- Hardware & Software IT Services

- Golf Simulator Market

Golf Simulator Market Size, Share, and Growth Forecast, 2025 - 2032

Golf Simulator Market By Simulator Type (Full Swing Simulators, Single Screen Simulators), Application (Commercial Use, Residential Use), Component, and Regional Analysis for 2025 - 2032

Golf Simulator Market Size and Trends Analysis

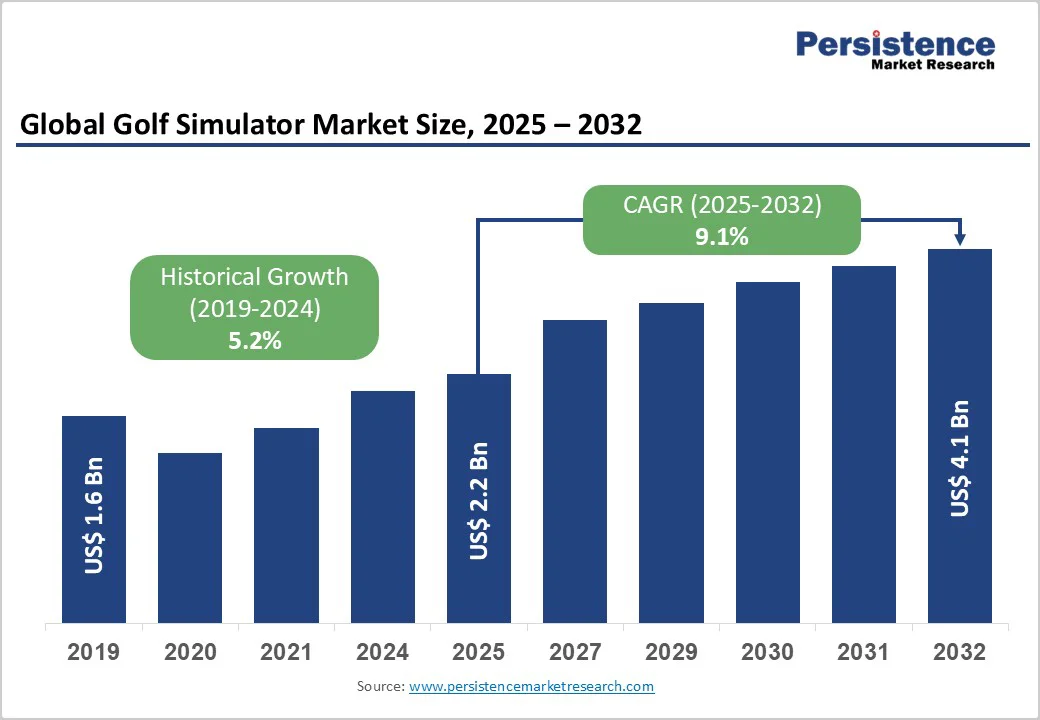

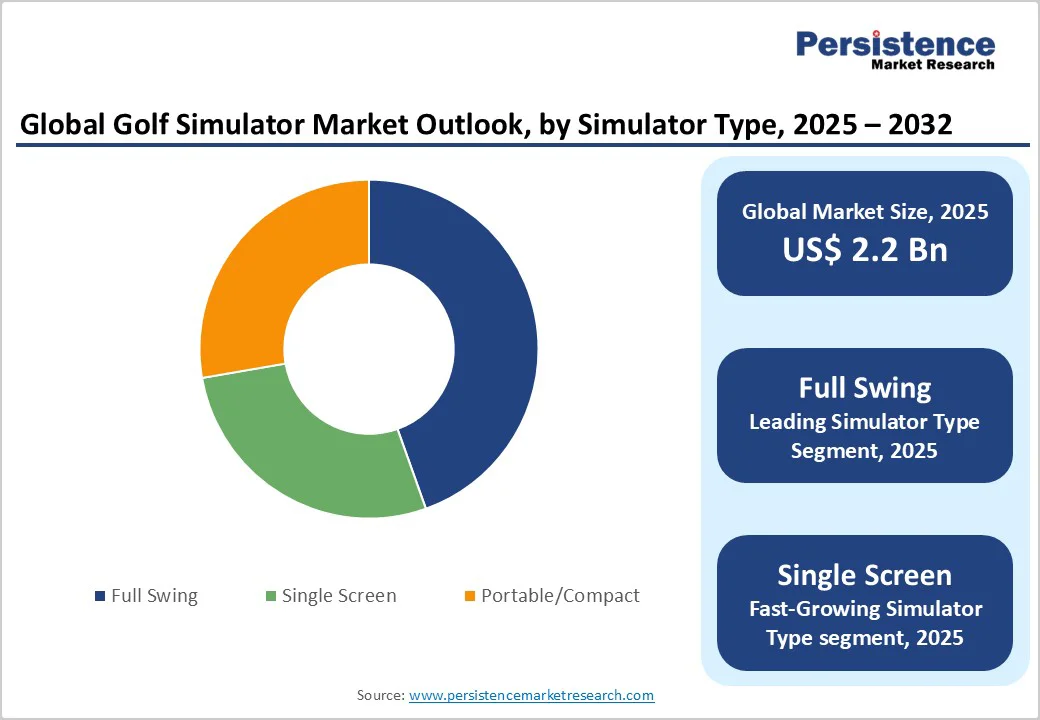

The global golf simulator market size is likely to be valued at US$2.2 Billion in 2025 and is expected to reach US$4.1 Billion by 2032, growing at a CAGR of 9.1% during the forecast period from 2025 to 