- HVAC

- Freeze Protection Cables Market

Freeze Protection Cables Market Size, Share, and Growth Forecast 2026 - 2033

Freeze Protection Cables Market by Product Types (Constant Wattage, Mineral Insulated, Parallel Constant Watt Heating Cable, Power-Limiting Heating Cable, Self-Regulating, Series Constant Watt Heating Cables and Skin Effect), by Applications (Floor Heating, Freeze Protection, Process Temperature Maintenance, Roof & Gutter De-Icing and Viscosity Control), and by End-User (Commercial, Food & Beverages, Oil & Gas, Pharmaceuticals, Power, Energy & Heavy Industry, Residential, Water & Wastewater Management and Other ) and Regional Analysis for 2026 – 2033

Freeze Protection Cables Market Share and Trends Analysis

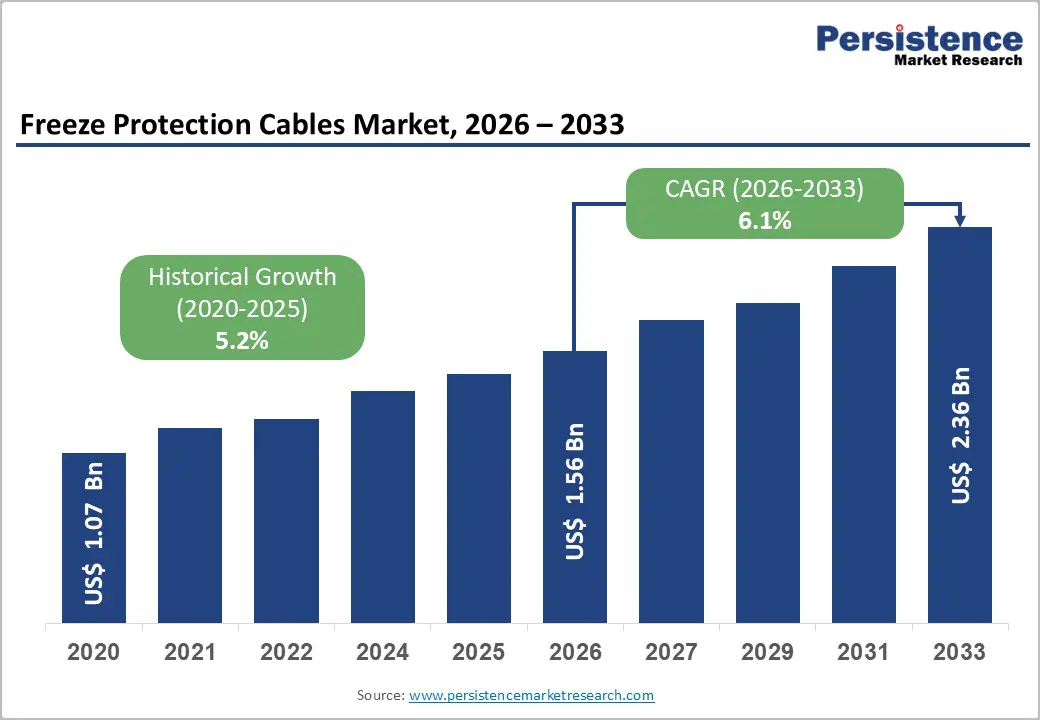

The global Freeze Protection Cables Market size was valued at US$ 1.6 Billion in 2026 and is projected to reach US$ 2.4 Billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033. Growing focus on infrastructure resilience in cold climates, expansion of process industries, and stricter building and safety codes are the core drivers behind this steady growth. Electrical heat tracing using constant wattage, self-regulating, and mineral-insulated cables has become a critical safeguard for pipelines, tanks, roofs, gutters, and floors across industrial, commercial, and residential environments, reducing downtime, preventing pipe bursts, and enhancing energy efficiency. Rising investment in energy-efficient buildings, modernization of oil & gas and chemical facilities.

