- Semiconductor Materials & Components

- Electronics Conformal Coating Market

Electronics Conformal Coating Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Electronics Conformal Coating Market by Material Type (Acrylic, Polyurethane, Hybrid, Silicone, Epoxy), by Operating Method (Manual & Automated Spraying, Brushing, Dipping), by Technology (Solvent Based, Water Based, UV Cured), by Application (Appearance, Moisture and Insulation Resistance, UV Fluorescence, Flammability, Thermal Shock, Adhesive), Industry (Consumer Electronics, Automotive, Aerospace & Defense, Industrial and Telecommunication, Marine, Medical), and Regional Analysis, 2026 - 2033

Electronics Conformal Coating Market Size and Trend Analysis

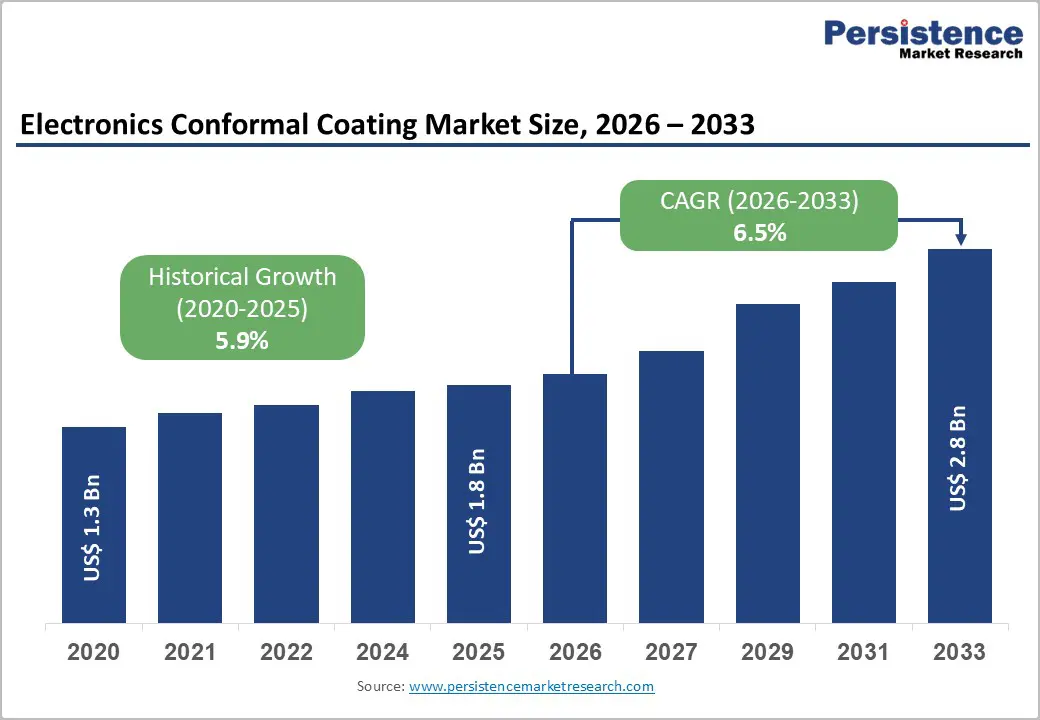

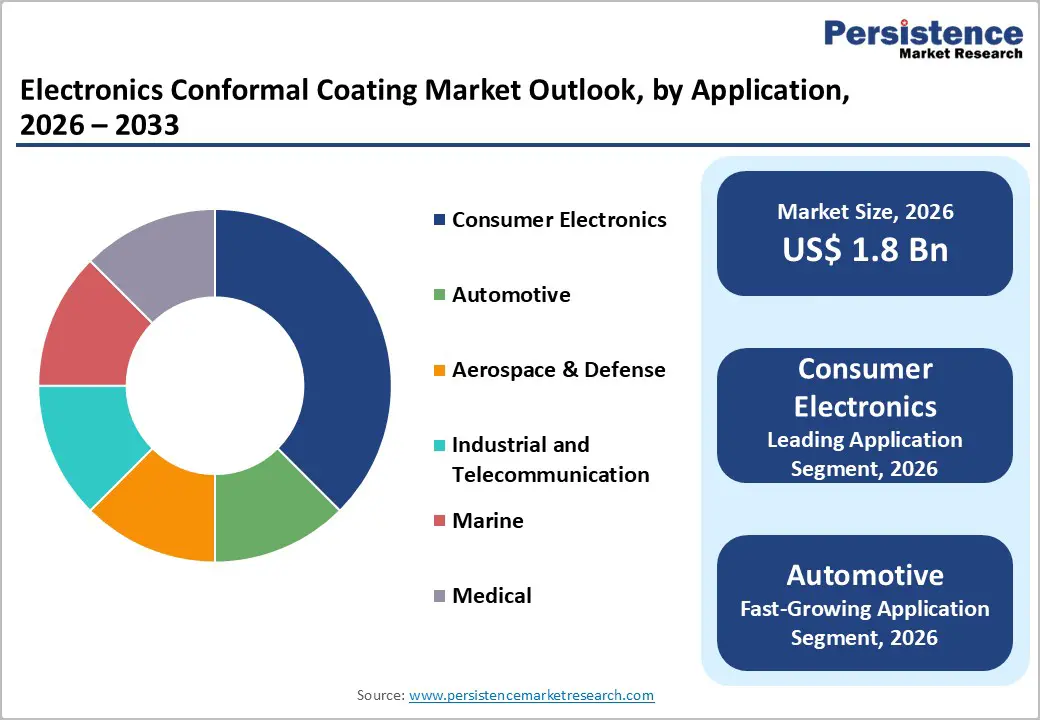

The global electronics conformal coating market size is expected to be valued at US$ 1.8 billion in 2026 and projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033.

This steady expansion reflects the accelerating demand for advanced protective coatings across electronics manufacturing as miniaturization trends intensify and environmental regulations become more stringent. The market growth is driven by the convergence of several critical factors including the exponential rise in consumer electronics demand with global consumer electronics market exceeding US$ 1.2 trillion annually, the acceleration of electric vehicle adoption with automotive electronics estimated to account for over 50% of total vehicle costs by 2030, and the escalating deployment of 5G infrastructure and IoT devices requiring robust protection against moisture, dust, and thermal stress.

Key Industry Highlights:

- Leading Region: Asia Pacific holds about 45% of the market in 2024 due to its high concentration of electronics manufacturing.

- Fastest Growing Region: Asia Pacific is projected to grow at a 9.2% CAGR during 2026 - 2033, driven by expanding electronics and EV production and supportive government schemes.

- Dominant Segment: Acrylic conformal coatings lead the market with roughly 44% share in 2025 owing to their ease of use, quick drying, and cost efficiency.

- Fastest Growing Segment: UV-curable coatings are expected to grow at an 8.5% CAGR during 2026 - 2033 due to efficient UV-LED curing and low-VOC environmental benefits.

