- Industrial Goods & Service

- Hammer Mill Market

Hammer Mill Market Size, Share, Growth, and Regional Forecast for 2025 - 2032

Hammer Mill Market by Product Type (Gravity Discharge, Pneumatic Discharge, Full Circle Screen, Horizontal In-Feed, Lump Breakers, and Others), Capacity (Upto 100 kg/h, 100 to 500 kg/h, 500 to 1000 kg/h, 1,000 to 5,000 kg/h, 5,000 to 10,000 kg/h, and Above 10,000 kg/h), End Use Industry (Agriculture, Cosmetics, Food & Feed, Metals & Mining, Energy and Power, and Others), and Region for 2025 - 2032

Hammer Mill Market Share and Trend Analysis

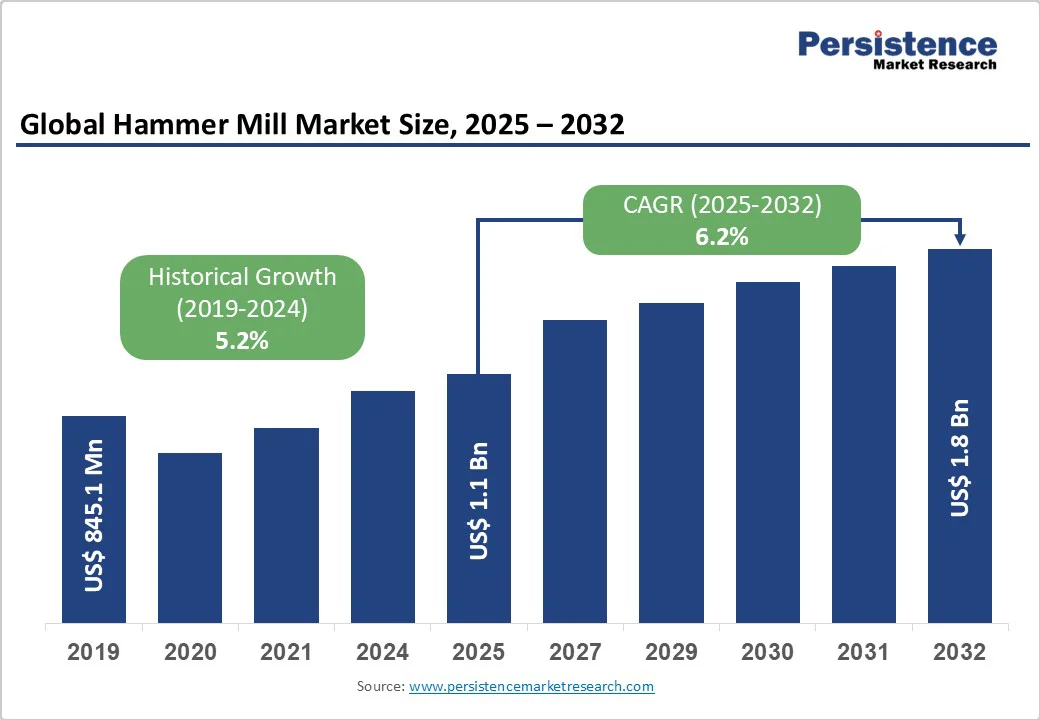

The global hammer mills market size is expected to be valued at US$1.1 billion in 2025 and is projected to reach US$1.8 billion by 2032, growing at a CAGR of 6.2% between 2025 and 2032.

The rising demand for size reduction equipment in the metals & mining sector, the expanding use in food and feed processing, and the increasing adoption of energy-efficient hammer mills in pharmaceutical and chemical manufacturing are all factors that encourage market growth.