Key Market Highlights

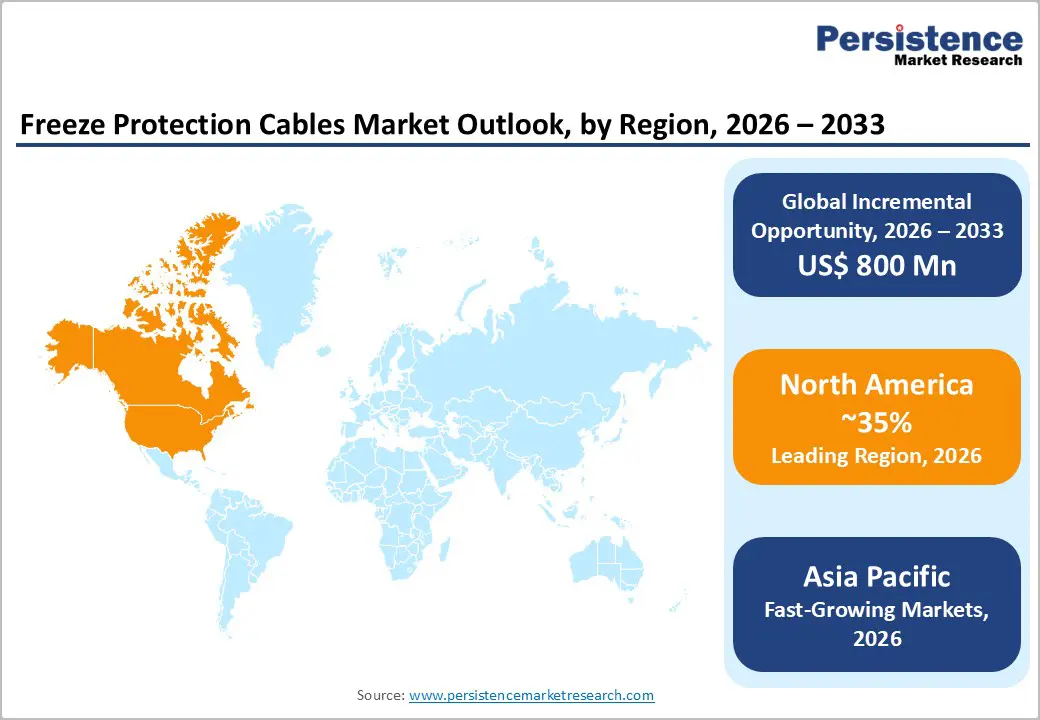

- North America leads the Freeze Protection Cables Market, supported by severe winters, dense pipeline infrastructure, and strict codes such as IBC, IMC, and ASHRAE 90.1, which drive widespread adoption of electric heat tracing across residential, commercial, and industrial facilities.

- Asia Pacific is the fastest-growing region, benefitting from rapid industrialization, expansion of petrochemical and power generation assets in cold or high-altitude locations, and rising local manufacturing capability for self-regulating and constant wattage cables in China and India.

