- Electrical Equipment & Services

- Electronics Adhesives Market

Electronics Adhesives Market Size, Share, and Growth Forecast, 2025 - 2032

Electronics Adhesives Market by Product Type (Heat-Curing, Room-Temperature-Curing, UV/Visible-Light Curing, Misc.), Composition (Epoxy, Silicone, Polyurethane, Acrylic), Application (Surface Mounting / PCB Assembly, Encapsulation / Circuit Protection, Conformal Coatings, Thermal Management, Automotive Electronics), and Regional Analysis for 2025 - 2032

Electronics Adhesives Market Size and Trends Analysis

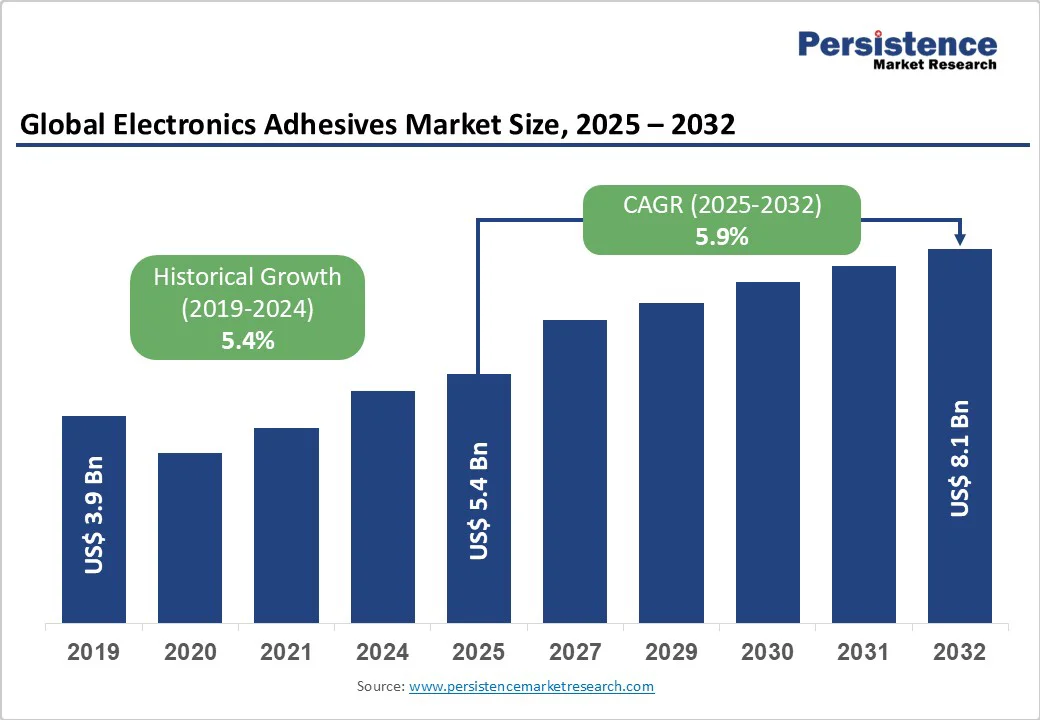

The global electronics adhesives market size is likely to be valued at US$ 5.4 Bn in 2025 and is projected to reach US$ 8.1 Bn by 2032, growing at a CAGR of 5.9% between 2025 and 2032.

Robust demand for miniaturized, high-performance electronic devices, the expansion of semiconductor and automotive electronics sectors, and technological advances in materials science underpin market growth.

The adoption of advanced manufacturing processes, such as surface mounting and UV/visible-light curing, enables rapid assembly, reliability, and thermal management in next-generation products.

Key Industry Highlights:

- Leading Product Type: Heat-curing adhesives dominated, holding a 48% share in 2025 due to their reliability and suitability for high-volume manufacturing; UV/visible-light curing adhesives represented the fastest-growing segment, driven by miniaturization and rapid assembly needs.

- Leading Composition: In terms of resin composition, epoxy adhesives led with a 37% market share in 2025, valued for durability and thermal stability, while silicone adhesives grew rapidly to hold 23% share due to flexibility and use in miniaturized electronics.

- Leading Application: Among application segments, surface mounting/PCB assembly commanded a 35% share in 2025, supported by increasing component density and consumer electronics demand, whereas automotive electronics held 10% share and was the fastest-growing segment, driven by EV adoption and ADAS integration.