2032, driven by the rising demand for realistic indoor golf experiences, coupled with increasing urban participation in the sport.

Advancements in sensors, launch monitors, and AI analytics are turning golf simulation into a data-driven training tool. Its expanding use in commercial venues and high-end homes marks a shift from niche entertainment to mainstream sports infrastructure.

Key Industry Highlights

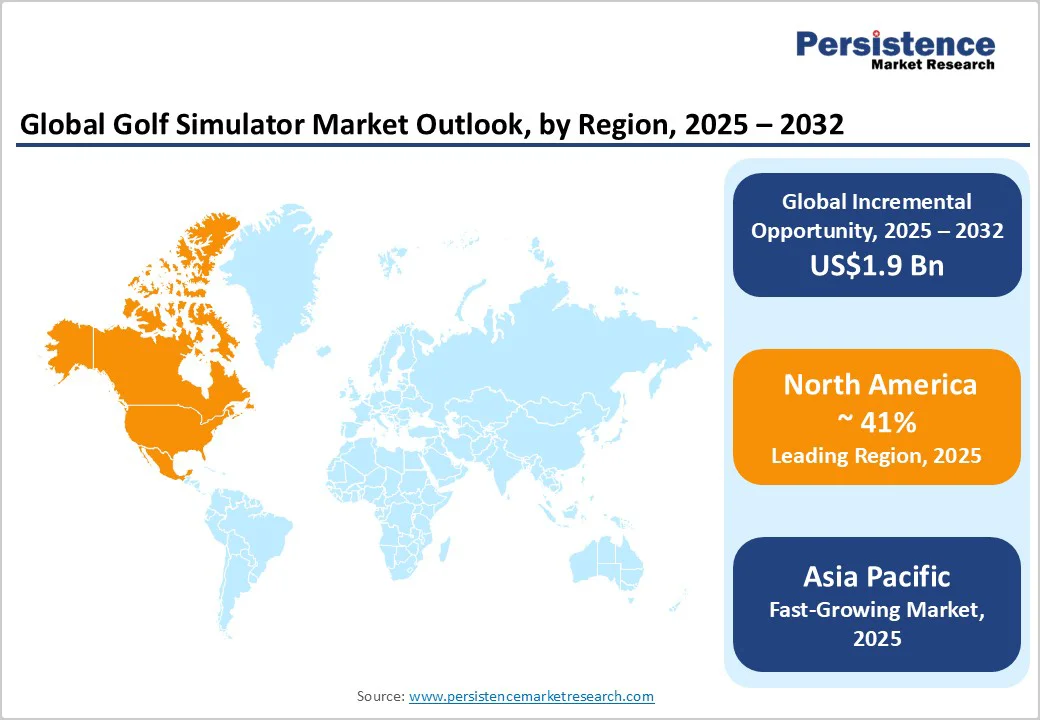

- Leading Region: North America accounted for over 41% of global revenue in 2025, driven by strong consumer demand, widespread commercial simulator installations, and technological innovation in the U.S.

