- HVAC

- Blast Chiller and Freezer Market

Blast Chiller and Freezer Market Size, Share, and Growth Forecast, 2026 – 2033

Blast Chiller and Freezer Market by Capacity (Small, Medium, Large), Application (Food Service, Bakery, Confectionery, Retail), End-User (Restaurants, Hotels, Catering Services, Supermarkets), and Regional Analysis for 2026-2033

Blast Chiller and Freezer Market Share and Trends Analysis

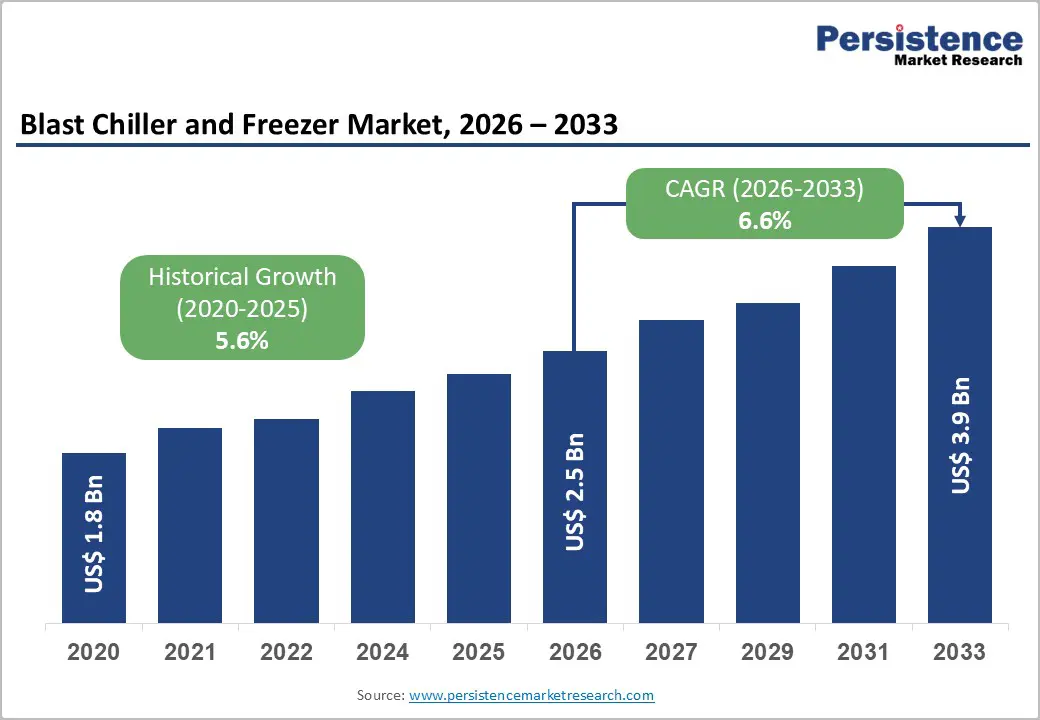

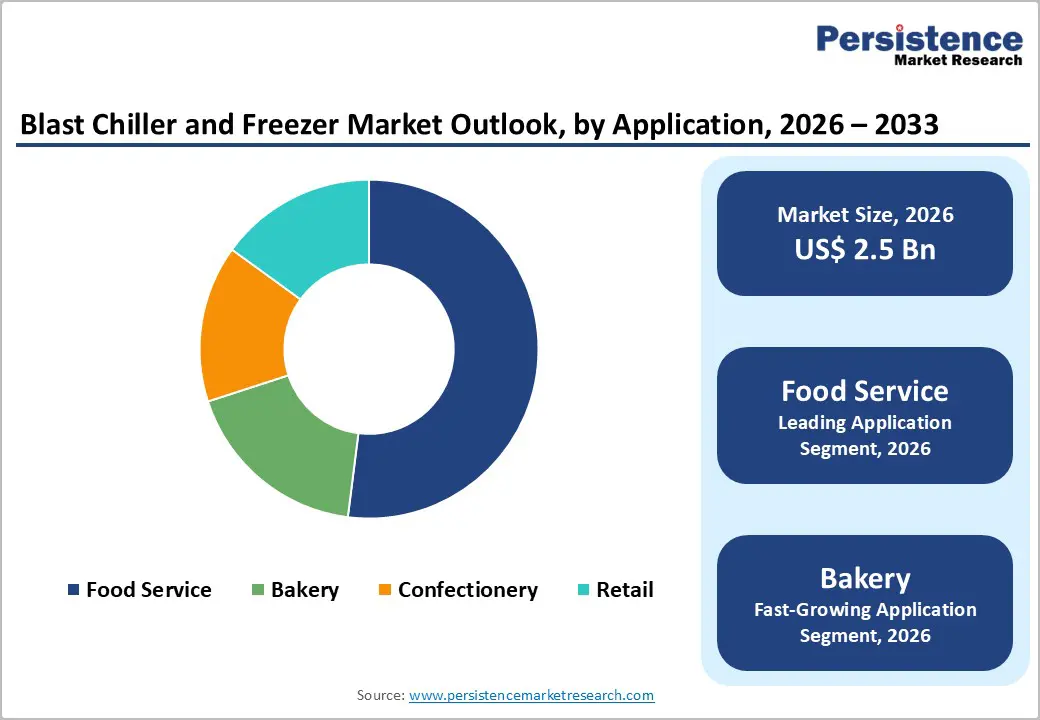

The global blast chiller and freezer market size is likely to be valued at US$ 2.5 billion in 2026, and is projected to reach US$ 3.9 billion by 2033, growing at a CAGR of 6.6% during the forecast period 2026−2033. Market expansion reflects sustained growth driven by rising demand across the commercial foodservice, retail, and industrial food-preservation sectors.

Rapid urbanization and expansion of organized food retail chains are increasing demand for efficient chilling and freezing solutions that enhance food safety and extend shelf life. Regulatory emphasis on food hygiene and