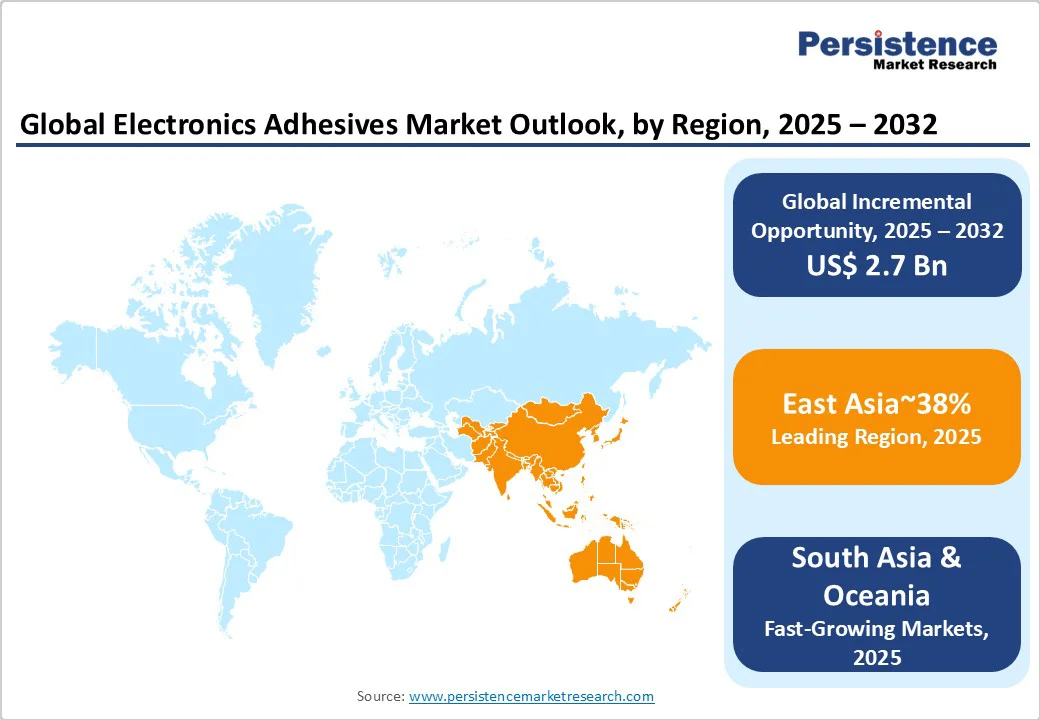

- Leading Region: Regionally, East Asia dominated with 38% market share, propelled by China’s semiconductor expansion and advanced manufacturing initiatives.

- Fast-growing Region: North America held a 21% share, buoyed by the US CHIPS Act investments exceeding USD 630 billion; South Asia and Oceania accounted for 11%, supported by India’s favorable manufacturing incentives.

| Key Insights | Details |

|---|---|

| Electronics Adhesives Market Size (2025E) | US$ 5.4 Bn |

| Market Value Forecast (2032F) | US$ 8.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.4% |

Market Dynamics

Driver - Electric Vehicle Battery Assembly Acceleration

The electric vehicle industry has emerged as a transformative force driving electronics adhesives demand, with global EV battery demand reaching 750 GWh in 2023, representing a 40% increase compared to 2022. Battery assembly processes require advanced adhesives for electrical insulation, cell bonding, thermal management, and vibration damping to ensure safety and reliability under extreme conditions. The United States and Europe witnessed over 40% year-on-year growth in EV battery demand, while China's market expanded by 35%, creating substantial opportunities for specialized adhesive applications.

Critical raw materials for battery production include 140 kt of lithium, 150 kt of cobalt, and 370 kt of nickel, all requiring precision bonding solutions throughout the manufacturing process. This unprecedented scale of battery manufacturing, concentrated near EV demand centers with Europe producing 110 GWh and the U.S. 70 GWh annually, necessitates high-performance adhesives that can withstand thermal cycling between -40°C to +85°C while maintaining structural integrity and electrical insulation properties essential for next-generation automotive applications.

Semiconductor Manufacturing Capacity Expansion

The global semiconductor industry achieved historic sales in 2024, marking a 19.1% increase from 2023 and surpassing the $600 billion milestone for the first time. This growth directly correlates with electronics adhesives demand, as semiconductor packaging requires specialized die attach, underfill, and encapsulation materials.

