- Off-Road Equipment & Machinery

- Vibratory Hammer Market

Vibratory Hammer Market Size, Share, Trends, Regional Forecasts, 2026 - 2033

Vibratory Hammer Market Product Type (Hydraulic Vibratory Hammers, Diesel Vibratory Hammers, Electric Vibratory Hammers, Pneumatic Vibratory Hammers), Mounting Type (Crane-Mounted, Excavator-Mounted), Centrifugal Force (Up to 1,000 kN, 1,000-2,000 kN, 2,000-3,000 kN, 3,000-4,000 kN, Above 4,000 kN), End-Use Industry (Construction Companies, Marine / Offshore Contractors, Infrastructure Developers, Oil & Gas Sector, Rental Service Providers), and Regional Analysis from 2026 - 2033

Vibratory Hammer Market Share and Trends Analysis

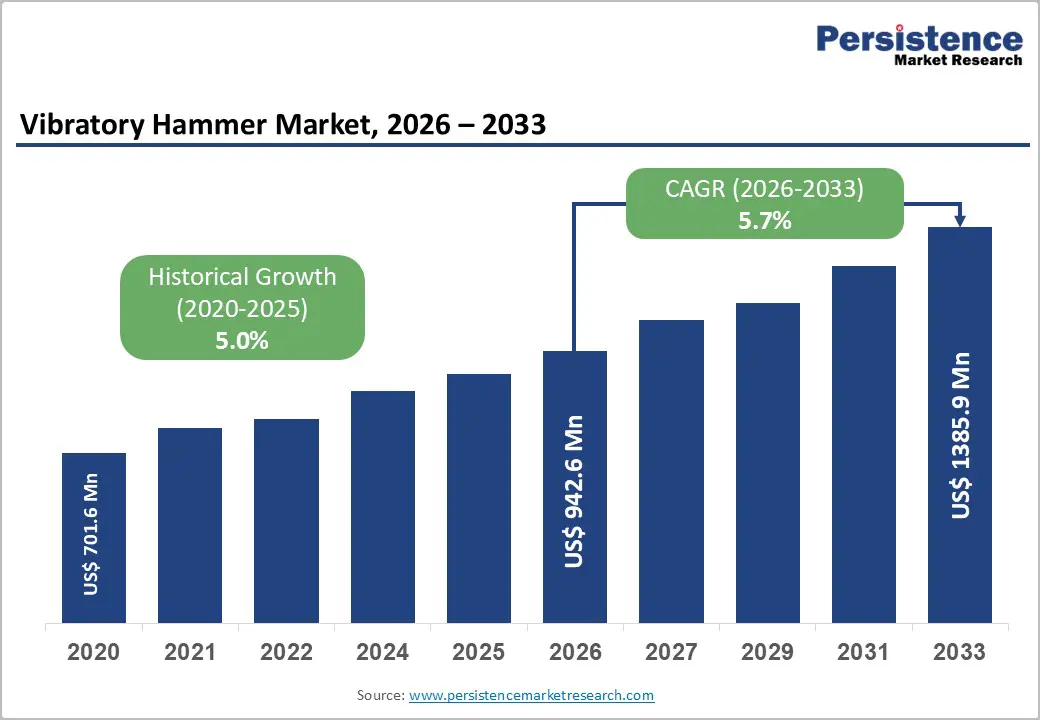

The global vibratory hammer market size anticipated at US$942.6 Million in 2026 and is projected to reach US$1,385.9 Million by 2033, growing at a CAGR of 5.7% between 2026 and 2033. Market expansion is driven by accelerating infrastructure investment globally projected to reach US$94 trillion by 2040, rapid urbanization with 68% of the world's population expected in urban areas by 2050, and renewable energy expansion, particularly offshore wind foundations requiring advanced piling solutions.

Technological advancements in vibratory hammer design, including automation, noise reduction, and variable moment systems, address regulatory compliance requirements while improving operational efficiency. The market's growth trajectory reflects the essential nature of foundation installation across construction, marine, and renewable energy sectors, establishing vibratory hammers as critical equipment for modern infrastructure development.