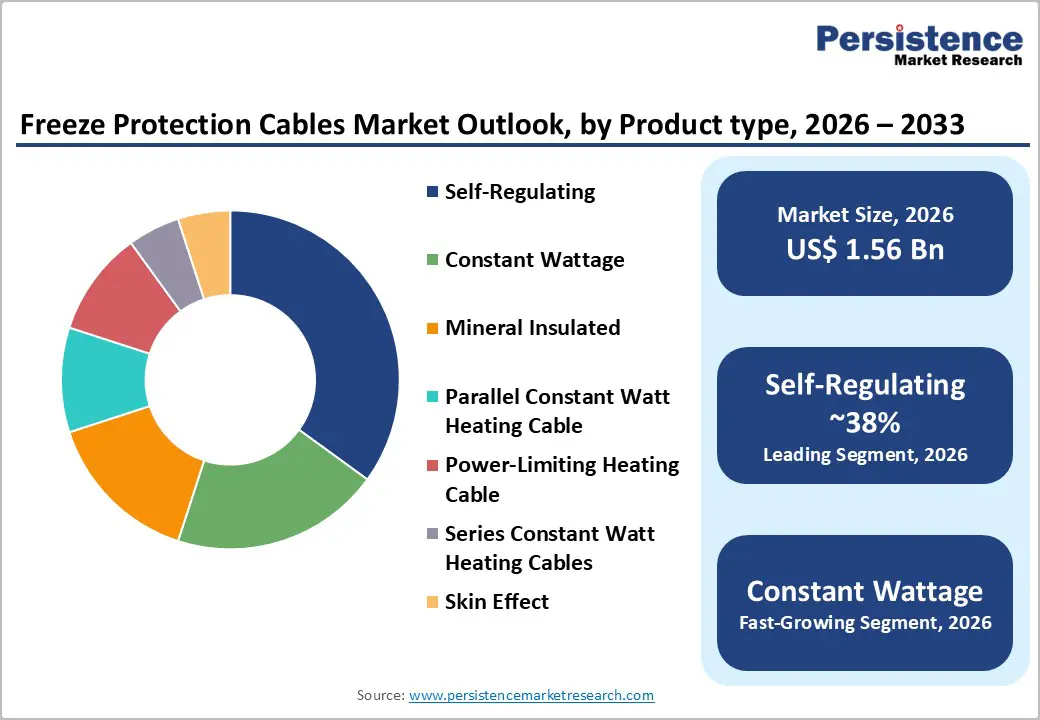

- Self-Regulating cables form the dominant product segment, capturing an estimated 38% share owing to their automatic power adjustment, installation safety, and energy efficiency advantages over traditional constant wattage solutions in freezer protection and low-temperature maintenance applications.

- Freeze Protection remains the largest application segment at about 44% share, as building owners, municipalities, and industrial operators rely on heating cables to prevent pipe bursts, roof ice dams, and sprinkler failures, especially in colder geographies with aging infrastructure.

| Key Insights | Details |

|---|---|

| Freeze Protection Cables Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 2.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2024) | 5.2% |

Market Dynamics

Market Growth Drivers

Rising incidence of extreme cold events and infrastructure winterization

Increasing frequency of polar vortex events and prolonged cold spells in North America, Europe, and parts of Asia is sharply elevating demand for reliable freeze protection of critical infrastructure. Municipal codes such as the International Building Code (IBC), International Mechanical Code (IMC), ASHRAE 90.1, and IECC increasingly require adequate pipe protection and minimum indoor temperatures to prevent freezing of plumbing and fire sprinkler systems, pushing building owners toward electric heat tracing. In the broader heating cable space, freeze protection is cited as the largest application, reflecting its role in preventing pipe bursts, roof ice dams, and service outages in commercial and residential buildings. As more warehouses, logistics centers, and speculative industrial buildings are designed with low base heating to save energy, heat tracing becomes essential to keep water and sprinkler lines above 0 °C, directly translating into higher consumption of constant wattage, self-regulating, and power-limiting freeze protection cables.

Expansion of process industries and critical pipelines in harsh climates

The rapid build-out of pipelines, terminals, and refineries in cold regions such as Northern Europe, Russia, Canada, and high-altitude locations is a major catalyst for industrial heat tracing demand. In the oil & gas sector, uncontrolled cooling can lead to wax deposition, hydrate formation, and viscosity increases that restrict flow or completely block lines, with a single frozen pipeline capable of shutting in production and causing multi-million-dollar losses. Electric heat tracing using self-regulating and constant wattage cables is widely deployed to maintain pipelines above critical temperatures and ensure safe transport of hydrocarbons, chemicals, and slurries. Similar requirements exist in the food & beverages and pharmaceuticals sectors, where process lines must be maintained within narrow temperature bands to uphold product quality and hygiene regulations. As refineries integrate more complex process schemes and as chemical producers handle a wider range of viscous and crystallization-prone fluids, demand for advanced freeze protection and process temperature maintenance cables continues to climb. In parallel, increased construction activity using advanced building envelopes and specialty Construction Chemicals Market products often incorporates embedded heat trace systems to protect exposed pipes and decks, further expanding cable usage.