Key Industry Highlights:

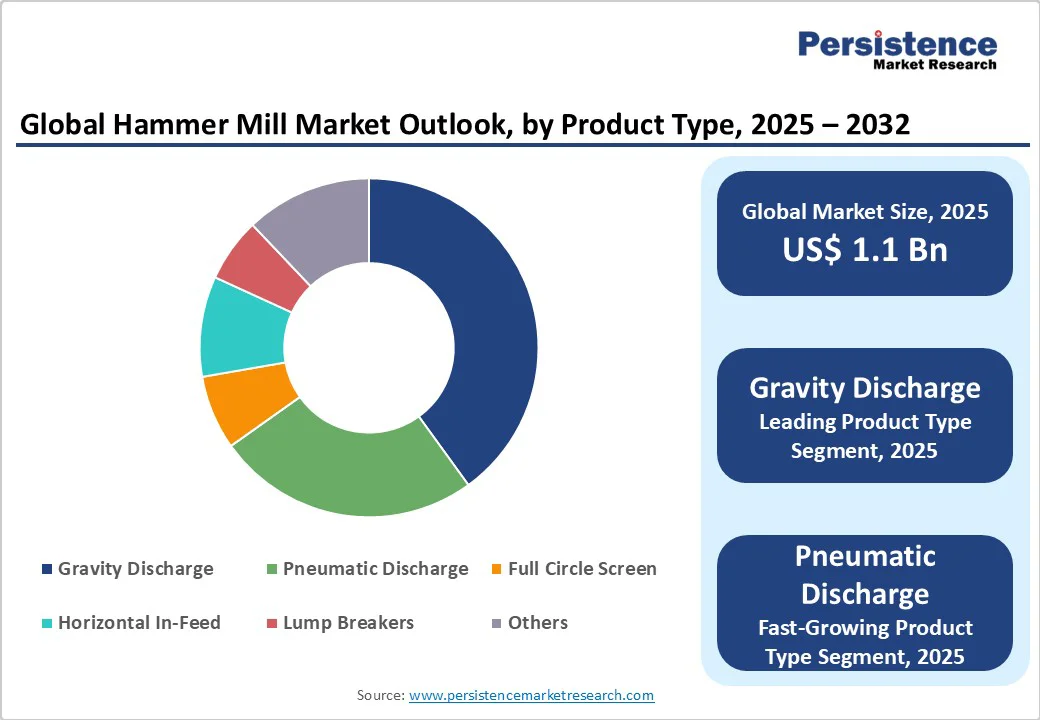

- Leading Product Type: Gravity discharge accounted for 32% of the product type in 2024, driven by its wide adoption in feed milling and grain processing for efficient size reduction.

- Leading Capacity: 1,000-5,000 kg/h capacity held a 29% share in 2024, due to increasing demand from mid-scale feed, biomass, and agro-processing industries that require flexible, medium-capacity hammer mills.

- Leading Industry: The Food & feed industry represented 37% of the end-use share in 2024, fueled by rising livestock feed demand, nutritional product processing, and reliable performance in grinding grains.

