- Executive Summary

- Global Foodservice Paper Bags Market Snapshot, 2025 and 2032

- Market Opportunity Assessment, 2025 - 2032, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Product Lifecycle Analysis

- Foodservice Paper Bags Market: Value Chain

- List of Raw Material Suppliers

- List of Manufacturers

- List of Distributors

- Profitability Analysis

- Forecast Factors - Relevance and Impact

- Covid-19 Impact Assessment

- PESTLE Analysis

- Porter Five Force’s Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Material Type Landscape

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- Global Parent Market Overview

- Price Trend Analysis, 2019 - 2032

- Key Highlights

- Key Factors Impacting Product Prices

- Prices By Product Type/Composition/Material Type

- Regional Prices and Product Preferences

- Global Foodservice Paper Bags Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Market Size and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast

- Historical Market Size Analysis, 2019-2024

- Current Market Size Forecast, 2025-2032

- Global Foodservice Paper Bags Market Outlook: Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Product Type, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Product Type, 2025 - 2032

- Flat Paper Bags

- Satchel Paper Bags

- Self-Opening Square (SOS) Paper Bags

- Pinch Bottom Bags

- Twist Handle Bags

- Die Cut Handle Bags

- Others

- Market Attractiveness Analysis: Product Type

- Global Foodservice Paper Bags Market Outlook: Material Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Material Type, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Material Type, 2025 - 2032

- Kraft Paper

- Recycled Paper

- Virgin Fiber Paper

- Others

- Market Attractiveness Analysis: Material Type

- Global Foodservice Paper Bags Market Outlook: Capacity

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Capacity, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Capacity, 2025 - 2032

- Up to 2 lbs

- 2-6 lbs

- 6-11 lbs

- Above 11 lbs

- Global Foodservice Paper Bags Market Outlook: Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Application, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Application, 2025 - 2032

- Bakery & Confectionery

- Quick Service Restaurants (QSRs)

- Cafes & Coffee Shops

- Catering Services

- Hotels & Restaurants

- Institutional Foodservice

- Food Delivery & Takeaway Services

- Others

- Market Attractiveness Analysis: Application

- Key Highlights

- Global Foodservice Paper Bags Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Region, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Region, 2025 - 2032

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Foodservice Paper Bags Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Market, 2019 - 2024

- By Country

- By Product Type

- By Material Type

- By Capacity

- By Application

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Country, 2025 - 2032

- U.S.

- Canada

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Product Type, 2025 - 2032

- Flat Paper Bags

- Satchel Paper Bags

- Self-Opening Square (SOS) Paper Bags

- Pinch Bottom Bags

- Twist Handle Bags

- Die Cut Handle Bags

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Material Type, 2025 - 2032

- Kraft Paper

- Recycled Paper

- Virgin Fiber Paper

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Capacity, 2025 - 2032

- Up to 2 lbs

- 2-6 lbs

- 6-11 lbs

- Above 11 lbs

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By End-User, 2025 - 2032

- Bakery & Confectionery

- Quick Service Restaurants (QSRs)

- Cafes & Coffee Shops

- Catering Services

- Hotels & Restaurants

- Institutional Foodservice

- Food Delivery & Takeaway Services

- Others

- Market Attractiveness Analysis

- Europe Foodservice Paper Bags Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Market, 2019 - 2024

- By Country

- By Product Type

- By Material Type

- By Capacity

- By Application

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Country, 2025 - 2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Product Type, 2025 - 2032

- Flat Paper Bags

- Satchel Paper Bags

- Self-Opening Square (SOS) Paper Bags

- Pinch Bottom Bags

- Twist Handle Bags

- Die Cut Handle Bags

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Material Type, 2025 - 2032

- Kraft Paper

- Recycled Paper

- Virgin Fiber Paper

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Capacity, 2025 - 2032

- Up to 2 lbs

- 2-6 lbs

- 6-11 lbs

- Above 11 lbs

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By End-User, 2025 - 2032

- Bakery & Confectionery

- Quick Service Restaurants (QSRs)

