- Electric Mobility

- Golf Cart Market

Golf Cart Market Size, Share, and Growth Forecast 2026 - 2033

Golf Cart Market by Product Type (Electric, Gasoline), End-User (Golf Clubs [Hotels/Resorts, Housing Projects, Others (Private)], Airports, Railways, PSUs, Private Community, Others [Gov]), Seating Capacity (Small [2–4], Medium [6–8], Large [10+]), and Regional Analysis for 2026 - 2033

Golf Cart Market Size and Trend Analysis

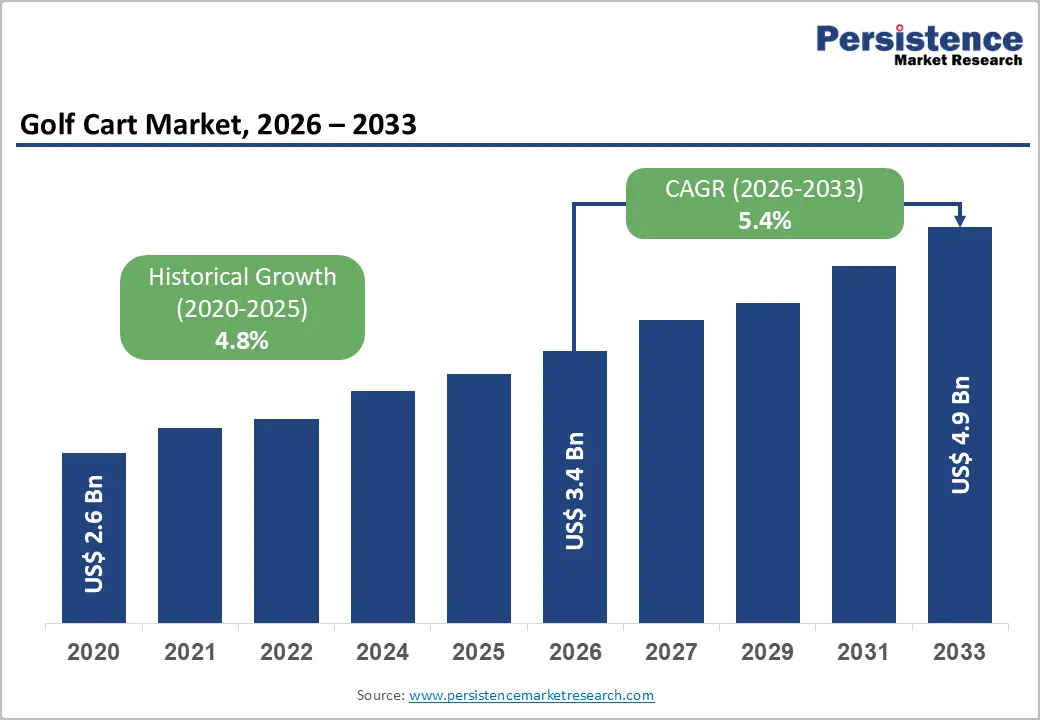

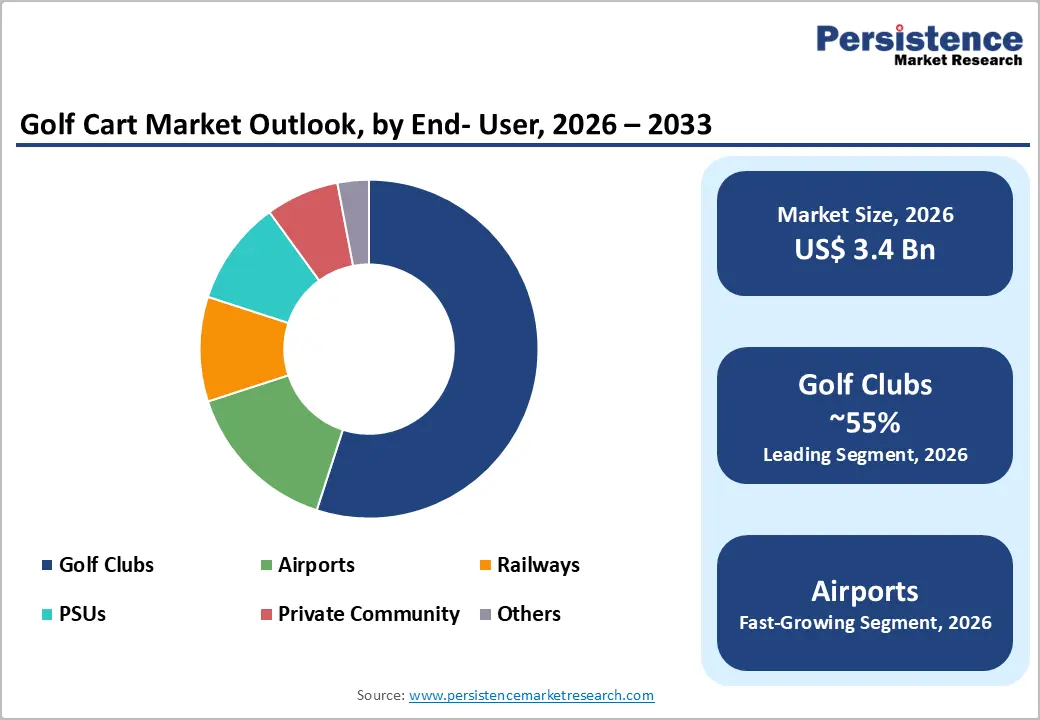

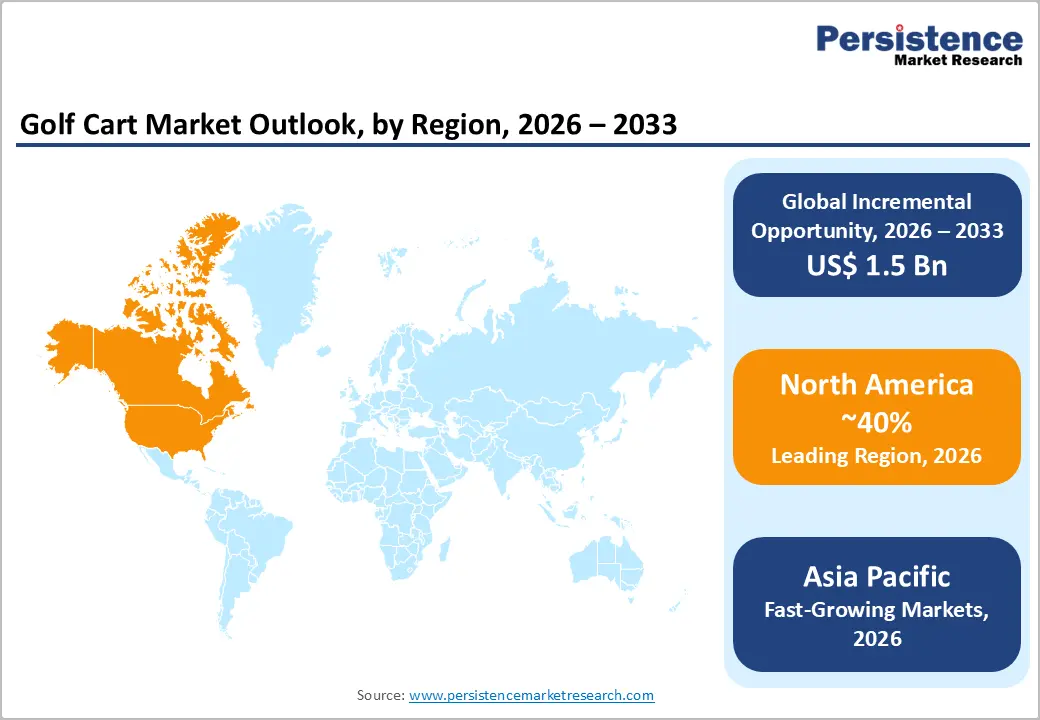

The global golf cart market size is valued at US$ 3.4 billion in 2026 and is projected to reach US$ 4.9 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