stringent standards in developed and emerging markets continues to support new installations and equipment replacement cycles. Technological advancements in energy efficiency, digital control, and IoT integration are improving product performance and operational cost metrics.

Key Industry Highlights

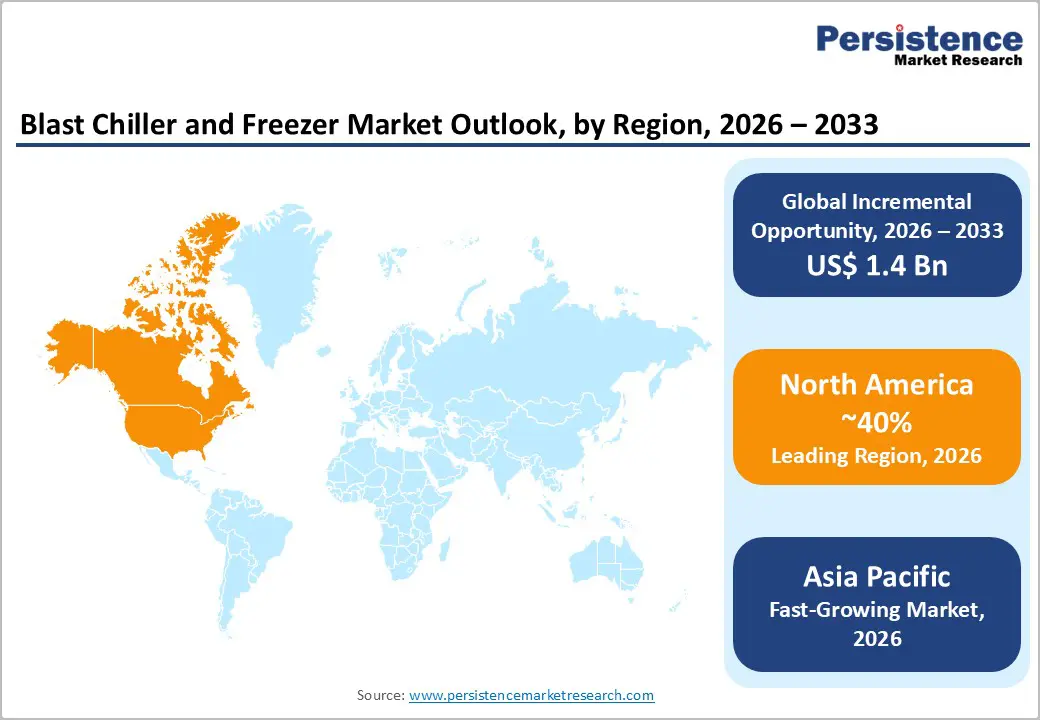

- Dominant Region: North America is expected to lead in 2026 with around 40% share, driven by strong foodservice infrastructure and strict food safety regulations.

- Fastest-growing Market: Asia Pacific is set to be the fastest-growing market through 2033, driven by rapidly growing demand for processed and ready-to-eat foods.

- Leading Application: Food service is expected to account for around 52% of revenue in 2026, supported by strict adherence to Hazard Analysis and Critical Control Points (HACCP) food safety standards.

- Fastest-growing Application: Bakery is set to be the fastest-growing segment through 2033, fueled by rising demand for artisan breads and pastries and the expansion of retail and specialty bakery networks.

