- Automotive

- Flex Fuel Vehicle Market

Flex Fuel Vehicle Market Size, Share, Trends, Regional Forecasts 2026 - 2033

Flex Fuel Vehicle Market Engine Type (Internal Combustion Engines, Hybrid Flex-Fuel Engines), Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles), and Regional Analysis from 2026 to 2033

Flex Fuel Vehicle Market Share and Trends Analysis

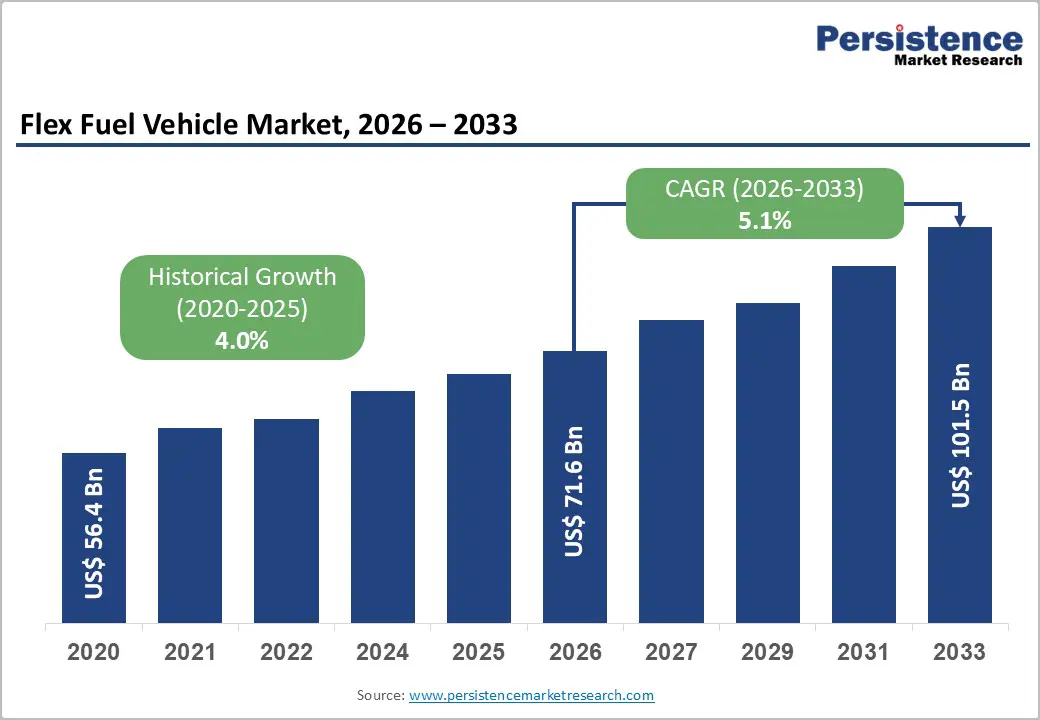

The global flex fuel vehicle market size is anticipated at US$ 71.6 billion in 2026 and is projected to reach US$ 101.5 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

