- Medical Devices

- Gelatin and Bone Glues Market

Gelatin and Bone Glues Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Gelatin and Bone Glues Market by Product (Gelatin, Bone Glues), Application (Arthroplasty, Sports Injury, Spine Surgery, Trauma, Others), End-user, and Regional Analysis from 2026 to 2033

Gelatin and Bone Glues Market Share and Trends Analysis

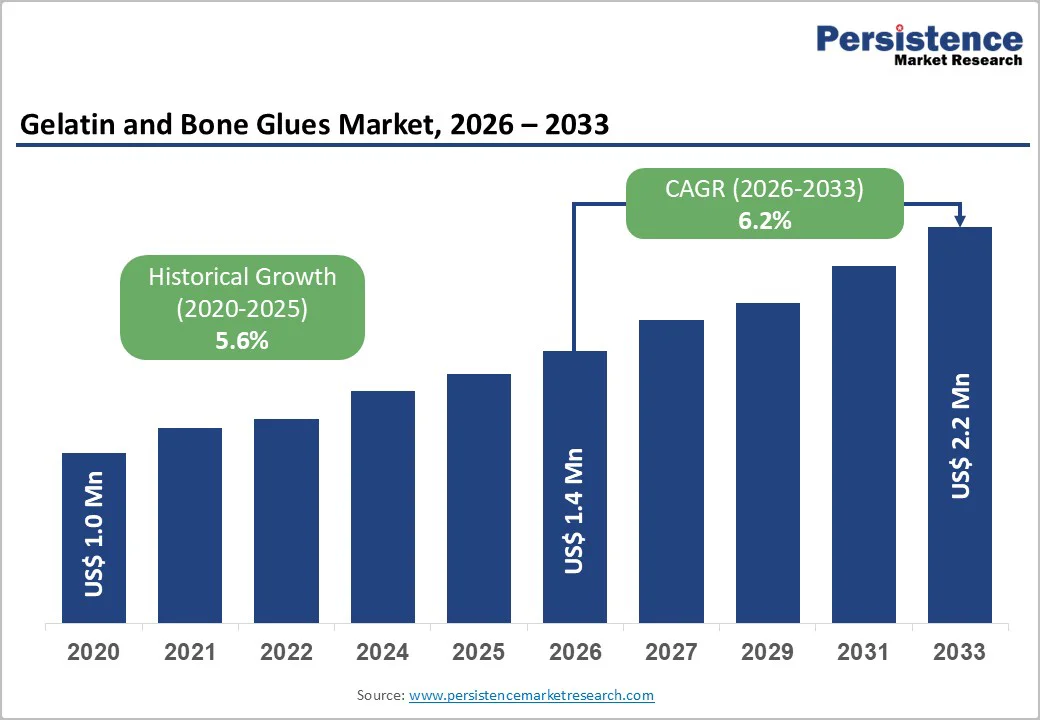

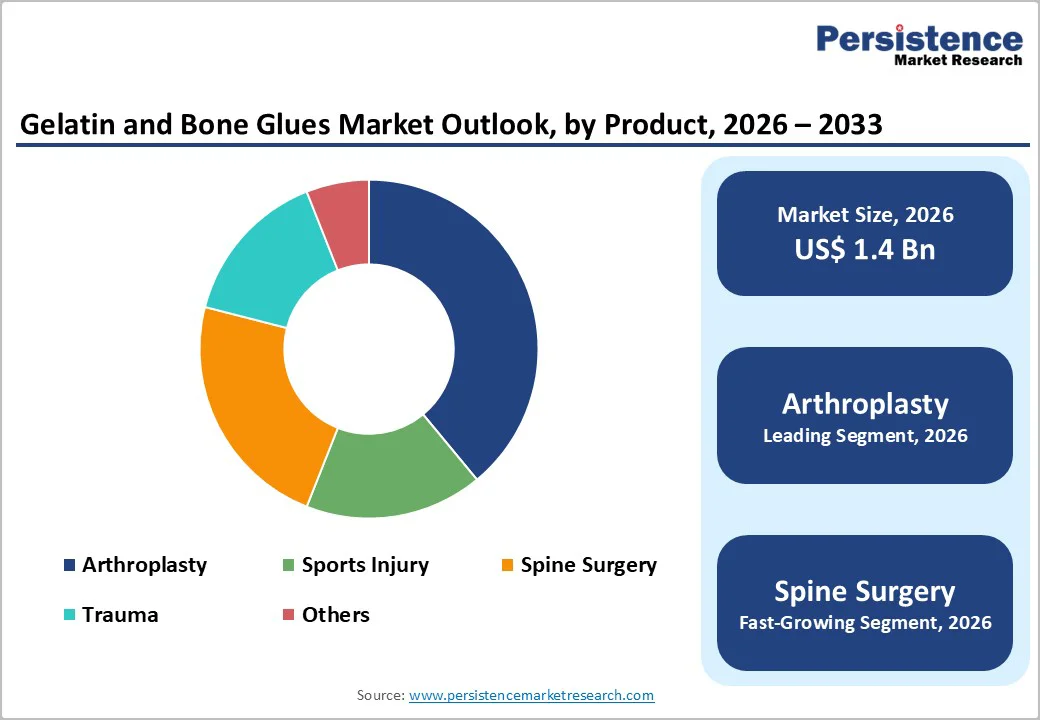

The global gelatin and bone glues market size is estimated to reach US$ 1.4 billion in 2026 and is projected to reach US$ 2.2 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. The adoption of gelatin and bone glues in orthopedic surgeries is rising steadily, driven by the need for stronger, safer, and more biologically compatible fixation solutions.