- March 2025: Blue Star launched a commercial refrigeration lineup, including deep freezers that reach -26°C, using eco-friendly technology to meet rising demand in quick-service restaurants (QSRs), hospitality, and food processing.

| Key Insights | Details |

|---|---|

| Blast Chiller and Freezer Market Size (2026E) | US$ 2.6 Bn |

| Market Value Forecast (2033F) | US$ 3.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Stringency of Food Safety Regulations

Stringent food safety regulations act as a critical growth driver by establishing mandatory standards for the storage and handling of perishable products. Compliance with these standards requires precise temperature control to prevent microbial growth, spoilage, and nutrient degradation. Businesses across foodservice, retail, and industrial sectors are compelled to adopt advanced chilling and freezing solutions to meet inspection criteria and avoid legal penalties. Regulatory frameworks incentivize replacing outdated equipment with high-performance units that maintain consistent cooling, reduce contamination risks, and extend product shelf life.

The regulatory landscape also stimulates innovation in equipment design, encouraging the integration of energy-efficient systems, digital monitoring, and automated temperature controls. These features support traceability, reporting compliance, and proactive quality management, aligning operational performance with statutory requirements. In regions where inspections are frequent and penalties severe, businesses prioritize installation of reliable, standardized chilling and freezing systems to safeguard brand reputation and consumer trust. The focus on food safety creates a continuous demand cycle for modernized equipment, driving both initial adoption and subsequent upgrades.

High Initial Capital Investment

High initial capital investment acts as a critical barrier in adopting advanced chilling and freezing equipment due to the substantial upfront cost of procurement, installation, and integration. These systems require precision engineering, specialized components, and compliance with stringent safety and hygiene standards, which collectively drive up the purchase price. For small and medium-scale foodservice operators or retail chains, allocating large capital for a single equipment category can strain financial resources, forcing decision-makers to prioritize operational expenses or invest in lower-cost alternatives.

The long-term financial commitment extends beyond purchase, encompassing energy consumption, maintenance, and potential technological upgrades. Advanced features such as digital controls, IoT connectivity, and energy optimization enhance operational efficiency but increase total cost of ownership. Organizations with tight budgets or high equipment turnover may delay investment to avoid depreciation risk and ensure better alignment with business cash flows. Procurement decisions often involve multi-stakeholder approvals and risk assessments, elongating the adoption cycle.

Growing Adoption of Energy-Efficient and Smart Technologies

The widening deployment of energy-efficient and smart technologies across industries can create transformative opportunities for this market, driven by operational cost optimization and sustainability imperatives. Commercial and industrial food operations face mounting pressure to reduce energy consumption, as refrigeration accounts for a significant portion of facility energy costs. Advanced systems with intelligent temperature management, adaptive cooling cycles, and predictive maintenance capabilities enable precise control over energy usage while maintaining consistent product quality. Integration of digital monitoring tools allows real-time tracking of performance metrics, minimizing wastage and improving efficiency of resource allocation.

Smart technologies also enhance operational agility and decision-making capabilities. IoT-enabled devices and automated controls provide actionable insights into equipment performance, allowing rapid response to fluctuations in demand and load. For instance, in March 2025, Traulsen's Dynamic Response Refrigeration™ (DRR) with Smart Control™ won the 2025 Kitchen Innovations Award for advancing efficiency and food safety in foodservice refrigeration. Data-driven analytics support predictive inventory management and reduce spoilage, contributing to cost savings and improved customer satisfaction. Remote monitoring and system connectivity facilitate centralized management of multiple locations, creating operational scalability without proportional increases in staffing or maintenance.

Category-wise Analysis

Capacity Insights

Large capacity blast chillers and freezers are expected to maintain a leading position in the market, with a projected revenue share of 44% in 2026. Their widespread deployment in high-volume kitchens, industrial food processing environments, and large retail cold storage facilities has been driven by the need for scalable throughput and consistent product quality. These units have consistently delivered operational benefits such as reduced handling time, optimized workflow, and compliance with stringent hygiene and safety standards, making them essential for institutional users managing bulk operations efficiently.

Medium capacity blast chillers and freezers are anticipated to experience the fastest growth between 2026 and 2033, as their flexibility suits the needs of mid-sized restaurants, hotel kitchens, and multi-concept foodservice operations. These units provide effective chilling and freezing capabilities without the high capital expenditure or extensive space requirements associated with larger systems. Their adoption is further supported by the rise of hybrid foodservice formats and new dining concepts, which require adaptable solutions to accommodate fluctuating production volumes and evolving customer demands.

