconductor Materials & Components

- Heating Equipment Market

Heating Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Heating Equipment Market By Product Type (Boilers, Furnaces, Others), Fuel Type (Electric, Gas, Others), Application, and Regional Analysis for 2025 - 2032

Heating Equipment Market Size and Trends Analysis

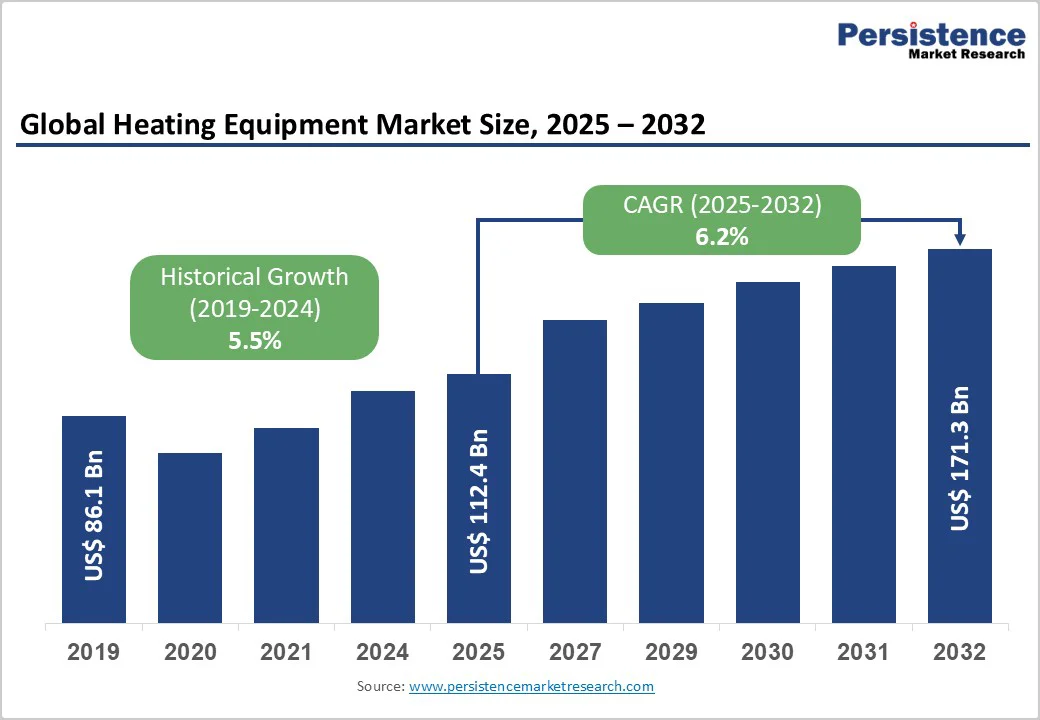

The global heating equipment market is expected to reach US$112.4 billion in 2025. It is expected to reach US$171.3 billion by 2032, growing at a CAGR of 6.2% during the forecast period from 2025 to 2032, driven by a shift toward electric heating, a surge in heat-pump adoption, regulatory decarbonization mandates across Europe and Asia, and rising industrial process-heating requirements in developing markets.

Energy-price volatility and ongoing replacement cycles in commercial and industrial applications support steady demand. Some forecast variability persists due to differences in the definitions of included equipment categories, so projections should be viewed within each vendor’s scope.