Key Industry Highlights:

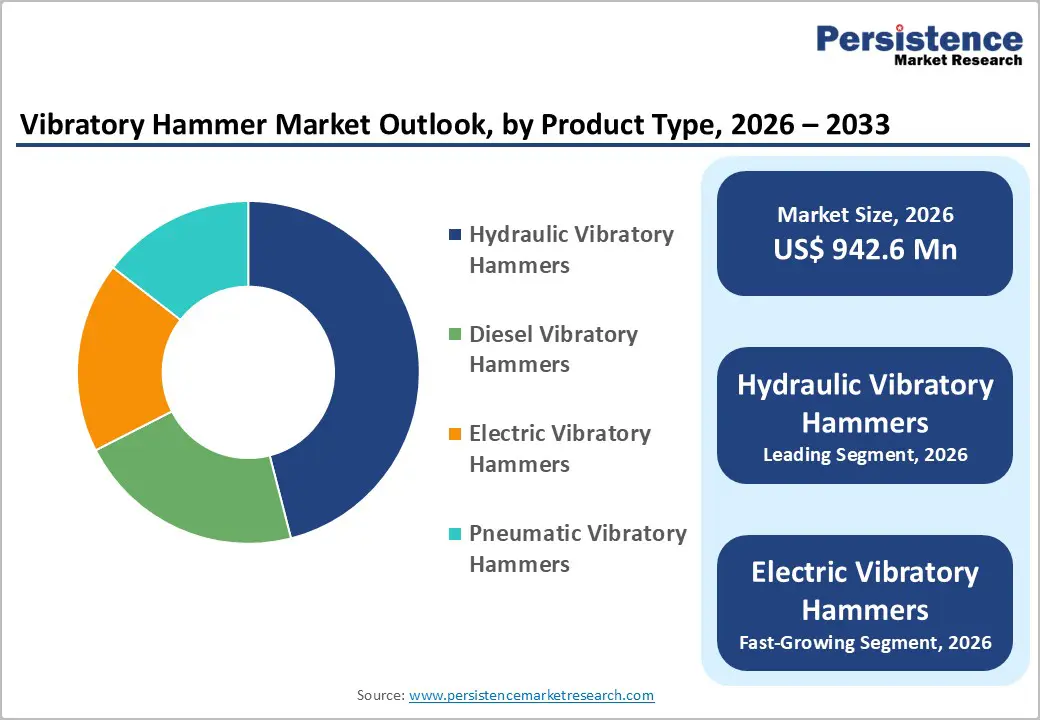

- Hydraulic Vibratory Dominance with Electric Growth: Hydraulic systems maintain 46% market share as established technology; electric vibratory hammers accelerate at 7.1% CAGR driven by sustainability mandates and 30-40% operational cost savings

- Crane-Mounted Leadership and Excavator Expansion: Crane-mounted systems command 58% market share; excavator-mounted equipment grows at 6% CAGR through rental service provider adoption enabling market accessibility

- High-Capacity Equipment Growth Driver: Above 4,000 kN centrifugal force segment expands fastest at 6.9% CAGR, directly correlating with offshore wind monopile installations and XXL-equipment development (Dieseko GIANT 2000)

- Rental Service Provider Acceleration: Equipment rental companies represent the fastest-growing end-use segment at 7.2% CAGR, democratizing access to advanced technology particularly in emerging markets with capital constraints