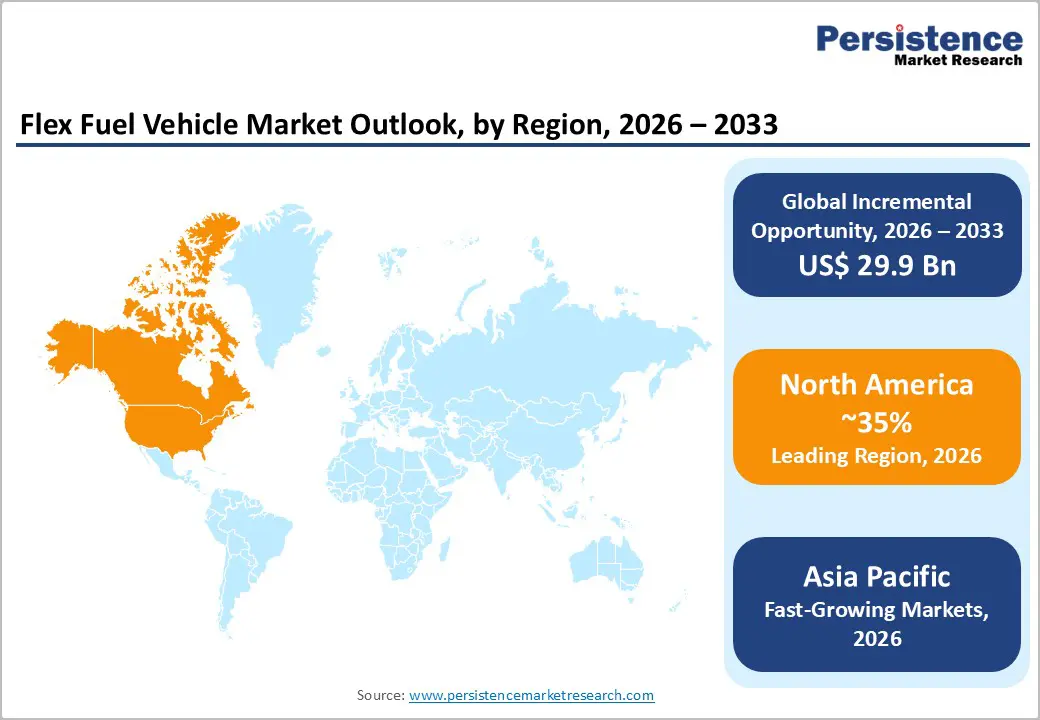

Market expansion is driven by ethanol blending mandates across the US, India, and Brazil, advancing hybrid flex fuel technologies, and rising demand for cost efficient low carbon mobility. North America holds nearly 35% market share supported by regulatory leadership and OEM investment, Europe expands at around 3.9% CAGR through policy harmonization, while Asia Pacific grows fastest at 5.6% CAGR driven by mandates and vehicle ownership growth.

Key Industry Highlights:

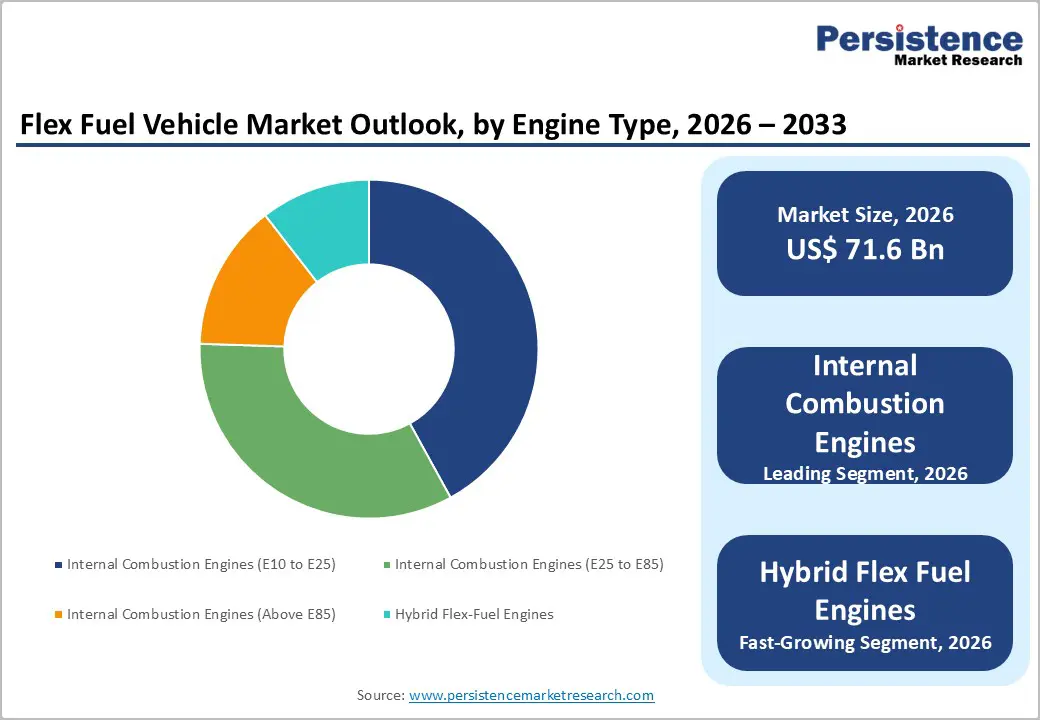

- Internal combustion engines command 89% market share with E10-E25 at ~42%, E25-E85 at 30 to 33%, and Above E85 as a rest in ICE, while Hybrid flex-fuel engines expand at 8.1% CAGR supporting emerging electric-hybrid convergence.

