- Medical Devices

- Functional Brain Imaging System Market

Functional Brain Imaging System Market Size, Share, and Growth Forecast, 2026 - 2033

Functional Brain Imaging System Market by Product Type (Functional Magnetic Resonance Imaging (fMRI) Systems, Others), Application (Neurology, Psychiatry, Oncology, Cognitive Science), End-user (Hospitals, Others), and Regional Analysis for 2026 - 2033

Functional Brain Imaging System Market Size and Trends Analysis

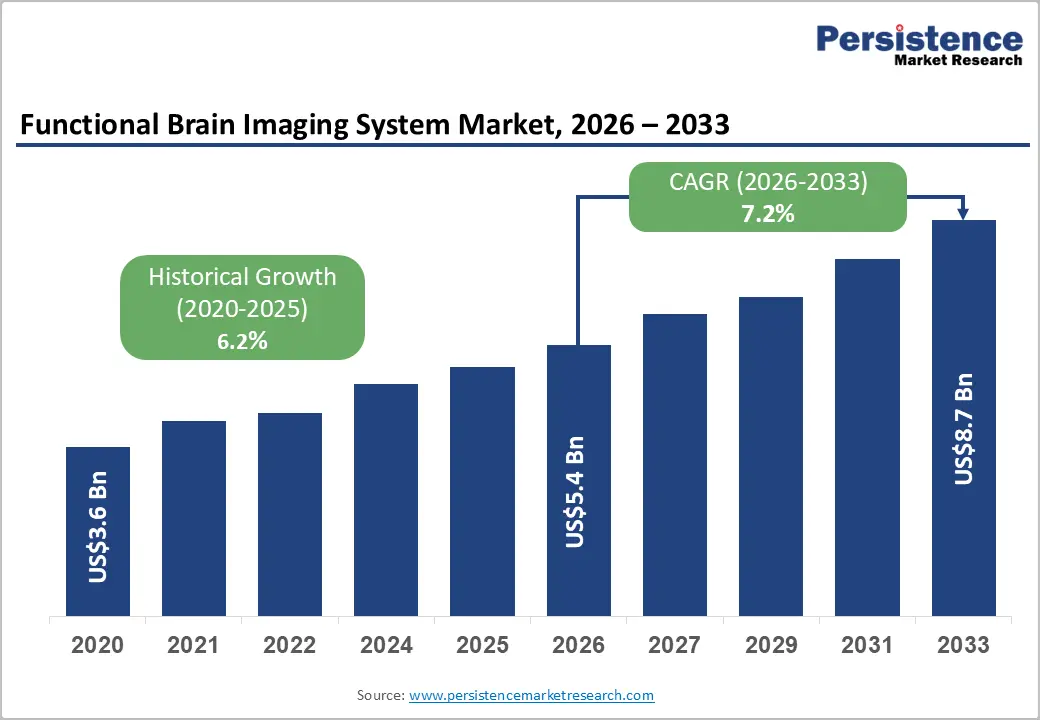

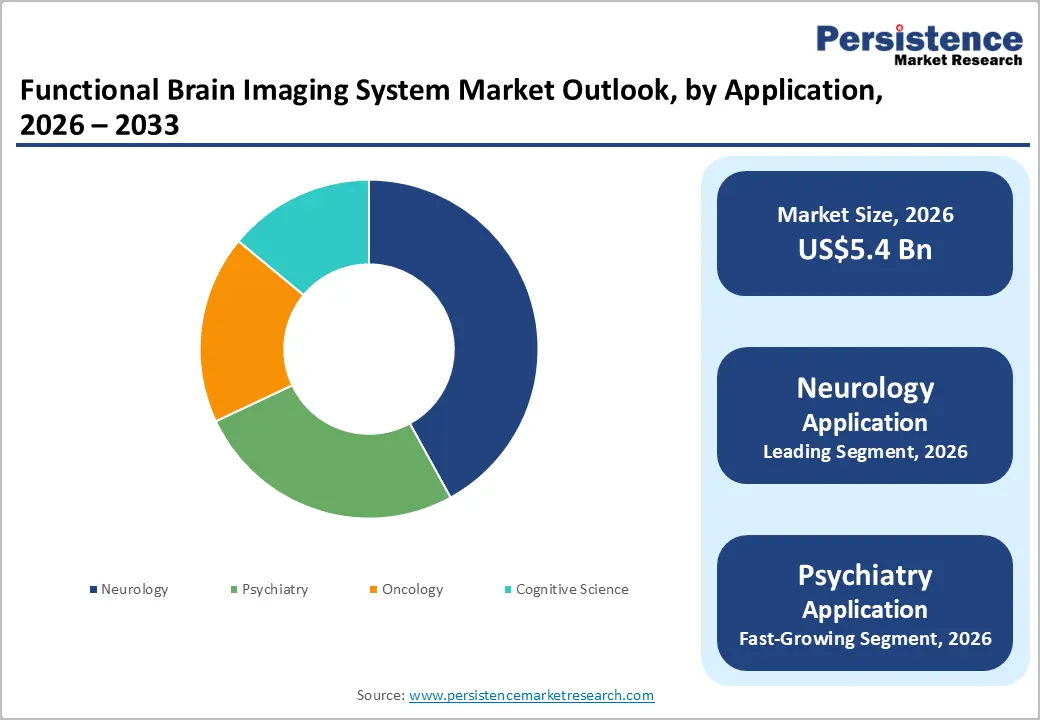

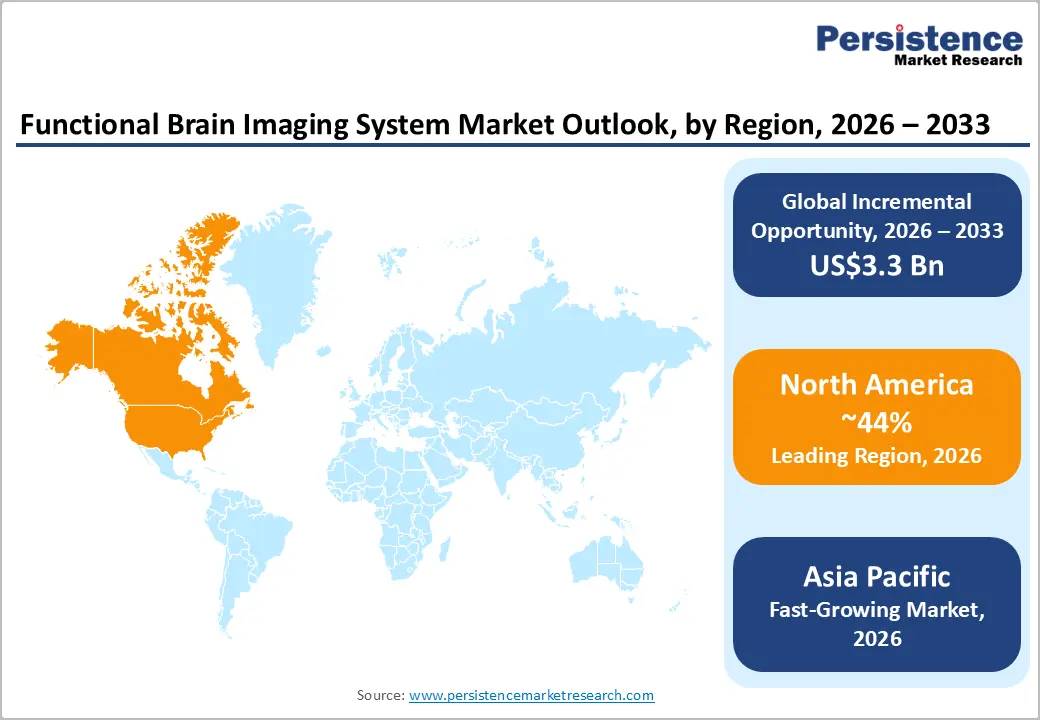

The global functional brain imaging system market size is likely to be valued at US$5.4 billion in 2026, and is expected to reach US$8.7 billion by 2033, growing at a CAGR of 7.2% during the forecast period from 2026 to 2033, driven by the rising prevalence of neurological and psychiatric disorders, increasing investments in large-scale neuroscience and brain research initiatives, continuous advancements in imaging technologies and AI-powered neuroimaging analytics, and the expanding use of functional brain imaging in applications such as neurosurgical planning, epilepsy diagnosis and monitoring, psychiatric drug development, and evaluation of cognitive impairment and neurodegenerative conditions.

