- Industrial Machinery

- Drain Cleaning Equipment Market

Drain Cleaning Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Drain Cleaning Equipment by Product Type (Hand Tools, and Power Tools), Sales Channel (Distributor, Retail Outlets, Online), End-user (Municipal, Residential, Industrial), and Regional Analysis, 20262033

Drain Cleaning Equipment Market Size and Trend Analysis

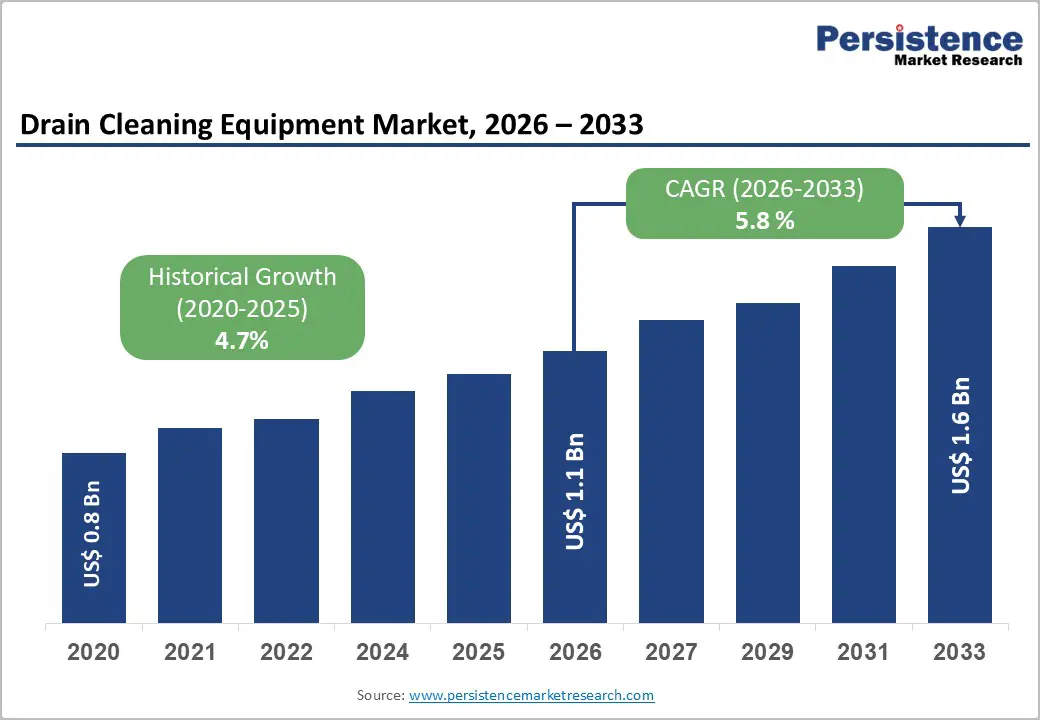

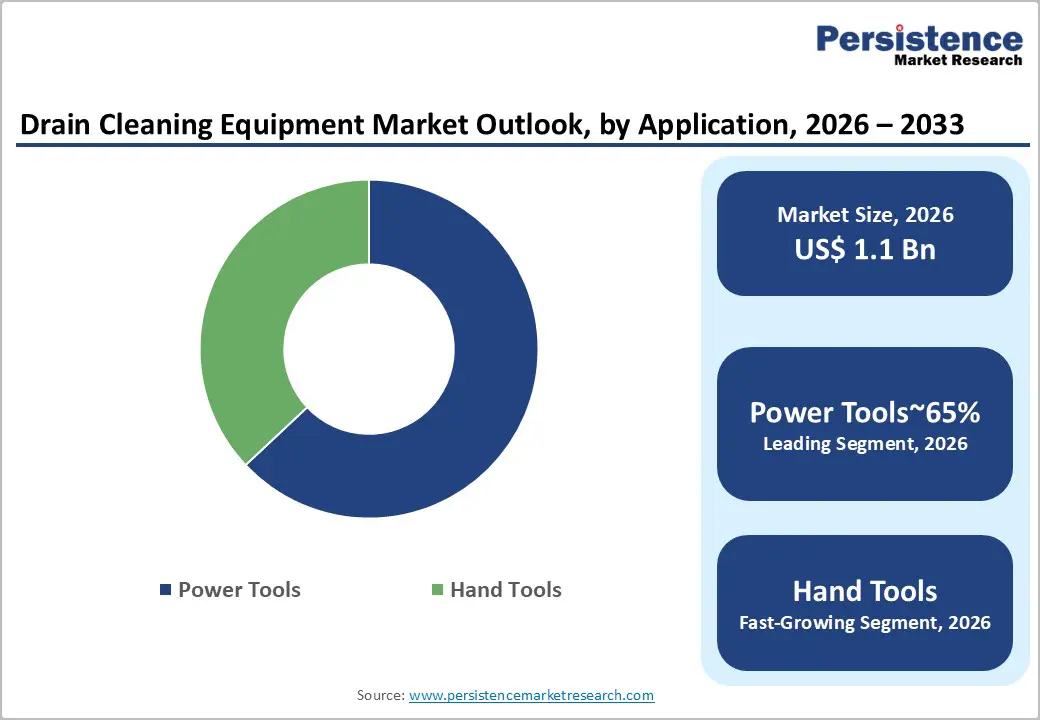

The global drain cleaning equipment market size is likely to be valued at US$ 1.1 billion in 2026 and is expected to reach US$ 1.6 billion by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033.

Market expansion is driven by urbanization-led infrastructure strain, heightened post-COVID sanitation awareness, and aging drainage systems requiring advanced drain cleaning technologies to manage complex blockages effectively.

Key Industry Highlights:

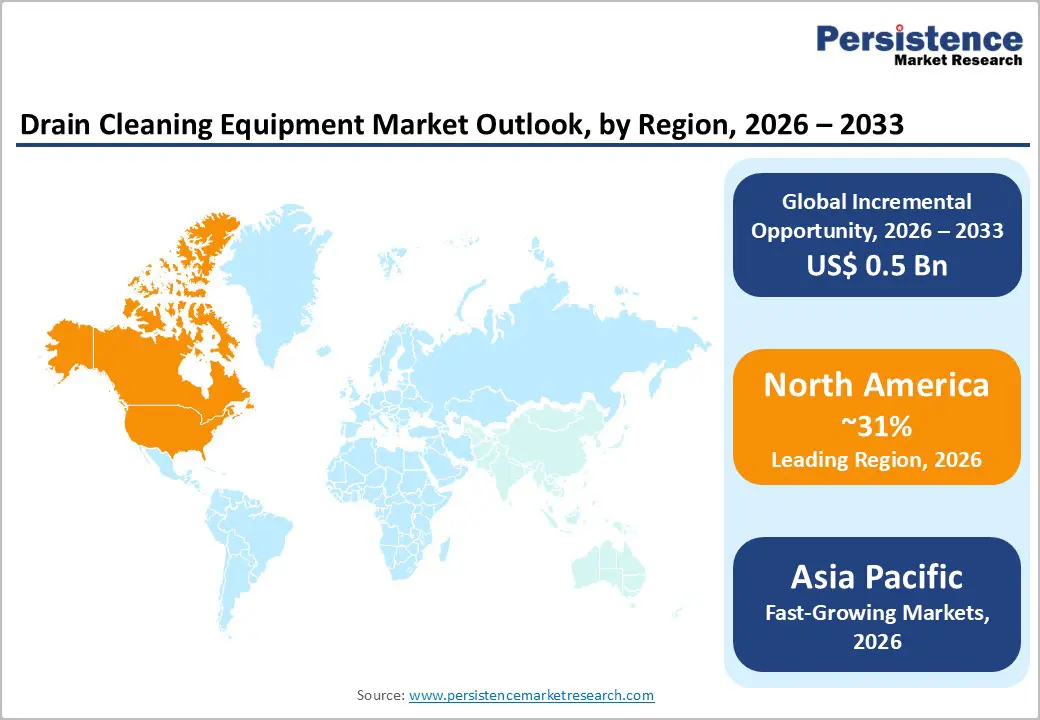

- Leading Region: North America maintains established market leadership, holding around 31% share, driven by aging infrastructure requiring systematic maintenance, stringent environmental regulations, and substantial government investment in municipal drainage system modernization supporting sustained equipment demand.

- Fastest Growing Region: Asia-Pacific experiences the fastest regional growth with a rising CAGR of 7.1%, supported by rapid urbanization, municipal infrastructure investment, and Smart Cities Mission mandates requiring professional drain cleaning equipment across expanding urban centers.

- Leading Segment: Power tools command 63% market share, driven by superior performance tackling complex blockages, including tree roots and mineral buildup that hand tools cannot effectively resolve, supporting widespread adoption across municipal, residential, and industrial applications.