- Key Market Opportunity: Aerospace and defense applications present the strongest opportunity due to stringent performance requirements and rising UAV and defense modernization programs.

| Key Insights | Details |

|---|---|

| Electronics Conformal Coating Market Size (2026E) | US$ 1.8 billion |

| Market Value Forecast (2033F) | US$ 2.8 billion |

| Projected Growth CAGR (2026 - 2033) | 6.5% |

| Historical Market Growth (2020 - 2025) | 5.9% |

Market Dynamics

Drivers - Explosive Growth in Consumer Electronics and Miniaturization Trends

The consumer electronics sector continues experiencing unprecedented growth, with the global market exceeding US$ 1.2 trillion annually, driven by surging demand for smartphones, wearables, tablets, and smart household devices incorporating advanced technologies, including artificial intelligence and machine learning. The persistent industry trend toward miniaturization of electronic components creates critical demand for conformal coatings that provide enhanced dielectric strength without adding significant bulk or weight to compact circuit boards.

Modern miniaturized printed circuit boards with densely packed components exhibit inherently lower resistance to electrical degradation from environmental factors, necessitating protective coatings capable of maintaining electrical insulation integrity in increasingly compact designs. Consumer electronics manufacturers increasingly recognize that conformal coatings provide cost-effective protection against corrosion, short circuits, and electrical interference without requiring space-consuming protective enclosures that conflict with compact product aesthetics. The proliferation of Internet of Things (IoT) devices utilizing wireless communication technologies creates particular vulnerability to electromagnetic interference (EMI) and radiofrequency interference (RFI), making conformal coatings essential for ensuring reliable wireless data transmission.

Automotive Sector Acceleration Driven by Electric Vehicle Proliferation

The automotive industry is experiencing transformative demand acceleration for conformal coatings, driven by the convergence of electrification trends and increasing electronic component integration. Electric vehicles utilize significantly higher electronics content than conventional internal combustion-based vehicles, with electronics accounting for over 50% of total vehicle production costs by 2030 as autonomous driving, battery management, and connectivity systems proliferate.