The market is being propelled by the rapid electrification of fleet vehicles across golf courses, hospitality venues, airports, and gated communities, driven by tightening emission norms and rising fuel costs. The global shift toward zero-emission intra-facility transport, combined with growing investments in smart city infrastructure and the expansion of golf tourism, particularly in North America, Europe, and the Asia Pacific, reinforces consistent demand.

Key Industry Highlights:

- Leading Region – North America dominates the global golf cart market, accounting for approximately 40% of revenue in 2025, driven by the U.S.'s dense golf facility network, strong electric fleet adoption, and large retirement community transport demand.

- Fastest Growing Region – Asia Pacific is projected to register the highest CAGR exceeding 7% through 2033, fueled by rapid golf infrastructure expansion in China and India, smart city deployments, and government EV incentive frameworks driving institutional fleet electrification.

- Dominant Product Segment – The electric product type accounts for approximately 72% market share, propelled by emission mandates, declining lithium battery costs, and total cost of ownership advantages over gasoline alternatives across golf, hospitality, and airport applications.

- Fastest Growing Segment – The Airports and Railways end-user segment is the fastest growing category, driven by global air traffic growth projected by IATA to exceed 8.2 billion passengers by 2037, necessitating scalable, sustainable intra-facility electric mobility solutions.

- Key Opportunity – Integration of LFP battery technology with IoT-enabled fleet management platforms presents a high-margin growth opportunity, enabling manufacturers to transition toward fleet-as-a-service models with recurring software and maintenance revenue streams.

DRO Analysis

Drivers - Accelerating Electrification and Sustainability Mandates Across End-Use Sectors

The global transition toward low-emission and zero-emission mobility solutions is a primary catalyst for the golf cart market. Governments across North America, Europe, and the Asia Pacific are implementing stringent regulations curbing internal combustion engine (ICE) usage within closed campuses, residential zones, and public facilities. In the United States, several state-level clean transportation incentive programs, including those under the Inflation Reduction Act (IRA), encourage the adoption of electric utility vehicles for commercial and institutional fleets.

The U.S. Department of Energy (DOE) has consistently promoted the electrification of short-range utility vehicles as part of the national net-zero target. As a result, golf courses, airports, and resorts are systematically replacing gasoline-powered carts with electric variants, driving both replacement demand and new fleet deployments at a compound pace above 6% annually in key developed markets.

Expanding Golf Tourism and Hospitality Infrastructure Investment

Global golf tourism has demonstrated robust recovery post-pandemic, with the World Golf Foundation reporting that golf participation in the U.S. reached approximately 41.1 million players in 2023, the highest recorded level in over two decades. This surge in participation has driven direct capital expenditure in golf course development and resort infrastructure globally.

The Asia Golf Industry Federation (AGIF) reports significant course expansion projects across Southeast Asia, South Korea, and India, each requiring full fleet replenishment. Simultaneously, luxury hotel chains and gated housing communities are adopting standardized electric golf carts as part of green hospitality commitments. UNWTO data confirms sustained growth in leisure tourism spending, ensuring long-term demand for intra-resort mobility solutions, including premium golf cart fleets.

Restraints - High Initial Capital Investment and Total Cost of Ownership

Despite long-term operational savings, the higher upfront cost of electric golf carts compared to gasoline variants remains a significant adoption barrier, particularly in price-sensitive markets. An electric golf cart can cost 30% more than an equivalent gasoline model due to battery pack expenses. Lithium-ion battery packs, which constitute nearly 40% of the total vehicle cost, are subject to raw material price volatility, especially for lithium, cobalt, and nickel.