- Cafes & Coffee Shops

- Catering Services

- Hotels & Restaurants

- Institutional Foodservice

- Food Delivery & Takeaway Services

- Others

- Market Attractiveness Analysis

- East Asia Foodservice Paper Bags Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Market, 2019 - 2024

- By Country

- By Product Type

- By Material Type

- By Capacity

- By Application

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Country, 2025 - 2032

- China

- Japan

- South Korea

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Product Type, 2025 - 2032

- Flat Paper Bags

- Satchel Paper Bags

- Self-Opening Square (SOS) Paper Bags

- Pinch Bottom Bags

- Twist Handle Bags

- Die Cut Handle Bags

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Material Type, 2025 - 2032

- Kraft Paper

- Recycled Paper

- Virgin Fiber Paper

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Capacity, 2025 - 2032

- Up to 2 lbs

- 2-6 lbs

- 6-11 lbs

- Above 11 lbs

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By End-User, 2025 - 2032

- Bakery & Confectionery

- Quick Service Restaurants (QSRs)

- Cafes & Coffee Shops

- Catering Services

- Hotels & Restaurants

- Institutional Foodservice

- Food Delivery & Takeaway Services

- Others

- Market Attractiveness Analysis

- South Asia & Oceania Foodservice Paper Bags Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Market, 2019 - 2024

- By Country

- By Product Type

- By Material Type

- By Capacity

- By Application

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Country, 2025 - 2032

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Product Type, 2025 - 2032

- Flat Paper Bags

- Satchel Paper Bags

- Self-Opening Square (SOS) Paper Bags

- Pinch Bottom Bags

- Twist Handle Bags

- Die Cut Handle Bags

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Material Type, 2025 - 2032

- Kraft Paper

- Recycled Paper

- Virgin Fiber Paper

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Capacity, 2025 - 2032

- Up to 2 lbs

- 2-6 lbs

- 6-11 lbs

- Above 11 lbs

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By End-User, 2025 - 2032

- Bakery & Confectionery

- Quick Service Restaurants (QSRs)

- Cafes & Coffee Shops

- Catering Services

- Hotels & Restaurants

- Institutional Foodservice

- Food Delivery & Takeaway Services

- Others

- Market Attractiveness Analysis

- Latin America Foodservice Paper Bags Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Market, 2019 - 2024

- By Country

- By Product Type

- By Material Type

- By Capacity

- By Application

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Country, 2025 - 2032

- Brazil

- Mexico

- Rest of LATAM

- Southeast Asia

- ANZ

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Product Type, 2025 - 2032

- Flat Paper Bags

- Satchel Paper Bags

- Self-Opening Square (SOS) Paper Bags

- Pinch Bottom Bags

- Twist Handle Bags

- Die Cut Handle Bags

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Material Type, 2025 - 2032

- Kraft Paper

- Recycled Paper

- Virgin Fiber Paper

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Capacity, 2025 - 2032

- Up to 2 lbs

- 2-6 lbs

- 6-11 lbs

- Above 11 lbs

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By End-User, 2025 - 2032

- Bakery & Confectionery

- Quick Service Restaurants (QSRs)

- Cafes & Coffee Shops

- Catering Services

- Hotels & Restaurants

- Institutional Foodservice

- Food Delivery & Takeaway Services

- Others

- Market Attractiveness Analysis

- Middle East & Africa Foodservice Paper Bags Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis By Market, 2019 - 2024

- By Country

- By Product Type

- By Material Type

- By Capacity

- By Application

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Country, 2025 - 2032

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Product Type, 2025 - 2032

- Flat Paper Bags

- Satchel Paper Bags

- Self-Opening Square (SOS) Paper Bags

- Pinch Bottom Bags

- Twist Handle Bags

- Die Cut Handle Bags

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Material Type, 2025 - 2032

- Kraft Paper

- Recycled Paper

- Virgin Fiber Paper

- Others

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By Capacity, 2025 - 2032

- Up to 2 lbs

- 2-6 lbs

- 6-11 lbs

- Above 11 lbs

- Current Market Size (US$ Bn) and Volume (Tons) Forecast By End-User, 2025 - 2032

- Bakery & Confectionery

- Quick Service Restaurants (QSRs)

- Cafes & Coffee Shops

- Catering Services

- Hotels & Restaurants

- Institutional Foodservice

- Food Delivery & Takeaway Services

- Others

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Apparent Production Capacity

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Mondi Group

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- International Paper

- Oji Holdings Corporation

- Smurfit Kappa

- Stora Enso

- DS Smith

- Novolex

- Wisconsin Converting Inc.