Key Industry Highlights:

- Dominant Region: North America is expected to dominate with an estimated 44% revenue share in 2026, driven by major government neuroscience funding programs, advanced hospital and academic research infrastructure, and the concentrated presence of leading imaging system manufacturers.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing regional market, driven by rapidly expanding hospital infrastructure investment in China and India, rising neurological disease burden, and growing neuroscience research program development.

- Leading Product Type: MRI systems are anticipated to dominate with approximately 52% share in 2026, reflecting their established role as the primary non-invasive functional brain mapping tool in both clinical neurology and neuroscience research settings globally.

- Dominant Application: Neurology is the leading application segment, accounting for approximately 42% of market value in 2026, underpinned by the large and growing clinical burden of stroke, epilepsy, neurodegenerative disease, and traumatic brain injury requiring functional neuroimaging assessment.

DRO Analysis

Driver - AI Integration and Advanced Analytics: Transforming Functional Neuroimaging Utility

The integration of artificial intelligence (AI) and machine learning (ML) into functional brain imaging workflows is significantly enhancing the clinical utility, operational efficiency, and diagnostic accuracy of fMRI, PET, and fNIRS systems, thereby accelerating system upgrade cycles and increasing adoption across hospitals and research institutions. Advanced AI-enabled fMRI analysis platforms leverage deep learning algorithms for automated brain atlas segmentation, functional connectivity analysis, resting-state network detection, and task-based activation mapping, enabling faster interpretation of imaging data and reducing the time required to generate clinically actionable insights.

The acquisition cost and the operational expense profile of functional MRI and PET brain imaging programs create sustained budget pressure for healthcare facilities. Helium consumption for MRI superconducting magnet cooling, despite advances in helium-free magnet technology, remains a high recurring cost for legacy 1.5T and 3T systems.

Restraint - Regulatory Complexity and Lengthy Clinical Validation for Novel Functional Imaging Biomarkers

The translation of novel functional brain imaging biomarkers, including resting-state fMRI connectivity signatures for psychiatric diagnosis, amyloid and tau PET tracers for Alzheimer's staging, and fNIRS-based neurofeedback protocols from research validation to routine clinical use, involves complex regulatory pathways that significantly delay market commercialization timelines. The U.S. FDA's qualification pathways for novel neuroimaging biomarkers as drug development tools require extensive multi-site validation datasets demonstrating biomarker reproducibility, sensitivity, specificity, and clinical outcome correlation processes that typically require 7-12 years from initial biomarker discovery to qualified clinical use designation.

In Europe, the EU In Vitro Diagnostic Regulation (IVDR) and Medical Device Regulation (MDR), which apply to functional imaging-associated companion diagnostic software and AI-based neuroimaging analysis tools, impose enhanced clinical evidence requirements and notified body review obligations that extend product development timelines and increase compliance costs for neuroimaging technology developers.

Opportunity - Portable and Wearable fNIRS Systems for Ambulatory and Point-of-Care Brain Monitoring

Functional Near Infrared Spectroscopy (fNIRS) technology represents a transformative market expansion opportunity for functional brain imaging, enabling lightweight, portable, and wearable brain monitoring capabilities that conventional MRI and PET systems cannot provide. fNIRS systems measure cortical hemodynamic responses using near-infrared light that can penetrate the scalp and skull, detecting oxygenation and blood volume changes associated with neural activity without ionizing radiation, contrast agents, or the stringent magnetic field constraints that limit MRI deployment environments.

Manufacturers, including Hitachi Medical Systems and specialized fNIRS system developers, are actively commercializing wearable fNIRS headsets for cognitive function monitoring, attention deficit disorder assessment, and sport concussion protocols, creating new market segments within the functional brain imaging system landscape that extend the addressable market well beyond traditional hospital-based scanner installations.