Electric vehicle platforms require robust protection of battery management systems, electric motor controllers, and high-voltage power distribution systems from harsh environmental conditions including temperature fluctuations, humidity, vibration, and corrosive substances. The global electric vehicle market is projected to reach 40% of total vehicle production by 2030, representing exponential conformal coating demand growth as automotive manufacturers systematically protect complex electronic systems. Advanced driver assistance systems (ADAS) incorporating cameras, radar sensors, and lidar systems demand specialized conformal coating protection to maintain sensor accuracy and reliability in challenging environmental conditions.

Restraints - High Initial Capital Investment and Complex Application Requirements

The deployment of comprehensive conformal coating infrastructure requires substantial capital expenditure for application equipment, with automated spray systems ranging from US$ 200,000 to US$ 500,000 per installation and representing significant budget constraints for small and medium-sized electronics manufacturers. Beyond equipment procurement, conformal coating implementation necessitates substantial professional services expenditure for process validation, operator training, quality control calibration, and establishment of production specifications compliant with industry standards including MIL-I-46058, IPC-A-610, and IPC-HDBK-612.

The complexity of material chemistry variations creates challenges for manufacturers attempting to optimize coating selection for specific application requirements. Inconsistent masking practices, incomplete material drying, and improper application technique frequently result in defective coatings requiring costly rework, quality inspection, and potential product rejection. Many contract manufacturers and smaller electronics assembly operations lack internal technical expertise to optimize conformal coating specifications for diverse application requirements, creating dependency on external consulting services and increasing implementation costs beyond material and equipment procurement.

Regulatory Complexity and Environmental Compliance Requirements

The fragmented regulatory landscape governing conformal coating formulations creates substantial compliance complexity for multinational electronics manufacturers. European Union regulations, including REACH, RoHS, and evolving VOC emission standards, impose stringent material restrictions and documentation requirements, while China, India, and emerging markets establish independently developed environmental standards that often conflict with established protocols.

The transition from traditional solvent-based coatings toward low-VOC water-based and UV-curable alternatives requires substantial reformulation investment and performance testing to ensure coating functionality equivalence. Healthcare and aerospace applications require additional regulatory approvals, material certifications, and biocompatibility testing, increasing cost and timeline complexity. The absence of globally harmonized conformal coating standards creates friction in international supply chains as manufacturers operating across multiple jurisdictions must maintain an inventory of regionally-specific coating formulations, increasing complexity and reducing manufacturing flexibility.

Opportunity - Aerospace and Defense Sector Expansion Through Advanced Material Development

The aerospace and defense sector represents a high-value growth opportunity for conformal coating providers as military and commercial aircraft manufacturers increasingly demand specialized protective coatings resistant to extreme operational environments. Aerospace electronics require coatings capable of withstanding extreme temperatures, salt fog corrosion exposure during maritime operations, and radiation effects encountered in high-altitude flight environments. Specialized conformal coatings incorporating polyurethane and epoxy chemistry are essential for protecting avionics systems, communication equipment, radar systems, and navigation electronics from harsh aerospace operational environments.

The U.S. Department of Defense procurement requirements mandate strict compliance with MIL-I-46058 and MIL-DTL-81706 specifications, establishing standardized demand drivers for compliant coating formulations. The integration of advanced unmanned aerial vehicles (UAVs) and satellite communication systems creates incremental demand for miniaturized, lightweight conformal coatings capable of protecting sophisticated electronics in space and high-altitude environments. The expertise requirements for aerospace coating specification compliance create barriers to entry for smaller manufacturers, enabling market concentration among established vendors capable of maintaining aerospace quality management systems and material traceability protocols.

Medical Device Sector Transformation Through Biocompatible and Specialized Formulations

The medical device industry represents an emerging high-growth opportunity for conformal coating providers offering specialized biocompatible and antimicrobial formulations. Medical device manufacturers increasingly require conformal coatings capable of protecting sophisticated electronics embedded in implantable devices, diagnostic equipment, and surgical instruments while maintaining rigorous biocompatibility standards. The integration of advanced materials, including silicone-based and hybrid formulations enable development of coatings capable of supporting complex medical device functionality while maintaining regulatory compliance with FDA guidance, ISO 13601 biocompatibility standards, and international medical device regulations.