For small-to-mid-sized golf clubs and municipal operators in developing economies, procurement budget constraints delay large-scale electrification. Additionally, inadequate charging infrastructure in rural or remote hospitality venues compounds ownership challenges.

Regulatory Complexity and Standardization Gaps in Emerging Markets

The absence of unified safety and operational standards for golf carts across emerging markets creates complexity for manufacturers seeking global scalability. Countries in Latin America, South Asia, and Africa lack comprehensive frameworks regulating low-speed electric vehicles (LSEVs) on private and semi-public premises.

This regulatory ambiguity discourages institutional buyers from committing to large-scale procurement, as compliance risks remain unclear. Furthermore, import tariff structures for electric drive-train components in several developing economies, including rates exceeding 15% in certain jurisdictions, elevate the landed cost of assembled carts, dampening market penetration outside established regions.

Opportunities - Rising Demand from Non-Golf Sectors: Airports, Railways, and Smart Campuses

One of the most significant market opportunities lies in non-golf end-use segments, particularly airports, railway stations, and large institutional campuses. Global air passenger traffic is projected by IATA to surpass 8.2 billion by 2037, requiring airports to scale intra-terminal mobility solutions, including electric carts for passenger assistance and baggage handling. The Airports Council International (ACI) has made sustainability a central pillar of its Airport Carbon Accreditation (ACA) program, compelling operators to transition to zero-emission ground vehicles.

Similarly, Indian Railways and several European transit hubs have already deployed electric golf carts for station-level passenger movement. These verticals represent structurally underserved demand pools with consistent government-backed procurement cycles, offering manufacturers stable, high-volume order opportunities independent of seasonal golf market fluctuations.

Technological Innovation: Lithium-Ion Battery Upgrades and Connectivity Features

Technological advancements in battery chemistry and vehicle connectivity are opening new avenues for premium product differentiation. The industry's transition from legacy lead-acid batteries to lithium iron phosphate (LFP) technology offers cart manufacturers the ability to position next-generation vehicles with longer range, reduced charge times, and a lifespan exceeding 2,000 charge cycles. According to the U.S. Advanced Battery Consortium, LFP battery cost per kWh has declined by over 85% in the last decade, improving affordability at scale.

Furthermore, integration of GPS fleet management, IoT-enabled diagnostics, and geofencing features is increasingly demanded by large fleet operators, including airport authorities and resort chains. Companies offering connected cart ecosystems can command significant price premiums while entering recurring software subscription revenue models, substantially improving long-term revenue per unit sold.

Category-wise Analysis

Product Type Insights

The electric segment is the leading product type in the golf cart market, accounting for approximately 72% of total market share. This dominance is underpinned by a structural shift in fleet procurement preferences driven by environmental regulation, declining battery costs, and total cost of ownership advantages over a 5–7-year lifecycle. The Club Car, E-Z-GO, and Yamaha Golf-Car Company, three of the most established manufacturers, now derive most of their volume from electric variants.

The Electric Drive Transportation Association (EDTA) confirms that electric utility vehicle adoption in commercial settings has grown at a rate exceeding gasoline counterparts for five consecutive years. Growing solar-powered charging integration and improved grid reliability in key geographies further reinforce the electric segment's sustained market leadership.

End-user Insights

The golf clubs type encompassing hotels/resorts, housing projects, and private golf clubs, constitutes the dominant end-user category, is likely to register 55% share in 2026. This primacy reflects the intrinsic relationship between golf cart usage and golf course operations, where fleet replenishment cycles, player transport logistics, and course maintenance all rely on purpose-designed carts.

According to the National Golf Foundation (NGF), the United States alone has approximately 16,000 golf facilities as of 2024, each maintaining average fleet sizes ranging from 50 to over 200 units. Hotels and resort complexes with integrated golf amenities represent a high-value sub-segment with premium vehicle specifications, supporting average selling price growth. Housing project communities with internal transport requirements and a growing sub-category within this leading segment.