Key Industry Highlights

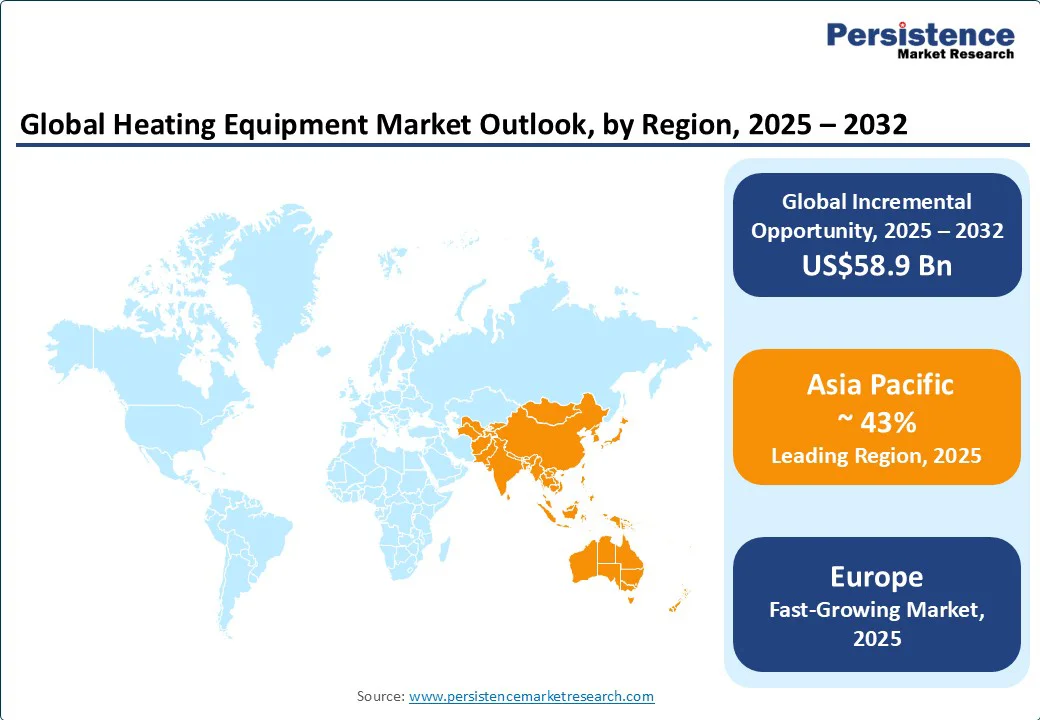

- Leading Region: Asia Pacific, contributing an estimated 43% of global heating-equipment demand, supported by China’s large industrial base, expanding district-heating programs, and strong manufacturing capacity.

- Fastest-Growing Region: Europe, driven by rapid heat-pump adoption, strong retrofit funding, strict efficiency mandates, and fossil-fuel restrictions in new buildings.

- Investment Plans: Major investment priorities include new heat-pump manufacturing lines, low-GWP refrigerant product development, digital energy-management platforms, industrial-equipment production expansions, and district-heating infrastructure upgrades across North America, Europe, and the Asia Pacific.

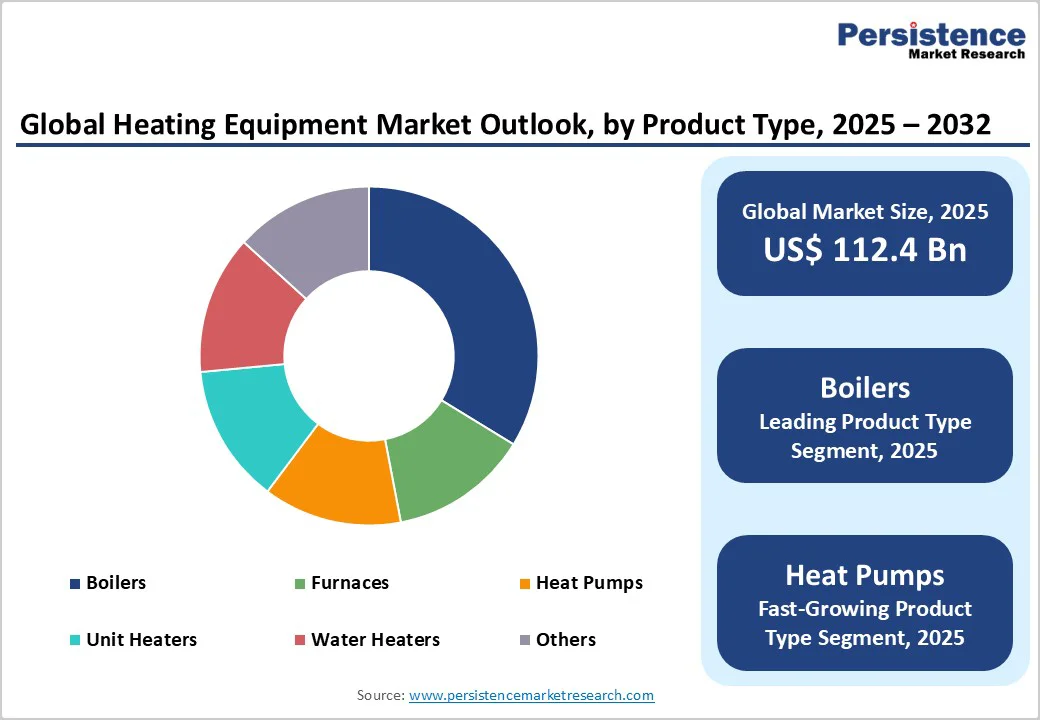

- Dominant Product Type: Boilers, representing approximately 28% of total market revenue due to extensive installed base in industrial facilities and district-heating networks.