Category-wise Analysis

Product Type Insights

fMRI systems are projected to dominate the market, accounting for an estimated 52% share of total revenue in 2026. fMRI's market leadership reflects its established position as the non-invasive gold standard for functional brain mapping, simultaneously offering whole-brain coverage, high spatial resolution, no ionizing radiation, and established clinical reimbursement pathways across neurology, neurosurgery, and psychiatric research applications. Siemens Healthineers integrated functional MRI into epilepsy and brain tumor presurgical planning through its MAGNETOM MRI systems, enabling non-invasive brain mapping with high spatial resolution and whole-brain coverage.

fNIRS systems represent the fastest-growing product type. This exceptional growth reflects the technology's unique combination of portability, lower cost, and motion tolerance that enables functional brain monitoring applications in ambulatory, neonatal ICU, pediatric, and sports medicine contexts where conventional MRI is impractical. Artinis Medical Systems expanded portable fNIRS use in sports science and rehabilitation, enabling real-time brain monitoring during movement, where conventional MRI was impractical.

Application Insights

Neurology is anticipated to dominate the application segment, accounting for an estimated 42% of revenue in 2026. Clinical neurological applications, including presurgical epilepsy focus localization, stroke connectivity assessment, traumatic brain injury functional outcome monitoring, and multiple sclerosis lesion activity characterization, generate the highest per-scan clinical reimbursement and most consistent institutional procurement demand. GE HealthCare supported advanced neurological imaging applications through its SIGNA MRI platform, which hospitals used for epilepsy presurgical mapping, stroke assessment, and traumatic brain injury evaluation.

Psychiatry is likely to be the fastest-growing application segment. The precision psychiatry movement, combining fMRI-derived functional connectivity biomarkers with AI-driven patient stratification algorithms for depression, schizophrenia, PTSD, and OCD, is creating rapidly growing institutional demand for high-field fMRI scanner capacity in psychiatric research and clinical programs. Philips collaborated with research institutions to advance AI-enabled fMRI and brain connectivity analysis for precision psychiatry research in depression and schizophrenia.

End-user Insights

Hospitals are expected to dominate the end-user segment, capturing approximately 55% of revenue in 2026. Major academic medical centers and tertiary care hospitals, which house the highest-complexity neurological, neurosurgical, and psychiatric patient populations, generate the greatest institutional demand for premium fMRI and PET/MRI system installations. Siemens Healthineers installed MAGNETOM MRI and Biograph PET/MRI systems at leading academic hospitals, including Mayo Clinic, to support advanced neurological and neurosurgical imaging.

Diagnostic imaging centers are expected to be the fastest-growing end-user segment. The rapid expansion of independent and hospital-affiliated outpatient diagnostic imaging networks driven by healthcare cost containment objectives, increasing outpatient procedure migration, and growing demand for accessible neuroimaging services beyond academic medical centers is creating significant new installation opportunities for functional brain imaging systems in high-volume outpatient settings. SimonMed Imaging expanded its outpatient imaging network with advanced MRI services to improve access to neurological and brain imaging outside major academic hospitals.

Regional Insights

North America Functional Brain Imaging System Market Trends

North America is projected to dominate, holding approximately 44% of the total revenue in 2026. The region benefits from major government neuroscience funding, the U.S. NIH BRAIN Initiative, NIMH research programs, and DARPA neurotechnology programs, combined with the world's most advanced academic medical center's neuroimaging infrastructure and comprehensive Medicare/Medicaid reimbursement frameworks for clinical functional neuroimaging procedures.

U.S. Functional Brain Imaging System Market Insights

The U.S. functional brain imaging market is driven by strong NIH neuroscience funding, CMS reimbursement for fMRI and PET brain imaging, and a large installed base of over 7,000 MRI systems. GE HealthCare, Siemens Healthineers, and Philips compete actively through advanced imaging platforms and academic research collaborations.

Canada Functional Brain Imaging System Market Insights

Market growth in Canada is supported by the Canadian Institutes of Health Research (CIHR) neuroscience research funding programs and provincial health authority investments in hospital MRI and PET neuroimaging capacity. Major Canadian neuroimaging research centers, including the Montreal Neurological Institute (The Neuro) and Baycrest Centre for Geriatric Care in Toronto, are internationally recognized functional neuroimaging research hubs that generate system procurement demand and influence global neuroimaging technology adoption trends.

Europe Functional Brain Imaging System Market Trends

Europe shows steady growth, driven by the EU Human Brain Project's legacy neuroimaging infrastructure investments, national health system fMRI reimbursement frameworks, and strong academic neuroscience research ecosystems across Germany, the U.K., France, and the Netherlands.