- Papier-Mettler

- Paperbags Ltd

- Welton Bibby & Baron

- York Paper Company Ltd

- Langston Companies, Inc.

- Baginco International

- ProAmpac

- Mondi Group

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Smart Packaging

- Foodservice Paper Bags Market

Foodservice Paper Bags Market Size, Share, and Growth Forecast, 2025 - 2032

Foodservice Paper Bags Market by Product Type (Flat Paper Bags, Satchel Paper Bags, Self-Opening Square (SOS) Paper Bags, Pinch Bottom Bags, Twist Handle Bags, Die Cut Handle Bags, Others), Material Type (Kraft Paper, Recycled Paper, Virgin Fiber Paper, Others), Application, and Regional Analysis for 2025 - 2032

Key Industry Highlights

- Dominant Region: Asia Pacific dominates the foodservice paper bags market with an estimated 30% share in 2025, underpinned by China’s massive foodservice sector and strong plastic-reduction policies.

- Leading Material Type: Kraft paper maintains leadership due to its superior tear resistance, grease barrier performance, and established global manufacturing base.

- Dominant Product Type: The SOS segment leads globally, driven by operational efficiency, compatibility with automation, and widespread use in bakery, QSR, and institutional foodservice applications.

- Key Trend: Rising consumer environmental awareness and sustainability-led brand transitions by major QSRs such as Starbucks and KFC are strengthening the demand for recyclable paper packaging.

- Market Opportunity: Surging meal delivery transactions across the Asia Pacific are creating exponential demand for single-use paper bags to support fast-scaling delivery ecosystems.