- Leading Fuel Type: Gas-fired systems, accounting for roughly 51% of market share across key regions with mature gas-distribution infrastructure and strong replacement demand.

| Key Insights | Details |

|---|---|

| Heating Equipment Market Size (2025E) | US$112.4 Bn |

| Market Value Forecast (2032F) | US$171.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Electrification and Energy-Efficiency Regulations

Electrification is the single strongest structural trend in the market. Heat pumps are expanding rapidly as countries enforce efficiency standards and reduce fossil-fuel reliance. Adoption is accelerating in Europe and advanced Asian markets, supported by building-retrofit programs and consumer incentives.

Electric heating sub-segments frequently record double-digit CAGRs, while fossil-fuel segments grow slowly or contract in mature regions. This shift is responsible for much of the mid-single-digit global CAGR projected through 2032.

Industrial Recovery and High-Capacity Electrified Process Heating

Industrial demand from chemicals, food processing, textiles, and pharmaceuticals continues to recover. Large-capacity boilers, high-temperature heat pumps, and district-heating systems are receiving increased investment.

Governments in several regions are funding industrial electrification and district-energy networks, generating multi-year procurement pipelines. High-temperature electric equipment and industrial heat pumps are increasingly identified as major growth areas within vendor roadmaps.

Retrofit Momentum and Cost-Efficiency Economics in Buildings

Rising energy prices and tightening building codes improve the payback period of efficient heating solutions such as condensing boilers, air-source/ground-source heat pumps, and smart controls. Strong residential and commercial retrofit activity in many developed markets is producing measurable increases in equipment demand. Higher adoption rates in 2023 - 2025 demonstrate the effectiveness of incentives and renovation schemes in lifting near-term revenues.

Barrier Analysis - Fragmented Value Chain and Limited Supply of Critical Components

Heating equipment manufacturing relies on compressors, advanced heat-exchanger materials, and specialized refrigeration components. Supply concentration in a few regions, combined with constraints on low-GWP refrigerants and inverters, has led to longer lead times and higher procurement costs.

OEM lead times in 2023 - 2024 are often extended by several weeks due to logistics and component shortages, increasing inventory pressure. These bottlenecks may hamper market growth unless manufacturers expand local production or diversify sourcing.

Uneven Policy Environments and High Upfront Installation Costs

Despite favorable lifecycle economics for efficient systems, initial capital costs remain a barrier, especially in developing markets. Policy fragmentation across countries results in inconsistent subsidies, financing options, and building-code timelines. Low fossil-fuel prices in some markets further slow transitions to electric systems. Sensitivity analyses presented in vendor studies show that adoption rates may drop by 20-40% in regions without financial incentives.

Opportunity Analysis - Electrified Industrial Heating and High-Temperature Heat Pumps

Industrial electrification presents a substantial long-term opportunity. High-temperature heat-pump systems capable of serving process heat are advancing toward commercialization.

Estimates based on technology roadmaps show that industrial electrified heating could represent an incremental market worth a meaningful percentage of total heating-equipment revenue by 2030, particularly in countries with large manufacturing bases. Integrating heat pumps with waste-heat recovery and digital management systems enables premium positioning.

Services and Heating-as-a-Service models

Service-based contracting and subscription heating models are becoming attractive for both end-users and OEMs. “Heating-as-a-service” packages, combining equipment, maintenance, and performance guarantees, generate recurring revenue and higher margins than one-time sales.

Early pilots in developed markets indicate strong customer retention and improved profitability. These models can mitigate cyclicality in equipment demand and improve OEM financial stability.

Category-wise Analysis

Product Type

Boilers maintain the largest share of the heating equipment market at about 28%, supported by their deep-rooted presence in industrial facilities, district-heating systems, and older building infrastructures. They consistently account for roughly one-quarter to one-third of global revenue, reflecting extensive usage and the higher prices of large-capacity units.