- Fastest-Growing Segment: Water jetter segments experience the fastest growth, driven by 80% efficiency improvement versus traditional methods, environmental sustainability advantages, and increasing municipal and commercial adoption supporting premium equipment penetration.

| Key Insights | Details |

|---|---|

| Drain Cleaning Equipment Market Size (2026E) | US$ 1.1 Bn |

| Market Value Forecast (2033F) | US$ 1.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Drivers - Advanced Drain Cleaning Technologies Driving Efficiency, Sustainability, and Data-Driven Service Models Across Global Markets

Advanced drain cleaning technologies are steadily reshaping market dynamics as municipalities and service providers recognize clear efficiency, cost, and environmental benefits over traditional methods. High-pressure water jetting systems can improve cleaning efficiency by up to 80% and reduce service time by nearly 30%, enabling operators to complete more jobs and enhance profitability. These systems also eliminate the need for harsh chemical cleaners, aligning strongly with environmental regulations and corporate sustainability goals.

Adoption of CCTV inspection systems, robotic drain cleaners, and automated pipe inspection tools is increasing, enabling precise identification of blockage type and location before cleaning begins. This reduces repeat visits, minimizes unnecessary work, and improves service accuracy. The industry is shifting from reactive maintenance toward proactive, data-driven operations, enabling service providers to offer premium solutions. These advanced capabilities support competitive differentiation and higher-margin service offerings across residential, commercial, and municipal applications.

Rising Government Infrastructure Spending and Mandatory Drainage Maintenance Programs Creating Stable Long-Term Market Demand

Governments worldwide are significantly increasing investments in drainage infrastructure maintenance to address aging sewer systems and prevent environmental damage. Municipal applications account for approximately 35.2% of the global share, driven by mandatory maintenance programs and strict wastewater discharge regulations. In the United States, many sewer and water networks built 50 to 100 years ago now require systematic upgrades, driving consistent demand for professional drain cleaning equipment.

India’s Smart Cities Mission mandates improvements in sanitation, water treatment, and waste management, thereby accelerating public-sector procurement of modern drain-cleaning solutions. China continues to expand drainage systems across rapidly urbanizing regions, accounting for 17.2% of global market revenue and projected to achieve a 7.8% CAGR through 2035. These government mandates create stable, recurring demand for reliable drain cleaning equipment, ensuring long-term market growth that remains resilient even during economic slowdowns.

Restraints - High Capital Costs and Ownership Expenses Limiting Advanced Drain Cleaning Equipment Adoption Among Small Operators

High upfront costs for advanced drain-cleaning equipment remain a major barrier, particularly for small contractors and operators in emerging economies. Sophisticated systems such as high-pressure water jetters, sectional machines, and CCTV inspection tools are significantly more expensive than basic hand tools, limiting adoption in price-sensitive markets. In regions such as India, Southeast Asia, and Latin America, equipment use is often limited to large municipal bodies and commercial enterprises due to affordability constraints.

Limited awareness about long-term efficiency and cost benefits further constrains demand among smaller users. In addition, advanced systems require ongoing maintenance, operator training, and access to specialized spare parts, increasing total ownership costs. These financial and operational challenges discourage budget-conscious buyers, slowing technology penetration and preventing the market from reaching its full potential in high-growth developing regions.

Environmental Compliance Pressures and Low-Cost Chemical Alternatives Restricting Equipment-Based Drain Cleaning Growth

Strict environmental regulations governing wastewater disposal, chemical usage, and pollution control are increasing compliance costs for drain cleaning service providers. While these regulations encourage sustainable practices, they also raise operational complexity and investment requirements. At the same time, low-cost chemical drain cleaners continue to compete with equipment-based solutions, particularly in residential and small commercial segments.

Many consumers remain unaware of the environmental and health risks associated with chemical cleaners, limiting the shift toward mechanical alternatives. Additionally, growing emphasis on sustainable manufacturing and circular economy principles is pushing equipment manufacturers to invest heavily in eco-friendly materials, energy-efficient designs, and cleaner production processes. These investments increase research and development costs and extend product development timelines. Together, regulatory pressure and competition among chemical products create challenges that can slow equipment adoption despite long-term sustainability benefits.

Opportunities - Smart Drainage Systems Using IoT and Predictive Analytics: Unlocking Preventive Maintenance and Premium Service Opportunities

The integration of IoT, artificial intelligence, and predictive analytics into drain cleaning equipment presents a strong growth opportunity for the market. Smart drainage systems equipped with sensors and real-time monitoring capabilities allow operators to detect potential blockages before major failures occur. This enables scheduled preventive maintenance, reducing emergency repairs and lowering long-term operating costs.