Germany Functional Brain Imaging System Market Trends

Germany led the functional brain imaging market through strong academic neuroimaging networks, including the Max Planck Institute for Human Cognitive and Brain Sciences and the German Center for Neurodegenerative Diseases. Siemens Healthineers strengthened its market position through its MAGNETOM MRI platform and broad installation base across university hospitals.

U.K. Functional Brain Imaging System Market Trends

The U.K. functional brain imaging market is driven by NHS investment in advanced 3T MRI systems and strong neuroimaging research infrastructure, including the Wellcome Centre for Human Neuroimaging. NICE guidance and multi-site programs led by the UK Dementia Research Institute continue to support fMRI and PET imaging utilization across NHS hospitals and research facilities.

Asia Pacific Functional Brain Imaging System Market Trends

Asia Pacific is likely to be the fastest-growing regional market, driven by rapidly expanding hospital infrastructure, rising neurological disease burden, growing government neuroscience research investment, and increasing MRI system density across major Asia Pacific healthcare systems.

China Functional Brain Imaging System Market Trends

China is the dominant Asia Pacific market. China's healthcare investments targeting hospital MRI capacity expansion and specialty neurological disease management capability are driving systematic procurement of functional imaging-capable 3T MRI systems across Chinese tertiary hospital networks. The China Brain Project is funding domestic neuroimaging research infrastructure development at Chinese universities and research institutes, creating institutional demand for advanced fMRI and PET imaging platforms.

India Functional Brain Imaging System Market Trends

India is one of the fastest-growing markets in Asia Pacific, driven by rapidly expanding private hospital and diagnostic imaging center networks, growing awareness of functional neuroimaging's clinical utility among Indian neurologists and neurosurgeons, and government investments in AIIMS (All India Institute of Medical Sciences) network expansion, which includes functional neuroimaging capabilities at multiple AIIMS campuses.

Competitive Landscape

The global functional brain imaging system market is moderately consolidated, with Siemens Healthineers, Philips, GE HealthCare, and Canon Medical Systems collectively accounting for 65%-75% of global fMRI system revenue. Siemens Healthineers led the market through its MAGNETOM MRI portfolio, including Prisma, Terra, and Altea systems, supported by advanced gradient performance and Syngo via imaging software.

Specialized and regional players occupy important competitive niches across specific functional imaging modalities and geographic markets. Hitachi Medical Systems and Nihon Kohden provide functional neuroimaging and EEG-based brain monitoring systems with strong Asia Pacific market presence. EB Neuro S.p.A. specializes in EEG and neurophysiology systems, complementing functional MRI in epilepsy monitoring applications.

Key Industry Developments:

- In February 2026, Positrigo launched the BrainPET Accelerator Program in the U.S. to help neurology practices integrate advanced brain PET imaging directly into their offices. The program combined the company’s compact NeuroLF brain PET system with operational, regulatory, and clinical support to simplify adoption and improve access to point-of-care neurological imaging.

- In July 2025, Philips received FDA 510(k) clearance for its SmartSpeed Precise dual AI MRI software, which improved scan speed and image precision across its 1.5T and 3.0T MRI systems. The company stated that the software enabled up to three times faster scans and delivered sharper images through integrated AI-powered denoising and image reconstruction technology.

Companies Covered in Functional Brain Imaging System Market

- Koninklijke Philips N.V.

- General Electric Company

- Canon Medical Systems Corporation

- EB Neuro S.p.A.

- MinFound Medical Systems Co., Ltd

- Neurosoft

- Medtronic Plc

- Nihon Kohden Corporation

- Hitachi Medical Systems

- Elekta

- Siemens AG

Frequently Asked Questions

The global functional brain imaging system market is projected to reach US$5.4 billion in 2026.

Rising demand for faster and more accurate MRI diagnostics drove the adoption of AI-powered imaging software across healthcare facilities.

The functional brain imaging system market is poised to witness a CAGR of 7.2% from 2026 to 2033.

Increasing use of precision imaging in neurology, oncology, and cardiovascular diagnostics also supported future market expansion.

Key players include Koninklijke Philips N.V., General Electric Company (GE Healthcare), Canon Medical Systems Corporation, EB Neuro S.p.A., MinFound Medical Systems Co. Ltd., Neurosoft, Medtronic Plc, Nihon Kohden Corporation, Hitachi Medical Systems, Elekta, and Siemens AG.