Medical-grade conformal coatings incorporating antimicrobial properties are gaining prominence as hospitals combat escalating healthcare-associated infection (HAI) challenges. The projected global medical device coating market growth of 8.0% CAGR through 2030 creates a substantial demand expansion opportunity for specialized conformal coating solutions. The convergence of advanced medical technology development, regulatory mandate stringency, and accelerating healthcare digital transformation is expected to generate sustained high-growth demand for specialized medical-grade conformal coating solutions.

Category-wise Analysis

Material Type Insights

Acrylic conformal coatings command the leading position within the Material Type category, capturing approximately 44% of market share in 2025, reflecting their exceptional performance characteristics, including ease of application, rapid drying properties, and strong moisture and electrical interference resistance. Acrylic formulations offer compelling advantages for high-volume manufacturing environments, with drying times as short as 30 minutes, enabling production throughput optimization without operational bottlenecks.

The dominance of acrylic technology is reinforced by cost-effectiveness advantages, with acrylic materials providing a superior value proposition compared to specialized polyurethane, epoxy, and silicone alternatives. Recent product innovations incorporating hybrid chemistry, combining acrylic base chemistry with polyurethane or silicone modifications, are expanding the acrylic performance envelope while preserving cost advantages and application simplicity.

Operating Method Insights

Automated Spraying emerges as the leading operating method within the Operating Method category, commanding approximately 52% of market share in 2025, reflecting the accelerating adoption of selective coating automation across electronics manufacturing facilities. Automated spray systems offer compelling advantages, including superior coating consistency, dramatically reduced material waste, and enhanced production throughput, enabling scaled manufacturing operations.

Selective spray equipment provides granular robotic control enabling precise masking of connector areas and component interfaces, eliminating manual masking requirements and substantially reducing process variability. The emerging deployment of inline conformal coating integration within circuit board assembly lines is expected to further accelerate automated spray system adoption as manufacturers optimize assembly floor space utilization and production efficiency.

Technology Analysis

Solvent-based conformal coatings maintain leadership within the Technology category, retaining approximately 58% of market share in 2025, though experiencing gradual erosion driven by accelerating environmental regulation and emerging water-based/UV-curable technology advancement. Solvent-based formulations provide an established performance track record spanning decades of aerospace, automotive, and industrial electronics applications, with extensive qualification across industry standards and customer specifications. However, solvent-based coating adoption faces escalating pressure from VOC emission regulations (REACH, RoHS, regional air quality standards), driving transition toward water-based alternatives containing less than 10-15% solvent content compared to 70-80% in traditional acrylic formulations. Water-based conformal coatings are experiencing rapid growth trajectory at estimated 8.2% CAGR through 2033, driven by regulatory compliance imperatives and improved performance characteristics closing performance gaps with solvent-based alternatives.

Application Insights

Moisture and Insulation Resistance emerges as the leading application within the Application category, commanding approximately 38% of market share in 2025, reflecting its fundamental criticality for electronics reliability. Moisture ingress represents the most prevalent failure mechanism for electronic equipment, with conformal coatings providing essential protection against humidity-induced corrosion, electrochemical migration, and insulation breakdown across printed circuit boards and electronic components.

The moisture protection application encompasses broad Industrys including consumer electronics, automotive, telecommunications, and industrial automation, creating large addressable market spanning diverse customer segments. The emerging trend toward high-density circuit integration and miniaturization intensifies requirements for superior insulation resistance, as component density reduction decreases electrical isolation clearances requiring enhanced dielectric protection. The expansion of IoT device deployment in challenging environmental conditions is expected to sustain robust demand growth for moisture and insulation protection conformal coatings.

Industry Analysis

Consumer Electronics commands the dominant position within the Industry category, capturing approximately 36% of market share in 2025, driven by exponential growth in personal electronic devices including smartphones, tablets, wearables, and smart home products. The consumer electronics sector represents the largest-volume application for conformal coatings, with annual production volumes exceeding 2 billion units requiring protective coating deployment during manufacturing processes.

Smartphone and wearable device production generates particular conformal coating demand, with manufacturers requiring coating protection for moisture-sensitive components including microphones, camera modules, and RF antennas exposed to perspiration and incidental water exposure during normal device usage. The emerging trend toward foldable and flexible electronics creates specialized coating requirements, with manufacturers deploying hybrid and silicone-based formulations providing superior flexibility compared to rigid acrylic alternatives.