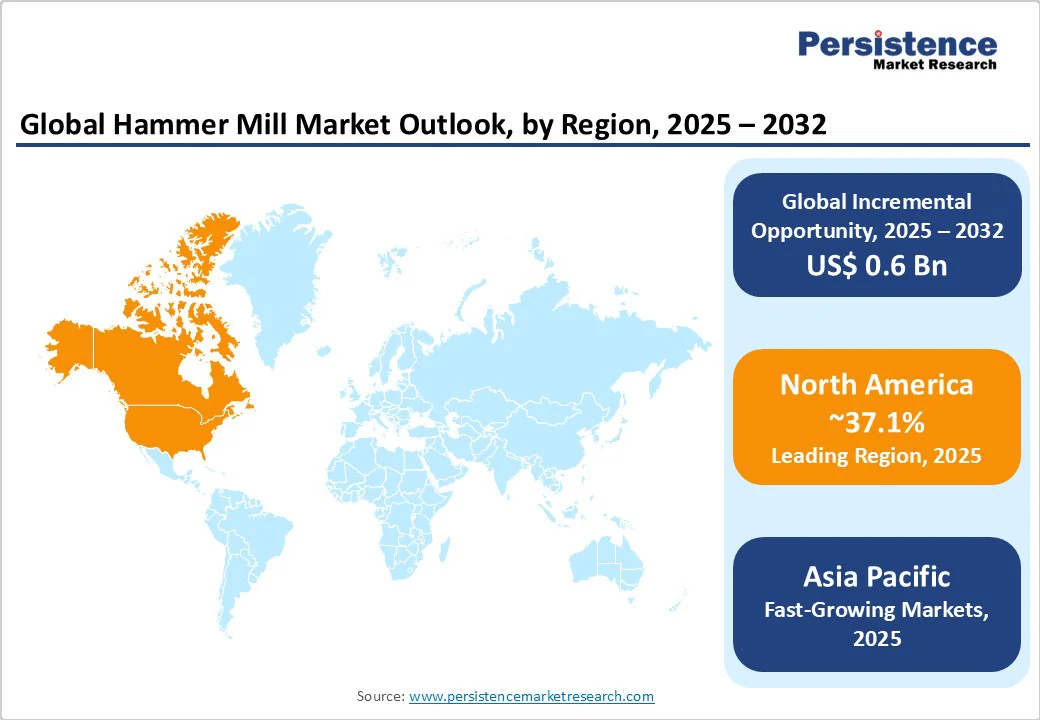

- Leading Region: North America captured 34% of the global hammer mills share in 2024, owing to advanced industrial infrastructure, feed production expansion, and adoption in biomass energy generation.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by expanding agriculture, aquaculture feed demand, and industrial processing in India, China, and Southeast Asia, boosting hammer mill adoption.

| Key Insights | Details |

|---|---|

| Hammer Mill Market Size (2025E) | US$1.1 Bn |

| Market Value Forecast (2032F) | US$1.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.2% |

Market Dynamics

Driver - Rising Industrial Automation and Smart Technology Integration

The global hammer mills industry is experiencing unprecedented transformation through IoT-enabled automation and predictive maintenance systems that are revolutionizing operational efficiency and productivity standards. Advanced manufacturers such as ANDRITZ and Bühler Group are implementing smart sensors, automated controls, and digital connectivity platforms that enable real-time performance monitoring, load optimization, and proactive maintenance scheduling. These technological innovations deliver energy savings of 10-30% while reducing operational downtime by up to 50% through predictive analytics and automated process adjustments.

Integrating machine learning algorithms and artificial intelligence enables hammer mills to autonomously optimize grinding parameters based on material characteristics and throughput requirements, resulting in improved particle size consistency and reduced processing costs. This automation revolution is particularly compelling for large-scale operations seeking to enhance competitiveness through reduced labor dependency and enhanced operational reliability.

Expanding Agricultural Mechanization and Feed Production Demand

The rise in global livestock population growth and increasing demand for processed animal feed creates substantial market opportunities for hammer mill manufacturers. The Food and Agriculture Organization (FAO) projects global feed production to exceed 1.2 billion metric tons by 2030, driving significant investments in efficient grain processing equipment. Hammer mills are essential for processing grains, seeds, and agricultural residues into uniform feed particles, with the agricultural sector representing approximately 30-35% of global market demand.

The trend toward precision feeding and nutritional optimization is further amplifying demand for high-capacity hammer mills capable of producing consistent particle sizes that enhance livestock digestibility and growth rates. Additionally, the mechanization of agricultural operations in emerging economies, particularly in the Asia-Pacific and Latin America, is creating new market segments for mid-capacity hammer mill systems.

Restraint - High Initial Capital Investment and Financing Constraints

Substantial upfront costs associated with advanced hammer mill systems present significant barriers to adoption, particularly for small and medium-sized enterprises operating with limited capital resources. The initial investment for high-capacity or technologically advanced hammer mills, including installation, infrastructure modifications, and operational training, can range from US$50,000 to US$500,000, depending on capacity and specifications. Maintenance costs alone can account for approximately 15-20% of total operating budgets, creating additional financial considerations that deter smaller operations from modernizing their equipment.