| Key Insights | Details |

|---|---|

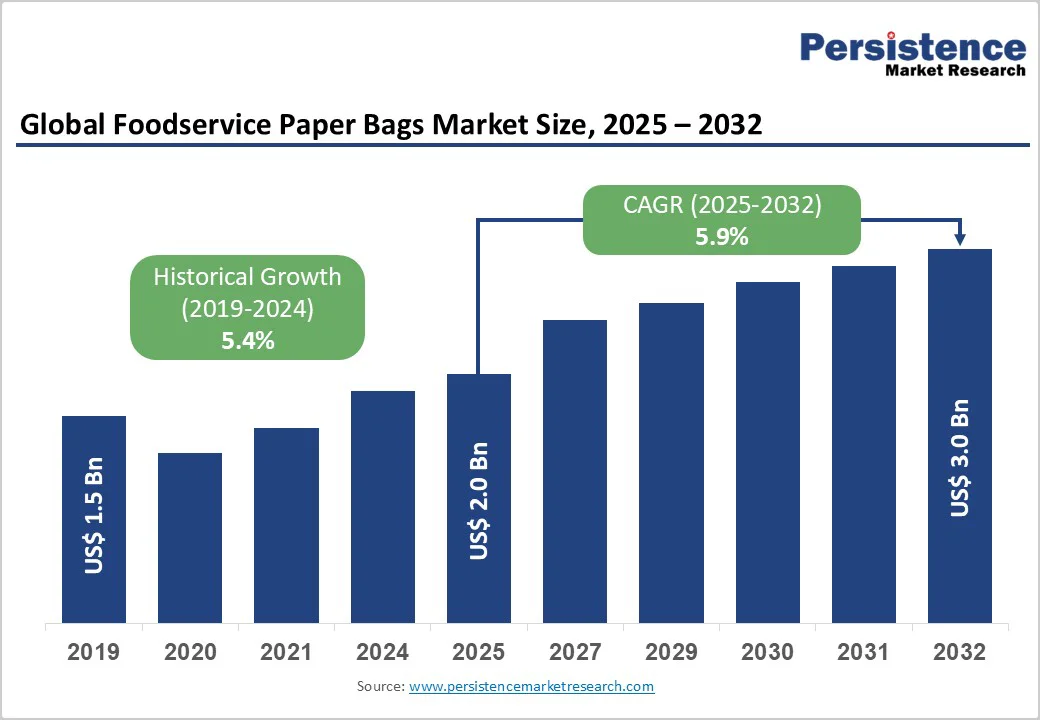

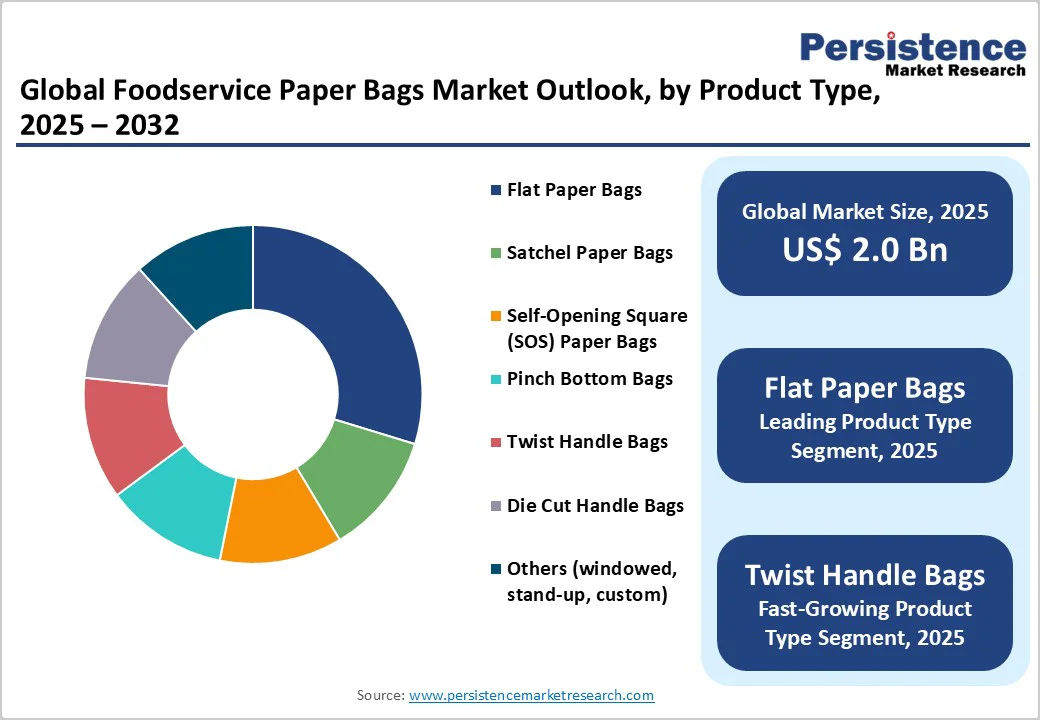

| Foodservice Paper Bags Market Size (2025E) | US$2.0 Bn |

| Market Value Forecast (2032F) | US$3.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Government Regulations and Plastic Bans Driving Substitution Demand

Regulatory prohibitions on single-use plastics are the most significant structural catalysts driving growth in the foodservice paper bags market. For instance, the European Union (EU)'s Packaging and Packaging Waste Regulation (PPWR), effective August 12, 2026, mandates full recyclability of all packaging by 2030 and explicitly bans single-use plastic packaging for fresh fruit and vegetables weighing less than 1.5 kilograms.

Similarly, California's amended SB 1046 restricts the distribution of non-compostable pre-checkout bags effective January 2025. These regulatory mechanisms actively transfer packaging selection authority from business discretion toward legal mandate, creating structural substitution demand independent of consumer preference or cost-benefit calculations.

Consumer preference for sustainable packaging has evolved from a discretionary choice into a core purchasing determinant. A comprehensive survey by Japan's Consumer Affairs Agency found that 76% of Japanese consumers actively select restaurants that prioritize sustainable packaging, with 82% explicitly favoring paper-based alternatives over plastic.