Industries such as chemicals, food processing, and pharmaceuticals depend on steam and hot-water boilers for core operations, reinforcing segment stability. Replacement of aging installations and ongoing demand for maintenance, retrofits, and emissions-control upgrades further sustain leadership. For example, district-energy networks in Northern Europe and East Asia continue to invest in high-efficiency condensing boiler upgrades, thereby preserving their long-term relevance.

Heat pumps represent the fastest-growing category across residential and commercial applications. Their expansion is driven by advances in variable-speed compressors, improved refrigerants, and stronger performance at low temperatures, increasing their suitability across diverse climates.

Air-source heat pumps are seeing robust adoption in Europe, Japan, and South Korea, while ground-source systems gain momentum in North America, particularly for new homes. Hybrid configurations that pair heat pumps with boilers or furnaces are increasingly used in retrofits.

Rising manufacturing capacity in China and Europe is lowering costs and accelerating global uptake. As policy incentives for high-efficiency systems intensify, heat-pump growth is expected to erode boiler share despite rising overall heating demand gradually.

Fuel Type Insights

Gas-fired heating equipment retains a dominant 51% market share, supported by a large installed base and extensive natural-gas distribution networks. Residential gas boilers remain vital in regions with mature pipeline infrastructure, including parts of North America, Europe, and the Middle East.

Ongoing replacement of aging units sustains recurring demand, while commercial buildings continue relying on high-efficiency gas systems for cost-effective performance. Gas heating remains especially important in colder climates where reliability and rapid heat delivery are essential. For example, multi-family housing in countries such as the U.K. and Italy continues to depend on compact gas-fired combi boilers, reinforcing long-term market strength.

Electric heating systems, however, are expanding at a much faster rate due to building electrification and surging adoption of heat pumps, which dominate the electric-heating category. Enhanced energy efficiency, quieter operation, and compatibility with smart thermostats make electric solutions attractive for both new construction and retrofits.

Regions with carbon-reduction mandates, particularly Western Europe and several U.S. states, are accelerating the shift toward electric technologies. Electric radiant floor heating is gaining traction in premium homes, while electric unit heaters are seeing increased use in warehouses and logistics facilities. With continued grid modernization worldwide, electricity-based heating systems are expected to post the highest CAGR across fuel types.

Regional Insights

North America Heating Equipment Market Trends -Electrification Momentum & Efficiency-Driven Retrofits

North America is a mature market, with the U.S. accounting for most regional revenue due to its large installed base and continuous replacement cycles. Market expansion is driven by aging residential infrastructure, strong retrofit activity in commercial buildings, and increasing preference for electric heating solutions. Cold-climate states in the Midwest and Northeast maintain high annual heating loads, creating recurring demand for boilers, furnaces, and heat pumps.

Canada continues to record strong heat-pump adoption supported by federal and provincial incentives aimed at improving building efficiency and reducing emissions. Programs promoting cold-climate air-source heat pumps have also accelerated deployment in regions such as British Columbia and Quebec.

Regulatory developments increasingly shape the technological direction of the market. Updated building-efficiency codes, minimum performance standards, and requirements for low-GWP refrigerants are prompting manufacturers to redesign systems and expand high-efficiency portfolios.

Some U.S. states are implementing electrification-focused policies that restrict the use of fossil-fuel systems in new buildings, shifting both residential and commercial project specifications toward electric alternatives. Investment activity is centered on expanding heat-pump manufacturing capacity, enhancing digital energy-management platforms, and developing service-oriented business models.

Europe Heating Equipment Market Trends - Policy-Led Decarbonization & Heat-Pump Acceleration

Europe is the fastest-growing and one of the most advanced and policy-driven heating markets globally, characterized by ambitious decarbonization programs and extensive funding for building retrofits.

The region continues to lead in heat pump adoption, with strong growth across Germany, France, the U.K., and the Nordic countries. Funding programs supporting home-insulation upgrades, boiler replacements, and efficient electric heating systems underpin sustained demand.

Germany’s heating transition framework, France’s grant-based home renovation incentives, and the U.K.’s low-carbon heating schemes play central roles in accelerating market transformation.

EU-level regulations requiring higher appliance efficiency and a structured phase-down of high-GWP refrigerants influence product design, refrigerant selection, and long-term investment decisions. Many countries are imposing restrictions on fossil-fuel systems in new residential construction, while others are planning phased replacement of oil-based heating systems in existing homes.