Market Restraints

High installation and lifecycle costs for large-scale systems

Comprehensive heat tracing projects for industrial plants and large commercial complexes require significant upfront investment, including engineering design, cables, controllers, insulation, and electrical upgrades. For complex pipelines, total installation cost can run into hundreds of thousands of dollars, and retrofits in operating facilities are especially expensive due to shutdown requirements and access constraints. Ongoing expenses for power consumption, periodic inspection, and replacement of damaged or aged cables add to the lifecycle cost burden. In cost-sensitive markets and smaller residential applications, this expense can deter adoption, encouraging continued reliance on lower-cost but less reliable alternatives such as passive insulation or intermittent space heating. Limited awareness of long-term savings from avoided freeze damage and downtime also slows investment decisions in emerging economies.

Design complexity, standards compliance, and skills gap

Effective freeze protection systems must be engineered to meet rigorous standards such as IEEE 515, IEC/IEEE 60079301, and 60079302, especially in hazardous areas with explosive atmospheres. Designing proper circuit lengths, power densities, control schemes, and insulation thickness requires specialist expertise, yet many small contractors and facility operators lack experienced heating engineers. Inadequate design or poor installation practices can lead to uneven heating, overheating, premature cable failure, or non-compliance with explosion-protection requirements, undermining trust in electric tracing solutions. In developing markets, scarcity of certified installers and limited access to standards documentation are further complicated system deployment. This skills gap slows adoption, particularly for advanced technologies such as skin effect and series constant watt systems intended for very long pipelines.

Market Opportunities

Rapid adoption of self-regulating and power-limiting cable technologies

Self-regulating heating cables automatically adjust their heat output along their length in response to ambient temperature changes, eliminating hotspots and reducing energy consumption. Technical literature shows that such cables significantly improve safety by virtually eliminating overheating risk, allowing them to be fully insulated and used on plastic pipes and complex geometries. Industry sources highlight self-regulating designs as the preferred solution for low-temperature freeze protection, especially in residential and light commercial environments where simplicity and energy efficiency are paramount. As energy codes tighten and electricity prices rise, facilities are seeking heat tracing solutions that minimize operating cost while maintaining reliability, making self-regulating and power-limiting cables the fastest-growing product types. Manufacturers that combine these cable technologies with intelligent electronic controllers, remote monitoring, and building-management-system integration stand to capture outsized growth as building owners pursue smart, energy-efficient freeze protection strategies aligned with broader decarbonization goals.

Integration of digital controls, analytics, and safety-critical compliance in industrial heat tracing

The industrial heat tracing environment is moving rapidly toward digitalization, with advanced control panels, distributed temperature sensing, and cloud-connected monitoring solutions enabling predictive maintenance and energy optimization. Digital controllers can duty-cycle circuits based on real-time temperature, ambient forecasts, and process conditions, yielding measurable energy savings compared to legacy thermostats. In oil & gas and chemical plants, integrated heat trace management platforms support documentation for Process Safety Management, regulatory audits, and functional safety standards, helping operators reduce the risk of freeze-induced spills and environmental incidents. The ongoing harmonization of IEC/IEEE 60079-30 and improvements in testing guidance are prompting operators to modernize existing systems with new, compliant equipment rather than extending the life of aging installations. Vendors that deliver end-to-end digital solutions—combining cables, controls, engineering, and lifecycle services—can differentiate themselves and tap sizeable modernization budgets over the next decade as industrial asset owners prioritize reliability and regulatory compliance.

Category-wise Insights

Product Type Analysis

In the Product Type category, Self-Regulating cables account for an estimated 38% of global market share, making them the leading segment within the Freeze Protection Cables Market. Technical guides describe self-regulating cables as the preferred option for freeze protection and low-temperature maintenance because they vary output with temperature and can be safely overlapped without risk of overheating. This feature simplifies installation and reduces the need for complex control systems, particularly in residential, commercial, and light industrial settings where pipe layouts are irregular and local temperatures vary widely.