- Fastest-Growing Region: Asia Pacific, fueled by rising urban incomes, expanding “screen golf” culture in South Korea, and the growing presence of premium indoor golf facilities across China, Japan, and India.

- Investment Plans: Post-2023, major players such as Golfzon, TrackMan, and TruGolf have expanded investments in AI-enabled systems, regional manufacturing (Vietnam), and software ecosystems, indicating strong capital flow toward product innovation and cloud-based service models.

- Dominant Simulator Type: Full swing simulators held a 44.7% market share in 2025, supported by professional training adoption and high-end commercial use across golf academies and luxury resorts.

- Leading Application: Commercial use captured over 59.8% of the total revenue in 2025, underpinned by the rapid growth of indoor golf lounges, sports bars, and entertainment chains offering multiplayer and analytics-driven experiences.

| Key Insights | Details |

|---|---|

| Golf Simulator Market Size (2025E) | US$2.2 Bn |

| Market Value Forecast (2032F) | US$4.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 9.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Popularity of Indoor Golf Facilities

The surge in indoor sports participation, particularly in regions with limited outdoor playing seasons, has driven the installation of golf simulators across urban centers. According to the National Golf Foundation (NGF), indoor simulator participation grew by over 30% between 2021 and 2024, driven by the convenience and year-round playability of the technology.

Facilities integrating social experiences, such as bars and entertainment venues, have seen revenue per square foot increase by 25-35% compared to traditional ranges. This growing consumer shift toward accessible golf experiences is significantly expanding commercial adoption and overall market penetration.

Technological Advancements in Tracking and Immersive Interfaces

Rapid innovation in optical sensors, radar-based tracking, and 3D rendering has revolutionized golf simulators’ accuracy and realism. Leading systems now integrate dual-camera photometric technology and AI swing analytics, achieving over 98% shot accuracy.

The integration of VR headsets and cloud-based analytics enhances player immersion and remote data synchronization. Industry leaders such as Foresight Sports and TrackMan have reported double-digit revenue growth since 2022, owing to the incorporation of precision sensors and software-as-a-service (SaaS) models. This convergence of simulation and digital coaching is driving premium product adoption globally.

Expansion of Golf Tourism and Virtual Tournaments

The post-pandemic rise in virtual competitions and digital golf leagues has strengthened engagement across the golfing community. The Professional Golfers’ Association (PGA) reported a 45% increase in simulator-based tournaments between 2022 and 2024, particularly among younger demographics and corporate teams.

These virtual formats enable global participation and consistent player engagement, supporting hardware and subscription growth. Golf resorts and training academies are increasingly deploying simulators as part of hybrid experiences, combining virtual play with outdoor practice, broadening both the revenue base and use-case spectrum.

Barrier Analysis - High Installation and Maintenance Costs

Comprehensive golf simulator systems require significant upfront investment, typically ranging from US$25,000 to US$70,000 for commercial-grade installations. High-end units involve advanced sensors, projector systems, and software licensing, inflating both setup and operational costs.

Smaller facilities and individual consumers often face affordability barriers, limiting overall adoption in price-sensitive regions. Maintenance requirements, including recalibration and software updates, further raise the total cost of ownership, constraining market scalability among mid-tier customers.

Space and Infrastructure Limitations

The physical space requirements, a minimum of 10 x 15 feet, and structural modifications needed for optimal simulator setup hinder residential penetration. Urban dwellings often lack adequate ceiling height or acoustics for professional installations.

Moreover, the need for controlled lighting and ventilation adds to customization complexity. These infrastructural limitations restrict broader market accessibility, particularly in dense metropolitan regions across Asia and Europe.

Opportunity Analysis - Integration of AI-Driven Performance Analytics

The convergence of artificial intelligence (AI) and biomechanics in golf simulation offers a significant growth opportunity. AI-enabled systems analyze swing mechanics, club trajectory, and body posture to generate personalized coaching insights.

The market for AI-integrated sports analytics is projected to exceed US$9 Billion by 2030, of which golf applications represent a rapidly growing niche. Embedding AI modules into simulators enhances training outcomes and creates subscription-based revenue models, improving vendor profitability.