South Korea's Ministry of Environment recorded a surge in customer preference for eco-friendly packaging, from 52% in 2020 to 71% in 2023. These behavioral indices translate into competitive differentiation mechanisms, whereby branded foodservice providers that incorporate visible sustainability attributes command premium positioning and customer retention advantages.

Raw Material Cost Volatility and Compliance Complexity

Paper bags manufacturing cost structure demonstrates heightened sensitivity to virgin fiber pulp pricing, which exhibits pronounced cyclicality driven by forestry operations, trading dynamics, and macroeconomic conditions. The cost of kraft paper, for instance, is subject to seasonal supply variations, geopolitical influences on timber sourcing, and energy-intensive production processes.

Paper manufacturing accounts for approximately 7% of global industrial energy consumption, establishing a direct correlation between petrochemical prices and input costs. European paper industry data documents total mill capacity declining from 1,570 to 861 facilities between 2000 and 2023, reflecting structural consolidation and increasing supplier concentration risk.

Manufacturers lacking integrated vertical supply chains and dependent on spot-market procurement face margin compression during cost-escalation phases, potentially constraining production capacity expansion and competitiveness against alternative packaging materials. This structural restraint will persist, particularly for smaller regional converters, potentially concentrating market consolidation among integrated producers maintaining proprietary pulp sourcing capabilities.

Rapid Foodservice Expansion in Developing Economies

The Asia Pacific foodservice industry is experiencing accelerated growth driven by rapid urbanization, expanding middle-income populations, and the proliferation of quick-service restaurant networks, thereby amplifying demand for paper bags.

India's packaging sector, constituting the fifth-largest industry globally at US$86 billion in 2024 with 22-25% annual growth, provides context for emerging market scale. Structural expansions in emerging markets can, therefore, generate volume opportunities for manufacturers establishing regional production footprints and localized supply chains, distinct from mature market saturation dynamics.

Advanced materials science developments in grease-resistant and moisture-barrier coating technologies can also enable the functional expansion of the foodservice paper bags market into previously restricted applications.

For example, water-resistant coatings made with nanofibrillated cellulose demonstrate barrier performance equivalent to that of polymer-based alternatives without compromising recyclability or biodegradability. Heat-retention technologies and tamper-evident innovations can enable diversification of applications into premium catering and specialty foodservice segments previously dominated by rigid containers.

Category-wise Analysis

Product Type Insights

Self-opening sack (SOS), expected to hold a 34% share in 2025, dominates on the basis of its structural functionality, which aligns with high-volume foodservice operations and retail automation.

This configuration enables mechanized filling operations standard in commercial bakeries, quick-service restaurant networks, and institutional foodservice environments, establishing operational necessity rather than discretionary selection. SOS formulations also provide structural rigidity without additional bracing components, supporting stacking efficiency and warehouse logistics optimization.

Twist handle bags represent an emerging growth area, driven by consumer preference for portable takeaway packaging and foodservice operators' requirements for branded, customizable designs that support customer experience differentiation. Handle-bag configurations enable convenient carry, essential for QSR drive-through operations, food delivery logistics, and consumer direct-to-home procurement.

Material Type Insights

Kraft paper formulations are likely to maintain overwhelming dominance through intrinsic technical properties that align with foodservice application requirements —superior tear resistance, load-bearing capacity, and a cost-competitive positioning relative to specialized formulations.

This paper's natural fiber structure delivers grease resistance properties essential for foodservice applications without requiring additional coating layers, reducing manufacturing complexity and waste management complications.

On the other hand, recycled paper bags are anticipated to grow at a notable pace during 2025 - 2032, on account of regulatory incentive structures, producer sustainability commitments, and cost-competitiveness advantages where suitable supply infrastructure is well-established. EU PPWR, for example, mandates minimum recycled-content requirements for plastic packaging.

Recycled paper sourced from post-consumer waste streams can also provide supply security advantages.