Cloud-connected systems collect valuable data on blockage patterns, pipe conditions, seasonal trends, and equipment performance. This data supports better decision-making, optimized maintenance schedules, and efficient resource allocation.

Municipal authorities and large facility managers increasingly prefer these intelligent solutions to improve system reliability and operational transparency. Equipment providers offering smart, connected drainage solutions can deliver premium value propositions and long-term service contracts, positioning themselves as strategic partners rather than basic equipment suppliers.

Rental and Subscription-Based Equipment Models Improving Accessibility, Flexibility, and Cost Management for Service Providers

The growing adoption of rental and subscription-based business models is creating new opportunities in the drain cleaning equipment market. These models allow service providers to access advanced equipment without large upfront investments, making high-performance tools more affordable. Monthly or annual subscription fees align better with operating budgets and improve cash flow management, particularly for small and mid-sized operators.

Rental services are especially attractive for seasonal demand patterns, enabling access during peak periods without long-term ownership costs. Municipal bodies, commercial facility managers, and fleet operators increasingly prefer rental solutions for flexibility and reduced capital expenditure.

Equipment manufacturers and distributors benefit from recurring revenue streams and higher customer engagement. In parallel, the expansion of e-commerce and direct-to-consumer platforms is improving accessibility for residential and small commercial users, supporting broader market penetration.

Category-wise Analysis

Product Type Insights

Power tools account for approximately 63% share due to their superior performance in handling complex and stubborn drain blockages. Equipment such as electric drain augers, drum machines, sectional cable systems, and high-pressure water jetters effectively removes grease, mineral buildup, debris, and tree roots across residential, commercial, and industrial applications.

Water jetting machines represent the fastest-growing segment, supported by high cleaning efficiency, chemical-free operation, and increasing adoption by municipalities and commercial facilities.

Sectional machines offer modular flexibility, allowing operators to adapt to different pipe sizes and layouts, enhancing versatility. Despite technological advances, hand tools continue to maintain steady demand among residential users and small contractors who prioritize affordability, simplicity, and portability. Together, these product segments ensure balanced demand across both advanced and entry-level market tiers.

Sales Channel Insights

Distributor channels dominate the market with approximately 55% share, serving professional contractors through specialized supply networks that provide technical guidance, demonstrations, and after-sales support. Retail outlets account for around 30% of demand, catering mainly to residential customers and small businesses through hardware stores and home improvement centers.

Online sales channels are the fastest-growing segment, expanding at an annual rate of 10%, driven by e-commerce growth, digital payment adoption, and direct manufacturer-to-consumer strategies. Online platforms enable broader geographic reach, transparent pricing, and easy product comparison, particularly appealing to residential users.

Digital channels are also helping manufacturers reduce dependency on intermediaries while improving customer engagement. The combination of traditional distribution strength and rapidly expanding digital channels is reshaping the overall sales landscape.

Industry Insights

Municipal applications lead the market with approximately 35.2% share, supported by mandatory drainage maintenance, regulatory compliance, and stable government funding. Residential users represent roughly 25% of demand, driven by routine household maintenance and increasing awareness of hygienic living environments. Industrial segments show strong growth, particularly in food processing, beverage production, pharmaceuticals, and hospitality, where regular drain cleaning is essential for operational efficiency and regulatory compliance.

Commercial facilities such as hospitals, hotels, office complexes, and shopping centers also generate consistent demand to maintain occupant comfort and safety. Across all end-use sectors, the growing emphasis on preventive maintenance and system reliability is driving steady adoption of professional drain-cleaning equipment and services.

Regional Insights

North America Drain Cleaning Equipment Market Trends

North America remains a leading market due to aging infrastructure, strong purchasing power, and established professional service networks. The United States drives regional demand through extensive sewer and water systems installed between the 1950s and 1980s that now require continuous maintenance. Major cities such as New York, Los Angeles, Chicago, and Boston are investing heavily in infrastructure renewal programs to prevent system failures and environmental contamination.

Demand is particularly strong for high-performance water jetting systems, CCTV inspection tools, and sectional machines. Strict environmental and public health regulations further support consistent investment in professional drain cleaning solutions. These factors ensure stable demand across economic cycles and encourage manufacturers to focus on advanced, premium equipment offerings.