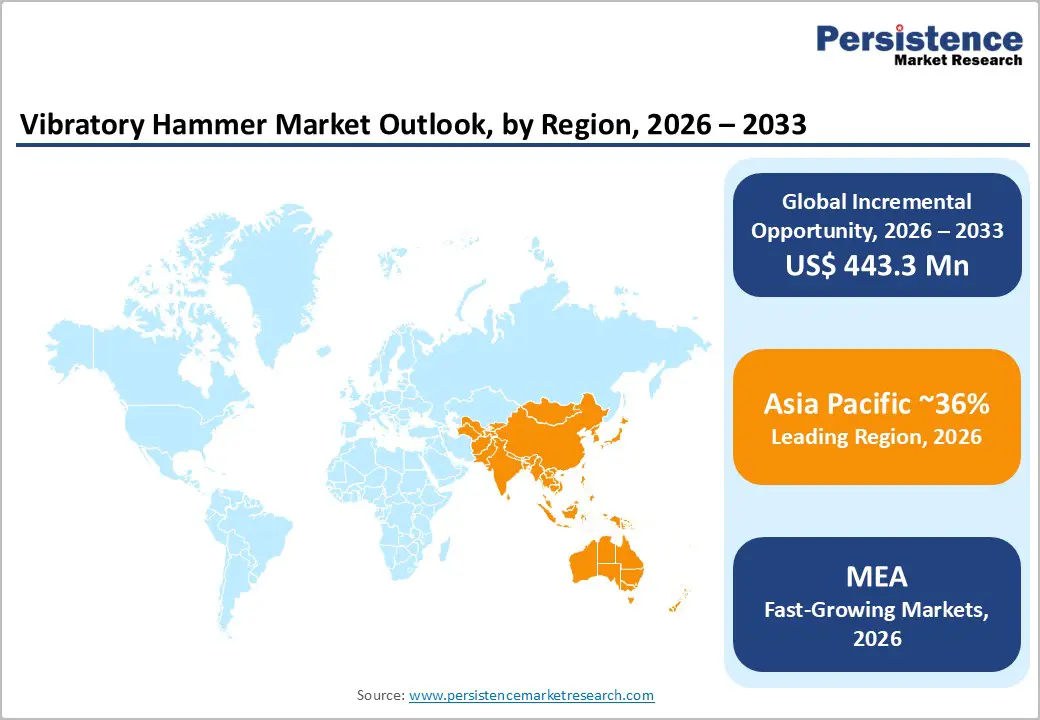

- Asia Pacific Market Dominance: Region commands ~36% global market share with India and China driving infrastructure investment (India's National Infrastructure Pipeline US$1.4 trillion, China's Belt and Road Initiative) and renewable energy expansion

- Offshore Wind Foundation Transformation: Renewable energy sector expansion, particularly offshore wind floating platforms, establishing foundation installation as a critical growth driver; strategic partnerships (VibroDrive+, Dieseko collaborations) validating market momentum

- MEA Infrastructure Expansion Momentum: The MEA is projected to experience the fastest growth, with a CAGR of 6.5%, fueled by mega transport and port infrastructure projects, oil & gas sector foundation works, and rising adoption of advanced vibratory hammers through rental services and government-led construction initiatives supporting regional industrialization and urbanization.

| Key Insights | Details |

|---|---|

|

Vibratory Hammer Market Size (2026E) |

US$ 942.6 million |

|

Market Value Forecast (2033F) |

US$ 1,385.9 million |

|

Projected Growth CAGR (2026-2033) |

5.7% |

|

Historical Market Growth (2020-2025) |

5.0% |

Market Dynamics Analysis

Drivers - Global Infrastructure Investment and Government Stimulus Programs

Governments worldwide are committing substantial capital to infrastructure development as strategic economic stimulus and long-term growth enablement. The International Monetary Fund projects global infrastructure investment could rise by 10% across multiple regions as countries prioritize resilient infrastructure development. Notable government initiatives include India's National Infrastructure Pipeline targeting US$1.4 trillion investment across transportation, energy, and urban development through 2040; China's Belt and Road Initiative driving infrastructure projects across Asia Pacific and beyond; and the United States' Bipartisan Infrastructure Law allocating US$110 billion specifically for transportation infrastructure, including bridges and highways requiring foundation work. The European Union's Green Infrastructure initiative promotes sustainable construction methodologies incorporating advanced equipment. These stimulus programs directly increase demand for vibratory hammers used in foundation installation, as infrastructure developers require efficient and reliable piling equipment to execute large-scale projects. Investment transparency and project pipeline visibility have created predictable demand patterns supporting manufacturer capacity planning and capital investment.