The U.S. CHIPS and Science Act has catalyzed over $630 billion in private sector investments across 130+ announced projects in 28 states, supporting over 500,000 American jobs and creating unprecedented demand for semiconductor-grade adhesives.

Major chipmakers, including Intel, GlobalFoundries, and Micron, are building advanced fabs requiring flip-chip adhesives for high-density packaging, chip-on-board adhesives for direct die attachment, and packaging adhesives for module assembly applications.

The Americas led regional semiconductor growth with a 44.8% annual expansion, while the Asia Pacific maintained 12.5% growth, reinforcing the global scale of semiconductor manufacturing expansion that drives specialized adhesive consumption across advanced packaging technologies.

Advanced Electronics Miniaturization Requirements

The consumer electronics sector's relentless pursuit of miniaturization has created sophisticated adhesive requirements for increasingly compact device architectures. Modern smartphones contain hundreds of electronic components requiring precision bonding solutions capable of withstanding thermal cycling, mechanical stress, and environmental exposure while maintaining electrical performance.

High-density packaging technologies push bond lines toward micron-level tolerances, demanding adhesives with controlled viscosity, minimal outgassing, and elastic moduli that accommodate differential expansion among stacked semiconductor dies.

Surface mount technology applications have grown significantly. This miniaturization trend extends beyond consumer devices into automotive ADAS systems, industrial sensors, and medical electronics, where reliable bonding performance in confined spaces directly impacts device functionality and longevity across diverse operating environments.

Restraint - Environmental Regulations and VOC Compliance Requirements

Stringent environmental regulations concerning volatile organic compound emissions present ongoing challenges for electronics adhesives manufacturers and users. The EPA regulates VOCs at the federal level through 40 CFR 59, establishing specific content limits for different adhesive categories, while state-level regulations often impose additional restrictions.

REACH and RoHS directives in Europe require extensive documentation, testing, and compliance verification for hazardous substances, adding complexity and costs to product development and market access. For instance, companies investing in reformulating products to achieve lower VOC content, develop halogen-free alternatives, must follow specialized storage and handling protocols to meet regulatory standards. Compliance requires ongoing investment in staff training, quality control measures, and specialized packaging to prevent UV exposure and contamination, increasing operational costs and complexity for manufacturers serving global markets.

Opportunities - Emerging 5G and IoT Infrastructure Development

The deployment of 5G networks and the expansion of Internet of Things applications create substantial opportunities for high-performance electronics adhesives designed for next-generation communication infrastructure. 5G technology demands specialized adhesives capable of managing higher frequencies, increased thermal loads, and enhanced signal integrity requirements across base stations, small cells, and user equipment.

IoT device proliferation necessitates adhesives with superior environmental protection, extended operational lifespans, and compatibility with diverse sensor technologies operating in challenging conditions. Advanced adhesive formulations incorporating nanotechnology enable superior bonding strength and electrical properties essential for miniaturized IoT sensors and wearable electronics.

Manufacturing automation trends associated with Industry 4.0 create demand for adhesives compatible with robotic assembly lines and high-speed production processes. UV-curable adhesives particularly benefit from this trend, offering rapid curing times, supporting just-in-time manufacturing, and reduced production bottlenecks.

The convergence of 5G infrastructure deployment with smart city initiatives presents additional market expansion opportunities. Smart traffic systems, environmental monitoring networks, and connected infrastructure require adhesives capable of maintaining performance across temperature extremes, moisture exposure, and mechanical vibration over multi-decade service lives. Companies developing specialized formulations for outdoor electronics applications can capitalize on government infrastructure investments and urban modernization projects worldwide.

Advanced Packaging Technologies and Heterogeneous Integration

The semiconductor industry's evolution toward advanced packaging technologies, including 2.5D/3D integration, fan-out packaging, and chiplet architectures, creates specialized adhesive requirements for next-generation electronic systems. These technologies demand materials capable of supporting multiple die stacking, thermal management across different semiconductor nodes, and mechanical stability under varying coefficients of thermal expansion conditions.

Redistribution layer materials, including polyimide and metal pastes, represent the fastest-growing segment in advanced packaging applications. Co-packaged optics for data center applications require adhesives tailored for photonic integrated circuits, single-mode fiber bonding, and precise optical alignment, maintaining signal integrity under temperature fluctuations.