Europe Drain Cleaning Equipment Market Trends

European markets emphasize sustainability, environmental compliance, and occupant health, driving the adoption of chemical-free and energy-efficient drain cleaning technologies. Countries such as Germany, the UK, France, and Spain benefit from strong industrial, healthcare, and hospitality sectors requiring regular drainage maintenance. Industrial drain cleaning equipment in Europe was valued at over US$ 184.5 million in 2023, with Germany and France leading demand.

Strict EU regulations on wastewater discharge and chemical usage compel operators to adopt advanced mechanical cleaning solutions. European buyers show a strong preference for premium, technologically advanced equipment offering durability and compliance. This supports demand for water jetting systems, automated inspection tools, and sensor-enabled solutions, creating opportunities for manufacturers focused on innovation and sustainability.

Asia Pacific Drain Cleaning Equipment Market Trends

Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, expanding middle-class populations, and large-scale infrastructure development. China leads the region with 17.2% global market share and strong growth supported by continuous urban expansion and municipal investment. India is experiencing robust growth at a 7.1%CAGR, driven by the Smart Cities Mission and sanitation-focused government initiatives.

Domestic manufacturing programs such as “Make in India” are helping reduce equipment costs and improve accessibility. Japan remains a technology leader, focusing on precision engineering and environmentally sustainable designs. Rapid development across Southeast Asian countries is further increasing demand, creating strong opportunities for manufacturers with localized products and regional distribution strategies.

Competitive Landscape

The global drain cleaning equipment market is moderately consolidated, with established players holding strong positions alongside regional specialists. Leading manufacturers such as Ridgid, General Wire Spring, Spartan Tools, Electric Eel, and Rothenberger collectively account for nearly 40% of global market share. These companies benefit from broad product portfolios, strong brand recognition, and extensive distribution networks.

Mid-tier players contribute an additional 20% share through regional expertise and niche technologies. Competitive differentiation increasingly focuses on water jetting efficiency, CCTV integration, IoT connectivity, and eco-friendly designs. Continuous investment in research and development is essential for maintaining market leadership as customer expectations evolve toward smarter, more sustainable drainage solutions.

Key Developments:

- In November 2024: Ridgid Inc. launched an IoT-enabled smart drain cleaning platform featuring real-time monitoring and predictive maintenance analytics. The solution helps service providers optimize equipment utilization, minimize unplanned downtime, and improve operational efficiency through data-driven insights.

- In August 2024: Spartan Tools LLC expanded its rental and subscription offerings to improve access to professional drain cleaning equipment. The initiative enables small contractors and municipal operators to reduce capital expenditure while maintaining operational flexibility and managing seasonal demand fluctuations effectively.

- In April 2024: ROTHENBERGER Werkzeuge GmbH announced the development of AI-powered, eco-friendly drain cleaning systems combining automated blockage detection with high-pressure water jetting, supporting chemical-free operations and aligning with global sustainability and environmental compliance requirements.

Companies Covered in Drain Cleaning Equipment Market

- Ridgid Inc.

- General Wire Spring Co.

- Spartan Tools LLC

- Electric Eel Manufacturing Co Inc.

- ROTHENBERGER Werkzeuge GmbH

- Mosco Corp.

- GT Water Product Inc.

- Gorlitz Sewer & Drain Inc.

- Duracable Manufacturing Co.

- Goodway Technologies Corp.

- Rioned UK Ltd.

- Kam-Avida Enviro Engineers Pvt. Ltd.

- Asada Corporation

- Lavelle Industries, Inc.

- Albert Roller GmbH & Co KG

- Milwaukee Tool

- Vactor Manufacturing

- General Pipe Cleaners

Frequently Asked Questions

The market is projected to reach US$ 1.6 billion by 2033, growing at a 5.8% CAGR from 2026, driven by urbanization, infrastructure aging, and sanitation investments.

Key drivers include municipal infrastructure investment, high-efficiency technological advancements, and aging drainage systems requiring regular professional maintenance.

Power tools lead with about 63% market share, supported by superior performance in removing complex blockages across municipal, residential, and industrial applications.

North America lead in market share, while Asia-Pacific is the fastest-growing region driven by urbanization and government infrastructure programs.

Major opportunities include IoT-enabled smart drainage systems and rental or subscription models that reduce capital costs and improve equipment accessibility.

Leading players include Ridgid, General Wire Spring, Spartan Tools, Electric Eel, and ROTHENBERGER, supported by strong portfolios and global distribution networks.