Renewable Energy Expansion and Offshore Wind Foundation Demand

The offshore wind energy sector represents the highest-growth driver for vibratory hammer demand, with floating offshore wind platforms demonstrating a prominent annual growth rate. Offshore wind installation requires specialized foundation solutions monopiles, jackets, and suction buckets installed at significant water depths, where vibratory technology provides distinct advantages over traditional impact hammering. Vibratory hammers enable 3-4 times faster pile installation compared to impact methods, reducing overall project duration and cost substantially. More critically, vibratory technology produces dramatically lower noise emissions critical for marine ecosystem protection; regulatory frameworks in Germany, Denmark, and other European waters mandate noise mitigation during foundation installation, directly incentivizing vibro technology adoption. Recent projects including RWE's Nordseecluster A (44 monopiles, 44-turbine capacity) and Empire Wind 1 (54 monopiles) demonstrate the accelerating deployment of vibratory solutions for major offshore projects. The International Energy Agency projects global offshore wind capacity could reach 380 gigawatts by 2040, establishing a substantial long-term demand foundation for specialized vibratory equipment.

Restraint - High Capital Equipment Costs and Cash Flow Constraints

Vibratory hammers represent significant capital investments for contractors and equipment rental companies, with specialized models exceeding around US$1-3 million in acquisition cost depending on centrifugal force capacity and offshore certification requirements. Equipment financing barriers disproportionately affect small and medium-sized construction contractors in developing markets, constraining market penetration despite significant project opportunity. Post-pandemic supply chain disruptions and inflation in critical input materials, particularly hydraulic components, specialized steel alloys, and electronic control systems, have elevated equipment costs 15-25% across the industry. Financing availability limitations in emerging markets restrict the expansion of rental service providers, who could otherwise democratize access to advanced equipment across geographies. This capital constraint particularly impacts India and Southeast Asian markets, where infrastructure investment opportunity remains substantial but financing infrastructure lags developed market availability.

Technological Transition Complexity and Skill Shortages

Despite superior performance advantages, the industry-wide transition from established impact hammer technology to vibratory methods faces organizational and skill-based inertia. Contractors experienced with impact hammer operations require retraining and operational procedure modification for vibratory equipment deployment, creating implementation friction. Specialized knowledge requirements for operating advanced variable-moment hammers, automated depth-control systems, and offshore-certified equipment create talent constraints in developing regions. Supply chain skills, manufacturing, precision engineering, certification audit compliance, and post-installation support concentrate disproportionately in developed markets. Regulatory certification requirements for offshore equipment (Lloyd's Register CLAME standards) create additional qualification barriers limiting equipment supplier base, particularly restricting competition and innovation diversity in specialized offshore segments.

Opportunity - Offshore Wind Acceleration and Floating Platform Foundation Requirements

Floating offshore wind represents the most significant near-term opportunity, expanding to deeper waters (100+ meters) where traditional fixed-bottom monopiles become economically unfeasible. Strategic partnerships, including Dieseko Group and CorPower Ocean's VibroDrive+ project (€400,000 Eureka funding), specifically target offshore anchor installation innovation, establishing technological convergence between wave energy and floating wind applications. India's 2024 offshore wind request for proposals targeting 4 gigawatts capacity represents a substantial future opportunity as projects progress from development to the construction phase. Global offshore wind acceleration, supported by falling turbine costs and renewable energy policies, projects 380 gigawatts operational capacity by 2040, creating an addressable market opportunity conservatively estimated around US$150-200 million incremental demand for specialized offshore vibratory equipment through 2033.

Electrification and Sustainability-Driven Equipment Evolution

Electric vibratory hammer technology represents the fastest-growing product segment at 7.1% CAGR, driven by convergent sustainability mandates and operational cost advantages. Electric systems reduce fuel consumption 30-40% compared to hydraulic equipment, while eliminating emissions in sensitive environments critical requirements for coastal and urban projects. EU environmental regulations and net-zero commitments accelerate equipment modernization timelines, establishing market opportunity for manufacturers offering electrified platforms. Bauma 2025 the global construction equipment showcase, highlighted Dieseko Group's zero-emission foundation equipment development as strategic priority, signaling the manufacturing sector’s commitment to electrification. Conservative estimates suggest electric vibratory hammers could capture 20-25% of new equipment sales by 2033, representing addressable market opportunity of US$80-120 million as cost premiums diminish through scale.

Category-wise Analysis

Product Type Insights

Hydraulic vibratory hammers command 46% of the global market, reflecting dominance driven by superior power density, proven reliability across diverse soil conditions, and seamless compatibility with existing crane infrastructure. Hydraulic systems deliver consistent force under variable operating conditions, essential for heterogeneous marine soils. Leadership is reinforced by over 50 years of operational history and Dieseko Group’s modular PVE and ICE platforms, spanning 345-5,374 kN, creating high switching costs and sustained customer confidence across global infrastructure and offshore construction markets worldwide.