Expansion into Emerging Asian Markets

Asia Pacific represents one of the fastest-growing regions for golf simulators, with increasing participation among middle-income groups in China, India, and South Korea. Rapid urbanization and the rise of premium entertainment spaces are driving installations in commercial settings.

The potential addressable market across Asia is expected to surpass US$1.2 Billion by 2032, fueled by domestic manufacturing capacity and localized pricing strategies. This geographic expansion presents a substantial opportunity for international vendors to establish regional production and distribution partnerships.

Development of Portable and Compact Simulator Solutions

Innovation in lightweight, modular simulator systems designed for home and office use is opening new customer segments. Compact projectors, foldable nets, and mobile tracking devices enable setup within confined spaces at a fraction of the traditional cost.

Entry-level systems priced below US$5,000 are gaining traction among amateur players and home users. The miniaturization trend aligns with the broader consumer electronics movement toward mobility and affordability, unlocking latent residential demand.

Category-wise Analysis

Simulator Type Insights

Full swing simulators dominate the global market with a share exceeding 44.7% in 2025, supported by high adoption across commercial facilities, golf clubs, and training centers. These systems employ multi-sensor configurations, infrared tracking, and realistic turf surfaces that replicate course play with near-real-time feedback.

Premium brands such as TrackMan, Foresight Sports, and HD Golf continue to lead this segment with integrated analytics and multi-course licensing options. Their advanced calibration capabilities and professional endorsement make them the preferred choice for competitive players and instructors.

Single-screen simulators are projected to register the highest CAGR, driven by affordability and compact design. Their modular structure and plug-and-play functionality appeal to small businesses and residential buyers. Integration with mobile apps and wireless swing analyzers enhances accessibility.

As software-based updates improve graphics and ball-flight accuracy, this category is expected to expand its footprint in the consumer segment, especially in North America and East Asia.

Application Insights

Commercial installations accounted for over 59.8% of the global revenue in 2025, led by entertainment centers, sports bars, and training academies. These venues leverage golf simulators to attract non-traditional audiences and maximize floor utilization. Multi-sport functionality and multiplayer modes are particularly appealing in leisure complexes.

The business model’s recurring revenue from hourly rentals and corporate events provides long-term profitability. Countries such as the U.S. and South Korea exhibit a high density of simulator-based golf lounges, showcasing robust commercial adoption.

The residential segment is the fastest-growing segment, fueled by rising disposable incomes and the desire for at-home recreation. Compact simulator designs, subscription-based course libraries, and remote coaching features are attracting affluent households.

Manufacturers have started offering financing and modular installation services to make home systems more accessible. The integration of simulators within home gyms and entertainment rooms is also accelerating consumer-side adoption across developed economies.

Component Insights

Hardware components, including cameras, projectors, screens, sensors, and impact surfaces, represent nearly 70% of total market revenue. The need for precision hardware in achieving realistic simulation ensures continuous demand.

Manufacturers are emphasizing higher-resolution optics, durable screen materials, and multi-sensor fusion technologies. The hardware segment’s stability is underpinned by the periodic upgrade cycle and replacement demand from commercial operators.

Software and analytics services are the fastest growing segment, driven by recurring subscription models and remote updates. Continuous improvement in user interfaces and cloud integration enhances player engagement. Value-added services such as data analytics dashboards and professional coaching support create ongoing revenue streams. The software segment’s scalability and innovation potential are reshaping long-term market competitiveness.

Regional Insights

North America Golf Simulator Market Trends - Innovation-Driven Growth and Strong Consumer Adoption

North America remains the largest regional market, accounting for over 41% of global revenue in 2025, anchored by the robust consumer base and technological leadership in the U.S. The region’s mature golf culture, high per-capita income, and widespread commercial simulator facilities drive sustained demand.

According to the National Golf Foundation, more than 6 million U.S. players engage with golf simulators annually, underscoring the sector’s mainstream acceptance.

Key growth drivers include the expansion of entertainment chains such as Topgolf Swing Suite and the integration of simulators in luxury resorts. Regulatory clarity on indoor entertainment licensing and strong data-protection standards enhance investor confidence.