Access to financing remains particularly challenging in emerging markets, where 85% of SMEs suffer from credit constraints, limiting their ability to invest in modern processing equipment despite potential long-term benefits. The payback period for advanced hammer mill systems typically ranges from 3-5 years, which may exceed the risk tolerance of smaller operators facing uncertain market conditions.

Opportunity - Asia-Pacific Industrialization and Infrastructure Development

The rapid industrialization across the Asia Pacific region, particularly in China, India, and Southeast Asian countries, presents substantial growth opportunities worth an estimated US$400-500 million in additional market value through 2032. These emerging markets are witnessing unprecedented construction activities, agricultural mechanization, and manufacturing expansion that create high demand for efficient material processing equipment.

China's dominance as a manufacturing hub and India's agricultural modernization initiatives are driving demand for both high-capacity and mid-scale hammer mill systems. The region benefits from competitive manufacturing costs, large domestic markets, and government support for industrial development and renewable energy initiatives, creating favorable conditions for the adoption of hammer mills. Strategic partnerships between international manufacturers and local distributors are enabling market penetration while reducing entry barriers and operational costs.

Circular Economy and Sustainable Manufacturing Applications

The growing emphasis on circular economy principles and waste-to-resource conversion is creating new market segments for specialized hammer mills in recycling, waste management, and sustainable manufacturing applications. These machines are increasingly used for processing scrap materials, electronic waste, food waste, and industrial by-products, supporting companies' sustainability initiatives and waste reduction goals.

The e-waste recycling market alone presents opportunities for specialized hammer mills worth $100-150 million annually as companies seek to recover precious metals and ensure data security through efficient size reduction. Government mandates for waste reduction and compliance with the circular economy are creating regulatory drivers that support investment in processing equipment capable of converting waste streams into valuable resources.

Category Wise Insights

By Product Type - Gravity Discharge Hammer Mills to Lead

Gravity discharge hammer mills are likely to command a 40% share in 2025, establishing their dominance through proven reliability, cost-effectiveness, and operational simplicity across diverse industrial applications. These systems utilize swinging hammers mounted on a high-speed rotating shaft, achieving particle size reduction through mechanical impact and particle-on-particle collisions, with materials discharged from the bottom under the force of gravity.

Their widespread adoption stems from lower maintenance requirements, reduced operational complexity, and excellent performance with hard, brittle materials, including ceramics, dry chemicals, glass, coal, and metals.

The segment benefits from established manufacturing processes and a proven track record in heavy-duty applications, making it the preferred choice for mining operations, industrial processing, and applications requiring consistent and reliable performance.

Cost advantages of 20-30% compared to pneumatic systems and simplified installation requirements further strengthen their market position, particularly among small and medium enterprises seeking robust processing solutions.

Pneumatic Discharge Hammer Mills

Pneumatic discharge hammer mills represent a rapidly growing segment, offering 300-400% higher production rates compared to gravity discharge systems when processing lightweight, fibrous materials such as biomass, paper, wood chips, and green wood.

These air-swept systems utilize fan-assisted material evacuation, creating controlled airflow that pulls processed materials through screens and transports them to collection or subsequent processing stages. Their superior performance with low-density materials stems from the ability to overcome rotor airflow resistance and efficiently handle materials with slightly higher moisture content than traditional gravity systems.

Enhanced dust containment and controlled material flow make pneumatic systems particularly valuable in food processing, pharmaceutical, and biomass applications where product quality and workplace safety are paramount. The segment's growth is driven by increasing demand for efficient biomass processing and expanding applications in renewable energy sectors.