Artificial intelligence and machine learning accelerator chips drive demand for specialized thermal interface materials and die attach adhesives capable of managing heat dissipation exceeding 500W per package. Advanced flip-chip technologies enabling high-performance computing applications require underfill materials with enhanced thermal conductivity and reliability under power cycling conditions.

Category-wise Analysis

Product Type Insights

Heat-curing adhesives maintain market leadership with a 48% share in 2025, driven by their proven reliability in high-volume manufacturing applications requiring consistent performance across diverse substrate materials.

These adhesives offer superior mechanical properties, chemical resistance, and thermal stability essential for automotive electronics, industrial control systems, and power management applications. Epoxy-based heat-curing formulations provide exceptional bond strength and environmental resistance, making them preferred solutions for applications experiencing thermal cycling, mechanical stress, and chemical exposure throughout extended service lives.

Manufacturing advantages include predictable cure profiles, excellent gap-filling capabilities, and compatibility with automated dispensing systems enabling high-throughput production processes.

UV/visible-light curing adhesives represent the fastest-growing product segment, achieving the highest CAGR due to miniaturization demands and rapid assembly requirements in modern electronics manufacturing. These adhesives enable precision bonding of temperature-sensitive components, supporting just-in-time production processes and reducing manufacturing bottlenecks through rapid curing capabilities.

Advanced LED curing systems consume up to 70% less energy than conventional UV lamps while providing superior temperature control essential for bonding sensitive substrates in semiconductor packaging and optical component assembly.

Technological innovations in photoinitiator chemistry enhance adhesion to challenging substrates, including glass, metals, and engineered plastics used in automotive and aerospace applications. Market growth is further supported by environmental benefits, including reduced VOC emissions, elimination of solvent-based alternatives, and compatibility with automated assembly lines requiring precise dispensing and instant curing capabilities.

Composition Insights

Epoxy adhesives represents a 37% share in 2025, offering excellent mechanical strength, thermal resistance, and electrical insulation properties. They are widely applied in PCB assembly, battery module encapsulation, and semiconductor packaging, ensuring longevity and operational reliability under extreme conditions.

Silicone adhesives, projected to hold 23% market share in 2025, are gaining traction due to flexibility, thermal stability, and suitability for miniaturized electronics. Applications include automotive electronics, LED modules, and wearable devices, where vibration damping, environmental protection, and thermal expansion accommodation are critical. The material supports high-density integration and reliability across multiple high-tech applications.

Automotive Electronics represents the fastest-growing application segment with 10% market share in 2025, driven by electric vehicle adoption, ADAS system deployment, and in-vehicle electronics expansion across global automotive markets. This segment benefits from the transition toward electrified powertrains requiring specialized adhesives for battery thermal management, power electronics assembly, and charging system integration.

Application Insights

Surface Mounting/PCB Assembly applications dominate with 35% market share in 2025, driven by continued expansion of consumer electronics production and increasing component density requirements in modern circuit board designs . SMT adhesives enable reliable component attachment during wave soldering and reflow processes, providing mechanical stability and thermal protection for surface-mounted components including resistors, capacitors, and integrated circuits.

Market growth is supported by automotive electronics proliferation, 5G infrastructure deployment, and industrial automation systems requiring high-reliability PCB assemblies capable of operating across extended temperature ranges and challenging environmental conditions.

Advanced SMT adhesives offer rapid cure characteristics, precise dispensing compatibility, and enhanced thermal stability supporting high-speed manufacturing processes essential for meeting growing consumer electronics demand. Technology innovations include conductive adhesives providing both mechanical bonding and electrical connectivity, reducing assembly complexity while improving signal integrity in high-frequency applications

Automotive Electronics represents the fastest-growing application segment with 10% market share in 2025, driven by electric vehicle adoption, ADAS system deployment, and in-vehicle electronics expansion across global automotive markets . This segment benefits from the transition toward electrified powertrains requiring specialized adhesives for battery thermal management, power electronics assembly, and charging system integration.

Regional Insights and Trends

East Asia Electronic Adhesives Market

East Asia commands 38% of global electronics adhesives market share, establishing regional dominance through massive electronics manufacturing capacity and strategic government initiatives supporting domestic technology development. China leads regional growth with its vast electronics manufacturing ecosystem producing over 50% of global consumer electronics while expanding semiconductor fabrication capabilities through strategic industrial policies.