- Passenger vehicles lead at 68% market share, while Light commercial vehicles expand at 4.8% CAGR, supporting fleet modernization and cost-effective commercial transportation adoption.

- North America maintains 35% market dominance with regulatory leadership and OEM concentration, Europe expands at 3.9% CAGR with sustainability emphasis, and Asia Pacific expands at 5.6% CAGR with India E20 mandate and Brazil's 80%+ flex-fuel adoption.

- Latin America and the Middle East & Africa are emerging as impactful markets, driven by Brazil’s mature 80%+ flex-fuel adoption, growing ethanol infrastructure, and government incentives, creating significant regional demand and investment opportunities.

- Toyota unveils world's first fully ethanol-powered HyCross, Volkswagen launches South American FFV product offensive, and Japanese automaker partners with AI provider for smart fuel optimization demonstrating technology advancement and regional market expansion momentum.

| Key Insights | Details |

|---|---|

| Flex Fuel Vehicle Market Size (2026E) | US$ 71.6 billion |

| Market Value Forecast (2033F) | US$ 101.5 billion |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.0% |

Market Dynamics Analysis

Drivers - Government Regulatory Mandates and Ethanol Blending Requirements Supporting Market Expansion

Government regulatory mandates and ethanol blending requirements are systematically accelerating flex fuel vehicle adoption worldwide, led by the US EPA Renewable Fuel Standard mandating 15 billion gallons of ethanol blending annually and enforcing strict RFS compliance requirements for refiners and automakers. India’s mandatory E20 fuel compatibility policy, effective April 2023, compels OEMs to align new vehicle platforms with higher ethanol blends while supporting domestic biofuel supply chains. Brazil’s decades long ethanol blending policy continues to sustain over 80% flex fuel penetration in new passenger vehicles. Meanwhile, the EU Renewable Energy Directive, supported by incentive programs, regulatory compliance deadlines, and long term policy frameworks, strengthens investment certainty, enabling OEM product planning, infrastructure development, and sustained consumer adoption across automotive markets.

Hybrid Flex-Fuel Engine Technology Innovation and Environmental Consciousness

Hybrid flex fuel engine innovation and rising environmental consciousness are systematically expanding market adoption, as automakers integrate hybrid electric systems with flex fuel capability to deliver extended driving range alongside measurable emissions reduction. Plug-in Hybrid Electric Flex Fuel Vehicles demonstrate approximately 38% lifecycle greenhouse gas savings on E85 compared to gasoline, while advanced low-carbon ethanol pathways unlock up to 77% total GHG reduction potential. Improved hybrid engine efficiency, electric-only range extension, and optimized fuel blending enhance real-world performance without compromising convenience. Simultaneously, growing consumer environmental awareness, carbon neutrality targets, and sustainability driven purchasing behavior reinforce demand for cleaner mobility solutions, positioning hybrid flex fuel platforms as a pragmatic transition technology supporting regulatory compliance, decarbonization.

Restraints - Limited Ethanol Infrastructure and Fuel Station Availability Constraining Market Penetration

Flex fuel vehicle market expansion remains constrained by insufficient ethanol fuel infrastructure, particularly for E85 and other high blend fuels, as limited fueling station availability restricts practical usability across many regions. Distribution network limitations and uneven geographic coverage create fuel sourcing uncertainty, reducing consumer confidence in daily operability. Significant infrastructure investment requirements deter rapid expansion, especially in markets lacking established ethanol logistics. Regional disparities in storage, transportation, and retail dispensing capacity further slow adoption, despite supportive policies. Without coordinated investment in ethanol production, distribution, and retail networks, flex fuel vehicles face adoption barriers and slower penetration outside mature ethanol markets.