Their use is expanding across trauma care, arthroplasty, and minimally invasive procedures due to their strong bond strength and ability to stabilize complex fractures. Growing clinical preference for surgical sealants, particularly in osteoporotic spines, where conventional hardware may fail, is further accelerating demand. As patient volumes increase and surgeons prioritize improved healing outcomes, gelatin and bone glues are expected to witness robust uptake throughout the forecast period.

Key Industry Highlights

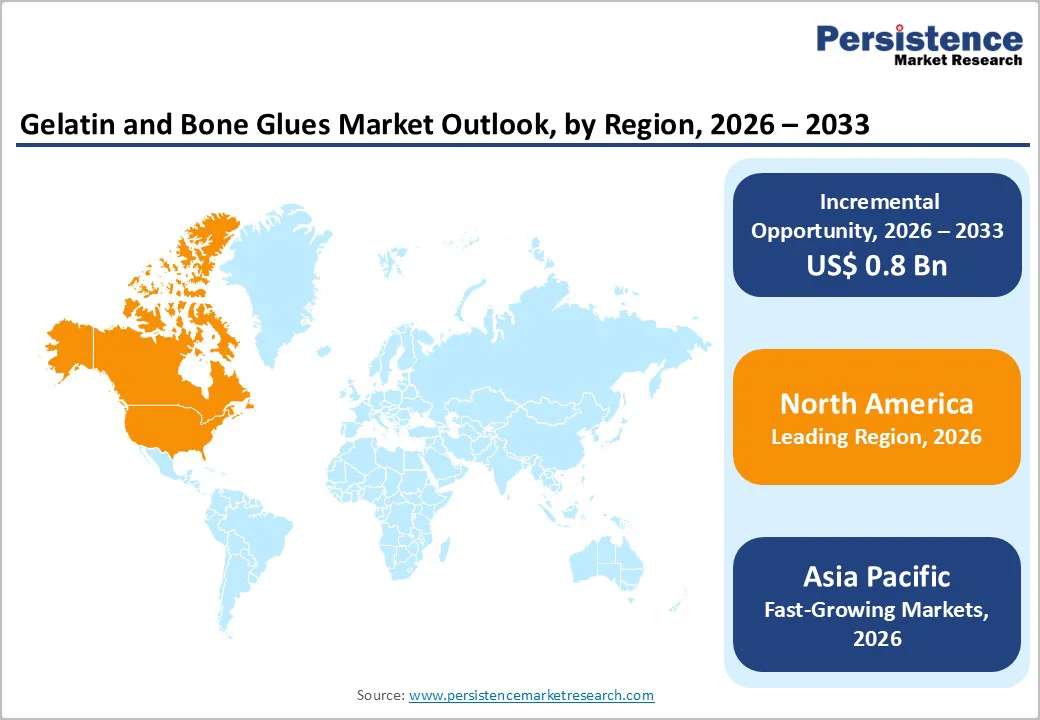

- Leading Region: North America dominates the global market with 34.1%, driven by strong orthopedic procedure volumes, early adoption of bioadhesives, and robust regulatory approvals supporting advanced fixation technologies.