Furthermore, their inherent energy efficiency output decreases automatically as pipes warm aligns with rising energy-efficiency codes and carbon-reduction targets, driving replacement of legacy constant wattage tapes. While constant wattage, mineral-insulated, and skin effect cables remain indispensable for high-temperature or very long-line industrial applications, self-regulating designs are expected to outpace the overall market growth as building modernization programs and infrastructure upgrades prioritize safe, easy-to-maintain solutions.

Applications Analysis

Within Applications, Freeze Protection clearly emerges as the dominant segment, representing around 44% of heating cable demand across residential, commercial, and municipal systems. Industry analysts note that freeze protection applications for water pipes, fire sprinkler systems, roofs, gutters, and downspouts generate the largest revenue share, as they directly prevent costly pipe bursts, building damage, and service interruptions during winter conditions. Electric heat tracing provides a reliable and relatively low-cost retrofit option compared with structural redesign or continuous space heating, making it attractive to building owners upgrading existing stock. Codes and standards such as IBC, IMC, and various European building specifications increasingly emphasize maintaining minimum temperatures in spaces with plumbing or fire water systems, mandating measures that often include heat tracing where insulation alone is insufficient. With urban areas in colder climates continuing to densify and building owners seeking to winter-proof critical infrastructure, freeze protection applications are expected to retain their lead over floor heating, process temperature maintenance, and roof & gutter de-icing, even as those segments also grow.

End Users Analysis

In the End Users category, the Residential segment holds the largest share at approximately 32% of global revenue, reflecting widespread adoption of heating cables for pipe freeze protection and underfloor heating in homes. Residential customers, particularly in North America and Northern Europe, increasingly view electric heat tracing as an essential winterization tool to shield domestic plumbing, driveways, and roofs from freezing conditions and ice buildup. Rising disposable incomes, growth in single-family housing, and consumer preference for comfortable, energy-efficient floor heating systems have all contributed to segment expansion. Policy drivers—such as stricter residential energy codes and high repair costs associated with burst pipes—encourage homeowners and insurers to invest in permanent freeze protection rather than rely on temporary measures. While oil & gas, power, energy & heavy industry, and water & wastewater management represent high-value, project-based opportunities, the sheer number of residential installations and ongoing replacement demand ensure that households will remain the largest and most stable end-use base for freeze protection cables during the forecast period.

Regional Insights

North America Freeze Protection Cables Market Trends

North America is a leading regional market for freeze protection cables, driven by severe winters, extensive pipeline networks, and mature regulatory frameworks that emphasize infrastructure reliability. In the United States, northern states routinely experience sub-zero temperatures, prompting widespread use of electric heat tracing for domestic water lines, municipal systems, and commercial buildings to comply with IBC, IMC, and ASHRAE 90.1 requirements for freeze protection and energy efficiency. The region hosts significant oil & gas and petrochemical operations, where electric heat tracing is critical to maintain flow assurance and prevent hydrate or wax formation in pipelines and process equipment.

Innovation in North America centers on advanced controls, digital monitoring, and high-reliability cable designs that meet IEEE 515 and IEC/IEEE 6007930 standards for both ordinary and hazardous locations. Manufacturers and engineering firms are integrating heat trace systems into broader industrial Internet of Things architectures, allowing operators to remotely monitor circuit status, energy consumption, and temperature profiles. Growing emphasis on sustainable building practices and electrification of heating is further supporting adoption of efficient self-regulating and power-limiting cables for commercial and residential applications.

Europe Freeze Protection Cables Market Trends

Europe constitutes another major market, underpinned by cold climates in Nordic countries, Germany, and parts of Central and Eastern Europe, as well as stringent building and energy regulations. European building codes, including EN 12828 and various national regulations, mandate adequate insulation and thermal protection of pipework in buildings, fostering systematic use of heat tracing to prevent frozen pipes and to meet conservation of fuel and power objectives. Countries such as Germany and the U.K. are noted as early adopters of freeze protection heating cables across residential and commercial buildings, combining pipe insulation with electric tracing to safeguard water services and roofs.