Seating Capacity Insights

The Small (2–4-seater) configuration dominates the seating capacity category, representing approximately 61% of the overall market. Standard 2-seater and 4-seater carts remain the primary choice for golf course operations, personal transport within gated communities, and utility applications in airports and hospitality settings, owing to their compact form factor and manoeuvrability.

The Golf Course Superintendents Association of America (GCSAA) notes that most U.S. golf courses maintain fleets composed predominantly of standard 2-seater electric carts due to course design optimization. However, the Medium (6–8-seater) segment is gaining traction in airport passenger assistance programs and resort shuttle applications, reflecting operational efficiency improvements. Large capacity (10+ seater) variants serve niche but growing roles in industrial campuses and large public events.

Regional Analysis

North America Golf Cart Market Trends & Analysis

North America is the largest regional market for golf carts, accounting for approximately 40% of global revenue, driven by the region's deep-rooted golf culture, high density of golf facilities, and progressive adoption of electric fleet mandates. The United States remains the epicentre of global golf cart manufacturing and consumption, supported by a mature supply chain and well-developed distribution network. The proliferation of retirement communities in states such as Florida, Arizona, and Georgia many of which operate entire electric cart-based internal transport ecosystems has expanded the addressable market beyond traditional golf applications.

U.S. Golf Cart Market Trends

The U.S. dominates North America, representing approximately 88% of regional revenue, supported by approximately 16,000 active golf facilities and expanding utility vehicle applications in industrial and municipal segments. The U.S. market reached approximately US$ 967.8 Bn in 2026 and is projected to grow steadily through 2033 driven by electric fleet transition momentum and strong retirement community demand.

Europe Golf Cart Market Trends

Europe represents the second-largest golf cart market globally, supported by a strong golf culture in the United Kingdom, Germany, France, Sweden, and Spain. The European Golf Association (EGA) reports over 6,800 golf courses across Europe as of 2023. The region benefits from stringent emission reduction targets under the European Green Deal, which is compelling golf course operators and facility managers to transition entirely to electric fleets. Airport and public institution procurement for accessibility and logistics carts is also a noteworthy growth vector.

Germany Golf Cart Market Trends

Germany holds the largest share in continental Europe, estimated at ~20% of European regional revenue, driven by industrial campus utility vehicle demand and robust golf infrastructure. Market value was approximately US$ 85 Mn in 2025.

U.K. Golf Cart Market Trends

The U.K. is a key European market with one of the highest golf course densities globally. The market was valued at approximately US$ 78 Mn in 2025, with strong growth projected from resort-based and hospitality fleet adoption.

France Golf Cart Market Trends

France is a growing contributor to the European market, with increasing hotel and resort investments in the Alps and Riviera regions driving premium golf cart procurement. Estimated at approximately US$ 45 Mn in 2025.

Asia Pacific Golf Cart Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market for golf carts, projected to expand at a CAGR exceeding 7% by 2033. The region's growth is anchored by the rapid expansion of golf infrastructure in China, India, Japan, South Korea, and Southeast Asia, alongside rising urbanization and smart city deployments. China's ambitious New Energy Vehicle (NEV) policy ecosystem and India's push for electric mobility under the FAME II Scheme are catalysing fleet transitions across institutional and hospitality sectors.

China Golf Cart Market Trends

China represents the dominant Asia Pacific market, estimated at approximately US$ 280 Mn in 2025. Government-backed electric vehicle policies and large-scale manufacturing capabilities from domestic players are key drivers.

India Golf Cart Market Trends

India is an emerging high-growth market, valued at approximately US$ 65 Mn in 2025. Airport expansions under the UDAN scheme and rising luxury resort construction are primary demand catalysts.

Japan Golf Cart Market

Japan has a mature golf culture with over 2,000 golf courses. The market is estimated at approximately US$ 120 Mn in 2025, with a gradual shift toward electric fleet renewal being the key growth driver.