The expansion of domestic semiconductor manufacturing, led by companies including SMIC, Huawei, and emerging GPU designers such as Biren and Moore Threads, drives specialized adhesive demand for flip-chip packaging, chip-on-board assembly, and advanced packaging applications[provided data].

Government-driven technology initiatives, including the National Unified Computing Power Network and investments in advanced lithography equipment from domestic suppliers, create robust demand for thermally conductive, electrically conductive, and UV-curable adhesives essential for high-performance computing applications.

Japan maintains a critical market position through its precision manufacturing expertise and high-performance materials development, supporting semiconductor, automotive electronics, and advanced display technologies. Japanese manufacturers lead innovation in next-generation adhesives, offering superior thermal conductivity, environmental resistance, and miniaturization compatibility essential for premium electronics applications.

South Korea's market strength derives from global leadership in memory chips and display technologies, with major conglomerates driving demand for high-precision adhesive solutions supporting advanced packaging and flexible electronics manufacturing.

Regional market dynamics benefit from established supply chains, skilled manufacturing workforces, and continued investment in research and development supporting adhesive technology advancement across diverse industrial applications.

North America Electronic Adhesives Market Trends

North America accounts for 21% of global market share, demonstrating strong growth momentum driven by substantial investments in domestic semiconductor manufacturing and electronics supply chain reshoring initiatives.

The CHIPS and Science Act has catalyzed over $630 billion in private sector investments across 130+ semiconductor projects, creating unprecedented demand for specialized adhesives supporting advanced packaging, wafer-level processing, and heterogeneous integration technologies [provided data].

Major manufacturers, including Intel, GlobalFoundries, and Micron are constructing state-of-the-art fabrication facilities requiring die attach films, underfill materials, and thermal interface solutions capable of supporting leading-edge process nodes and advanced packaging architectures.

Competitive Landscape

The Global Electronics Adhesives Market exhibits a consolidated competitive landscape, dominated by a few key players with substantial technological capabilities and global reach. Leading companies include Henkel AG & Co. KGaA, 3M Company, H.B. Fuller, LORD Corporation, and Panacol-Elosol GmbH, collectively shaping product innovation, advanced adhesive formulations, and end-use application standards.

Market competition is primarily driven by R&D investments in high-performance and UV/visible-light curing adhesives, strategic collaborations, and regional expansions. While smaller regional players exist, the market’s concentration around major multinational corporations reflects high barriers to entry due to technological complexity, quality standards, and regulatory compliance requirements. Strategic differentiation focuses on specialty adhesives for EV batteries, semiconductor packaging, and PCB assembly, where reliability and precision are critical.

Key Industry Developments:

- In September 2025, Henkel doubled its Brandon, South Dakota, facility to 70,000 sq. ft., boosting production of high-performance adhesives and thermal management solutions for electronics and EVs under LOCTITE® and BERGQUIST®, emphasizing sustainability and supporting market growth.

- In September 2025, DELO validated directional conductive adhesives for miniLED connections as a robust solder alternative, demonstrating high reliability under extreme temperature and humidity, targeting scalable production for miniLED and future microLED displays.

- In November 2025, Avery Dennison launched pressure-sensitive adhesive tapes for EV battery cell wrapping, offering insulation, corrosion resistance, and durability, with some products manufactured in the U.S. to support local production and sustainability.

Companies Covered in Electronics Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Dow Inc.

- Sika AG

- Bostik

- Hermon Manufacturing Inc.

- Master Bond

- Avery Dennison

- Kohesi Industries

- DELO Industrial Adhesives

- Meridian Adhesives Group

Frequently Asked Questions

The global electronics adhesives market is projected to be valued at US$ 5.4 Bn in 2025.

The Epoxy segment is leading due to its superior mechanical strength, thermal stability, and widespread use in high-performance electronics adhesives.

The electronics adhesives market is poised to witness a CAGR of 5.9% from 2025 to 2032.

The Electronics Adhesives market growth is driven by escalating demand from electric vehicle battery assembly, rapid semiconductor manufacturing expansion, and increasing miniaturization in consumer electronics.

Key market opportunities lie in the deployment of 5G and IoT infrastructure, advancements in semiconductor packaging and heterogeneous integration, and expanding automotive electronics applications fueled by EV and ADAS adoption.