Application Insights

The food service segment is projected to account for around 52% of the blast chiller and freezer market revenue share by 2026, supported by high-volume restaurants and institutional kitchens that require reliable preservation of prepared foods to protect quality and margins. Strong adherence to HACCP standards has been enhancing adoption, since operators have been using compliant systems to reduce food safety risks and strengthen audit readiness. Rapid chilling and freezing capabilities have minimized spoilage, improved inventory turns, and reduced waste, enabling larger operations to maintain product consistency while controlling labor and energy costs.

The bakery category is expected to be the fastest-growing application between 2026 and 2033, as demand for artisan breads, pastries, and specialty baked goods has been increasing alongside rising global baking output. Preservation of yeast-based dough and rapid chilling of finished items require specialized equipment that maintains precise temperature and humidity conditions to extend shelf life without compromising texture or taste. Both small craft bakeries and large industrial facilities have been adopting these systems to optimize production schedules, smooth out batch variability, and reduce write-offs from overproduction or quality defects. Growth in this segment has been further supported by evolving consumer preferences, the expansion of retail and specialty bakery networks, and a stronger focus on consistent, documented processes that meet stringent food safety and brand standards across jurisdictions.

End-User Insights

Restaurants are projected to command about 40% of revenue share in 2026, as high-volume kitchens have relied on predictable soft and hard chill cycles that align with U.S. Food and Drug Administration (FDA) guidance. Daily prep and service flows have been requiring dependable, repeatable performance to protect sensory consistency, limit spoilage, and keep stations moving without bottlenecks. Rapid chilling of mise en place and finished items has been supporting tighter inventory control while helping teams reduce rework, shorten handling steps, and maintain compliance with food safety expectations. To strengthen results, restaurant leaders are increasingly mapping chill capacity to peak-hour demand, menu complexity, and batch sizes so equipment selection has been matching throughput targets rather than only floor-space constraints.

Catering services are set to be the fastest-growing application through 2033, as the events economy continues to expand across formats such as corporate meetings, weddings, and large public gatherings. Catering teams have been needing flexible and transport-friendly chilling and freezing solutions that preserve quality during staging, delivery, and on-site service. Purpose-built equipment has enabled safe holding of perishable components, parallel production of multiple menus, and quick scaling for variable headcount. As demand for safe, punctual delivery has risen in urban and emerging markets, caterers standardizing pack-out procedures, temperature checks, and loading sequences will improve consistency and reduce risk during transit.

Regional Insights

North America Blast Chiller and Freezer Market Trends

North America is expected to dominate with an estimated 40% of the blast chiller and freezer market share in 2026, reflecting its strong presence of large-scale foodservice chains, industrial food processors, and advanced cold chain infrastructure that drives adoption of high-capacity and technologically advanced chilling solutions. The dominance stems from operational scale and regulatory rigor. High-volume commercial kitchens, institutional caterers, and food manufacturing plants require equipment capable of handling significant throughput while ensuring precise temperature control to maintain food safety and quality. Strict adherence to the United States Department of Agriculture (USDA) and the FDA guidelines sustains demand for reliable systems.

The strategic advantage also lies in early adoption of energy-efficient and smart technologies, which provides a competitive edge over competitors elsewhere. Operators prioritize solutions with the IoT-enabled monitoring, adaptive cooling cycles, and energy optimization features to manage operational costs and environmental impact. Rising consumer demand for fresh, ready-to-eat meals and low-waste solutions drives investments in medium- and large-capacity units that balance flexibility with scalability. Urbanization, high disposable income, and growth of multi-concept kitchens further reinforce market penetration. The presence of leading global equipment manufacturers ensures rapid technology deployment and after-sales support, creating barriers to entry for emerging competitors.

Europe Blast Chiller and Freezer Market Trends

Europe occupies a strong position in the market for blast chillers and freezers owing to operators having consistently prioritized food quality preservation, regulatory discipline, and broad deployment across professional kitchens and food manufacturing sites. The region has been placing sustained emphasis on food traceability and rigorous hygiene compliance, which has encouraged frequent replacement cycles and well-timed upgrades. Demand has also been supported by the high density of specialty outlets such as bakeries, patisseries, delicatessens, and premium foodservice venues that have required precision cooling to protect texture, flavor, and nutritional integrity. From a planning perspective, buyers have increasingly benefited from aligning equipment specifications with menu mix, batch size variability, and verification needs under HACCP.