- Fastest-Growing Region: Asia Pacific market is expected to grow rapidly with a CAGR of 7.8% in the forecast period, fueled by rising fracture incidence, expanding healthcare infrastructure, and increasing adoption of bone adhesives in cost-sensitive orthopedic settings.

- Leading Product: Gelatin leads with 68.2% share, supported by its biocompatibility, versatility in bone repair, and widespread usage across trauma, arthroplasty, and spine procedures.

- Leading Application: Arthroplasty to dominate with 38.8%, driven by increasing joint replacement volumes, higher fixation needs, and preference for bioadhesive support to enhance implant stability and healing.

- Leading Sales Channel: Institutional Sales lead with 48.6% share, due to high product utilization in hospitals and surgical centers performing trauma care, complex fractures, and joint reconstruction procedures.

- Increasing global road accidents and sports injuries are accelerating demand for bioadhesive fixation solutions that offer faster stabilization and reduced postoperative complications.

- Continuous R&D in biodegradable and osteoconductive adhesive materials supports safer, stronger fixation options, improving long-term clinical outcomes in orthopedic reconstruction.

- Rising shift toward ambulatory surgery centers increases demand for fast-curing adhesives that shorten operating time and support same-day discharge.

| Key Insights | Details |

|---|---|

| Global Gelatin and Bone Glues Market Size (2026E) | US$ 1.4 Billion |

| Market Value Forecast (2033F) | US$ 2.2 Billion |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Dynamics

Driver - Rising Orthopedic Burden and Innovation in Regenerative Bone Adhesives

The global gelatin and bone glues market is driven by the escalating clinical burden of fractures and orthopedic disorders, which is increasing demand for advanced biomaterials that enhance fixation, reduce hardware use, and support regenerative healing.

Rising orthopedic surgical volumes underline this need, with the 2024 American Joint Replacement Registry (AJRR) reporting 4.3 million hip and knee arthroplasties in the U.S., and ambulatory surgery centers increasing case submissions by nearly 300% since 2021, reflecting expanding procedure throughput.

The growing global incidence of fractures further accelerates adoption, as highlighted by the October 2024 World Health Organization (WHO) Fragility Fractures fact sheet, which reported 178 million new fractures in 2019-a 33.4% increase since 1990-along with a 70.1% surge in prevalent long-term fracture complications.

Unmet needs in complex fracture fixation also propel innovation, particularly for periarticular injuries that have postoperative complication rates up to 37% and failure rates of 10-20%. This gap is driving the development of next-generation adhesives such as OsStic™, which received U.S. Food and Drug Administration Breakthrough Device Designation in 2023 and again achieved a major milestone in January 2024, positioning bioadhesive technologies as essential solutions for stabilization where conventional methods fall short.

Restraints - Safety Concerns and Limited Regulatory Approvals for Advanced Bone Adhesive Products

The growth of the global gelatin and bone glues market is restrained primarily by regulatory complexity, limited clinical validation for load-bearing indications, and safety concerns around bone adhesives in high-stress orthopedic environments.

Stringent approval pathways remain a major bottleneck, as bone adhesives must demonstrate long-term biomechanical stability, biocompatibility, and remodeling capability-requirements far more demanding than traditional wound or soft-tissue adhesives, resulting in extended review timelines and delayed commercialization.

Clinical adoption is further limited by narrow approved indications, since most products remain restricted to cranial, dental, or non-load-bearing sites, preventing widespread use in weight-bearing fractures where failure risks are higher.

Surgeon hesitancy also constrains penetration, as historical complications associated with fixation materials such as aseptic loosening, infection, or interface instability in cement-augmented arthroplasty raise concerns about integrating new adhesive technologies into complex reconstructive procedures.

In addition, technical constraints persist as well, including variability in bonding strength in bleeding environments, challenges in achieving consistent curing profiles, and inadequate performance in osteoporotic bone-all of which slow integration into routine orthopedic trauma workflows. These limitations collectively temper global market expansion despite rising clinical need.