Manufacturing Cost Premiums and Technical Complexity Affecting Affordability

Flex fuel vehicle market expansion is constrained by higher manufacturing costs linked to flexible fuel system complexity and required engine modifications. FFV platforms require ethanol resistant materials, upgraded fuel sensors, injectors, and calibration, increasing component sourcing challenges and production expenses versus conventional vehicles. These added costs translate into production cost premiums and elevated vehicle price points, limiting adoption in budget conscious passenger segments and cost sensitive fleet buyers. Competitive pricing pressure from conventional ICE and electrified alternatives further compresses margins, discouraging OEM scale up in entry level models. Without cost optimization and localized sourcing, price premiums remain a restraint globally.

Opportunities - Emerging Market Vehicle Proliferation and Government Ethanol Production Support

Emerging market vehicle proliferation and government ethanol production investment represent a substantial growth opportunity, driven by Asia Pacific expanding at 5.6% CAGR as India, Brazil, and Southeast Asia exhibit accelerating vehicle ownership and production growth. Governments are actively supporting domestic ethanol production through policy incentives, farmer income enhancement programs, and biofuel blending mandates, strengthening supply chain reliability for flex fuel vehicles. Rising passenger and commercial vehicle demand, combined with local production facility development, improves affordability and market penetration. Government incentive programs further encourage OEM localization, while regional manufacturing scale development reduces costs and enhances competitiveness. Collectively, these dynamics create a favorable ecosystem for sustained flex fuel vehicle deployment across emerging economies over medium to long term horizons globally strategically.

Second-Generation Ethanol Production and Sustainability Enhancement

Second generation ethanol production and sustainability advancement represent a significant emerging opportunity, as the industry transitions from food crop-based ethanol toward agricultural waste and non-food feedstocks. Using residues such as crop straw, bagasse, and organic waste strengthens sustainability positioning while eliminating food crop dependency concerns that previously constrained adoption. Advanced production technologies improve conversion efficiency, reduce lifecycle emissions, and enhance long-term economic viability for flex fuel ecosystems. Integration of circular economy principles enables value creation from waste streams, supporting premium sustainability narratives for automakers and fuel suppliers. This shift enhances regulatory acceptance, attracts environmentally conscious consumers, and supports long-term market resilience by aligning flex fuel vehicles with decarbonization targets, resource efficiency goals, and energy frameworks globally.

Category-wise Analysis

Engine Type Insights

Internal combustion engines command 89% of the flex fuel vehicle market share, with E10-E25 segment representing around 42% of the total market, the E25-E85 segment represent in between 30-33%, and Above E85 segment holds the rest in the ICE Category, reflecting a broad adoption of flexible fuel compatibility across varying ethanol blend levels supporting diverse regional regulatory requirements and consumer preferences. Regulatory flexibility accommodation. Global compliance support. Consumer choice enablement. Technology standardization achievement.

Hybrid flex-fuel engines expand as the fastest-growing category at 8.1% CAGR, driven by combining electric motor and flex-fuel engine capabilities creating vehicles with extended driving range and reduced emissions supporting emerging consumer demand for a balanced sustainability and practicality approach. Electric-hybrid integration. Extended range capability. Emission reduction achievement. Consumer preference convergence. Technology convergence momentum. Premium market positioning. Future powertrain leadership.

Vehicle Type Insights

Passenger vehicles command 68% of flex fuel vehicle market share, representing dominant segment reflecting highest production volumes and broad consumer base adoption across diverse geographic markets supporting sustained market growth and technology standardization. Volume production leadership. Consumer adoption breadth. Regulatory compliance requirement. Technology standardization driving. Global distribution networks. Market penetration leadership. Revenue generation dominance.

Light commercial vehicles expand as a prominent-growing vehicle category at 4.8% CAGR, driven by fleet operators seeking cost-effective and sustainable vehicle options supporting commercial fleet modernization and logistics sector adoption enabling emerging growth opportunity in commercial transportation segments. Fleet operator focus. Cost savings emphasis. Commercial adoption expansion. Operating cost reduction. Fuel flexibility value. Supply chain reliability. Emerging fleet leadership.

Regional Market Insights

North America

North America maintains 35% market share, driven by US regulatory leadership, extensive OEM investments, established ethanol infrastructure, and consumer environmental consciousness supporting market development and premium positioning. US EPA RFS mandate leadership. OEM concentration supporting adoption. Ethanol infrastructure expansion. Consumer environmental consciousness. Regulatory compliance requirement. Technology innovation ecosystem. Premium market development.