Application Insights

Quick-service restaurants are likely to lead the foodservice paper bags market revenue share in 2025, owing to their operational dependency on disposable packaging, high transaction velocity, and established supply chain standardization.

Major multinational QSR networks, such as McDonald's, which serves 80 million customers daily, have established baseline demand volumes, enabling manufacturing scale economics. QSR operational models emphasizing speed, consistency, and standardization mandate packaging specifications to enable mechanized filling and rapid service fulfillment.

At the same time, third-party food delivery platforms represent the fastest-growing application segment, driven by exponential adoption of delivery platforms, increased meal frequency among delivery-engaged populations, and the necessity of protective packaging inherent in multi-touch logistics networks.

Regional Insights

Asia Pacific Foodservice Paper Bags Market Trends

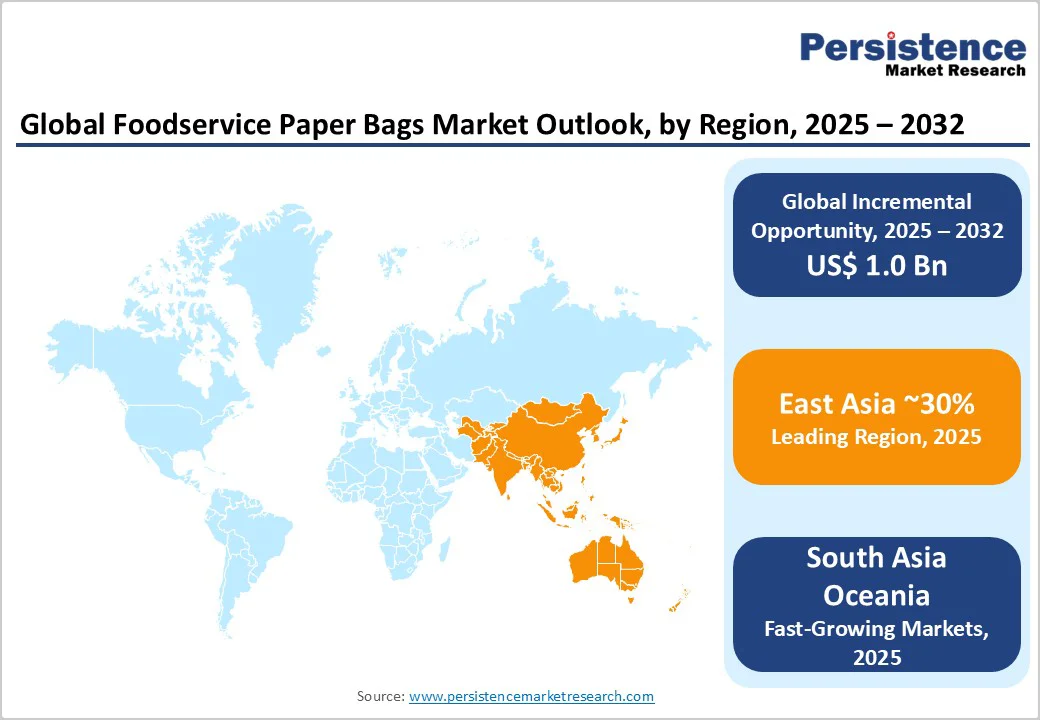

Asia Pacific is poised to dominate, holding around 30% of the foodservice paper bags market share in 2025, attributable to absolute consumption scale, driven by China's massive foodservice sector, representing 41.6% of regional consumption.

Online food delivery penetration in the region is predicted to reach the highest global density, with Chinese delivery platforms facilitating multi-billion order volumes annually, necessitating equivalent paper packaging supply expansion.

Regional government plastic-restriction policies, including major city plastic-straw/cutlery bans, have also catalyzed a significant increase in demand for paper alternatives. Supply-side dynamics have further solidified Asia Pacific as a manufacturing hub, with Shanghai's annual production capacity enabling regional export alongside domestic fulfillment.

Europe Foodservice Paper Bags Market Trends

Europe occupies a prominent position in the market, with approximately 24% share in 2025, fueled by stringent regulatory frameworks driving plastic substitution and premium pricing tolerance that enable manufacturer profitability despite competitive saturation.