Opportunity - Breakthrough Bioadhesives and Light-Activated Technologies Expanding Orthopedic Applications Globally

Significant opportunities for the global gelatin and bone glues market are emerging as next-generation bioadhesive technologies progress toward stronger, more versatile, and more biocompatible orthopedic applications. Breakthrough innovations in multifunctional, regenerative adhesives are expanding the scope of use beyond traditional fixation.

For instance, in October 2023, researchers at the Indian Institute of Science Education and Research (IISER) Bhopal developed A30, a biodegradable, biocompatible adhesive capable of binding tissues, bone, eggshells, and even underwater surfaces, with an Indian patent secured, opening opportunities for bone repair, soft-tissue reconstruction, and drug-delivery applications.

Growing investment in new technologies such as light-activated, on-demand orthopedic adhesives also creates strong commercialization potential. In May 2025, Sweden’s Biomedical Bonding, a KTH spinoff, advanced a blue-light-cured thiol-ene adhesive designed to fix complex fractures with precision and minimal thermal damage, currently undergoing veterinary testing ahead of planned human trials-highlighting demand for alternatives to metal hardware in periarticular and comminuted fractures.

The market also benefits from rising global interest in minimally invasive and hardware-sparing techniques, where injectable or moldable bone glues can reduce surgical time, improve fragment stabilization, and support osteoconduction. Expanding approvals and research funding, particularly for adhesives that can integrate with screws or complement fixation plates, further strengthen the opportunity landscape for next-generation orthopedic biomaterials.

Category-wise Analysis

By Product Inisghts

Gelatin is expected to capture 68.2% of the global gelatin and bone glues market by 2026, supported by its extensive biomedical compatibility, favorable safety profile, and widespread use in hemostasis, wound sealing, and drug-delivery systems.

Its ability to integrate with other biomaterials for enhanced bone regeneration further strengthens demand across orthopedic and trauma care. Additionally, the growing preference for biocompatible, cost-effective alternatives to synthetic adhesives and cements is accelerating gelatin adoption in both developed and emerging healthcare settings, ensuring sustained product leadership within the market.

By Application Insights

Arthroplasty is projected to hold 38.8% of the global gelatin and bone glues market in 2026, driven by rising hip and knee replacement surgeries worldwide and increasing need for reliable fixation solutions.

The surge in aging populations, higher osteoarthritis burden, and greater adoption of minimally invasive joint procedures are further elevating adhesive use for stabilization, defect filling, and improved implant integration. As cases become more complex, gelatin-based adhesives and bone glues support enhanced post-operative outcomes, reinforcing their essential role in modern arthroplasty workflows across hospitals and specialty orthopedic centers.

By End-user Insights

Hospitals are projected to account for 48.6% of the global gelatin and bone glues market in 2026, supported by their high surgical caseloads, advanced orthopedic capabilities, and increasing adoption of regenerative biomaterials. Complex trauma care, joint reconstruction, and revision procedures performed in hospital settings consistently require adhesive solutions for bone repair, fixation support, and tissue reinforcement.

Growing investments in surgical infrastructure, multidisciplinary orthopedic teams, and access to next-generation bioadhesives further strengthen hospitals’ market share, ensuring they remain the primary consumers of gelatin and bone glue products globally.

Regional Insights

North America Gelatin and Bone Glues Market Trends

North America is projected to capture 34.1% of the global gelatin and bone glues market by 2026, driven by the region’s rise in orthopedic burden and rapid advancement in biomaterial-based fixation technologies. Growing fracture prevalence among older adults is a key demand driver, supported by the December 2023 American Academy of Orthopaedic Surgeons update showing global hip fractures rising from 1.26 million (1990) to 4.5 million by 2050, with one-year mortality at 24% and recovery rates below 50%.

Rising vertebral fracture incidence further amplifies biomaterial needs, with around 850,000 U.S. cases annually, highlighting limitations of polymethylmethacrylate due to thermal necrosis risks, non-biodegradability, and leakage rates up to 75%.

Continuous regional innovation in bone adhesives also accelerates adoption, demonstrated by RevBio’s August 2023 FDA approval for a 20-patient Tetranite® dental implant trial, the September 2024 NIH grant for cranial fixation studies, the December 2024 CMS reimbursement for Tetranite-assisted cranial flap fixation, and multiple 2025 NIH Phase II grants enabling further trials in aging-related and complex fracture repair-collectively strengthening North America’s leadership in regenerative bone adhesives.