The North American market is characterized by regulatory leadership and OEM investment focus, with Ford, General Motors, and Chrysler maintaining dominant positions. Strong emphasis on RFS compliance and E85 fuel availability expansion. Established supply chains and technical support networks enabling rapid deployment.

Europe Flex Fuel Vehicle Market Trends

Europe expands at 3.9% CAGR, driven by renewable energy directives, sustainability emphasis, automotive technology leadership, and regulatory harmonization supporting advanced technology adoption and environmental compliance focus. EU renewable energy directive. Sustainability emphasis prioritization. Biofuel regulation support. Carbon reduction target alignment. Technical standards leadership. Premium market positioning. Regional harmony advancement.

The European market is characterized by sustainability consciousness and regulatory compliance emphasis with manufacturers focusing on emission reduction and environmental standards. Growing emphasis on second-generation biofuels and renewable fuel sourcing. Established technical standards supporting reliability and consistency. Partnership ecosystems supporting innovation and market development.

Asia Pacific Flex Fuel Vehicle Market Share and Trends Analysis

Asia Pacific expands at 5.6% CAGR, driven by vehicle production dominance, rapid urbanization, government ethanol mandates, and emerging market vehicle ownership growth supporting market expansion exceeding global averages. India E20 fuel mandate implementation. Brazil flex-fuel leadership (80%+ adoption). Vehicle production scale dominance. Government ethanol production support. Farmer benefit programs. Manufacturing cost advantages. Regional expansion momentum.

Asia Pacific market is characterized by rapid growth with India and Brazil leading through government ethanol mandates and production support. India's E20 fuel compatibility requirement for all new vehicles (April 2023) driving manufacturer adoption. Brazil's 80%+ flex fuel vehicle adoption demonstrating mature market development. Cost-competitive production attracting global supply chain development. Government focus on domestic ethanol production, creating a sustainable ecosystem.

Competitive Landscape

The flex fuel vehicle market remains moderately consolidated, led by multinational manufacturers such as Ford Motor Company, General Motors, and Volkswagen AG through strong OEM partnerships, ethanol infrastructure alignment, and mature technology platforms. Asian automakers, including Toyota, Honda, Maruti Suzuki, and Tata Motors, enhance geographic reach, while regional specialists address niche demand through cost-competitive strategies and localized technology development.

Strategic Developments

- In August 2023, Toyota announced the world's first fully ethanol-powered car based on the HyCross MPV model with a flex-fuel engine, demonstrating technology leadership and commitment to alternative fuel vehicles, supporting sustainable transportation innovation and emerging market focus, particularly in regions with ethanol availability.

- In April 2023, Volkswagen announced a strategic product offensive in South America targeting increased FFV model availability and market penetration, recognizing Brazil's mature flex-fuel market and expanding product portfolio to capture regional growth opportunities with localized flex-fuel compatible vehicles.

- In March 2025, a leading Japanese automobile manufacturer announced a collaboration with an AI analytics provider to develop a smart fuel-blend optimization system that automatically learning driving patterns and adjusts the ethanol-to-gasoline ratio in real-time while maximizing fuel efficiency and environmental performance.

Companies Covered in Flex Fuel Vehicle Market

- Ford Motor Company

- General Motors

- Volkswagen AG

- Toyota Motor Corporation

- Honda Motor Company

- Maruti Suzuki

- Tata Motors

- Fiat Chrysler Automobiles

- Volvo Cars

- Hyundai Motor Group

- Mahindra & Mahindra

- BMW Group

Frequently Asked Questions

The global flex fuel Vehicle Market is anticipated at US$ 71.6 Billion in 2026 and is projected to reach US$ 101.5 Billion by 2033.

Market growth is driven by mandatory ethanol blending regulations, lower fuel costs reducing crude oil dependency, and hybrid flex-fuel engine innovations delivering up to 77% lifecycle GHG reduction.

The market is projected to expand at a 5.1% CAGR between 2026 and 2033.

Key opportunities lie in emerging market vehicle growth backed by ethanol mandates, second-generation bioethanol adoption, and AI-enabled smart fuel-blend optimization systems.

The market is led by Ford, General Motors, and Volkswagen, with strong innovation momentum from Toyota, Honda, Maruti Suzuki, and Tata Motors driving regional flex-fuel expansion.