Competitive Landscape

The global golf cart market exhibits a moderately consolidated structure, with a small number of well-established original equipment manufacturers (OEMs) commanding significant combined revenue share at the global level, while regional and niche players account for a growing proportion in price-sensitive markets. Leading players are investing aggressively in lithium-ion battery integration, fleet telematics, and connected vehicle platforms as key differentiators.

Strategic partnerships with golf course management companies and airport authorities, along with geographic expansion into Asia Pacific and the Middle East, are primary growth levers. OEM strategies increasingly focus on total lifecycle service contracts, transitioning from pure hardware sales to fleet-as-a-service models that provide recurring revenue streams and long-term customer retention.

Key Developments:

- In January 2026, Samara Land Transportation declared the start of a project to produce electric golf cart assemblies in Saudi Arabia within a brand-new joint venture with Raya Holding. The project will put together a strong leadership capability and a deep market penetration by Samara in the Kingdom and the manufacturing/ mobility capability of Raya Holding via its mobility division and portfolio company, Raya Auto.

- In November 2025, Kinetic Green Tonino Lamborghini (KGTL) signed Surge Systems Pvt Ltd as the Indian representative of its electric luxury golf and lifestyle carts. The joint venture will combine the luxury electric cars of KGDL and the proven market of Surge Systems, which will make its contribution to the market development of professional turf maintenance.

Global Golf Cart Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$2.6 Bn |

|

Current Market Value (2026) |

US$ 3.4 Bn |

|

Projected Market Value (2033) |

US$ 4.9 Bn |

|

CAGR (2026-2033) |

5.4% |

|

Leading Region |

North America, 40% share |

|

Dominant Application |

Small (2-4), 61% share |

|

Top-ranking Product |

Golf Clubs, 55% |

|

Incremental Opportunity |

US$ 1.5 Bn |

Companies Covered in Golf Cart Market

- Club Car, LLC

- E-Z-GO (Textron Inc.)

- Yamaha Golf-Car Company

- Polaris Inc.

- Cushman

- Garia A/S

- Suzhou Eagle Electric Vehicle

- JH Global Services Inc.

- Advanced EV

- BIG Companies Inc.

- Columbia Vehicle Group Inc.

- Tomberlin Automotive Group

- ICON Electric Vehicles

- UFI Filters

Frequently Asked Questions

The global golf cart market is valued at US$ 3.4 Bn in 2026 and is projected to reach US$ 4.9 Bn by 2033, expanding at a CAGR of 5.4% during the forecast period. This growth is supported by accelerating electrification trends across golf, hospitality, airport, and smart campus applications globally.

The primary demand drivers include the global shift toward electric utility vehicles driven by emission regulations and declining lithium battery costs, expanding golf participation as recorded by the World Golf Foundation at 41.1 million U.S. players in 2023, growing airport and intra-facility mobility requirements, and increasing luxury resort and gated community deployments across Asia Pacific and North America.

The Electric product type dominates the golf cart market with approximately 72% share. Its leadership is attributed to stringent emission mandates, total cost of ownership advantages over a 5–7-year fleet lifecycle, and the declining cost of lithium-ion battery technology, which has made electric carts increasingly cost-competitive with gasoline alternatives even at the point of purchase.

North America is the leading region, holding approximately 40% of the global golf cart market. The United States' unparalleled golf course density of approximately 16,000 facilities, strong electric vehicle policy support under federal and state programs, a large and affluent retirement community ecosystem, and established major manufacturers headquartered in the region collectively underpin North America's market leadership.

The global golf cart market is led by Club Car, LLC, E-Z-GO (Textron Inc.), and Yamaha Golf-Car Company, which collectively account for a dominant share of global OEM revenue. Other notable participants include Polaris Inc., Garia A/S, Suzhou Eagle Electric Vehicle Manufacturing Co., Advanced EV, ICON Electric Vehicles, and Columbia Vehicle Group Inc., among others.