Electric vibratory hammers are the fastest-growing segment at 7.1% CAGR, supported by sustainability mandates, 30-40% lower operating costs, and zero direct emissions. Grid-powered operation improves utilization in ports and offshore vessels, though cable routing, voltage compatibility, and limited remote-site power availability constrain broader adoption across developing and infrastructure-light construction regions.

Mounting Type Insights

Crane-mounted systems dominate with 58% market share, reflecting cost-effectiveness through equipment integration with existing crane assets already present at major construction sites. Crane mounting provides flexibility across diverse installation heights and pile depths, accommodating variable project requirements. Market dominance reinforces through network effects: contractors with crane assets naturally gravitate toward hammer solutions integrating seamlessly with existing equipment, reducing capital requirements and training needs.

Excavator-mounted systems expand at 6% CAGR, driven by rental service provider adoption enabling equipment mobility and simplified logistics. Excavator integration reduces installation complexity at remote sites lacking specialized crane infrastructure, expanding addressable market into smaller regional contractors and tier-2/3 cities in emerging markets. Dieseko's comprehensive excavator-mounted series (ICE B & PVE A standard, ICE RFB & PVE VMA resonance-free variants, ICE SH & PVE SH swivel-head designs, ICE SG & PVE SG side-gripper configurations) demonstrates product evolution matching diverse contractor requirements.

Centrifugal Force Insights

The 1,000-2,000 kN centrifugal force range commands 26% market share, representing optimal balance between pile installation capability and equipment portability for typical onshore construction projects. This category encompasses the highest-volume product family, supporting infrastructure projects including bridge foundations, building basements, and highway underpasses requiring penetration depths of 15-35 meters through variable soil conditions.

Equipment exceeding 4,000 kN centrifugal force expands at 6.9% CAGR, driven by offshore wind monopile installation requirements where XXL-capacity equipment enables rapid deep penetration at 50+ meter water depths. Dieseko's GIANT 2000 upending vibratory hammer with 5,374+ kN capacity represents technological culmination, specifically engineered for next-generation offshore wind foundation installations with monopiles exceeding 1,500 tonnes weight. High-capacity segment growth directly correlates with offshore project acceleration and turbine scale-up trajectory toward 15-20 megawatt unit capacities by 2030.

End-Use Industry Insights

Construction companies maintain 40% market share as primary end users, encompassing general contractors, specialized foundation companies, and infrastructure developers executing residential, commercial, and civil infrastructure projects. Market dominance reflects fundamental necessity of foundation installation across all construction categories, establishing consistent baseline demand independent of economic cycles.

Equipment rental companies expand at 7.2% CAGR, reflecting structural shift toward equipment outsourcing particularly in emerging markets where capital constraints favor operational expenditure over capital investment. Rental service expansion democratizes access to advanced vibratory technology across smaller contractors, expanding total addressable market geographically. This segment demonstrates highest elasticity to infrastructure investment stimulus, capturing disproportionate growth from government-funded projects where contractors prioritize capital preservation.

Regional Insights

North America Vibratory Hammer Market Trends

North America commands approximately 24% of the global vibratory hammer market, reflecting a mature, capital-intensive landscape with technologically sophisticated contractors. The U.S., representing roughly 70% of the region, benefits from the Bipartisan Infrastructure Law’s US$110 billion allocation for transportation modernization, driving demand for foundation equipment in bridge reconstruction, elevated transit, and seismic retrofits. Market growth of around 5.2% is supported by steady infrastructure maintenance cycles and offshore wind development in the Atlantic and Gulf. Advanced operational capabilities, including GPS-integrated automated depth control, combined with OSHA safety standards and EPA emissions regulations, drive innovation in noise reduction, safety automation, and electrified powertrains. Regional equipment distribution and dealer networks ensure robust aftermarket support and high utilization rates across construction and renewable energy projects.