Regional Insights

North America Electronics Conformal Coating Market Trends and Insights

North America maintains strong regional market position, commanding approximately 24% of global market share in 2025, driven by mature electronics manufacturing infrastructure, stringent regulatory frameworks, and concentration of major aerospace and defense suppliers. The United States represents the largest North American market, with aerospace and defense sector conformal coating adoption driven by military specification requirements and government procurement mandates establishing standardized demand drivers. Major automotive manufacturers including General Motors, Ford, and Tesla are systematically deploying conformal coating protection across electric vehicle electronics as part of broader reliability optimization initiatives addressing performance in demanding automotive environments.

The region is experiencing an accelerating transition toward water-based and UV-curable conformal coatings driven by stringent EPA VOC emission standards and corporate sustainability commitments from major electronics manufacturers. The concentration of aerospace suppliers, including Collins Aerospace, Raytheon, and Lockheed Martin, creates sustained demand for aerospace-specification conformal coatings compliant with MIL-I-46058 and MIL-DTL-81706 standards. Innovation ecosystem maturity in North America has fostered the development of specialized coating formulations, including silicone-polyurea hybrids and advanced water-based systems, addressing performance requirements across diverse application segments.

Europe Electronics Conformal Coating Market Trends and Insights

Europe represents the second-largest regional market, capturing approximately 22% of global market share in 2025, with market dynamics fundamentally shaped by rigorous environmental regulation, including REACH, RoHS, and evolving VOC emission standards. Germany, the United Kingdom, France, and Spain lead European conformal coating adoption, driven by sophisticated automotive and electronics manufacturing sectors concentrated in these jurisdictions. The German automotive industry, representing the world’s largest automobile manufacturer by volume, has systematically adopted low-VOC water-based and UV-curable conformal coatings meeting EU environmental compliance requirements while maintaining performance standards for electric vehicle electronics protection.

Regulatory harmonization through ePrivacy Directive review and the emerging ePrivacy Regulation is expected to establish consistent conformal coating standards across European Union member states. The concentration of automotive suppliers and electronics contract manufacturers in Germany and Eastern Europe creates regional demand concentration, with companies including Henkel AG & Co. KGaA and Chase Corporation subsidiaries maintaining dominant market positions through established customer relationships and specialized product portfolios.