In industrial contexts, European chemical, food processing, and pharmaceutical plants widely deploy mineral-insulated and parallel constant wattage cables for process temperature maintenance and viscosity control, often in conjunction with sophisticated control panels. Environmental policies targeting decarbonization encourage replacement of fossil-fuel-based heat maintenance with electric trace heating powered increasingly by renewable electricity.

Asia Pacific Freeze Protection Cables Market Trends

Asia Pacific is emerging as the fastest-growing regional market, supported by rapid industrialization, expanding petrochemical capacity, and infrastructure development in cold and high-altitude zones. China has significant footprints in chemicals, oil & gas pipelines, and coal-to-chemicals plants located in northern provinces where winter temperatures routinely fall well below freezing, necessitating extensive use of electric heat tracing to ensure flow assurance and process stability. Domestic manufacturers across China and India are increasingly capable of producing self-regulating and constant wattage cables, reducing costs and encouraging adoption in power plants, refineries, and municipal networks.

In Japan, strong focus on reliability and safety in nuclear and conventional power stations drives demand for high-quality mineral-insulated and series constant watt cables with proven performance and rigorous certification. Meanwhile, colder regions of India and high-elevation areas in South Asia and ASEAN are beginning to deploy heat tracing for water and wastewater systems to avoid service disruptions during winter snaps, especially in rapidly urbanizing cities. The region also benefits from cost-competitive manufacturing for global suppliers, making Asia Pacific an important production hub for freeze protection cables exported to North America and Europe.

Competitive Landscape

Market Structure Analysis

The Freeze Protection Cables Market is moderately fragmented, with a mix of global electrical and industrial technology companies and specialized heat tracing manufacturers. No single company holds an overwhelming share, but established players leverage strong brand recognition, engineering expertise, and long-standing relationships with EPC contractors and end users.

Competitive differentiation centers on cable technology breadth (self-regulating, constant wattage, mineral-insulated, skin-effect), compliance with international standards, project engineering capabilities, and lifecycle services such as commissioning and maintenance. Leading companies increasingly offer integrated solutions that combine cables, controllers, monitoring software, and turnkey installation, moving toward subscription and service-based models rather than pure product sales.

Key Market Developments

- In February 2024, Thermon announced new digital heat trace control platforms featuring advanced energy-management algorithms and cloud-based dashboards, enabling industrial customers to optimize freeze protection energy use and streamline compliance reporting across multi-site operations.

- In July 2024, Tempsens highlighted smart self-regulating heat tracing solutions for oil & gas pipelines, emphasizing energy conservation, remote monitoring, and integration with SCADA systems to maintain flow assurance in harsh climates while reducing operational costs.

Companies Covered in Freeze Protection Cables Market

- 3M

- Bartec

- Briskheat Corporation

- Chromalox Inc.

- Danfoss

- Drexan Energy Systems

- eltherm GmbH

- Emerson Electric Co

- Heat Trace Products LLC

- Parker-Hannifin

- Others Key Players

Frequently Asked Questions

The global Freeze Protection Cables Market is projected to reach US$ 2.4 Billion by 2033, increasing from US$ 1.6 Billion in 2026 at a forecast CAGR of 6.3%, driven by infrastructure winterization and industrial process requirements.

Core demand drivers include more frequent extreme cold events, stricter building and energy codes, expansion of oil & gas and chemical pipelines in cold regions, and the need to prevent pipe bursts, flow blockages, and downtime through reliable electric heat tracing.

Self‑Regulating cables lead the product mix with an estimated 38% share, favored for their automatic output adjustment, safety against overheating, energy efficiency, and simplified installation across residential and commercial freeze protection applications.

North America dominates the market due to harsh winter climates, extensive pipeline and industrial infrastructure, and comprehensive standards such as IEEE 515, IBC, and ASHRAE 90.1 that actively require or encourage electric heat tracing for freeze protection.

Key players include 3M, Bartec, Briskheat Corporation, Chromalox Inc., Danfoss, Drexan Energy Systems, eltherm GmbH, Emerson Electric Co, Heat Trace Products LLC, Parker‑Hannifin.