Regional market growth is accelerating as investments shift toward energy-efficient and environmentally compliant platforms that have aligned with sustainability targets across the European Union (EU). Operators are prioritizing lower power consumption, natural refrigerant readiness, and connected digital controls that are enabling condition monitoring, predictive servicing, and clearer key performance indicator (KPI) reporting. Medium-capacity adoption has been rising in institutional catering, healthcare foodservice, and airline catering, where consistency and uptime have outweighed aggressive capacity expansion. By 2033, refurbishment programs across Southern and Eastern Europe will have created steady incremental demand, especially where modernized infrastructure has been improving reliability and reducing total cost of ownership (TCO) across multi-site operations.

Asia Pacific Blast Chiller and Freezer Market Trends

Asia Pacific is projected to emerge as the fastest-growing market for blast chillers and freezers during the 2026–2033 forecast period, supported by rapid urbanization, expansion of organized food retail chains, and rising demand for processed and ready-to-eat foods. Growth in hotel kitchens, quick-service restaurants, and institutional catering operations is creating strong demand for medium- and large-capacity chilling and freezing solutions that offer efficiency without large capital or space requirements. Increasing focus on food safety, hygiene, and quality preservation, along with adoption of digital monitoring and Internet of Things-enabled systems, is driving operators to modernize facilities and optimize workflow across production and storage operations.

The growth trajectory is further accelerated by the rise of multi-concept kitchens, artisanal bakeries, and small- to mid-sized food manufacturers that require flexible, energy-efficient equipment to maintain freshness and extend shelf life. Governments and local authorities are supporting infrastructure upgrades in cold chain logistics, enabling efficient transportation and storage of perishable goods across urban and semi-urban markets. Rising disposable incomes and evolving consumer preferences for premium and ready-to-eat foods are expanding the customer base, encouraging adoption of smart technologies for rapid chilling, freezing, and inventory management.

Competitive Landscape

The global blast chillers and freezers market features a moderately consolidated structure, with a limited number of established manufacturers commanding strong brand recognition and extensive distribution networks. Leading players such as GEA Group, Carrier, MAYEKAWA Manufacturing, ALFA LAVAL, and Sammic have built durable relationships with foodservice chains, industrial food processors, and institutional buyers, which has enabled them to secure consistent order volumes and repeat installations. These longstanding partnerships have been providing manufacturers with insights into evolving operational needs, allowing them to refine product portfolios and service models that address real-world challenges such as uptime requirements, space constraints, and lifecycle costs. Buyers working with these established suppliers have been benefiting from proven service networks, readily available replacement parts, and technical support that minimizes downtime across critical production environments.

Competitive dynamics have been shifting toward product differentiation rather than pricing alone, as operators have increasingly prioritized total value over initial capital outlay. Leading manufacturers are focusing on improving energy efficiency, expanding capacity ranges, and integrating advanced digital controls to enhance both performance and reliability. Smart features such as automated temperature management, real-time monitoring systems, and predictive maintenance capabilities have been strengthening value propositions for high-volume operators who require seamless integration with enterprise resource planning and facility management platforms

Key Industry Developments

- In November 2025, MEDLOG opened a 300,000 sq. ft. cold chain facility near Savannah Port, Georgia, featuring the largest U.S. blast freezing capacity to process up to 3 million pounds of protein daily. The site offers 20,000 pallet positions, multimodal access, and will create over 100 jobs with a US$ 65 million economic impact.

- In August 2025, Everidge launched Cool on the Move, a next-generation mobile cold storage solution with dual cooler/freezer modes and plug-and-play convenience designed to support foodservice, healthcare, education, and emergency response applications.

- In July 2025, Irinox introduced MultiFresh® Next XL-XXL, the first multifunction roll-in blast chiller with built-in unit, offering greater chilling speed, lower energy use, and zero environmental impact. It supports sustainable, powerful trolley-based chilling for professional kitchens.

Companies Covered in Blast Chiller and Freezer Market

- GEA Group Aktiengesellschaft

- Carrier.

- MAYEKAWA MFG. CO., LTD.

- ALFA LAVAL

- Sammic S.L.

- Air Products and Chemicals, Inc.

- Cold Jet

- Ali Group Worldwide

- Traulsen

Frequently Asked Questions

The global blast chiller and freezer market is projected to reach US$ 2.5 billion in 2026.

Rising demand for food safety compliance, reduction of food waste, expansion of organized foodservice and cold chain infrastructure, and adoption of energy-efficient and smart refrigeration technologies drive the market.

The market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Key market opportunities include adoption of energy-efficient and smart technologies, expansion of organized foodservice and cold chain infrastructure in emerging economies, and rising demand from bakeries, catering services, and multi-concept kitchens.

Key players in the Blast Chiller and Freezer market include GEA Group Aktiengesellschaft, Carrier, MAYEKAWA MFG. CO., LTD., and ALFA LAVAL.