By Capacity - 100 to 500 kg/h Capacity Range

The 100 to 500 kg/h capacity segment dominates with a 35% share in 2024, representing the optimal balance between production efficiency, operational flexibility, and capital investment for diverse industrial applications. This capacity range serves as the sweet spot for small to medium-sized enterprises across the agriculture, food processing, pharmaceutical, and chemical industries, seeking to mechanize their operations without incurring excessive capital expenditure.

The popularity of the segment is driven by its versatility in handling various materials, cost-effectiveness, and suitability for both batch and continuous processing applications. Market demand is particularly strong in emerging economies where companies are transitioning from manual to mechanized processing, with this capacity range offering scalable solutions that can accommodate business growth. Energy efficiency improvements of 15-20% in modern mid-capacity systems and reduced space requirements make them attractive for facilities with limited floor space and moderate production volumes.

By End Use Industry - Metals & Mining Dominate

The metals and mining sector is expected to maintain a 32.1% share in 2025, utilizing hammer mills for primary and secondary crushing applications, ore processing, and material size reduction in extractive operations. Hammer mills excel in processing abrasive materials, including limestone, gypsum, ores, and industrial minerals, offering excellent reduction ratios and handling capabilities for tough, resilient materials.

The segment benefits from robust demand for efficient crushing equipment in both surface and underground mining operations, with specialized designs featuring wear-resistant components and heavy-duty construction that can handle continuous, high-volume processing.

The growing emphasis on operational efficiency and energy conservation in mining operations is driving the adoption of advanced hammer mill systems. The optimized hammer designs and improved screen configurations reduce energy consumption per ton of processed material. Expanding mineral extraction activities in emerging markets and increasing demand for specialty minerals used in technology and renewable energy applications also contribute to the segment growth.

Agriculture and food & feed processing represent a critical growth segment with approximately 30% combined market share, driven by global population growth, livestock industry expansion, and increasing mechanization of agricultural processing operations. Hammer mills are essential for grain processing, animal feed production, and the management of agricultural residues, with applications that span corn grinding, wheat processing, and the conversion of agricultural by-products into valuable feed ingredients.

The segment benefits from growing demand for processed animal feed, with global feed production exceeding 1.2 billion metric tons annually and projected continued growth supporting the nutrition requirements of livestock. Precision feeding trends and nutritional optimization are driving demand for consistent particle size reduction that enhances digestibility and feed conversion efficiency, creating premium market opportunities for advanced hammer mill systems.

Regional Insights and Trends

North America Hammer Mill Market Trends

North America maintains the market leadership with approximately 40% share, driven by the United States' advanced agricultural infrastructure, established mining operations, and sophisticated manufacturing ecosystem. The region benefits from a mature industrial base, technological innovation leadership, and strong adoption of automation technologies across key end-use sectors, including food processing, pharmaceuticals, and renewable energy.

The presence of major manufacturers such as Williams Patent Crusher, Schutte Hammermill, and Fitzpatrick Company, combined with world-class research facilities, supports continuous product development and technological advancement.

EPA regulations on emission control and dust management are driving demand for advanced hammer mill systems with integrated environmental compliance features, creating premium market segments. Investment in biofuel production facilities and waste-to-energy infrastructure is generating additional demand worth an estimated US$150-200 million annually, with projected growth supported by renewable energy mandates and infrastructure modernization initiatives.

The region's focus on operational efficiency and regulatory compliance positions it well for continued adoption of high-performance, automated hammer mill systems with advanced monitoring and control capabilities.

Europe Hammer Mill Market Trends

Europe demonstrates significant market potential with steady 2-3% annual growth, driven by stringent environmental regulations promoting efficient and sustainable processing technologies across member states. The region's emphasis on regulatory harmonization, emissions control, and circular economy principles creates strong demand for advanced hammer mill systems with enhanced environmental compliance features and energy efficiency ratings.

Key markets, including Germany (26% regional market share), the United Kingdom, France, and Spain, benefit from established manufacturing sectors, technological expertise, and robust investment in renewable energy projects.