Europe Gelatin and Bone Glues Market Trends

Europe is projected to account for 28.2% of the global gelatin and bone glues market by 2026, driven by the region’s accelerating shift toward regenerative biomaterials and the need for alternatives to conventional orthopedic fixation methods.

Growing demand for solutions that address complex fractures and defects underpins this trend, demonstrated by the January 2024 U.S. Food and Drug Administration Breakthrough Device Designation granted to OsStic®, an injectable bioadhesive developed through a multi-year collaboration between Biodesign Europe at Dublin City University, PBC Biomed, and Biomimetic Innovations. The designation reflects its potential to treat fractures where standard fixation fails to restore mobility or full joint function.

Expanding clinical evidence for next-generation bone adhesives further strengthens regional uptake, supported by the May 2025 approval from the Medicines and Healthcare Regulatory Agency in the United Kingdom for a 15-patient pilot trial using RevBio’s TETRANITE® for cranial flap reintegration.

The trial aims to improve cosmetic outcomes, enhance flap stability, and reduce cerebrospinal fluid leakage risks-demonstrating Europe’s growing emphasis on biomaterial-based fixation solutions that improve neurosurgical and orthopedic outcomes.

Asia Pacific Gelatin and Bone Glues Market Trends

Asia Pacific gelatin and bone glues market is rapidly expanding and is projected to achieve a CAGR of 7.8%, supported by the region’s strong push toward advanced, minimally invasive orthopedic repair technologies.

Rising demand for faster, hardware-free bone fixation is accelerating research and adoption, particularly in China, where major breakthroughs are reshaping clinical capabilities. This trend is exemplified by the September 2025 announcement from Chinese scientists, who unveiled a medical bone adhesive - “Bone 02”-designed to repair fractured and shattered bone fragments within minutes.

Inspired by oyster adhesion mechanisms, the injectable glue can bond bone fragments in 2-3 minutes, even in blood-rich environments where conventional adhesives struggle. Its reported bonding force exceeding 400 pounds, shear strength of 0.5 MPa, and compressive strength of 10 MPa signal the potential to replace metal plates, screws, and invasive fixation procedures.

By offering rapid stabilization, reduced infection risks, and the possibility of implant-free healing, innovations including Bone 02 demonstrate the region’s accelerating shift toward next-generation orthopedic adhesives, thereby strengthening Asia Pacific’s role as a key growth.

Competitive Landscape

The competitive landscape is shaped by innovators advancing next-generation regenerative bone adhesives, focusing on rapid fixation, high bonding strength, and alternatives to metal implants. Players are accelerating clinical trials, securing regulatory clearances, and gaining government or grant support to scale applications across cranial, orthopedic, and trauma repair, intensifying technology-led differentiation in the market.

Key Industry Developments:

- In December 2024, RevBio received FDA approval to expand its TETRANITE® clinical trial for immediate cranial flap fixation, supported by CMS reimbursement. The expansion follows successful safety outcomes in the first five patients, reinforcing its globally patented regenerative bone adhesive platform.

- In October 2025, RevBio secured a $2.2 million Phase II SBIR grant from the National Institute on Aging to advance preclinical testing under grant 1R44AG097243-01, building on prior Phase I work and progressing toward FDA clearance for initiating human clinical trials.

- In November 2025, RevBio gained approval for a 20-patient pilot study evaluating TETRANITE’s safety and efficacy for complex multi-fragmented wrist fractures, assessing its gap-filling, fragment-fixation, and osteoconductive performance as both an intraoperative aid and adjunct to hardware fixation.

Companies Covered in Gelatin and Bone Glues Market

- Artivion, Inc

- Baxter

- RevBio, Inc.

- H.B. Fuller Company

- PBC BioMed

- B. Braun SE

- Amend Surgical

- Halifax

Frequently Asked Questions

The global gelatin and bone glues market is projected to be valued at US$ 1.4 Billion in 2026.

Rising orthopedic surgical volumes and demand for biocompatible, regenerative adhesives that reduce hardware use drive market growth.

The global market is poised to witness a CAGR of 6.2% between 2026 and 2033.

Expanding use in minimally invasive fracture repair and next-generation bioactive adhesives present major growth opportunities.

Major players in the global are Artivion, Inc., Baxter, RevBio, Inc., H.B. Fuller Company, and others.