The EU PPWR establishes binding recyclability mandates (100% by 2030), single-use plastic restrictions in foodservice, and reuse system requirements, creating structural demand vectors for paper-based solutions.

Germany, France, Italy, the Netherlands, and Belgium collectively account for 81.7% of the value-added contribution in the accommodation and food services sector across the EU, driven by premium foodservice consumption and higher-margin packaging specifications. Operational standardization is playing a central role in aiding market expansion in Europe.

North America Foodservice Paper Bags Market Trends

North America is projected to account for about 22% of the foodservice paper bags market share in 2025, powered by an strong QSR network, which in turn is complemented by emerging delivery platform scaling.

For example, McDonald's, which operates more than 13,000 locations across North America and serves millions of customers daily, exemplifies channel scale by establishing supply specifications and manufacturing standards. Federal and state-level plastic reduction mandates, such as California SB 1046 and Delaware’s polystyrene restrictions effective 2025, have exerted pressure on QSRs and manufacturers to transition to paper delivery bags.

Competitive Landscape

The global foodservice paper bags market structure is broadly fragmented but is still dominated by a handful of companies supplying large-volume standardized formats and barrier/functional papers. At the same time, numerous regional converters and niche suppliers serve local QSRs, bakeries and bespoke branding needs.

Leading players include Mondi Group, International Paper, Smurfit Kappa, Stora Enso, DS Smith, and Novolex, which together command significant scale in raw material supply, R&D, including barrier and recyclable solutions, and global distribution.

Smaller specialists, local bag makers and converters compete on customization, speed and price, keeping the market competitive. The result is a market where scale and sustainability credentials provide a clear advantage, yet opportunity remains for agile regional players and innovative entrants.

Key Industry Developments

- In October 2025, ProAmpac acquired International Paper’s bag converting operations, expanding its kraft paper bag portfolio. This acquisition enables ProAmpac to offer more customized packaging solutions for grocery, convenience stores, and quick-service restaurants, including handled shopping bags and self-opening sacks. The deal marks ProAmpac’s first expansion into California and complements its ongoing “fiberization” strategy to grow fiber-based packaging in diverse applications like frozen foods and to-go containers.

- In August 2025, Mondi expanded its portfolio with the launch of Functional Barrier Paper Ultimate, a recyclable high-barrier paper offering superior protection against oxygen, moisture, and grease. Designed for food items such as coffee, tea, and snacks, this innovation reflects a significant advancement in sustainable, high-performance packaging solutions relevant to the foodservice paper bags market, enabling enhanced product protection and reduced carbon footprint.

- In April 2025, Mondi and Evonik collaborated to develop a recyclable pre-made paper bag for chemical powders, specifically fumed silica. This new lightweight, two-ply paper bag eliminates a plastic-coated layer, reducing overall packaging weight by 30% and lowering the carbon footprint. Made from Mondi’s high porosity kraft paper, the bag offers superior strength and allows efficient vacuum chamber filling with secure sealing.

Companies Covered in Foodservice Paper Bags Market

- Mondi Group

- International Paper

- Oji Holdings Corporation

- Smurfit Kappa

- Stora Enso

- DS Smith

- Novolex

- Wisconsin Converting Inc.

- Papier-Mettler

- Paperbags Ltd

- Welton Bibby & Baron

- York Paper Company Ltd

- Langston Companies, Inc.

- Baginco International

- ProAmpac

Frequently Asked Questions

The global foodservice paper bags market is projected to reach US$ 2.0 billion in 2025.

Stringent plastic ban regulations, sustainability-focused consumer preferences, and expanding online food delivery networks are driving the market.

The market is poised to witness a CAGR of 5.9% from 2025 to 2032.

Key market opportunities lie in recyclable material innovation, premium customization for QSRs, and expansion across emerging food delivery ecosystems across Asia Pacific.

The leading market players are Mondi Group, International Paper, Smurfit Kappa, Stora Enso, DS Smith, and Novolex. Etc.