The U.S. market benefits from a vibrant innovation ecosystem, particularly in sensor design, motion capture, and software integration, supported by high R&D expenditure. Canada’s market is also growing steadily due to increasing adoption in sports training institutes and residential installations. Venture capital inflows into golf-tech startups further reinforce the region’s technological dominance.

Europe Golf Simulator Market Trends - Digital Integration and Sustainable Manufacturing

Europe’s golf simulator market is led by Germany, the U.K., France, and Spain, constituting over 70% of regional demand, supported by strong club membership bases and golf tourism. European consumers show increasing preference for indoor training environments due to weather variability and limited outdoor availability.

The U.K. leads regional adoption, with premium indoor golf lounges expanding across London, Manchester, and Edinburgh. Germany’s manufacturing expertise supports localized production of simulation hardware, reducing import dependency.

The European Golf Association (EGA) has emphasized digital training integration, encouraging professional academies to include simulators in certification programs. Stringent energy-efficiency and data-security regulations influence system design, while sustainable material sourcing remains a key trend. Private equity investment and cross-border partnerships are promoting product standardization and wider market access.

Asia Pacific Golf Simulator Market Trends - Rapid Expansion and Tech-Enabled Urban Leisure

Asia Pacific is forecast to exhibit the fastest growth, driven by rising urban incomes and a growing interest in golf among younger demographics. China, Japan, and South Korea collectively account for nearly 60% of regional demand. China’s indoor golf facilities have expanded by over 20% annually since 2022, aided by government support for sports infrastructure modernization.

Japan’s mature technology base supports the integration of high-precision sensors and compact designs, catering to limited space conditions. South Korea remains a global leader in simulator density, with “screen golf” culture deeply embedded in urban recreation.

India and Southeast Asian countries are emerging as new growth frontiers, with premium residential communities and malls incorporating entertainment-based simulator zones. Manufacturing cost advantages, localized service networks, and rising e-commerce penetration further accelerate regional expansion.

Competitive Landscape

The global golf simulator market is moderately consolidated, with the top five companies controlling nearly 55% of total revenue. Leading participants, including Foresight Sports, TrackMan, TruGolf, and Golfzon, compete through technology differentiation and software ecosystems. Market concentration is higher in premium commercial applications, while residential segments remain fragmented, allowing smaller players to enter with cost-efficient solutions.

Market leaders emphasize innovation, digital ecosystem expansion, and cost-optimized regional manufacturing. Subscription-based models, modular product lines, and direct-to-consumer channels are emerging as key differentiators that enhance lifetime customer value and market resilience.

Key Industry Developments

- In March 2024, Foresight Sports launched the GCHawk, a ceiling-mounted photometric tracking system offering 360° ball-flight capture, expanding its professional and consumer reach.

- In June 2025, the indoor-golf venue operator Golf VX announced a new franchise location in North Dartmouth, Massachusetts (Boston region), marking its second U.S. franchise and underlining an expansion of premium multi-user simulator entertainment venues in the United States.

Companies Covered in Golf Simulator Market

- Foresight Sports

- TrackMan A/S

- Golfzon Co. Ltd.

- TruGolf Inc.

- HD Golf

- SkyTrak LLC

- OptiShot Golf

- Uneekor Inc.

- Full Swing Golf Inc.

- aboutGolf Ltd.

- Creative Golf 3D

- Visual Sports Systems

- GOLFZONDEMAND

- JoyGolf Smart Sim

- ProTee United B.V.

- Sports Coach Systems Ltd.

- Ernest Sports

- GSA Golf

- Garmin Ltd.

- OKONGOLF

Frequently Asked Questions

The golf simulator market size is estimated at US$2.2 Billion in 2025.

The market is expected to reach US$4.1 Billion by 2032.

The market is projected to grow at a CAGR of 9.1% from 2025 to 2032.

Key trends include the integration of AI for swing analysis, expansion of indoor entertainment venues, rise of portable and compact simulator systems, and the emergence of cloud-based multiplayer platforms, enhancing engagement and training efficiency.

The commercial segment leads the golf simulator market, accounting for the largest revenue share in 2025 due to widespread installations in golf lounges, sports bars, and training academies offering immersive and social gameplay experiences.

Key players include Foresight Sports, TrackMan A/S, Golfzon Co. Ltd., TruGolf Inc., and Full Swing Golf Inc.