Investment trends highlight expansion of heat-pump factories, upgrades to local production lines, and R&D programs focused on next-generation, low-GWP refrigerant systems. District-heating expansion across Scandinavia, Germany, and Central Europe remains an important driver of large-scale equipment demand.

Municipal energy transition initiatives are creating opportunities for high-efficiency boilers, heat exchangers, and modular heat pump plants. Recent developments include the launch of new European production lines dedicated to low-refrigerant-charge heat pumps, government approval of large-scale building-retrofit funding programs, and municipal investments to expand district-heating networks powered by renewable energy.

Asia Pacific Heating Equipment Market Trends -Industrial Scale Growth & Expanding District-Heating Networks

Asia Pacific is the largest market, accounting for 43%, supported by China’s industrial scale, extensive manufacturing ecosystem, and expanding residential base. Continuous urbanization, a growing middle-income population, and rapid construction across major cities in China, India, and Southeast Asia underpin sustained demand for heating solutions.

China maintains a strong domestic manufacturing industry and continues to expand district-heating networks, particularly in Northern provinces. Japan has established a market for high-technology, energy-efficient heating systems, while South Korea and Taiwan continue to invest in high-performance residential units.

India is growing from a smaller baseline, supported by industrial expansion, commercial development, and gradual improvement in electrification readiness. Variability in climate, building stock, and policy enforcement means adoption patterns differ across states. ASEAN markets, particularly Thailand, Malaysia, and Vietnam, are witnessing increasing heat-pump penetration in commercial applications such as hotels, multi-residential complexes, and retail developments.

Investments include expansions of heat-pump manufacturing facilities, upgrades to industrial heating-equipment production lines, and deployment of large municipal heating infrastructure across urban centers.

Recent developments include the commissioning of new heat-pump factories in East Asia to support domestic demand, the expansion of district-heating capacity in northern China, and new government-backed efficiency initiatives in Japan and South Korea to promote next-generation low-energy heating systems.

Competitive Landscape

The global heating equipment market is moderately fragmented. A limited number of global companies possess a strong international presence, while many regional manufacturers compete in specific product niches. Boilers tend to be supplied by specialized industrial firms, whereas heat pumps and residential systems involve a broader set of manufacturers.

Consolidation is rising as companies acquire service providers, expand manufacturing footprints, or integrate complementary product lines.

Core strategies include sustained investment in heat-pump innovation, regional manufacturing localization, expansion through acquisitions, and growth of service-based business models such as maintenance contracts and performance-based heating solutions.

Key Industry Developments

- In March 2025, Daikin announced the EWYK-QZ modular air-to-water heat pump, using propane (R-290), offering capacities from 100 kW (single module) up to 2,000 kW in modular arrays, and able to supply water up to 75 °C.

- In September 2025, Daikin introduced the Altherma 4 H air-to-water heat pump, built for residential use with R-290, ultra-low noise (28 dB), and the capability to heat water up to 75 °C while operating down to -28 °C.

Companies Covered in Heating Equipment Market

- Gilead Sciences

- AbbVie

- Merck & Co.

- Carrier

- Mitsubishi Electric Corporation

- Emerson Electric Co.

- Daikin Industries, Ltd

- Trane

- Robert Bosch GmbH

- Lennox International

- Johnson Controls, Inc.

- Midea Group

- Hitachi, Ltd.

- Rheem Manufacturing Company

- Haier (General Electric)

- Panasonic Holdings Corporation

- Danfoss

- Fujitsu

- LG Electronics, Inc.

- Samsung

Frequently Asked Questions

The global heating equipment market size in 2025 is estimated at US$112.4 Billion.

By 2032, the heating equipment market is projected to reach US$171.3 Billion, driven by rising heat-pump installations, industrial modernization, and building-efficiency mandates.

Key trends include rapid adoption of electric and heat-pump systems, wider use of low-GWP refrigerants, modernization of industrial heating infrastructure, expansion of district-heating networks, and growing integration of smart thermostats and digital energy-management platforms.

Boilers remain the leading product category, contributing 28% of global revenue, due to their widespread use in industrial and district-heating systems.

The heating equipment market is expected to grow at a CAGR of 6.2% between 2025 and 2032, supported by technology advancements, electrification mandates, and ongoing infrastructure upgrades.

Major companies include Carrier Global Corporation, Trane Technologies, Daikin Industries, Johnson Controls, and Lennox International.