Europe Vibratory Hammer Market Trends

Europe is projected to achieve a 5.4% CAGR in the forecast period fueled by significant infrastructure investment in renewable energy and transportation. Germany, the UK, France, and Spain account for roughly 65% of the regional market, with Germany leading in per-capita equipment intensity due to ambitious offshore wind targets exceeding 30 GW by 2030 and stringent environmental regulations promoting vibro technology. European contractors prioritize high-value equipment with superior noise and vibration control. EU marine mammal protection standards, sustainable construction mandates, and Green Infrastructure initiatives incentivize adoption of energy-efficient, low-emission vibratory hammers. CE certification ensures quality compliance, while projects such as RWE Kaskasi and Nordseecluster demonstrate industrial-scale vibro-driven monopile installations as effective noise-mitigation strategies, reinforcing Europe’s advanced technical adoption landscape.

Asia Pacific Vibratory Hammer Market Trends

Asia Pacific dominates the global vibratory hammer market with approximately 36% share, driven by China’s Belt and Road Initiative, India’s National Infrastructure Pipeline and Bharatmala projects, and rapid Southeast Asian urbanization. China contributes 15-18% of global demand through coastal city construction, transportation modernization, and floating offshore wind targets of 18 GW by 2035, while India’s infrastructure investment of US$1.4 trillion through 2040 expands foundation equipment demand into tier-2/3 cities. The region accounts for 60-65% of global manufacturing capacity, leveraging labor efficiency and vertical integration for cost leadership. Key players like SANY Heavy Industry, combined with rental service growth and government programs such as “Make in India” and “Made in China 2025,” drive domestic production, technology development, and broader market accessibility.

Competitive Landscape

Market leaders adopt differentiated strategies: Dieseko focuses on technology innovation, offshore certification, and modular platforms for emerging applications, while Liebherr, Soilmec, and Bauer leverage broad portfolios offering integrated foundation solutions. Asian cost-competitive suppliers expand via rental partnerships and tiered offerings. Emerging trends include rental dominance, technological bundling with automation and monitoring, and sustainability adoption through electric/hybrid powertrains and noise-reduction solutions.

Strategic Developments:

- In November 2025, Dieseko Group and CorPower Ocean announced VibroDrive+ consortium research project with €400,000 Eureka funding, targeting offshore anchor installation optimization for floating wind and wave energy applications, establishing technological convergence innovation.

- In June 2025, Bauer Group unveiled next-generation electric piling rig eBG33, integrating emission-free drive technology and smart control systems with 405 kW asynchronous motor, delivering 50% noise reduction and zero CO2 emissions for urban infrastructure.

- In March 2025, Junttan unveiled the Evolution DR5 drilling rig, HHx160 impact hammer and VH30VM vibratory hammer product ranges at Bauma 2025, expanding UK/Irish rental market presence with advanced variable moment technology solutions for urban construction projects.

Companies Covered in Vibratory Hammer Market

- Dieseko Group B.V.

- Liebherr-Werk Nenzing GmbH

- Junttan Oy

- Bauer AG

- Soilmec SpA

- Casagrande SpA

- SANY Heavy Industry Co Ltd

- Xuzhou Construction Machinery Group

- IHC Fundex Equipment

- BRUCE Piling Equipment Co Ltd

- Mait S.p.A.

- Comacchio SpA

- Enteco S.r.l

- Van Oord

- CorPower Ocean

Frequently Asked Questions

The global vibratory hammer market was valued at US$701.6 Million in 2020, reached US$942.6 Million in 2026, and is projected to reach US$1,385.9 Million by 2033.

Market growth is fueled by government-led infrastructure programs, offshore wind foundation demand, rapid Asia Pacific urbanization, automation and noise-reduction technologies, superior installation efficiency, and rising rental-based equipment adoption.

The Vibratory Hammer Market is projected to grow at a CAGR of 5.7% between 2026 and 2033.

Major opportunities lie in floating offshore wind foundations, Asia Pacific infrastructure megaprojects, electric and hybrid vibratory hammers, rental penetration in emerging markets, and high-capacity systems for next-generation monopiles.

The market is led by Dieseko Group, alongside Liebherr, Junttan, Bauer, Soilmec, Casagrande, SANY, XCMG, IHC Fundex, BRUCE Piling Equipment, and other specialized European and Asian manufacturers.