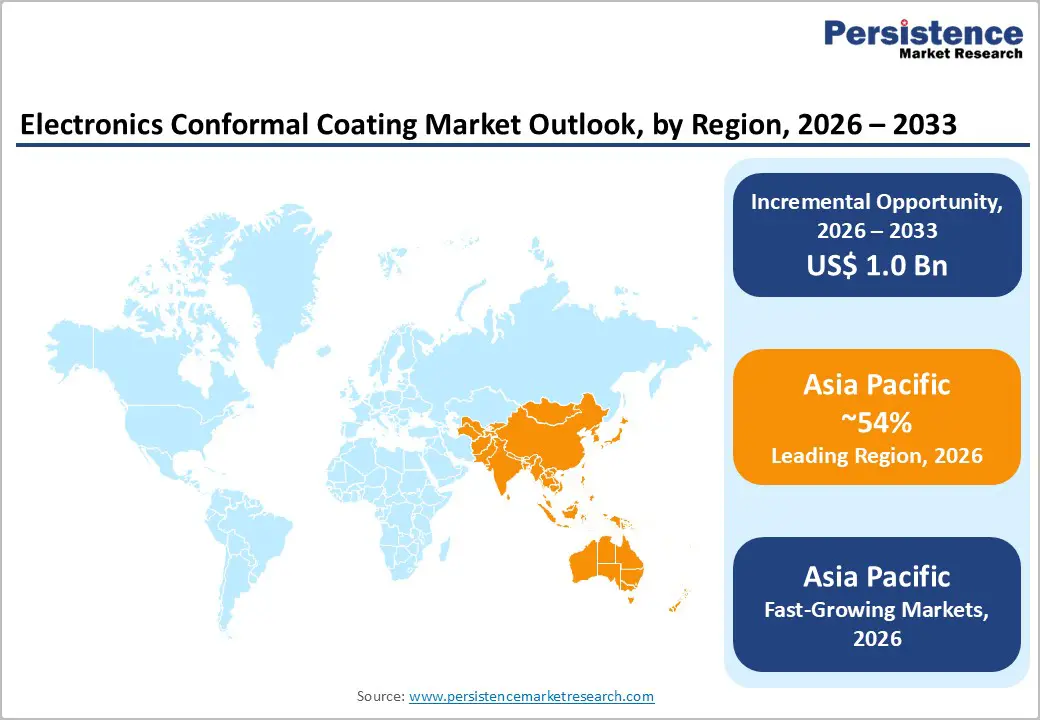

Asia Pacific Electronics Conformal Coating Market Trends and Insights

Asia Pacific emerges as the fastest-growing region, projected to expand at 9.2% CAGR during 2026-2033, driven by exponential consumer electronics and automotive electronics manufacturing expansion across China, Japan, India, and Southeast Asia. The region accounts for over 45% of global conformal coating demand in 2025, reflecting massive electronics production concentration in countries including China, Taiwan, South Korea, and Vietnam. China dominates regional conformal coating consumption, with smartphone manufacturers including Apple’s primary manufacturing partners, tablet producers, and wearable device manufacturers requiring protective coating deployment across production facilities.

The region’s emergence as global electronics manufacturing hub, combined with India’s PLI Scheme allocating over US$ 10 billion to electronics manufacturing, is driving accelerating conformal coating demand growth. Japanese manufacturers, including Sony, Panasonic, and Nintendo maintain stringent quality standards requiring premium conformal coating protection across consumer electronics portfolios. Vietnam and Thailand are emerging as key manufacturing hubs for consumer electronics and components, with government support for electronics manufacturing creating infrastructure investments driving conformal coating adoption. The region’s labor cost advantages and vertically integrated supply chains enable competitive manufacturing, enabling electronics producers to allocate resources toward quality and reliability initiatives, supporting continued conformal coating market expansion.

Competitive Landscape

The global electronics conformal coating market is moderately consolidated, with a mix of large chemical suppliers and specialized niche providers shaping competitive dynamics through differentiated technologies and long-term customer partnerships. Market structure is defined by broad portfolio players that leverage global manufacturing scale, regulatory certifications, and integrated supply chains to secure consistent demand across consumer electronics, automotive, aerospace, and medical segments. These companies pursue strategies such as acquisitions, sustainability-driven product innovation, and expansion of advanced application equipment integrations to strengthen market presence.

Smaller specialized providers compete through customized formulations, faster service responsiveness, and focused expertise in high-reliability environments. The industry is also experiencing gradual consolidation and increasing collaboration among major vendors to address decarbonization, low-VOC formulation development, and compliance with evolving global environmental regulations, reinforcing the shift toward sustainable and high-performance coating technologies.

Key Developments:

- April 2024: Henkel AG & Co. KGaA successfully acquired US-based Seal for Life Industries, a provider of innovative coating and sealing solutions, substantially expanding Henkel’s portfolio of specialized protective coatings for electronics applications requiring enhanced thermal and chemical resistance.

- October 2025: Henkel Adhesive Technologies and Dow Inc. expanded their long-standing strategic partnership to accelerate decarbonization in adhesives and coatings manufacturing, introducing low-carbon feedstocks and renewable electricity into production processes, targeting 20-40% product carbon footprint reduction across conformal coating portfolios.

- November 2025: HumiSeal, under Chase Corporation, expands its pan-European distributor network with partners ConRo Electronics, Biesterfeld, Caplinq Europe, and Ellsworth Adhesives, enhancing local technical support, faster delivery, and product accessibility for electronics, automotive, aerospace, military, and industrial markets.

Companies Covered in Electronics Conformal Coating Market

- Henkel AG & Co. KGaA

- Dow Inc.

- H.B. Fuller Company

- Chase Corporation

- Shin-Etsu Chemical Co., Ltd.

- Illinois Tool Works Inc. (Chemtronics)

- Electrolube Limited (MacDermid Alpha)

- MG Chemicals Ltd.

- Dymax Corporation

- Specialty Coating Systems, Inc.

- ELANTAS PDG, Inc. (ALTANA AG)

- Peters Group - Lackwerke Peters GmbH & Co. KG

- Panacol-Elosol GmbH

- Specialty Polymer Coatings Inc.

- Shenzhen DeepMaterial Technologies Co., Ltd.

Frequently Asked Questions

The market is expected to reach about US$ 1.8 billion in 2026.

Growth is driven by rising consumer electronics demand, EV expansion, 5G and IoT deployment, miniaturization, and stricter environmental regulations.

Asia Pacific leads with roughly 45% share due to strong electronics manufacturing activity.

Key opportunities lie in aerospace and defense applications and fast-growing medical device coating needs.

The leading market players include Henkel AG & Co. KGaA, Dow Inc., Shin-Etsu Chemical Co., Ltd., H.B. Fuller Company, Chase Corporation’s HumiSeal, Illinois Tool Works, etc.