The European market is characterized by demand for precision-engineered systems meeting strict quality standards and environmental regulations, with premium pricing for advanced automation and emission control features. Germany's leadership position is supported by a strong industrial base, renowned research institutions, and government initiatives promoting sustainable manufacturing and e-waste recycling.

The region's focus on innovation, sustainability standards, and circular economy compliance is driving investment in specialized hammer mill applications for waste processing and resource recovery, representing growth opportunities worth $80-100 million through 2032.

Asia Pacific Hammer Mill Market Trends

Asia Pacific is positioned for the highest regional growth rate at 6-8% CAGR, driven by rapid industrialization, urbanization, and expanding manufacturing sectors in China, India, and Southeast Asian countries. China represents the largest individual growth opportunity with its massive agricultural sector, expanding pharmaceutical industry, and significant infrastructure development projects, creating demand for high-capacity processing equipment. India's agricultural modernization and growing food processing industry, supported by government mechanization initiatives, create substantial opportunities for mid-capacity hammer mill adoption.

The region benefits from competitive manufacturing costs, large domestic markets, and government support for industrial development and renewable energy initiatives that create favorable investment conditions. Southeast Asian countries are witnessing increased construction activities and agricultural mechanization that drive demand for efficient material processing solutions. The region's manufacturing advantages and cost competitiveness are attracting international manufacturers to establish local production facilities and strategic partnerships, further accelerating market growth and technology transfer.

Competitive Landscape

The global hammer mills market is characterized by a mix of global players and regional manufacturers, creating a moderately fragmented competitive environment. Larger companies focus on advanced engineering, high-capacity machines, and integration with automation technologies, while smaller firms emphasize cost-efficient, versatile solutions catering to niche applications in feed, food, and local industries.

Competition is increasingly driven by innovation in wear-resistant materials, energy efficiency, and modular designs that allow customization. Sustainability goals, including reduced energy consumption and dust emissions, are shaping product development. Strategic moves such as capacity expansions, technology partnerships, and geographic diversification further define the evolving market landscape.

Key Industry Developments:

- In September 2025, A new Triplet Hammer Mill was launched, featuring a three-stage crushing structure (coarse, medium, fine) in a single unit. The design claims 50% higher production efficiency, 20% lower energy consumption, and reduced maintenance by eliminating multiple equipment transfers.

- In February 2025, Schutte’s recent communications emphasize delivering advanced hammer mills for recycling, particularly plastics, e-waste, and mixed materials, focusing on precision, versatility, and efficiency in waste processing.

- In December 2024, Tietjen introduced the FD 32 Pro hammer mill tailored for pet food/fish feed in December 2024. It includes an enlarged rotor diameter, reduced hammer-to-screen distance (less clogging), and faster maintenance access.

Companies Covered in Hammer Mill Market

- Schutte Hammermill, LLC

- Prater Industries, Inc.

- American Pulverizer Company

- Hosokawa Micron Powder Systems

- FEECO International, Inc.

- Stedman Machine Company

- Williams Patent Crusher & Pulverizer Co., Inc.

- Munson Machinery Company, Inc.

- Fitzpatrick Company

- ANDRITZ AG

- Van Aarsen International

- L.B. Bohle Maschinen und Verfahren GmbH

- SaintyCo

- Dinnissen Process Technology

- Fragola S.p.a.

Frequently Asked Questions

The global hammer mill market is projected to be valued at 1.1 bn in 2025.

Growth is driven by industrial automation and IoT integration, expanding agricultural feed demand, and renewable energy biomass processing.

The hammer mill market is poised to witness a CAGR of 6.2% between 2025 and 2032.

Opportunities lie in Asia-Pacific industrialization, circular economy recycling applications, and Industry 4.0 smart milling innovations.

Major players in the hammer mill market include Olam International, Naturex S.A., Symrise AG, Mercer Foods, LLC, BC Foods, Inc., Harmony House Foods, Inc, and others.